You might also like

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNo ratings yet

- Accounting AssignmentDocument2 pagesAccounting Assignmentjannatulnisha78No ratings yet

- ACCT 1107 - Assignment #4Document3 pagesACCT 1107 - Assignment #4hkarim8641No ratings yet

- Tutorial 4 QAsDocument6 pagesTutorial 4 QAsJin HueyNo ratings yet

- Week 3 Lecture Illustrative ExampleDocument2 pagesWeek 3 Lecture Illustrative ExamplewainikitiraculeNo ratings yet

- Assign AcctDocument12 pagesAssign AcctNaeemullah baig100% (1)

- Class Project - SolvedDocument8 pagesClass Project - SolvedMarcoNo ratings yet

- Book 2Document8 pagesBook 2May ManseNo ratings yet

- 12-Mar Accounts Receivable 11,000 Service Revenue 11,000 20-Mar Cash 10,780 Sales Discount 220 Accounts Receivable 11,000Document6 pages12-Mar Accounts Receivable 11,000 Service Revenue 11,000 20-Mar Cash 10,780 Sales Discount 220 Accounts Receivable 11,000Tess CoaryNo ratings yet

- Adjusted Financial StatementDocument4 pagesAdjusted Financial StatementYousef AL-HAZMINo ratings yet

- Trial balance financial recordsDocument12 pagesTrial balance financial recordsEhtisham Ul HaqNo ratings yet

- mgt101 Questions With AnswersDocument11 pagesmgt101 Questions With AnswersKinza LaiqatNo ratings yet

- Financial Statement Analysis of Tie Beauty EnterpriseDocument15 pagesFinancial Statement Analysis of Tie Beauty Enterprisenur anisNo ratings yet

- MGT 101Document13 pagesMGT 101MuzzamilNo ratings yet

- Chapter 4Document35 pagesChapter 4Mohammad Mostafa MostafaNo ratings yet

- POADocument7 pagesPOAjohnnyNo ratings yet

- WorkshitDocument12 pagesWorkshitLukman ArimartaNo ratings yet

- Go Green Lawn adjusting entriesDocument2 pagesGo Green Lawn adjusting entriesMd. Rokon KhanNo ratings yet

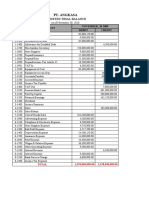

- Kerja Kelompok PT Angkasa BDocument28 pagesKerja Kelompok PT Angkasa BElisa EndrianiiNo ratings yet

- Adjusting Entry Math LatestDocument4 pagesAdjusting Entry Math LatestOyon Nur newazNo ratings yet

- Unit 2 WorksheetDocument13 pagesUnit 2 WorksheetHhvvgg BbbbNo ratings yet

- Practice Questions DM112 No 22Document13 pagesPractice Questions DM112 No 22Bianca BenNo ratings yet

- Closing entries for Gray Electronics Repair ServicesDocument1 pageClosing entries for Gray Electronics Repair Serviceswindell arth MercadoNo ratings yet

- AE 25 Module 1 Lesson 1Document99 pagesAE 25 Module 1 Lesson 1Queeny Mae Cantre ReutaNo ratings yet

- LkhgyDocument2 pagesLkhgyDynNo ratings yet

- Calculate adjustments to trial balance for A Albert and J O'SheaDocument3 pagesCalculate adjustments to trial balance for A Albert and J O'SheaUnais AhmedNo ratings yet

- The Parable of The Talents - 20190714Document6 pagesThe Parable of The Talents - 20190714LynnHanNo ratings yet

- Bfar Chapter 8 Problems 6 7Document9 pagesBfar Chapter 8 Problems 6 7Rhoda Claire M. GansobinNo ratings yet

- MD JiloDocument6 pagesMD JiloAbdi Mucee TubeNo ratings yet

- Class Project - November - HomeworkDocument13 pagesClass Project - November - HomeworkMarcoNo ratings yet

- Accounting Cycle of A Service Business: Mr. Jan CupangDocument30 pagesAccounting Cycle of A Service Business: Mr. Jan Cupangbanigx0xNo ratings yet

- DSR Mock Test - 1 - Ca FoundationDocument5 pagesDSR Mock Test - 1 - Ca Foundationmaskguy001No ratings yet

- Name Roll No Program: Hamza Iqbal 2021-25-0001 Financial ManagementDocument9 pagesName Roll No Program: Hamza Iqbal 2021-25-0001 Financial ManagementHamza IqbalNo ratings yet

- ABM Fundamentals of AccountingDocument3 pagesABM Fundamentals of AccountingtsukiNo ratings yet

- Cheng Company: Selected Transactions From The Journal of June Feldman, Investment Broker, Are Presented BelowDocument4 pagesCheng Company: Selected Transactions From The Journal of June Feldman, Investment Broker, Are Presented BelowHà Anh Đỗ100% (1)

- Hot Qus Class 12thDocument13 pagesHot Qus Class 12thNaveen ShahNo ratings yet

- Completing The Accounting Cycle: Service Concern: Subject-Descriptive Title Subject - CodeDocument12 pagesCompleting The Accounting Cycle: Service Concern: Subject-Descriptive Title Subject - CodeRose LaureanoNo ratings yet

- Trial Balance CompletedDocument1 pageTrial Balance CompletedapachemonoNo ratings yet

- 605701b41234414fbf70f2a0d6734ae1Document3 pages605701b41234414fbf70f2a0d6734ae1BabaNo ratings yet

- Bacc 126 Assignment 1 Aug - Dec 2023Document11 pagesBacc 126 Assignment 1 Aug - Dec 2023TarusengaNo ratings yet

- B&B Repair Services Income StatementDocument22 pagesB&B Repair Services Income Statementrhyayuli0% (1)

- TM PQsDocument10 pagesTM PQsAnooshayNo ratings yet

- Journal Entries Trial BalanceDocument3 pagesJournal Entries Trial BalanceLiu CellNo ratings yet

- Compreh Problems - AAA - SolutionDocument28 pagesCompreh Problems - AAA - SolutionNicola NaberNo ratings yet

- Add: Cheque Issued But Not Presented Interest Credited Less: Bank ChargesDocument9 pagesAdd: Cheque Issued But Not Presented Interest Credited Less: Bank ChargesSiddharth RoyNo ratings yet

- 2019-06 ICMAB FL 001 PAC Year Question JUNE 2019Document3 pages2019-06 ICMAB FL 001 PAC Year Question JUNE 2019Mohammad ShahidNo ratings yet

- Aminah Quiz Answer Done by Abdullah Narejo-The Great.Document10 pagesAminah Quiz Answer Done by Abdullah Narejo-The Great.Abdullah NarejoNo ratings yet

- Kotak Mahindra Bank Limited Payslip For The Month of AUGUST - 2010Document1 pageKotak Mahindra Bank Limited Payslip For The Month of AUGUST - 2010Bharat Shahane33% (3)

- Worksheet SolutionDocument1 pageWorksheet SolutionFahim Ahmed RatulNo ratings yet

- Comprehensive 1 2 Chapters 1-4Document38 pagesComprehensive 1 2 Chapters 1-4api-35603600250% (2)

- V1620034 - Dzaky FarhansyahDocument11 pagesV1620034 - Dzaky FarhansyahDzaky FarhansyahNo ratings yet

- Mansa Building Case Financial AnalysisDocument10 pagesMansa Building Case Financial AnalysisSanyam RahejaNo ratings yet

- CHP 6 Partnership Exercise 1-4Document5 pagesCHP 6 Partnership Exercise 1-4jasongojinkai2007No ratings yet

- BBB - Assignment FARDocument23 pagesBBB - Assignment FARcha618717No ratings yet

- 2019 Unit 4 Budgeting SAC Solution BookDocument3 pages2019 Unit 4 Budgeting SAC Solution BookLachlan McFarlandNo ratings yet

- Exercise 2 (Cashflow Statements)Document2 pagesExercise 2 (Cashflow Statements)Prince TshepoNo ratings yet

- Acc 102 Drill No. 1 Answer Key 3Document17 pagesAcc 102 Drill No. 1 Answer Key 3Hanan MacalbeNo ratings yet

- F1. FIOO.P December 2020Document6 pagesF1. FIOO.P December 2020Laskar REAZNo ratings yet

- Finals Activity No .2 Completing THE Accounting Cycle: Palad, Nica C. Mr. Alfred BautistaDocument6 pagesFinals Activity No .2 Completing THE Accounting Cycle: Palad, Nica C. Mr. Alfred BautistaMica Mae CorreaNo ratings yet

- Adjust Financial Statements & Prepare ReportsDocument1 pageAdjust Financial Statements & Prepare ReportsalexandraNo ratings yet

- 7 Plus English Paper SampleDocument12 pages7 Plus English Paper SampleDoan Chan PhongNo ratings yet

- 7 Plus Maths Paper SampleDocument14 pages7 Plus Maths Paper SampleDoan Chan PhongNo ratings yet

- 7 Plus English ComprehensionDocument3 pages7 Plus English ComprehensionAlyssa LNo ratings yet

- The Haberdashers' Aske's Boys' School Elstree: Sample PaperDocument3 pagesThe Haberdashers' Aske's Boys' School Elstree: Sample Paperbujjibangaru2012No ratings yet

- 7 Plus English GrammarDocument3 pages7 Plus English Grammarbujjibangaru2012No ratings yet

- Model Theory Lecture Back-and-Forth EquivalenceDocument48 pagesModel Theory Lecture Back-and-Forth EquivalenceDoan Chan PhongNo ratings yet

- Many-Sorted First-Order Model Theory Lecture 6: Easy Halves and Unions of ChainsDocument37 pagesMany-Sorted First-Order Model Theory Lecture 6: Easy Halves and Unions of ChainsDoan Chan PhongNo ratings yet

- Many-Sorted First-Order Model Theory: 25 June, 2020Document31 pagesMany-Sorted First-Order Model Theory: 25 June, 2020Doan Chan PhongNo ratings yet

- Many-Sorted First-Order Model Theory Lecture 11: Homogeneity and ω-categoricityDocument33 pagesMany-Sorted First-Order Model Theory Lecture 11: Homogeneity and ω-categoricityDoan Chan PhongNo ratings yet

- One Two-Hour Lecture A Week: Thursday 16:00-18:00 JST. Zoom Sessions For Practice Classes: To Be Organised On DemandDocument28 pagesOne Two-Hour Lecture A Week: Thursday 16:00-18:00 JST. Zoom Sessions For Practice Classes: To Be Organised On DemandDoan Chan PhongNo ratings yet

- Many-Sorted First-Order Model Theory: 19 June, 2020Document48 pagesMany-Sorted First-Order Model Theory: 19 June, 2020Doan Chan PhongNo ratings yet

- Many-Sorted First-Order Model Theory: 2 July, 2020Document37 pagesMany-Sorted First-Order Model Theory: 2 July, 2020Doan Chan PhongNo ratings yet

- Exercise 5.1: A Werribee Office Cleaners: Cash Receipts JournalDocument9 pagesExercise 5.1: A Werribee Office Cleaners: Cash Receipts JournalDoan Chan PhongNo ratings yet

- Many-Sorted First-Order Model Theory Lecture 3: Presentation Morphisms and Entailment RelationsDocument14 pagesMany-Sorted First-Order Model Theory Lecture 3: Presentation Morphisms and Entailment RelationsDoan Chan PhongNo ratings yet

- Many-Sorted First-Order Model TheoryDocument22 pagesMany-Sorted First-Order Model TheoryDoan Chan PhongNo ratings yet

- Many-Sorted First-Order Model Theory: 2 June, 2020Document18 pagesMany-Sorted First-Order Model Theory: 2 June, 2020Doan Chan PhongNo ratings yet

- Many-Sorted First-Order Model Theory Lecture 5Document56 pagesMany-Sorted First-Order Model Theory Lecture 5Doan Chan PhongNo ratings yet

- Mathematics Test 2Document15 pagesMathematics Test 2annabellehoohNo ratings yet

- Exercise 3.1: A B C D eDocument3 pagesExercise 3.1: A B C D eDoan Chan PhongNo ratings yet

- Exercise 7.1: S.O. Heater Installations: Bank Reconciliation Statement As at 31 July 2015Document12 pagesExercise 7.1: S.O. Heater Installations: Bank Reconciliation Statement As at 31 July 2015Doan Chan PhongNo ratings yet

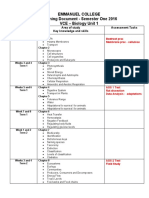

- Emmanuel College Planning Document - Semester One 2016 VCE - Biology Unit 1Document2 pagesEmmanuel College Planning Document - Semester One 2016 VCE - Biology Unit 1Doan Chan PhongNo ratings yet

- Mathstest1 PDFDocument15 pagesMathstest1 PDFManju GalagangodageNo ratings yet

- Selective Schools Sample Test 2Document4 pagesSelective Schools Sample Test 2Doan Chan PhongNo ratings yet

- Selective Schools Sample Test 1Document4 pagesSelective Schools Sample Test 1Doan Chan PhongNo ratings yet

- Selective Schools Sample Test 2 AnswersDocument1 pageSelective Schools Sample Test 2 AnswersDoan Chan PhongNo ratings yet

- Finaflex Main Catalog 2022Document50 pagesFinaflex Main Catalog 2022Benlee Calderón LimaNo ratings yet

- FentonTech Wastewater Ghernaout 2020Document29 pagesFentonTech Wastewater Ghernaout 2020BrankNo ratings yet

- Insertion Mangement Peripheral IVCannulaDocument20 pagesInsertion Mangement Peripheral IVCannulaAadil AadilNo ratings yet

- Final Order in The Matter of M/s Alchemist Capital LTDDocument61 pagesFinal Order in The Matter of M/s Alchemist Capital LTDShyam SunderNo ratings yet

- American SpartansDocument4 pagesAmerican SpartansArya V. VajraNo ratings yet

- Thời gian làm bài: 90 phút (không kể thời gian giao đề)Document8 pagesThời gian làm bài: 90 phút (không kể thời gian giao đề)Nguyễn KiênNo ratings yet

- Letter To Editor NDocument5 pagesLetter To Editor NNavya AgarwalNo ratings yet

- SCC800-B2 SmartSite Management System V100R002C00 Installation GuideDocument190 pagesSCC800-B2 SmartSite Management System V100R002C00 Installation GuideHamza OsamaNo ratings yet

- EthicsDocument10 pagesEthicsEssi Chan100% (4)

- June 10Document16 pagesJune 10rogeliodmngNo ratings yet

- Flamme Rouge - Grand Tour Rules - English-print-V2Document3 pagesFlamme Rouge - Grand Tour Rules - English-print-V2dATCHNo ratings yet

- Isoenzyme ClassifiedDocument33 pagesIsoenzyme Classifiedsayush754No ratings yet

- 03 IoT Technical Sales Training Industrial Wireless Deep DiveDocument35 pages03 IoT Technical Sales Training Industrial Wireless Deep Divechindi.comNo ratings yet

- Sheet-Pan Salmon and Broccoli With Sesame and Ginger: by Lidey HeuckDocument2 pagesSheet-Pan Salmon and Broccoli With Sesame and Ginger: by Lidey HeuckllawNo ratings yet

- Shlokas and BhajansDocument204 pagesShlokas and BhajansCecilie Ramazanova100% (1)

- German Modern Architecture Adn The Modern WomanDocument24 pagesGerman Modern Architecture Adn The Modern WomanUrsula ColemanNo ratings yet

- Post Graduate Dip DermatologyDocument2 pagesPost Graduate Dip DermatologyNooh DinNo ratings yet

- FSN Lullaby Warmer Resus Plus&PrimeDocument4 pagesFSN Lullaby Warmer Resus Plus&PrimemohdkhidirNo ratings yet

- Antianginal Student222Document69 pagesAntianginal Student222MoonAIRNo ratings yet

- Document 3Document5 pagesDocument 3SOLOMON RIANNANo ratings yet

- Armenian Question in Tasvir-İ Efkar Between 1914 and 1918Document152 pagesArmenian Question in Tasvir-İ Efkar Between 1914 and 1918Gültekin ÖNCÜNo ratings yet

- Salman Sahuri - Identification of Deforestation in Protected Forest AreasDocument9 pagesSalman Sahuri - Identification of Deforestation in Protected Forest AreaseditorseajaetNo ratings yet

- Speidel, M. O. (1981) - Stress Corrosion Cracking of Stainless Steels in NaCl Solutions.Document11 pagesSpeidel, M. O. (1981) - Stress Corrosion Cracking of Stainless Steels in NaCl Solutions.oozdemirNo ratings yet

- Exam On Multiculturalism: - Acculturation Process of Immigrants From Central and Eastern Europe in SwedenDocument60 pagesExam On Multiculturalism: - Acculturation Process of Immigrants From Central and Eastern Europe in SwedenMarta santosNo ratings yet

- Christmas Elf NPCDocument4 pagesChristmas Elf NPCDrew CampbellNo ratings yet

- Individual Learning Monitoring PlanDocument2 pagesIndividual Learning Monitoring PlanJohnArgielLaurenteVictorNo ratings yet

- Igbe Religion's 21st Century Syncretic Response to ChristianityDocument30 pagesIgbe Religion's 21st Century Syncretic Response to ChristianityFortune AFATAKPANo ratings yet

- Types of EquityDocument2 pagesTypes of EquityPrasanthNo ratings yet

- CPSC5125 - Assignment 3 - Fall 2014 Drawing Polygons: DescriptionDocument2 pagesCPSC5125 - Assignment 3 - Fall 2014 Drawing Polygons: DescriptionJo KingNo ratings yet

- A Place in Lake County - The Property Owner's Resource GuideDocument16 pagesA Place in Lake County - The Property Owner's Resource GuideMinnesota's Lake Superior Coastal ProgramNo ratings yet