You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5819)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (845)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (348)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Wang - Oceanic Feeling and Communist Affect (Original)Document18 pagesWang - Oceanic Feeling and Communist Affect (Original)Christoph CoxNo ratings yet

- Wireless Service AgreementDocument6 pagesWireless Service AgreementSerguei100% (1)

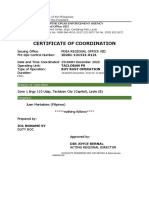

- Certificate of Coordination: Area(s) of OperationDocument3 pagesCertificate of Coordination: Area(s) of OperationervingabralagbonNo ratings yet

- Order For Farewell and Thanksgiving For PastorDocument2 pagesOrder For Farewell and Thanksgiving For PastorBrince Mathews0% (1)

- Reaction Paper Rizal in DapitanDocument4 pagesReaction Paper Rizal in DapitanTatlonghariChristine79% (28)

- Tacloban City Police Station: Hotline - 0998.598.6680Document2 pagesTacloban City Police Station: Hotline - 0998.598.6680ervingabralagbonNo ratings yet

- Legal & Judicial Ethics & Practical Exercises SyllabusDocument8 pagesLegal & Judicial Ethics & Practical Exercises Syllabuservingabralagbon100% (1)

- Outline of Topics Taxation Law Review IvDocument6 pagesOutline of Topics Taxation Law Review IvervingabralagbonNo ratings yet

- Ethics - FINALS - Additional CasesDocument12 pagesEthics - FINALS - Additional CaseservingabralagbonNo ratings yet

- People Vs MarbabiesDocument3 pagesPeople Vs MarbabieservingabralagbonNo ratings yet

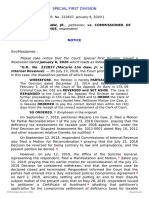

- 46 Gaw Jr. v. Commissioner of Internal Revenue (NOTICE)Document9 pages46 Gaw Jr. v. Commissioner of Internal Revenue (NOTICE)ervingabralagbonNo ratings yet

- 36 Commissioner of Internal Revenue v. T Shuttle20210428-11-1vpfpc0Document10 pages36 Commissioner of Internal Revenue v. T Shuttle20210428-11-1vpfpc0ervingabralagbonNo ratings yet

- 53 Commissioner of Internal Revenue v. Fitness20210505-12-Mxv1tfDocument20 pages53 Commissioner of Internal Revenue v. Fitness20210505-12-Mxv1tfervingabralagbonNo ratings yet

- 35 Philippine Dream Company Inc. V.20210424-12-1jxqs4iDocument11 pages35 Philippine Dream Company Inc. V.20210424-12-1jxqs4iervingabralagbonNo ratings yet

- Petitioner Respondent: Medicard Philippines, Inc., Commissioner of Internal RevenueDocument19 pagesPetitioner Respondent: Medicard Philippines, Inc., Commissioner of Internal RevenueervingabralagbonNo ratings yet

- 48 Commissioner of Internal Revenue v. J.P.20210424-12-14n6uedDocument19 pages48 Commissioner of Internal Revenue v. J.P.20210424-12-14n6uedervingabralagbonNo ratings yet

- Surah Al-Hashr: All That Is in The Heavens and The Earth Glorifies Allah, and He Is The Almighty, The All-WiseDocument7 pagesSurah Al-Hashr: All That Is in The Heavens and The Earth Glorifies Allah, and He Is The Almighty, The All-WiseChinese ClassNo ratings yet

- Notification Regarding H S Pre Final Examination 2023 in Connection With The H S Final Examination 2024Document1 pageNotification Regarding H S Pre Final Examination 2023 in Connection With The H S Final Examination 2024sarkaramortoNo ratings yet

- Lesson Plan: "Pete The Cat-Rocking in My School Shoes" by Eric Litwin (Document9 pagesLesson Plan: "Pete The Cat-Rocking in My School Shoes" by Eric Litwin (FranciscoDiegoNo ratings yet

- SWOT Analysis of Financial Technology in The BankiDocument9 pagesSWOT Analysis of Financial Technology in The BankiArif HasanNo ratings yet

- Press Release - Breast Cancer Awareness Drive - EditedDocument2 pagesPress Release - Breast Cancer Awareness Drive - EditedParag DhurkeNo ratings yet

- Riset NZTE ReportDocument93 pagesRiset NZTE ReportRdy SimangunsongNo ratings yet

- Sugarfina v. Bouquet Bar - Motion To DismissDocument106 pagesSugarfina v. Bouquet Bar - Motion To DismissSarah BursteinNo ratings yet

- Worksheet 1Document2 pagesWorksheet 1Smoked PeanutNo ratings yet

- Isha-Upanishad English VersionDocument99 pagesIsha-Upanishad English VersionPranay KumarNo ratings yet

- Financial Analyst - ELBISCO - LinkedInDocument3 pagesFinancial Analyst - ELBISCO - LinkedInMarina PsimopoulouNo ratings yet

- Minutes NDC 2 Construction Meeting 20 June 23Document3 pagesMinutes NDC 2 Construction Meeting 20 June 23GlorieNo ratings yet

- Victory Liner v. Gammad, GR No. 159636Document7 pagesVictory Liner v. Gammad, GR No. 159636Nikki Rose Laraga AgeroNo ratings yet

- EGE 102 Course SyllabusDocument2 pagesEGE 102 Course SyllabusDave Matthew LibiranNo ratings yet

- Renewable Energy Lesson PlanDocument4 pagesRenewable Energy Lesson PlanSofía Berrotarán100% (1)

- Instant Download Solution Manual For Police Ethics 2nd Edition PDF ScribdDocument32 pagesInstant Download Solution Manual For Police Ethics 2nd Edition PDF ScribdJerry Williams100% (17)

- Serving Christ by Learning, Leading and Loving: Our Mission StatementDocument3 pagesServing Christ by Learning, Leading and Loving: Our Mission StatementDHUMCNo ratings yet

- The Gift of The Magi DocumentationDocument19 pagesThe Gift of The Magi DocumentationPriyansh JainNo ratings yet

- Sermon Notes First Ecumenical Church Service Palm Sunday April 1, 2012Document3 pagesSermon Notes First Ecumenical Church Service Palm Sunday April 1, 2012api-180169039No ratings yet

- Can Police Grant Bail For A Non-Bailable Offence - A Discussion by Rakesh Kumar SinghDocument3 pagesCan Police Grant Bail For A Non-Bailable Offence - A Discussion by Rakesh Kumar SinghLatest Laws Team33% (3)

- CSE - One Week National Level Bootcamp - BroucherDocument2 pagesCSE - One Week National Level Bootcamp - BroucherAbcd EfghNo ratings yet

- PintoDocument18 pagesPintoAto SumartoNo ratings yet

- Challenges To Translate IdiomsDocument9 pagesChallenges To Translate IdiomsOrsi SimonNo ratings yet

- Intro To Qual Research - Uwe FlickDocument33 pagesIntro To Qual Research - Uwe FlickadsdNo ratings yet

- Moot Court PropositionDocument4 pagesMoot Court PropositionMathumita A.BNo ratings yet

- Budget: The New York State Unified Court SystemDocument183 pagesBudget: The New York State Unified Court SystemjspectorNo ratings yet

- O Imperador de Todos Os Males - Siddhartha MukherjeeDocument8 pagesO Imperador de Todos Os Males - Siddhartha MukherjeeAfonso FeitosaNo ratings yet