You might also like

- MC - Exercises On Donor's Tax (PRTC)Document12 pagesMC - Exercises On Donor's Tax (PRTC)Anna Charlotte50% (4)

- Other Percentage TaxDocument3 pagesOther Percentage TaxHafi DisoNo ratings yet

- Donor's Tax and Foreign Tax Credit (Presentation Slides)Document5 pagesDonor's Tax and Foreign Tax Credit (Presentation Slides)Kez100% (1)

- Chapter 4 Exempt SalesDocument23 pagesChapter 4 Exempt SalesHazel Jane Esclamada0% (2)

- Chapter 4 Exempt SalesDocument23 pagesChapter 4 Exempt SalesHazel Jane Esclamada0% (2)

- Donor's Tax: Answer: DDocument6 pagesDonor's Tax: Answer: DAngela Miles DizonNo ratings yet

- Gross Estate of Married Decedent: Marriage SettlementDocument10 pagesGross Estate of Married Decedent: Marriage SettlementSheryl Paja100% (1)

- Donor's Tax Post QuizDocument12 pagesDonor's Tax Post QuizMichael Aquino0% (1)

- Chapter 17 Donor's TaxDocument7 pagesChapter 17 Donor's TaxHazel Jane Esclamada100% (3)

- Estate Tax - ProblemsDocument6 pagesEstate Tax - ProblemsKenneth Bryan Tegerero Tegio100% (2)

- Module 1 - Deductions From Gross EstateDocument68 pagesModule 1 - Deductions From Gross EstateKat Miranda100% (1)

- This Study Resource Was: Midterm-Final Exam Aec 215 - Business TaxationDocument8 pagesThis Study Resource Was: Midterm-Final Exam Aec 215 - Business TaxationGray JavierNo ratings yet

- Acco 20173 Quiz 1Document7 pagesAcco 20173 Quiz 1Lyra EscosioNo ratings yet

- Practice Exercises: Donor'S TaxDocument37 pagesPractice Exercises: Donor'S TaxErica NicolasuraNo ratings yet

- Estate Tax NotesDocument13 pagesEstate Tax NotesDonFrascoNo ratings yet

- Quiz 1 - Estate TaxDocument7 pagesQuiz 1 - Estate TaxKevin James Sedurifa Oledan100% (4)

- Tax Reviewer - Donor'sDocument3 pagesTax Reviewer - Donor'sNicole Autriz100% (1)

- Course Financial Management Developer and Their Background: See Assignment / Agreement SectionDocument33 pagesCourse Financial Management Developer and Their Background: See Assignment / Agreement SectionHazel Jane Esclamada100% (1)

- Chapter 17 Donor's TaxDocument7 pagesChapter 17 Donor's TaxHazel Jane Esclamada100% (3)

- Chapter 9 Input VatDocument10 pagesChapter 9 Input VatHazel Jane EsclamadaNo ratings yet

- Chapter 3 Introduction To Business TaxationDocument27 pagesChapter 3 Introduction To Business TaxationHazel Jane Esclamada100% (1)

- Chapter 10 Vat Still DueDocument7 pagesChapter 10 Vat Still DueHazel Jane EsclamadaNo ratings yet

- Questionnaire For Consumer Perception in Investment in ULIP and Mutual FundDocument4 pagesQuestionnaire For Consumer Perception in Investment in ULIP and Mutual Fundrahul_jayaswal80% (10)

- Estate TaxDocument9 pagesEstate TaxHafi DisoNo ratings yet

- Deductions From The Gross Estate Supplementary Pro 230712 100820Document8 pagesDeductions From The Gross Estate Supplementary Pro 230712 100820nichNo ratings yet

- Exercises On Estate Tax Additional ProblemsDocument8 pagesExercises On Estate Tax Additional ProblemsMidas Troy VictorNo ratings yet

- Solutions To Problems: Pe On Estate TaxDocument11 pagesSolutions To Problems: Pe On Estate TaxErica NicolasuraNo ratings yet

- Deductions From Gross EstateDocument20 pagesDeductions From Gross EstateJamaica David100% (2)

- Concept of Succession and Estate Tax and Gross Estate Common Rules & Special Rules (Married Decedents)Document12 pagesConcept of Succession and Estate Tax and Gross Estate Common Rules & Special Rules (Married Decedents)Hazel Jane Esclamada100% (1)

- Estate Taxation - Discussions...............Document5 pagesEstate Taxation - Discussions...............jangjangNo ratings yet

- CHAPTER 7 Conjugal PartnershipDocument15 pagesCHAPTER 7 Conjugal PartnershipClaire BarbaNo ratings yet

- Estate Tax Practice Set With AnswersDocument6 pagesEstate Tax Practice Set With AnswersXin ZhaoNo ratings yet

- Tax QuizDocument12 pagesTax QuizJamaica DavidNo ratings yet

- Cpa Reviewer in TaxationDocument34 pagesCpa Reviewer in TaxationMika MolinaNo ratings yet

- Tax2 DQ4Document17 pagesTax2 DQ4Kurt dela Torre100% (1)

- Quiz 2 Tax 2 Answer KeyDocument10 pagesQuiz 2 Tax 2 Answer KeyJamaica DavidNo ratings yet

- Computation of Net Taxable Estate & Estate Tax Due If Decedent Was Married With Surviving SpouseDocument1 pageComputation of Net Taxable Estate & Estate Tax Due If Decedent Was Married With Surviving SpouseanneNo ratings yet

- Chapter 3 ExercisesDocument5 pagesChapter 3 Exercisesdennilyn recaldeNo ratings yet

- ModuleDocument6 pagesModuledennissabalberinojrNo ratings yet

- Compilation of MCQDocument34 pagesCompilation of MCQDaphnie Bolo100% (1)

- Introduction To Donor's TaxDocument7 pagesIntroduction To Donor's TaxHazel Jane EsclamadaNo ratings yet

- Tax 04 10 Estate TaxationDocument9 pagesTax 04 10 Estate TaxationLab Dema-alaNo ratings yet

- True or False 1Document13 pagesTrue or False 1Mary DenizeNo ratings yet

- Reviewer For Final Examination - ProblemsDocument11 pagesReviewer For Final Examination - Problemsreynald animosNo ratings yet

- Tax Review (Taxrev) BSA 4th Year (Saturday, 8:00AM - 11:00AM) I - Multiple ChoiceDocument8 pagesTax Review (Taxrev) BSA 4th Year (Saturday, 8:00AM - 11:00AM) I - Multiple ChoiceDavidson Galvez0% (1)

- TAX-101 (Estate Tax)Document11 pagesTAX-101 (Estate Tax)Edith DalidaNo ratings yet

- Computation Gross EstateDocument6 pagesComputation Gross Estatemusic lyricsNo ratings yet

- Chapter 15 - Estate Tax Payable: Multiple Choice - TheoryDocument12 pagesChapter 15 - Estate Tax Payable: Multiple Choice - TheorytruthNo ratings yet

- Business Tax 4Document24 pagesBusiness Tax 4Cheska AtienzaNo ratings yet

- Output TaxDocument15 pagesOutput TaxAmie Jane MirandaNo ratings yet

- Foreign Tax CreditDocument2 pagesForeign Tax CreditSophiaFrancescaEspinosaNo ratings yet

- Tax 1 Activity (Soriano Book)Document18 pagesTax 1 Activity (Soriano Book)Sara Andrea SantiagoNo ratings yet

- Quizzers On Percentage TaxationDocument10 pagesQuizzers On Percentage Taxation?????No ratings yet

- Tax Review Overview Vat and Opt QuizDocument4 pagesTax Review Overview Vat and Opt QuizYochabel Eureca BorjeNo ratings yet

- Gross EstateDocument11 pagesGross EstateBiboy GSNo ratings yet

- Arturo Died Leaving The Following PropertiesDocument1 pageArturo Died Leaving The Following PropertiesCristine Salvacion PamatianNo ratings yet

- Tax 3216Document5 pagesTax 3216Rich William PagaduanNo ratings yet

- Tax2 Quiz2 FinalsDocument11 pagesTax2 Quiz2 Finalsishinoya keishiNo ratings yet

- VAT-Computation 2Document28 pagesVAT-Computation 2Alvin Dagohoy100% (1)

- Exercise No. 1-Estate TaxationDocument4 pagesExercise No. 1-Estate TaxationRed Velvet100% (1)

- Dynasty Corporation 2019 2019 2019 Phils. China TotalDocument17 pagesDynasty Corporation 2019 2019 2019 Phils. China TotalAngela RuedasNo ratings yet

- Chapter 6 Deductions From The Gross Estate PDFDocument7 pagesChapter 6 Deductions From The Gross Estate PDFDudz MatienzoNo ratings yet

- Accountancy Review Center (ARC) of The Philippines Inc.: Student HandoutsDocument6 pagesAccountancy Review Center (ARC) of The Philippines Inc.: Student HandoutsJaneNo ratings yet

- Chapter 4Document18 pagesChapter 4christineNo ratings yet

- Determination of The Net Taxable Estate Illustration 1: Single Resident or Citizen DecedentDocument14 pagesDetermination of The Net Taxable Estate Illustration 1: Single Resident or Citizen DecedentLea ChermarnNo ratings yet

- TAXATION 2 Chapter 5 Estate Tax Payable PDFDocument5 pagesTAXATION 2 Chapter 5 Estate Tax Payable PDFKim Cristian MaañoNo ratings yet

- Problem 1: Net Taxable Estate 530,000 75,000 605,000Document3 pagesProblem 1: Net Taxable Estate 530,000 75,000 605,000camscamsNo ratings yet

- Photography 3 (Updated)Document28 pagesPhotography 3 (Updated)Hazel Jane EsclamadaNo ratings yet

- Report - Roles of CEODocument2 pagesReport - Roles of CEOHazel Jane EsclamadaNo ratings yet

- Photography 2Document48 pagesPhotography 2Hazel Jane EsclamadaNo ratings yet

- Introduction To Financial ManagementDocument43 pagesIntroduction To Financial ManagementHazel Jane EsclamadaNo ratings yet

- MAS-3-Roque - Answer KeyDocument6 pagesMAS-3-Roque - Answer KeyHazel Jane Esclamada100% (1)

- Topic 3 & 4 - EXERCISES3 - Working Capital Management - TheoriesDocument36 pagesTopic 3 & 4 - EXERCISES3 - Working Capital Management - TheoriesHazel Jane EsclamadaNo ratings yet

- Introduction To Donor's TaxDocument7 pagesIntroduction To Donor's TaxHazel Jane EsclamadaNo ratings yet

- Inventory Management: Multiple Choice QuestionsDocument3 pagesInventory Management: Multiple Choice QuestionsHazel Jane Esclamada33% (3)

- Mas 3 Module 1 Fs AnalysisDocument19 pagesMas 3 Module 1 Fs AnalysisHazel Jane EsclamadaNo ratings yet

- Working Capital FinanceDocument12 pagesWorking Capital FinanceYeoh Mae100% (4)

- Topic 4 - EXERCISES6 - Capital Current Liabilities ManagementDocument36 pagesTopic 4 - EXERCISES6 - Capital Current Liabilities ManagementHazel Jane Esclamada100% (1)

- Concept of Succession and Estate Tax and Gross Estate Common Rules & Special Rules (Married Decedents)Document12 pagesConcept of Succession and Estate Tax and Gross Estate Common Rules & Special Rules (Married Decedents)Hazel Jane Esclamada100% (1)

- Warranties, Provisions and Contingent LiabilitiesDocument31 pagesWarranties, Provisions and Contingent LiabilitiesHazel Jane EsclamadaNo ratings yet

- What To Do With Perceived Environmental ViolationsDocument15 pagesWhat To Do With Perceived Environmental ViolationsHazel Jane EsclamadaNo ratings yet

- Reclassification: of Financial AssetsDocument15 pagesReclassification: of Financial AssetsHazel Jane EsclamadaNo ratings yet

- Module Far1 Unit-1 Part-1bDocument5 pagesModule Far1 Unit-1 Part-1bHazel Jane EsclamadaNo ratings yet

- Module Far1 Unit-1 Part-1c.1Document6 pagesModule Far1 Unit-1 Part-1c.1Hazel Jane EsclamadaNo ratings yet

- Module 2.1 (Property, Plant, and Equipment)Document15 pagesModule 2.1 (Property, Plant, and Equipment)Hazel Jane EsclamadaNo ratings yet

- Introduction To Transfer TaxationDocument6 pagesIntroduction To Transfer TaxationHazel Jane EsclamadaNo ratings yet

- TSU PNP New Rank Classification The Meaning of The Symbols in The Seal and Badge of The PNPDocument3 pagesTSU PNP New Rank Classification The Meaning of The Symbols in The Seal and Badge of The PNPHazel Jane EsclamadaNo ratings yet

- MODULE FinalTerm FAR 3 Operating Segment Interim Reporting Events After Reporting Period 1Document19 pagesMODULE FinalTerm FAR 3 Operating Segment Interim Reporting Events After Reporting Period 1Hazel Jane Esclamada0% (1)

- Topic 7 Transfer PricingDocument3 pagesTopic 7 Transfer PricingHazel Jane EsclamadaNo ratings yet

- Chapter 1 Tax 2Document5 pagesChapter 1 Tax 2Hazel Jane EsclamadaNo ratings yet

- Topic 4 - Current Liabilities Sample ProblemsDocument8 pagesTopic 4 - Current Liabilities Sample ProblemsHazel Jane EsclamadaNo ratings yet

- Perancangan Model Data Warehouse Dan Perangkat Analitik Untuk Memaksimalkan Proses Pemasaran Hotel: Studi Kasus Pada Hotel AbcDocument10 pagesPerancangan Model Data Warehouse Dan Perangkat Analitik Untuk Memaksimalkan Proses Pemasaran Hotel: Studi Kasus Pada Hotel Abcfaisal zafryNo ratings yet

- FinMar SemiDocument3 pagesFinMar SemiJoy CastillonNo ratings yet

- Joyalukkas DRHPDocument357 pagesJoyalukkas DRHPஅன்பே சிவாNo ratings yet

- Public Reports Pack 22062021 1400 Growth Infrastructure and Planning Cabinet PanelDocument298 pagesPublic Reports Pack 22062021 1400 Growth Infrastructure and Planning Cabinet Panelakk76No ratings yet

- Class 12 - Payout Policy - 1Document1 pageClass 12 - Payout Policy - 1Stepan MaykovNo ratings yet

- An Assesment of Cash Management Practice in Commercial Bank of EthiopiaDocument2 pagesAn Assesment of Cash Management Practice in Commercial Bank of EthiopiaSolomon Abebe100% (25)

- Challenges Faced by Microfinance InstitutionsDocument20 pagesChallenges Faced by Microfinance InstitutionsPrince Kumar Singh100% (2)

- WEF Forging New Pathways 2020Document207 pagesWEF Forging New Pathways 2020marciosalesdf-1No ratings yet

- Ebook - Financial Statements of Not-for-Profit OrganizationsDocument38 pagesEbook - Financial Statements of Not-for-Profit OrganizationsRahulNo ratings yet

- 52 Metrobank v. CIRDocument1 page52 Metrobank v. CIRNN DDLNo ratings yet

- Bhavana ResumeDocument3 pagesBhavana ResumechanikyaNo ratings yet

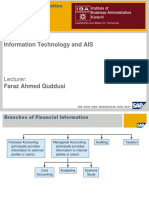

- Role of AISDocument20 pagesRole of AISFaraz Ahmed QuddusiNo ratings yet

- RegaloDocument3 pagesRegaloVia ExpoNo ratings yet

- S&P - High-Yield Bond Market PrimerDocument8 pagesS&P - High-Yield Bond Market Primerlady_raistlynNo ratings yet

- Jensen Margaret Ann PDFDocument412 pagesJensen Margaret Ann PDFsahibakhurana12No ratings yet

- Municipality of Santa Cruz, Davao Del SurDocument19 pagesMunicipality of Santa Cruz, Davao Del SurAer AsedoNo ratings yet

- Economics: Number Key Number Key Number KeyDocument11 pagesEconomics: Number Key Number Key Number KeySilenceNo ratings yet

- Business Project ReportDocument3 pagesBusiness Project ReportNelson NofantaNo ratings yet

- Job Order Assignment PDFDocument3 pagesJob Order Assignment PDFAnne Marie100% (1)

- 2016-12 ICMAB FL 001 PAC Year Question December 2016Document3 pages2016-12 ICMAB FL 001 PAC Year Question December 2016Mohammad ShahidNo ratings yet

- Math 112 Final ExamDocument1 pageMath 112 Final ExamMildred MuzonesNo ratings yet

- Assignment Strategic SCMDocument20 pagesAssignment Strategic SCMWillem Jacobus CoetseeNo ratings yet

- Accounting 101 Chapter 2Document11 pagesAccounting 101 Chapter 2Kriss AnnNo ratings yet

- Jharkhand World BanK ReportDocument148 pagesJharkhand World BanK ReportJitendra NayakNo ratings yet

- Gail Omvedt - Reinventing Revolution - New Social Movements and The Socialist Tradition in India-Routledge (1993)Document24 pagesGail Omvedt - Reinventing Revolution - New Social Movements and The Socialist Tradition in India-Routledge (1993)Lishi DodumNo ratings yet

- Zarra Supply Chain Management ProjectDocument16 pagesZarra Supply Chain Management ProjectSaif KhanNo ratings yet

- BOI FAQs QA 01.12.2024Document38 pagesBOI FAQs QA 01.12.2024abhishek.vynNo ratings yet

- Accounts Nitin SirDocument11 pagesAccounts Nitin Sirpuneet.sharma1493No ratings yet

- Bank Account StatementDocument11 pagesBank Account StatementJohn SmitNo ratings yet