You might also like

- Special Commercial Laws CasesDocument162 pagesSpecial Commercial Laws CasesRoberto Suarez II100% (1)

- Quick Credit Reference Guide (DC17 - )Document12 pagesQuick Credit Reference Guide (DC17 - )Horace0% (1)

- SBA Loan SecretsDocument3 pagesSBA Loan SecretsPNWBizBrokerNo ratings yet

- BMO Business Checking: Important Account InformationDocument5 pagesBMO Business Checking: Important Account InformationSAM100% (2)

- VSA-IRS Obligations Part 1 ReviewDocument32 pagesVSA-IRS Obligations Part 1 ReviewjpbluejnNo ratings yet

- Citi Statment PDFDocument4 pagesCiti Statment PDFBERNARD KUSINo ratings yet

- Cash Flow Service Obligation Net Worth Assets Secure Debt EconomyDocument8 pagesCash Flow Service Obligation Net Worth Assets Secure Debt EconomypopatiaNo ratings yet

- Accounts Payble and Receivable.Document8 pagesAccounts Payble and Receivable.haris123786No ratings yet

- Understand Your Credit Report and ScoreDocument34 pagesUnderstand Your Credit Report and ScoreshalzadhawanNo ratings yet

- Bookkeeping: Learning The Simple And Effective Methods of Effective Methods Of Bookkeeping (Easy Way To Master The Art Of Bookkeeping)From EverandBookkeeping: Learning The Simple And Effective Methods of Effective Methods Of Bookkeeping (Easy Way To Master The Art Of Bookkeeping)No ratings yet

- False True True True TrueDocument16 pagesFalse True True True TrueArt B. EnriquezNo ratings yet

- Financing Options for Small BusinessesDocument6 pagesFinancing Options for Small BusinessesJo Angeli100% (2)

- Loan Discounts Finance 7Document41 pagesLoan Discounts Finance 7Elvie Anne Lucero ClaudNo ratings yet

- Definition of MoneyDocument5 pagesDefinition of MoneyM .U.KNo ratings yet

- Introduction To Debits and CreditsDocument12 pagesIntroduction To Debits and CreditskjvillNo ratings yet

- myIM3 6285727027131 201906Document3 pagesmyIM3 6285727027131 201906Irfan ArifinNo ratings yet

- Quiz 1Document11 pagesQuiz 1Art B. EnriquezNo ratings yet

- Financial Ratio AnalysisDocument47 pagesFinancial Ratio AnalysisUlash KhanNo ratings yet

- Why Men Disappear-Matthew-HusseyDocument1 pageWhy Men Disappear-Matthew-HusseyRochelle0% (3)

- 5 C'sof CreditDocument2 pages5 C'sof CreditarshhussainNo ratings yet

- Test Bank Law 1 CparDocument26 pagesTest Bank Law 1 CparJoyce Kay Azucena73% (22)

- Loans Payable DefinedDocument2 pagesLoans Payable DefinedHsin Wua ChiNo ratings yet

- Notes Payable vs Accounts Payable: Key DifferencesDocument3 pagesNotes Payable vs Accounts Payable: Key DifferencesEllaine Pearl AlmillaNo ratings yet

- How Are Notes Payable Different From Accounts Payable?Document3 pagesHow Are Notes Payable Different From Accounts Payable?Ellaine Pearl AlmillaNo ratings yet

- Accounts PayableDocument4 pagesAccounts PayableTina ParkNo ratings yet

- "Running Head:" Accounting For Current LiabilitiesDocument7 pages"Running Head:" Accounting For Current Liabilitieskeysha2009No ratings yet

- Liabilities ProjectDocument5 pagesLiabilities ProjectIslam HassanNo ratings yet

- What Are Accounts Receivable (AR) ?Document3 pagesWhat Are Accounts Receivable (AR) ?Sheila Mae AramanNo ratings yet

- Basic Accounting TermsDocument3 pagesBasic Accounting TermsAllyza VillapandoNo ratings yet

- Bookkeeping To Trial Balance 7Document10 pagesBookkeeping To Trial Balance 7elelwaniNo ratings yet

- Macro 2 Responses 125Document3 pagesMacro 2 Responses 125Ali RanjhaNo ratings yet

- What Are Accounts Payable (AP) ?Document3 pagesWhat Are Accounts Payable (AP) ?Art B. EnriquezNo ratings yet

- Working Capital $170,000 of Current Assets Minus $100,000 of Current Liabilities $70,000Document4 pagesWorking Capital $170,000 of Current Assets Minus $100,000 of Current Liabilities $70,000Linh ĐàmNo ratings yet

- What Is Accounts Payable (AP) ?: General LedgerDocument3 pagesWhat Is Accounts Payable (AP) ?: General LedgerDarlene SarcinoNo ratings yet

- Basis of Debit and CreditDocument17 pagesBasis of Debit and CreditBanaras KhanNo ratings yet

- What Is A Loan ReceivableDocument2 pagesWhat Is A Loan ReceivableArt B. EnriquezNo ratings yet

- What Is Accounts ReceivableDocument3 pagesWhat Is Accounts ReceivableHsin Wua ChiNo ratings yet

- Notes receivable allowance aging methodsDocument10 pagesNotes receivable allowance aging methodsppate110No ratings yet

- RulesDocument1 pageRulesArbab Usman KhanNo ratings yet

- Accounting 101 Chapter 7 - Accounts and Notes Receivable Prof. JohnsonDocument6 pagesAccounting 101 Chapter 7 - Accounts and Notes Receivable Prof. JohnsonbikilahussenNo ratings yet

- A Bad Debt Is An Account Receivable That Has Been Clearly Identified As Not Being Collectible Auto Saved)Document10 pagesA Bad Debt Is An Account Receivable That Has Been Clearly Identified As Not Being Collectible Auto Saved)Isa Joseph KabagheNo ratings yet

- Basic AccountingDocument23 pagesBasic AccountingEthan Manuel CarriedoNo ratings yet

- Cash and Cash Equivalents - Bank OverdraftsDocument3 pagesCash and Cash Equivalents - Bank OverdraftsjdhfiEWNo ratings yet

- Are Liabilities Always A Bad ThingDocument2 pagesAre Liabilities Always A Bad ThingSyed fayas thanveer SNo ratings yet

- Choose Between Loan or Shares When Starting a BusinessDocument19 pagesChoose Between Loan or Shares When Starting a BusinessChristian Nicolaus MbiseNo ratings yet

- Notes 08Document11 pagesNotes 08FantayNo ratings yet

- AA LiabilitiesDocument2 pagesAA LiabilitiesJoresol AlorroNo ratings yet

- What Is Accounts Receivable (AR) ?Document2 pagesWhat Is Accounts Receivable (AR) ?Art B. EnriquezNo ratings yet

- Fundamentals of Accountancy, Business, and Management 2: ExpectationDocument131 pagesFundamentals of Accountancy, Business, and Management 2: ExpectationAngela Garcia100% (1)

- H What Is ReconciliationDocument3 pagesH What Is ReconciliationDanica BalinasNo ratings yet

- Menagement of ReceiveableDocument5 pagesMenagement of ReceiveableMuhammad Furqan AkramNo ratings yet

- Credit AnalysisDocument3 pagesCredit Analysisjon_cpaNo ratings yet

- A AccrualsDocument4 pagesA AccrualsBetelehem ZenawNo ratings yet

- Can You Deduct Business Loans ExpensesDocument9 pagesCan You Deduct Business Loans ExpensesJulie Ann SisonNo ratings yet

- Financing ConceptsDocument5 pagesFinancing ConceptsSoothing BlendNo ratings yet

- The Barrington Guide to Property Management Accounting: The Definitive Guide for Property Owners, Managers, Accountants, and Bookkeepers to ThriveFrom EverandThe Barrington Guide to Property Management Accounting: The Definitive Guide for Property Owners, Managers, Accountants, and Bookkeepers to ThriveNo ratings yet

- Debit and Credit Are The Two Aspects of Every Financial TransactionDocument16 pagesDebit and Credit Are The Two Aspects of Every Financial TransactionPoseidon NipNo ratings yet

- Chapter 4 AccountingDocument22 pagesChapter 4 AccountingChan Man SeongNo ratings yet

- Complete FinanceDocument5 pagesComplete FinanceKappala AbhishekNo ratings yet

- Engineering EconomicsDocument12 pagesEngineering EconomicsAwais SiddiqueNo ratings yet

- How to Improve Your CIBIL Score in 6 StepsDocument4 pagesHow to Improve Your CIBIL Score in 6 StepssahilkuNo ratings yet

- Act 2100 LectureDocument39 pagesAct 2100 Lecturekeyanna gilletteNo ratings yet

- Financial Management HomeworkDocument33 pagesFinancial Management HomeworkShielaNo ratings yet

- Aid Lender Identify Risky Small Business LoansDocument5 pagesAid Lender Identify Risky Small Business LoansAbhay SharmaNo ratings yet

- Introduction To Debits and CreditsDocument16 pagesIntroduction To Debits and CreditsMeiRose100% (1)

- What Is FactoringDocument11 pagesWhat Is FactoringDimas HardiNo ratings yet

- Understanding Current AssetsDocument10 pagesUnderstanding Current AssetsnadeemNo ratings yet

- Loans Payable Defined: The Differences Between Accounts Payable & Bills PayableDocument2 pagesLoans Payable Defined: The Differences Between Accounts Payable & Bills PayableArt B. EnriquezNo ratings yet

- Official Hand SignalsDocument5 pagesOfficial Hand SignalsArt B. EnriquezNo ratings yet

- Starbucks InfosDocument18 pagesStarbucks InfosArt B. EnriquezNo ratings yet

- Heart Erica B. Abag 44188Document4 pagesHeart Erica B. Abag 44188Art B. EnriquezNo ratings yet

- What Is Accounts Receivable (AR) ?Document2 pagesWhat Is Accounts Receivable (AR) ?Art B. EnriquezNo ratings yet

- STATEMENT II: The Nullity Od The Penal Clause Carries With It The Nullity of The Principal ObligationDocument11 pagesSTATEMENT II: The Nullity Od The Penal Clause Carries With It The Nullity of The Principal ObligationCrizhae OconNo ratings yet

- What Is A Loan ReceivableDocument2 pagesWhat Is A Loan ReceivableArt B. EnriquezNo ratings yet

- What Are Accounts Payable (AP) ?Document3 pagesWhat Are Accounts Payable (AP) ?Art B. EnriquezNo ratings yet

- p1 Review With AnsDocument7 pagesp1 Review With AnsJiezelEstebeNo ratings yet

- What Are Notes ReceivableDocument2 pagesWhat Are Notes ReceivableArt B. EnriquezNo ratings yet

- Antiderivatives of Functions: Integral CalculusDocument4 pagesAntiderivatives of Functions: Integral CalculusArt B. EnriquezNo ratings yet

- Basic Volleyball Rules: How To Play VolleyballDocument2 pagesBasic Volleyball Rules: How To Play VolleyballArt B. EnriquezNo ratings yet

- Special Report: Vhong Navarro's Latest Investment Has Experts in Awe and Big Banks TerrifiedDocument2 pagesSpecial Report: Vhong Navarro's Latest Investment Has Experts in Awe and Big Banks TerrifiedArt B. EnriquezNo ratings yet

- History of VolleyballDocument5 pagesHistory of VolleyballAlex CorporalNo ratings yet

- Antiderivatives of Functions: Integral CalculusDocument4 pagesAntiderivatives of Functions: Integral CalculusArt B. EnriquezNo ratings yet

- Antiderivatives of Functions: Integral CalculusDocument4 pagesAntiderivatives of Functions: Integral CalculusArt B. EnriquezNo ratings yet

- Terms in This SetDocument1 pageTerms in This SetArt B. EnriquezNo ratings yet

- Overconfidence Bias: Cognitive DissonanceDocument3 pagesOverconfidence Bias: Cognitive DissonanceArt B. EnriquezNo ratings yet

- At The Period End of 2018Document2 pagesAt The Period End of 2018Art B. EnriquezNo ratings yet

- Overconfidence Bias: Cognitive DissonanceDocument3 pagesOverconfidence Bias: Cognitive DissonanceArt B. EnriquezNo ratings yet

- Product Costs vs Period Costs ExplainedDocument1 pageProduct Costs vs Period Costs ExplainedHeart Erica AbagNo ratings yet

- Engineering Econ Lab - Week 1Document2 pagesEngineering Econ Lab - Week 1Zac QuezonNo ratings yet

- Levels of Symptoms in COVID-19 Suspect: Probable CaseDocument3 pagesLevels of Symptoms in COVID-19 Suspect: Probable CaseArt B. EnriquezNo ratings yet

- Chapter 01Document64 pagesChapter 01federicoNo ratings yet

- Oblicon 2016Document8 pagesOblicon 2016Art B. EnriquezNo ratings yet

- Accountancy XI Half Yearly WorksheetDocument8 pagesAccountancy XI Half Yearly WorksheetDeivanai K CSNo ratings yet

- Chapter 5 - RevisionDocument13 pagesChapter 5 - RevisionActOn Business Solutions (Simplifying Business)No ratings yet

- Project Report: Online BankingDocument38 pagesProject Report: Online BankingRoshan ShawNo ratings yet

- Wirecard Funds Accessible Blog Post Updated - 30 June 2020 PDFDocument2 pagesWirecard Funds Accessible Blog Post Updated - 30 June 2020 PDFAsia Binta Amanat SumiNo ratings yet

- Statement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocument3 pagesStatement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing Balancernghmbwk8mNo ratings yet

- Legal Notice 8441363 1-7b8ae25223f76cd0Document2 pagesLegal Notice 8441363 1-7b8ae25223f76cd0Yash SharmaNo ratings yet

- Volcker Rule Facts On MetricsDocument15 pagesVolcker Rule Facts On Metricschandkhand2No ratings yet

- International Financial Management Canadian Canadian 3rd Edition Brean Test Bank 1Document17 pagesInternational Financial Management Canadian Canadian 3rd Edition Brean Test Bank 1beatrice100% (45)

- ECN 111 Chapter 12 Lecture Notes: 12.1 How Banks Create MoneyDocument2 pagesECN 111 Chapter 12 Lecture Notes: 12.1 How Banks Create MoneyShivendu AnandNo ratings yet

- Jasleen Kaur Report NewDocument85 pagesJasleen Kaur Report NewDaman Deep Singh ArnejaNo ratings yet

- BEC 3303 Financial Economics Session 2Document58 pagesBEC 3303 Financial Economics Session 2Tharindu PereraNo ratings yet

- Bank Lending Process & DocumentationDocument13 pagesBank Lending Process & Documentationsagar kaleNo ratings yet

- Sonam Phoenix Refund Form 1Document1 pageSonam Phoenix Refund Form 1pema lhamoNo ratings yet

- Depository Institutions: Take Charge of Your Finances 1.7.3Document21 pagesDepository Institutions: Take Charge of Your Finances 1.7.3taani345No ratings yet

- INKOLLU-Hyderabad bus ticketDocument2 pagesINKOLLU-Hyderabad bus ticketEswar RaoNo ratings yet

- SbiDocument6 pagesSbiPawan SaxenaNo ratings yet

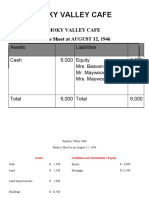

- Smoky Valley CafeDocument3 pagesSmoky Valley CafeRajkumar KrishnamoorthyNo ratings yet

- Vertex42 Money Manager 2.0: INSTRUCTIONS - For Excel 2010 or LaterDocument26 pagesVertex42 Money Manager 2.0: INSTRUCTIONS - For Excel 2010 or LaterNikkiNo ratings yet

- BPI: Q1 Balance SheetDocument1 pageBPI: Q1 Balance SheetBusinessWorldNo ratings yet

- Rbi Ar 2020-21Document350 pagesRbi Ar 2020-21Praveen PNo ratings yet

- STAT 3820 Homework 1 Chapter 1 ProblemsDocument2 pagesSTAT 3820 Homework 1 Chapter 1 ProblemsestarianNo ratings yet

- (Bank Journal No.) (Only Numeric) (Bank Journal No.) (Only Numeric)Document1 page(Bank Journal No.) (Only Numeric) (Bank Journal No.) (Only Numeric)chayan_m_shahNo ratings yet

- Cash and Cash Equivalents 1Document15 pagesCash and Cash Equivalents 1Micko LagundinoNo ratings yet

- SIBL AssignmentDocument12 pagesSIBL AssignmentDipayan_luNo ratings yet

- Basic Instructions For A Bank Reconciliation Statement PDFDocument4 pagesBasic Instructions For A Bank Reconciliation Statement PDFKassandra EbolNo ratings yet