You might also like

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNo ratings yet

- Wiley Practitioner's Guide to GAAS 2006: Covering all SASs, SSAEs, SSARSs, and InterpretationsFrom EverandWiley Practitioner's Guide to GAAS 2006: Covering all SASs, SSAEs, SSARSs, and InterpretationsRating: 2 out of 5 stars2/5 (2)

- Audit of ReceivablesDocument48 pagesAudit of Receivablescarl fuerzasNo ratings yet

- AACONAPPS2 A433 - Audit of ReceivablesDocument23 pagesAACONAPPS2 A433 - Audit of ReceivablesDawson Dela CruzNo ratings yet

- Audit of Receivables and Sales SolutionsDocument16 pagesAudit of Receivables and Sales SolutionsNICELLE TAGLENo ratings yet

- 3 Months PlanDocument8 pages3 Months PlanWaleed ZakariaNo ratings yet

- Lembar Jawaban Mahesa - SalinDocument10 pagesLembar Jawaban Mahesa - Salinricoananta10No ratings yet

- AE 111 Midterm Summative Assessment 3 SolutionsDocument12 pagesAE 111 Midterm Summative Assessment 3 SolutionsDjunah ArellanoNo ratings yet

- Accounts Receivable and AFBDDocument18 pagesAccounts Receivable and AFBDeia aieNo ratings yet

- Assumptions - Assumptions - Financing: Year - 0 Year - 1 Year - 2 Year - 3 Year - 4Document2 pagesAssumptions - Assumptions - Financing: Year - 0 Year - 1 Year - 2 Year - 3 Year - 4PranshuNo ratings yet

- Template 2 Task 3 Calculation Worksheet - BSBFIM601Document17 pagesTemplate 2 Task 3 Calculation Worksheet - BSBFIM601Writing Experts0% (1)

- Lembar Jawab Laporan KeuanganDocument10 pagesLembar Jawab Laporan Keuanganricoananta10No ratings yet

- AA Chapter2Document6 pagesAA Chapter2Nikki GarciaNo ratings yet

- PERSIJADocument10 pagesPERSIJAricoananta10No ratings yet

- Fa July2023-Far210-StudentDocument9 pagesFa July2023-Far210-Student2022613976No ratings yet

- Consolidated financial statements worksheetDocument38 pagesConsolidated financial statements worksheetJeane Mae BooNo ratings yet

- Key Financial Indicators of The Company (Projected) : Cost of The New Project & Means of FinanceDocument15 pagesKey Financial Indicators of The Company (Projected) : Cost of The New Project & Means of FinanceRashan Jida ReshanNo ratings yet

- Capital Budgeting ExamplesDocument16 pagesCapital Budgeting ExamplesMuhammad azeemNo ratings yet

- Itsa Excel SheetDocument7 pagesItsa Excel SheetraheelehsanNo ratings yet

- WBS WPL PT Palu GadaDocument10 pagesWBS WPL PT Palu GadaLucky AristioNo ratings yet

- Technopreneurship PPT Presentation Group 1Document57 pagesTechnopreneurship PPT Presentation Group 1Mia ElizabethNo ratings yet

- Ats Consolidated (Atsc), Inc. Fiscal Fitness Analysis (Draft)Document6 pagesAts Consolidated (Atsc), Inc. Fiscal Fitness Analysis (Draft)Marilou CagampangNo ratings yet

- Financial Analysis - Mini Case-Norbrook-Group BDocument2 pagesFinancial Analysis - Mini Case-Norbrook-Group BErrol ThompsonNo ratings yet

- Inventory Sales Accounts Receivable PurchasesDocument4 pagesInventory Sales Accounts Receivable PurchasesPhilip CastroNo ratings yet

- Aud PWDocument16 pagesAud PWJikaNo ratings yet

- Receivables Morning Star Corporation: I Will Manually Check Your Answer For Rounding Off DifferencesDocument3 pagesReceivables Morning Star Corporation: I Will Manually Check Your Answer For Rounding Off DifferencesGlance BautistaNo ratings yet

- Vederinus Stefanus 86220 0Document9 pagesVederinus Stefanus 86220 0PdoneeverNo ratings yet

- STAR LORD CORP. EMPLOYEE STOCK OPTIONSDocument20 pagesSTAR LORD CORP. EMPLOYEE STOCK OPTIONSadieNo ratings yet

- Solutions WK 6Document8 pagesSolutions WK 6simamo4203No ratings yet

- Exercises Module 3Document12 pagesExercises Module 3jpNo ratings yet

- Valuation Final ExamDocument4 pagesValuation Final ExamJeane Mae Boo100% (1)

- Book 1Document4 pagesBook 1almira garciaNo ratings yet

- Exercises - Cash and ReceivablesDocument8 pagesExercises - Cash and ReceivablesjpNo ratings yet

- Menyusun Laporan KeuanganDocument18 pagesMenyusun Laporan KeuanganAngelaNo ratings yet

- Cat 1 SD23Document2 pagesCat 1 SD23HarusiNo ratings yet

- Panther Tyre Company Balance Sheet 43,100.00 2,018.00 2,019.00 2,020.00 Assets Current Assets Increase or (Decrease)Document7 pagesPanther Tyre Company Balance Sheet 43,100.00 2,018.00 2,019.00 2,020.00 Assets Current Assets Increase or (Decrease)HussainNo ratings yet

- UAS PA 2020-2021 Ganjil - JawabanDocument27 pagesUAS PA 2020-2021 Ganjil - JawabanNuruddin AsyifaNo ratings yet

- Less: Present value of expected cash flowsDocument8 pagesLess: Present value of expected cash flowsMaricar PinedaNo ratings yet

- Trial Balance Adjustments FinancialsDocument2 pagesTrial Balance Adjustments FinancialsMichelle BabaNo ratings yet

- Practice Set 1Document6 pagesPractice Set 1moreNo ratings yet

- 2.0 Telus AnalysisDocument6 pages2.0 Telus Analysiskevin kipkemoiNo ratings yet

- Nur Atiqah Binti Saadon (Kba2761a) - 2023448576Document3 pagesNur Atiqah Binti Saadon (Kba2761a) - 2023448576nuratiqahsaadon89No ratings yet

- AP Receivablesdocx PDF FreeDocument13 pagesAP Receivablesdocx PDF FreeAnn SaturayNo ratings yet

- Audit Receivables SalesDocument13 pagesAudit Receivables SalesRegina Rebulado40% (5)

- Perpetual Bank: ReceivablesDocument13 pagesPerpetual Bank: ReceivablesYes ChannelNo ratings yet

- Closing P2 JayatamaDocument2 pagesClosing P2 JayatamaShula KinantiNo ratings yet

- Adesoye, Adeniji-Scena - CorrectDocument11 pagesAdesoye, Adeniji-Scena - CorrectAdesoye AdenijiNo ratings yet

- Calculating adjustments for Pacers Company inventory, payables, and salesDocument13 pagesCalculating adjustments for Pacers Company inventory, payables, and salesShiela Mae BautistaNo ratings yet

- Assignment 1Document6 pagesAssignment 1Nichole TumulakNo ratings yet

- Chapter 4Document7 pagesChapter 4Eumar FabruadaNo ratings yet

- CF 2Document26 pagesCF 2PUSHKAL AGGARWALNo ratings yet

- DebitCreditAnalysisComparesAccountsYear"TITLE "CashflowStatementAnalyzesPrimeSportsGearCashFlows2013" TITLE "RatioAnalysisComparesGlobalTechFinancialsSalesProfit201213Document7 pagesDebitCreditAnalysisComparesAccountsYear"TITLE "CashflowStatementAnalyzesPrimeSportsGearCashFlows2013" TITLE "RatioAnalysisComparesGlobalTechFinancialsSalesProfit201213shineneigh00No ratings yet

- Chapter 7 Up StreamDocument14 pagesChapter 7 Up StreamAditya Agung SatrioNo ratings yet

- March June 2022-PlatformDocument4 pagesMarch June 2022-PlatformOlivier MNo ratings yet

- BRS3B Assessment Opportunity 1 2019Document11 pagesBRS3B Assessment Opportunity 1 2019221103909No ratings yet

- Final Exam Far1Document4 pagesFinal Exam Far1Chloe CatalunaNo ratings yet

- Additional Problem SubsequentDocument4 pagesAdditional Problem SubsequentasdasdaNo ratings yet

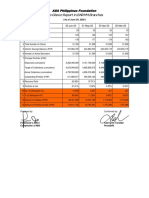

- ASA Philippines BARMM Report Highlights Key MetricsDocument3 pagesASA Philippines BARMM Report Highlights Key MetricsAbdulmanan HaridNo ratings yet

- ENTI Ver 1Document72 pagesENTI Ver 1krishna chaitanyaNo ratings yet

- FinmanDocument4 pagesFinmanAngel ToribioNo ratings yet

- Auditing Problems Prelims AdjustmentsDocument11 pagesAuditing Problems Prelims AdjustmentsannyeongchinguNo ratings yet

- Sales (De Leon)Document737 pagesSales (De Leon)Bj Carido100% (7)

- JCO Donuts and Coffee Expansion PlanDocument37 pagesJCO Donuts and Coffee Expansion PlanannyeongchinguNo ratings yet

- Annexes Syllabi Effective October 2022Document26 pagesAnnexes Syllabi Effective October 2022Rhad Estoque100% (9)

- 664 672 1 PBDocument22 pages664 672 1 PBcharlenesantos89No ratings yet

- Pay Standards & Practices: Accommodation and Food ServicesDocument2 pagesPay Standards & Practices: Accommodation and Food ServicesannyeongchinguNo ratings yet

- Franchise Application (Starbucks)Document9 pagesFranchise Application (Starbucks)annyeongchinguNo ratings yet

- Midterm ExamDocument12 pagesMidterm ExamGracias0% (2)

- NPO ProblemsDocument3 pagesNPO ProblemsAdam Smith50% (2)

- USJR Private University Statement of ActivitiesDocument13 pagesUSJR Private University Statement of ActivitiesSy Him80% (5)

- Uniform CPA Examination. Questions and Unofficial Answers 1988 NDocument96 pagesUniform CPA Examination. Questions and Unofficial Answers 1988 NShy LopezNo ratings yet

- QuestionsDocument16 pagesQuestionsLian GarlNo ratings yet

- Forever Bright Export PartnersDocument1 pageForever Bright Export PartnersannyeongchinguNo ratings yet

- Forever Bright Export PartnersDocument1 pageForever Bright Export PartnersannyeongchinguNo ratings yet

- Quiz 1 - Without AnswersDocument6 pagesQuiz 1 - Without AnswersannyeongchinguNo ratings yet

- Chapter 21 Accounting For Non Profit OrganizationsDocument21 pagesChapter 21 Accounting For Non Profit OrganizationsHyewon100% (1)

- Calibo vs Mike Abella: Validity of tractor pledgeDocument3 pagesCalibo vs Mike Abella: Validity of tractor pledgeannyeongchinguNo ratings yet

- Timeline of Rizal FinalDocument1 pageTimeline of Rizal FinalannyeongchinguNo ratings yet

- Timeline of Rizal FinalDocument1 pageTimeline of Rizal FinalannyeongchinguNo ratings yet

- All Subj Board Exam Picpa Ee PDF FreeDocument9 pagesAll Subj Board Exam Picpa Ee PDF FreeannyeongchinguNo ratings yet

- Timeline of Rizal FinalDocument1 pageTimeline of Rizal FinalannyeongchinguNo ratings yet

- Timeline of Rizal FinalDocument1 pageTimeline of Rizal FinalannyeongchinguNo ratings yet

- Congrats BSA 3 Namo Welcome To Auditing ProblemsDocument60 pagesCongrats BSA 3 Namo Welcome To Auditing ProblemsannyeongchinguNo ratings yet

- Module 1 Lesson 1 PDFDocument15 pagesModule 1 Lesson 1 PDFKatherine EderosasNo ratings yet

- Chapter 1 Introduction To Corporate FinanceDocument8 pagesChapter 1 Introduction To Corporate FinanceNicole BelisarioNo ratings yet

- Ch15 Beams10e TBDocument22 pagesCh15 Beams10e TBIm In Trouble50% (4)

- Timeline of Rizal FinalDocument1 pageTimeline of Rizal FinalannyeongchinguNo ratings yet

- Ch15 Beams10e TBDocument22 pagesCh15 Beams10e TBIm In Trouble50% (4)

- Annexes Syllabi Effective October 2022Document26 pagesAnnexes Syllabi Effective October 2022Rhad Estoque100% (9)

- Corporate Finance 11Th Edition Ross Solutions Manual Full Chapter PDFDocument35 pagesCorporate Finance 11Th Edition Ross Solutions Manual Full Chapter PDFvernon.amundson153100% (10)

- Gr. 12 2nd Sem ReviewerDocument8 pagesGr. 12 2nd Sem ReviewerLeric De VeraNo ratings yet

- Financial Performance Analysis of SIFCODocument8 pagesFinancial Performance Analysis of SIFCONamuna JoshiNo ratings yet

- BHC Customer DrivenDocument3 pagesBHC Customer DrivenKhanh NguyễnNo ratings yet

- Model - Student Version: MODULE 13 CORAL BAY HOSPITAL: Traditional Project AnalysisDocument23 pagesModel - Student Version: MODULE 13 CORAL BAY HOSPITAL: Traditional Project AnalysisHassanNo ratings yet

- MacalalagDocument1 pageMacalalagChristian Nehru ValeraNo ratings yet

- HRM 111Document21 pagesHRM 111Charles MasanyiwaNo ratings yet

- Mba Dainik JagranDocument78 pagesMba Dainik Jagranarvind tripathi100% (1)

- Adani Ports Balance Sheet DataDocument2 pagesAdani Ports Balance Sheet DataTaksh DhamiNo ratings yet

- Advertising Effectiveness: by Jerry W. Thomas, Decision AnalystDocument4 pagesAdvertising Effectiveness: by Jerry W. Thomas, Decision AnalystsalunkhevirajNo ratings yet

- Financial Accounting CH 2Document12 pagesFinancial Accounting CH 2Karim KhaledNo ratings yet

- Tax Invoice/Bill of Supply/Cash MemoDocument1 pageTax Invoice/Bill of Supply/Cash MemoPrem ChanderNo ratings yet

- You Exec - MECE Principle FreeDocument6 pagesYou Exec - MECE Principle FreefullaNo ratings yet

- Management Accounting Practice Questions ABC Costing and Make vs Buy AnalysisDocument3 pagesManagement Accounting Practice Questions ABC Costing and Make vs Buy AnalysisOsama RiazNo ratings yet

- BSBFIA301 Maintain Financial RecordsDocument7 pagesBSBFIA301 Maintain Financial RecordsMonique BugeNo ratings yet

- ACC0 20053 - Intermediate Accounting 1 - 2022 Final Departmental ExamDocument41 pagesACC0 20053 - Intermediate Accounting 1 - 2022 Final Departmental ExamNathalie Faye TajaNo ratings yet

- AirtelDocument25 pagesAirtelSrabani PalNo ratings yet

- Lahore Waste Management Company PDFDocument3 pagesLahore Waste Management Company PDFBint e HawaNo ratings yet

- NCERT Class XI Accountancy Part IIDocument333 pagesNCERT Class XI Accountancy Part IInikhilam.com67% (3)

- DeterminantsofCustomerLoyalty PuplishedDocument7 pagesDeterminantsofCustomerLoyalty PuplishedAdrianne Mae Almalvez RodrigoNo ratings yet

- HRM CROSSWORD (Team 16) - Crossword LabsDocument2 pagesHRM CROSSWORD (Team 16) - Crossword LabsAastha PawarNo ratings yet

- National Income and Price DeterminationDocument3 pagesNational Income and Price Determinationbustiman20No ratings yet

- Monopolistically CompetitiveDocument26 pagesMonopolistically Competitivebeth el100% (1)

- Thought: by Constance E. BagleyDocument3 pagesThought: by Constance E. Bagleyjitender KUMARNo ratings yet

- Social Media Marketing Impact On Delivery CompaniesDocument12 pagesSocial Media Marketing Impact On Delivery CompaniesSaima AsadNo ratings yet

- Priscilla's CVDocument2 pagesPriscilla's CVPriscillaNo ratings yet

- PM0010 Introduction To Project Management Fall 10Document2 pagesPM0010 Introduction To Project Management Fall 10santoshbn7No ratings yet

- International Business - AssignmentDocument5 pagesInternational Business - AssignmentAkshatNo ratings yet

- Employment News 25 Feb-03 MarDocument32 pagesEmployment News 25 Feb-03 MarDevesh GargNo ratings yet

- IPO Restored 1Document85 pagesIPO Restored 1JamesNo ratings yet