You might also like

- Indian Textile Industry: Yarn, Cloth, Fabrics, and Other Products Not Made Into GarmentsDocument24 pagesIndian Textile Industry: Yarn, Cloth, Fabrics, and Other Products Not Made Into GarmentsUrvashi SinghNo ratings yet

- International Trade NishantDocument28 pagesInternational Trade Nishantnishant kumarNo ratings yet

- The Multifibre AgreementDocument40 pagesThe Multifibre AgreementVarun MehrotraNo ratings yet

- 1246 4675 1 PBDocument40 pages1246 4675 1 PBkashNo ratings yet

- Kesavan SIP NewDocument43 pagesKesavan SIP NewRohitNo ratings yet

- Porter Five Forces AnalysisDocument40 pagesPorter Five Forces AnalysisNimesh Gunasekera100% (1)

- CIPS Level 5 - AD3 May14 Pre ReleaseDocument15 pagesCIPS Level 5 - AD3 May14 Pre ReleaseNyeko Francis100% (1)

- Textiles and ClothingDocument3 pagesTextiles and ClothingAli IshfaqNo ratings yet

- Manage-A Comparative Analysis of Indo-Eu Textiles Trade-Asiya ChaudharyDocument12 pagesManage-A Comparative Analysis of Indo-Eu Textiles Trade-Asiya ChaudharyImpact JournalsNo ratings yet

- Subject: International Trade Law: Chanakya National Law University, PatnaDocument25 pagesSubject: International Trade Law: Chanakya National Law University, PatnaAmit DipankarNo ratings yet

- Status of The Textile Industry in Kenya:global, Regional and National Perspectives 1997Document37 pagesStatus of The Textile Industry in Kenya:global, Regional and National Perspectives 1997Geoffrey Koech50% (2)

- MPRA Paper 88112 PDFDocument31 pagesMPRA Paper 88112 PDFaryanNo ratings yet

- Term Paper On: Wto and Singapore Textile IndustryDocument23 pagesTerm Paper On: Wto and Singapore Textile IndustryAvinash KumarNo ratings yet

- Indian Textile IndustryDocument62 pagesIndian Textile IndustryAnkit Shah0% (1)

- Challenges Vietnam Garment IndustryDocument19 pagesChallenges Vietnam Garment IndustryGimhan GodawatteNo ratings yet

- Korean Soju DisputeDocument20 pagesKorean Soju Disputekrishna6941100% (1)

- Ready Made GarmentDocument5 pagesReady Made GarmentRajeev AttriNo ratings yet

- Market Systems Analysis of Working Conditions in AsiaDocument94 pagesMarket Systems Analysis of Working Conditions in AsiaarjmandqayyumNo ratings yet

- Dismantling Quota Restrictions (QR) in International Textile Trade - India S ResponseDocument12 pagesDismantling Quota Restrictions (QR) in International Textile Trade - India S ResponseDr. Bina Celine DorathyNo ratings yet

- A Study On Cash Management Anaiysis in Sri Angalaman Finance Limited Chapter-IDocument61 pagesA Study On Cash Management Anaiysis in Sri Angalaman Finance Limited Chapter-IJayaprabhu PrabhuNo ratings yet

- Growth Prospects For Indias Cotton and TDocument44 pagesGrowth Prospects For Indias Cotton and TYoume SinghNo ratings yet

- Phasing Out The Multi-Fibre Arrangement: Implications For IndiaDocument26 pagesPhasing Out The Multi-Fibre Arrangement: Implications For IndiaChirag DaveNo ratings yet

- Chapter - 1 An Overview of The IndustryDocument37 pagesChapter - 1 An Overview of The IndustryAdarsh MohanNo ratings yet

- Impact of WTO On Textile & Clothing IndustriesDocument14 pagesImpact of WTO On Textile & Clothing IndustriesAsjad JamshedNo ratings yet

- Disha CompanyDocument61 pagesDisha CompanyAmogh GuptaNo ratings yet

- Introduction of Intellectual Property Rights in India Chapter 1 Part 3Document10 pagesIntroduction of Intellectual Property Rights in India Chapter 1 Part 3NishantNo ratings yet

- Korean Soju DisputeDocument10 pagesKorean Soju DisputeAnuj KumarNo ratings yet

- Apparel Free Trade Agreements Between India and AustraliaDocument4 pagesApparel Free Trade Agreements Between India and AustraliaSmritiNo ratings yet

- Schaumburg Muller 3Document11 pagesSchaumburg Muller 3KARMA NEGINo ratings yet

- Business Ethics Final Report DraftDocument18 pagesBusiness Ethics Final Report DraftrabirizviNo ratings yet

- Market StructureDocument16 pagesMarket StructureKanchan SinghNo ratings yet

- Roject Work Antidumping MeasuresDocument20 pagesRoject Work Antidumping Measuresdevrudra07No ratings yet

- Project Report Garment SCMDocument10 pagesProject Report Garment SCMManpreet Singh KhuranaNo ratings yet

- International Trade Law ProjectDocument4 pagesInternational Trade Law ProjectAJITABH0% (1)

- PresentationDocument18 pagesPresentationSohanul Haque ShantoNo ratings yet

- Itl Project UjjawalDocument31 pagesItl Project UjjawalRaqesh Malviya100% (1)

- Chapter 1 IntroductionDocument29 pagesChapter 1 Introductionmarysruthyanto89No ratings yet

- Project Report - Garment - SCMDocument10 pagesProject Report - Garment - SCMRajeev SinghNo ratings yet

- The Global Textile and Clothing Industry Post TheDocument42 pagesThe Global Textile and Clothing Industry Post TheKirinnieNo ratings yet

- Indian Textile Industry in The Next Era-2004Document22 pagesIndian Textile Industry in The Next Era-2004abhishekthakur19No ratings yet

- MANIDocument78 pagesMANIPothumbu N P ManikandanNo ratings yet

- Alliance School of LawDocument16 pagesAlliance School of LawshariqueNo ratings yet

- Alliance School of LawDocument16 pagesAlliance School of LawshariqueNo ratings yet

- Indian Retail & Its Effect On Fashion Trend (MKTG)Document90 pagesIndian Retail & Its Effect On Fashion Trend (MKTG)Himanshu JoshiNo ratings yet

- National Law Institute University Kerwa Dam Road Bhopal: Ubmitted O Ubmitted Y ROF Aubhagya Hadkaria Ipul OhleDocument17 pagesNational Law Institute University Kerwa Dam Road Bhopal: Ubmitted O Ubmitted Y ROF Aubhagya Hadkaria Ipul OhleVicky DNo ratings yet

- From Obligation To Opportunity: A Market Systems Analysis of Working Conditions in Asia's Garment Export IndustryDocument55 pagesFrom Obligation To Opportunity: A Market Systems Analysis of Working Conditions in Asia's Garment Export IndustryLâm Ngọc HùngNo ratings yet

- ARTICLE XIII OF THE GATT AND THE Banana Dispute StudyDocument14 pagesARTICLE XIII OF THE GATT AND THE Banana Dispute StudySoumiki Ghosh100% (1)

- Execution Process of Garment Export Order Is One of The Principal Parts of The MerchandiserDocument32 pagesExecution Process of Garment Export Order Is One of The Principal Parts of The Merchandisersuruchi singhNo ratings yet

- Textile IndustryDocument41 pagesTextile IndustryPrasadNarayanB100% (1)

- Textiles-Garments and The Industrialization ProcessDocument15 pagesTextiles-Garments and The Industrialization ProcessNavaneethReddyNo ratings yet

- Oxfam GB, Taylor & Francis, Ltd. Development in PracticeDocument13 pagesOxfam GB, Taylor & Francis, Ltd. Development in PracticeManpreet Singh KhuranaNo ratings yet

- WTO On Textile Clothing IndustriesDocument14 pagesWTO On Textile Clothing IndustriesLaxman ZaggeNo ratings yet

- Dr. Ram Manohar Lohiya National Law University Lucknow 2016-2017Document19 pagesDr. Ram Manohar Lohiya National Law University Lucknow 2016-2017NidaFatimaNo ratings yet

- Export Process in FGMDocument78 pagesExport Process in FGMPothumbu N P ManikandanNo ratings yet

- Dr. Ram Manohar Lohiya National Law University, Lucknow: Project Topic-"1947 and WTO"Document14 pagesDr. Ram Manohar Lohiya National Law University, Lucknow: Project Topic-"1947 and WTO"Abhishek K. SinghNo ratings yet

- Critical Issues in The Garment Industry PDFDocument88 pagesCritical Issues in The Garment Industry PDFSneha Karpe100% (2)

- Last Nightshift in Savar: The Story of the Spectrum Sweater Factory CollapseFrom EverandLast Nightshift in Savar: The Story of the Spectrum Sweater Factory CollapseNo ratings yet

- Enviroment Law ProjectDocument21 pagesEnviroment Law Projectritu kumarNo ratings yet

- Chanakya Nationallaw University: ProjectDocument22 pagesChanakya Nationallaw University: Projectritu kumarNo ratings yet

- Chanakya Nationallaw University: ProjectDocument18 pagesChanakya Nationallaw University: Projectritu kumarNo ratings yet

- Chanakya National Law University: ProjectDocument22 pagesChanakya National Law University: Projectritu kumarNo ratings yet

- Chanakya National Law University ProjectDocument17 pagesChanakya National Law University Projectritu kumarNo ratings yet

- Chanakya National Law University ProjectDocument17 pagesChanakya National Law University Projectritu kumarNo ratings yet

- Enviroment Law ProjectDocument21 pagesEnviroment Law Projectritu kumarNo ratings yet

- Subject: Jurisprudence - Ii: Project TopicDocument25 pagesSubject: Jurisprudence - Ii: Project Topicritu kumarNo ratings yet

- Competition Law LLMDocument17 pagesCompetition Law LLMritu kumarNo ratings yet

- Competition Law LLMDocument17 pagesCompetition Law LLMritu kumarNo ratings yet

- Look East Policy and Act East Policy - A ComparisonDocument6 pagesLook East Policy and Act East Policy - A Comparisontiara kunderNo ratings yet

- Symbiosis Law School, Pune Course: Global Legal Skills: ST TH THDocument2 pagesSymbiosis Law School, Pune Course: Global Legal Skills: ST TH THUjjwal AnandNo ratings yet

- World Trade Organisation and Global Development 1Document11 pagesWorld Trade Organisation and Global Development 1Saakshi KhandelwalNo ratings yet

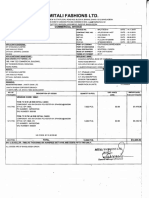

- '. Mitali Fashions LTDDocument11 pages'. Mitali Fashions LTDFaruque UddinNo ratings yet

- Tariff Day 01TLC - Orientation, Outline, References HANDOUT-1Document7 pagesTariff Day 01TLC - Orientation, Outline, References HANDOUT-1RBT BoysNo ratings yet

- ITC SME Trade Academy - Case Study Exercise (C093) - Attempt ReviewDocument27 pagesITC SME Trade Academy - Case Study Exercise (C093) - Attempt ReviewStevenNo ratings yet

- Application For Certificate of OriginDocument1 pageApplication For Certificate of OriginRajeev ChoubeyNo ratings yet

- Compensation For Indirect Expropriation in InternaDocument35 pagesCompensation For Indirect Expropriation in InternaAulia Nur RachmiNo ratings yet

- Ec Bed Linen CaseDocument8 pagesEc Bed Linen CaseAditya PandeyNo ratings yet

- 137 - Gatt, Gats, TripsDocument6 pages137 - Gatt, Gats, Tripsirma makharoblidze100% (1)

- Thesis Proposal On International TradeDocument6 pagesThesis Proposal On International Tradebsq5ek6t100% (2)

- Lesson 2 (Global Economy) - 1 PDFDocument43 pagesLesson 2 (Global Economy) - 1 PDFJervyn GuiananNo ratings yet

- IETP Tutorial 1 Group 1 PDFDocument12 pagesIETP Tutorial 1 Group 1 PDFPuteri Nelissa MilaniNo ratings yet

- A Broad Overview of Export Policy, Promotion and RegulationsDocument3 pagesA Broad Overview of Export Policy, Promotion and RegulationsGAURAV VIMALNo ratings yet

- Pn7-Rajesh Mehta-Textile & Apparel TradeDocument7 pagesPn7-Rajesh Mehta-Textile & Apparel TradeAnuj SinghNo ratings yet

- Thesis 1.5,1.5Document434 pagesThesis 1.5,1.5tayyaba redaNo ratings yet

- Ibo 1 em PDFDocument9 pagesIbo 1 em PDFFirdosh Khan70% (10)

- Post-Class Activities Week 2: Question 1Document20 pagesPost-Class Activities Week 2: Question 1Kim TuyếnNo ratings yet

- Voting Procedures Presentation by Muheki JonathanDocument23 pagesVoting Procedures Presentation by Muheki JonathanGumisiriza BrintonNo ratings yet

- Impact of WTO On Textile & Clothing IndustriesDocument14 pagesImpact of WTO On Textile & Clothing IndustriesAsjad JamshedNo ratings yet

- Naman Agrawal Mathur - Evaluation of Proposed RTAs of IndiDocument32 pagesNaman Agrawal Mathur - Evaluation of Proposed RTAs of IndiKatyayan Rajmeet UpadhyayNo ratings yet

- Easyparcel - Butik Rehlaizaa 2Document1 pageEasyparcel - Butik Rehlaizaa 2shahid 0208No ratings yet

- Dornbusch Fischer SamuelsonDocument18 pagesDornbusch Fischer SamuelsonBlanca MecinaNo ratings yet

- Sub - Technical VocabularyDocument20 pagesSub - Technical VocabularyFendi AchmadNo ratings yet

- MGT 9chap2Document6 pagesMGT 9chap2Anjelika ViescaNo ratings yet

- Lecture-6 - WTO Anti-Dumping MeasuresDocument2 pagesLecture-6 - WTO Anti-Dumping MeasuresRizky AuliaNo ratings yet

- Gatt/Wto: Academic TechnologiesDocument8 pagesGatt/Wto: Academic TechnologiesOliver TalipNo ratings yet

- Gebra Grup 4 Assignment LatestDocument7 pagesGebra Grup 4 Assignment LatestSALIM SHARIFUNo ratings yet

- Bosnia y HeerzgovinaDocument13 pagesBosnia y HeerzgovinaSantiago RamírezNo ratings yet

- WTO Assignment Bussiness LawDocument18 pagesWTO Assignment Bussiness LawAarav TripathiNo ratings yet