You might also like

- 1.1 Problems On VAT (PRTC) PDFDocument17 pages1.1 Problems On VAT (PRTC) PDFmarco poloNo ratings yet

- Quiz 4 VATDocument3 pagesQuiz 4 VATAsiong Salonga100% (2)

- Since 1977: Philippine TaxationDocument6 pagesSince 1977: Philippine TaxationXyza JabiliNo ratings yet

- Value Added TaxDocument5 pagesValue Added TaxRaven Vargas DayritNo ratings yet

- Donor's Tax SeatworkDocument12 pagesDonor's Tax SeatworkVirginia PalisukNo ratings yet

- Adaptive Solutions Online: Eight-Year Financial Projection For Product XDocument3 pagesAdaptive Solutions Online: Eight-Year Financial Projection For Product XLinh MaiNo ratings yet

- TAX - DrillDocument5 pagesTAX - DrillKriztleKateMontealtoGelogoNo ratings yet

- MINDANAO STATE UNIVERSITY ACCOUNTANCY QUIZ SERIES 3Document4 pagesMINDANAO STATE UNIVERSITY ACCOUNTANCY QUIZ SERIES 3Cardo DalisayNo ratings yet

- Departmental Finals Answer Key PDFDocument4 pagesDepartmental Finals Answer Key PDFJacob AcostaNo ratings yet

- Sde WRDocument10 pagesSde WRNitinNo ratings yet

- Value Added TaxDocument4 pagesValue Added TaxAllen KateNo ratings yet

- VAT and OPTDocument10 pagesVAT and OPTSharon CarilloNo ratings yet

- Review Business and Transfer TaxDocument201 pagesReview Business and Transfer TaxReginald ValenciaNo ratings yet

- Pinnacle IPCC Value Added TaxDocument44 pagesPinnacle IPCC Value Added TaxSneh ShahNo ratings yet

- TAX 56 - Business and Transfer TaxesDocument8 pagesTAX 56 - Business and Transfer TaxesAl JovenNo ratings yet

- LawDocument43 pagesLawMARIANo ratings yet

- SAMPLE PROBLEMS ON REGULAR TAXES (CTT Exam)Document1 pageSAMPLE PROBLEMS ON REGULAR TAXES (CTT Exam)Mharck AtienzaNo ratings yet

- Short Quiz 7 Set A With AnswerDocument3 pagesShort Quiz 7 Set A With AnswerJean Pierre Isip100% (1)

- Assignment Transfer Tax ComputationDocument3 pagesAssignment Transfer Tax ComputationAngelyn SamandeNo ratings yet

- Tax SolutionDocument1 pageTax SolutionRodel Francis G. SanitaNo ratings yet

- TAX ON INDIVIDUALS PART 1Document14 pagesTAX ON INDIVIDUALS PART 1Veel Creed100% (1)

- Exercises - Percentage TaxesDocument2 pagesExercises - Percentage TaxesMaristella GatonNo ratings yet

- Quiz On VAT154623Document5 pagesQuiz On VAT154623Sandy100% (1)

- Chapt 10 - Mixed Business TransactionsDocument6 pagesChapt 10 - Mixed Business TransactionsGemine Ailna Panganiban NuevoNo ratings yet

- Review in Business Law and TaxationDocument4 pagesReview in Business Law and TaxationFery AnnNo ratings yet

- Quiz 405Document3 pagesQuiz 405Shaika HaceenaNo ratings yet

- Income Taxation Ind PracticeDocument3 pagesIncome Taxation Ind PracticeJanine Tividad100% (1)

- Corporation Quiz PDFDocument8 pagesCorporation Quiz PDFangelo vasquezNo ratings yet

- Taxation: Far Eastern University - ManilaDocument4 pagesTaxation: Far Eastern University - ManilacamilleNo ratings yet

- Percentage Tax ProblemsDocument9 pagesPercentage Tax ProblemsAira Rhialyn MangubatNo ratings yet

- Chapter 14 Percentage TaxesDocument11 pagesChapter 14 Percentage TaxesGeraldNo ratings yet

- Tax Compliance RequirementsDocument8 pagesTax Compliance RequirementsJocelyn Verbo-AyubanNo ratings yet

- Sol Man - MC VatDocument9 pagesSol Man - MC Vatiamjan_101No ratings yet

- TAX-402 (Other Percentage Taxes - Part 2)Document6 pagesTAX-402 (Other Percentage Taxes - Part 2)VKVCPlaysNo ratings yet

- Revenue Etc For Income TaxationDocument286 pagesRevenue Etc For Income TaxationpurplebasketNo ratings yet

- Business and Transfer Taxation by Valencia and Roxas-Solution ManualDocument4 pagesBusiness and Transfer Taxation by Valencia and Roxas-Solution ManualFiona Manguerra81% (32)

- Individual Taxpayers Classified and Taxed DifferentlyDocument95 pagesIndividual Taxpayers Classified and Taxed DifferentlyRoronoa Zoro67% (3)

- 3 Floor, Business & Engineering Building, Matina, Davao City Telefax: (082) 300-1496 Phone No.: (082) 244-34-00 Local 137Document13 pages3 Floor, Business & Engineering Building, Matina, Davao City Telefax: (082) 300-1496 Phone No.: (082) 244-34-00 Local 137Abigail Ann PasiliaoNo ratings yet

- 17002Document2 pages17002Alvin YercNo ratings yet

- (Tax1) - Income Tax On Individuals - Discussion and ActivitiesDocument12 pages(Tax1) - Income Tax On Individuals - Discussion and ActivitiesKim EllaNo ratings yet

- This Study Resource Was: Value Added Tax (CPAR) TheoriesDocument6 pagesThis Study Resource Was: Value Added Tax (CPAR) TheoriesAllen KateNo ratings yet

- XBUSTAX Percentage and Other TaxesDocument5 pagesXBUSTAX Percentage and Other TaxesFlorine Fate SalungaNo ratings yet

- VAT problems with sales and purchase calculationsDocument3 pagesVAT problems with sales and purchase calculationsReginald ValenciaNo ratings yet

- Business and Transfer Taxation Chapter 13 Discussion Questions and AnswerDocument2 pagesBusiness and Transfer Taxation Chapter 13 Discussion Questions and AnswerKarla Faye LagangNo ratings yet

- H13.3 - Excise Tax - DSTDocument9 pagesH13.3 - Excise Tax - DSTnona galidoNo ratings yet

- 90,000 40,000 102,000 Correct Answer 110,000 100,000 300,000 312,000 314,000Document11 pages90,000 40,000 102,000 Correct Answer 110,000 100,000 300,000 312,000 314,000Hazel Grace PaguiaNo ratings yet

- Mock Quiz 1 FAR CFFR FS PresentationDocument7 pagesMock Quiz 1 FAR CFFR FS PresentationRodelLaborNo ratings yet

- Report of Law1 - Other Percentage TaxDocument16 pagesReport of Law1 - Other Percentage TaxJonalyn Maraña-ManuelNo ratings yet

- Value Added TaxDocument6 pagesValue Added TaxjamNo ratings yet

- VAT (Theory & Problem)Document10 pagesVAT (Theory & Problem)dimpy dNo ratings yet

- VAT Review PhilippinesDocument19 pagesVAT Review PhilippinesJuan Miguel UngsodNo ratings yet

- Midterm Examination BSAISDocument11 pagesMidterm Examination BSAISAlexis Kaye DayagNo ratings yet

- Tax2 FinalsDocument8 pagesTax2 FinalsKevin Elrey Arce100% (2)

- DocxDocument28 pagesDocxGrace Managuelod GabuyoNo ratings yet

- TAX2UNIT9TO12Document4 pagesTAX2UNIT9TO12Catherine Joy VasayaNo ratings yet

- Prelim Examination. AY 2nd SEM 2023 2024Document5 pagesPrelim Examination. AY 2nd SEM 2023 2024amseservices18No ratings yet

- Tax Lecture VATDocument4 pagesTax Lecture VATRozzane Ann RomaNo ratings yet

- Agricultural tax exemptions quizDocument19 pagesAgricultural tax exemptions quizJona Celle Castillo100% (1)

- 1.2. Problems On VAT - For Tax ReviewDocument19 pages1.2. Problems On VAT - For Tax ReviewJem ValmonteNo ratings yet

- VAT ReviewDocument8 pagesVAT ReviewabbyNo ratings yet

- PrefinalDocument7 pagesPrefinalLeisleiRagoNo ratings yet

- Dimla Selene S Assignment On Aggregate PlanningDocument3 pagesDimla Selene S Assignment On Aggregate PlanningSelene DimlaNo ratings yet

- The Activities and Time Estimates For A Particular Project Are As Follows. A. Construct The Network DiagramDocument2 pagesThe Activities and Time Estimates For A Particular Project Are As Follows. A. Construct The Network DiagramSelene DimlaNo ratings yet

- Dimla Selene 03 JournalDocument3 pagesDimla Selene 03 JournalSelene DimlaNo ratings yet

- Chapter 7 - Regular Output VATDocument17 pagesChapter 7 - Regular Output VATSelene DimlaNo ratings yet

- Introduction To Consumption Taxes NotesDocument2 pagesIntroduction To Consumption Taxes NotesSelene DimlaNo ratings yet

- VAT On Importation NotesDocument1 pageVAT On Importation NotesSelene DimlaNo ratings yet

- Exempt Sale of Goods Properties and Services NotesDocument2 pagesExempt Sale of Goods Properties and Services NotesSelene DimlaNo ratings yet

- Business Taxation NotesDocument2 pagesBusiness Taxation NotesSelene DimlaNo ratings yet

- Wrangler Jeans (Greensboro, North Carolina, USA) Form 6166-Certification of U.S. Tax ResidencyDocument2 pagesWrangler Jeans (Greensboro, North Carolina, USA) Form 6166-Certification of U.S. Tax ResidencyEman VillacorteNo ratings yet

- PMIS Code Servicebook PDFDocument1 pagePMIS Code Servicebook PDFPrakash kumarNo ratings yet

- SMV Updating and General Revision and General Revision of Real Property AssessmentsDocument27 pagesSMV Updating and General Revision and General Revision of Real Property Assessmentseva t. abrasaldo100% (1)

- VAT on Importation and Consumption Taxes ExplainedDocument4 pagesVAT on Importation and Consumption Taxes ExplainedJamaica DavidNo ratings yet

- Goods and Services TaxDocument5 pagesGoods and Services TaxphukerakeshraoNo ratings yet

- Tax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Document1 pageTax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Jyoti MorkundeNo ratings yet

- Employee Loan Grant FormatDocument2 pagesEmployee Loan Grant FormatDawit SolomonNo ratings yet

- My - Invoice - 2 Aug 2021, 23 - 01 - 47 - 300573249965Document2 pagesMy - Invoice - 2 Aug 2021, 23 - 01 - 47 - 300573249965Bibhor KumarNo ratings yet

- Calculating Salaries, Wages and Minimum Wage RatesDocument24 pagesCalculating Salaries, Wages and Minimum Wage RatesjohnNo ratings yet

- ONETT - RMO 15-2003 - Policies&GuidelinesDocument19 pagesONETT - RMO 15-2003 - Policies&GuidelineszneraNo ratings yet

- 143-Article Text-481-1-10-20210326Document12 pages143-Article Text-481-1-10-20210326Tania LystiaNo ratings yet

- 2 - PBC VS Cir - GR No 194065Document4 pages2 - PBC VS Cir - GR No 194065Sopongco ColeenNo ratings yet

- On January 1 2015 Evers Company Purchased The Following Two: Unlock Answers Here Solutiondone - OnlineDocument1 pageOn January 1 2015 Evers Company Purchased The Following Two: Unlock Answers Here Solutiondone - OnlineAmit PandeyNo ratings yet

- BIR VAT Ruling No. 076-99Document3 pagesBIR VAT Ruling No. 076-99Adrian CabanaNo ratings yet

- Go Digit General Insurance Limited Financials Income StatementDocument3 pagesGo Digit General Insurance Limited Financials Income StatementShuchita AgarwalNo ratings yet

- Zimbabwe - OverviewDocument4 pagesZimbabwe - OverviewdumidlodloNo ratings yet

- Liability of JDA entered prior to GST when SA is entered post GSTDocument3 pagesLiability of JDA entered prior to GST when SA is entered post GSTKunalKumarNo ratings yet

- Invoice SA2022-2765Document1 pageInvoice SA2022-2765OlegNo ratings yet

- Memorial For RespondentDocument28 pagesMemorial For Respondentdevil_3565100% (1)

- Coral Bay Nickel v. CIR PDFDocument10 pagesCoral Bay Nickel v. CIR PDFLiz KawiNo ratings yet

- Solar Purchase BillDocument2 pagesSolar Purchase BillMansi ShahNo ratings yet

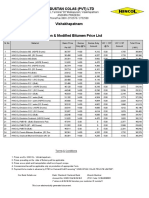

- HINDUSTAN COLAS Emulsion & Modified Bitumen Price ListDocument2 pagesHINDUSTAN COLAS Emulsion & Modified Bitumen Price ListRama Raju Gottumukkala0% (1)

- Evaluate 1 - Estate Taxation Answer KeyDocument3 pagesEvaluate 1 - Estate Taxation Answer KeyNicolas AlonsoNo ratings yet

- Amount claimed for work period May-Aug 2006Document3 pagesAmount claimed for work period May-Aug 2006anup jenaNo ratings yet

- Learn key income reporting principlesDocument15 pagesLearn key income reporting principlesRoligen Rose PachicoyNo ratings yet

- Foreign Account Tax ComlianceDocument66 pagesForeign Account Tax Comliancegaurav.oza393No ratings yet

- InvoiceDocument1 pageInvoiceHemant YadavNo ratings yet

- 175,120.00 31555288280 42,409.00 132,711.00 Credited To: SBI, DIGWADIHDocument1 page175,120.00 31555288280 42,409.00 132,711.00 Credited To: SBI, DIGWADIHshamb2020No ratings yet