You might also like

- Optimal Mean Reversion TradingDocument26 pagesOptimal Mean Reversion TradingyurijapNo ratings yet

- SSRN Id2222196Document26 pagesSSRN Id2222196hzauccgNo ratings yet

- Optimal Trading With A Trailing Stop: Tim Leung Hongzhong Zhang February 18, 2019Document26 pagesOptimal Trading With A Trailing Stop: Tim Leung Hongzhong Zhang February 18, 2019SrinivasaNo ratings yet

- Calculating Convexity Adjustment for Interest Rates Using Martingale TheoryDocument18 pagesCalculating Convexity Adjustment for Interest Rates Using Martingale Theoryswinki3No ratings yet

- Optimal Trend Following Trading RulesDocument25 pagesOptimal Trend Following Trading RulesDavid PopleNo ratings yet

- Stochastic Analysis in Finance and InsuranceDocument16 pagesStochastic Analysis in Finance and InsurancepostscriptNo ratings yet

- SSRN Id1762118Document25 pagesSSRN Id1762118parkjoonsuuNo ratings yet

- Gauge Invariance, Geometry and Arbitrage: Samuel E. VázquezDocument44 pagesGauge Invariance, Geometry and Arbitrage: Samuel E. VázquezLeyti DiengNo ratings yet

- Bouchard, Dang, Lehalle - Optimal Control of Trading Algorithms - A General Impulse Control ApproachDocument30 pagesBouchard, Dang, Lehalle - Optimal Control of Trading Algorithms - A General Impulse Control ApproachnguyenhoangnguyenntNo ratings yet

- Optimal High-Frequency Market Making StrategyDocument19 pagesOptimal High-Frequency Market Making StrategyJose Antonio Dos Ramos100% (3)

- Buy Low Sell HighDocument20 pagesBuy Low Sell HighDamon BankheadNo ratings yet

- Estimating A Regime Switching Pairs Trading Model: Robert J. Elliott and Reza BradraniaDocument16 pagesEstimating A Regime Switching Pairs Trading Model: Robert J. Elliott and Reza Bradraniawilcox99No ratings yet

- Optimal Algorithms For Online Time Series Search and One-Way Trading With Interrelated Prices PDFDocument8 pagesOptimal Algorithms For Online Time Series Search and One-Way Trading With Interrelated Prices PDFhall hallNo ratings yet

- Comparing Risk of Sharia and Non-Sharia Stocks in IndonesiaDocument13 pagesComparing Risk of Sharia and Non-Sharia Stocks in IndonesiarifkaindiNo ratings yet

- Pairs Trading: An Implementation of The Stochastic Spread and Cointegration ApproachDocument29 pagesPairs Trading: An Implementation of The Stochastic Spread and Cointegration ApproachRichard BertemattiNo ratings yet

- Some of Existing Method of Pair TradingDocument11 pagesSome of Existing Method of Pair TradingKapilNo ratings yet

- r93723092 FinalDocument29 pagesr93723092 Final吳明世No ratings yet

- From Implied To Spot Volatilities: Valdo DurrlemanDocument21 pagesFrom Implied To Spot Volatilities: Valdo DurrlemanginovainmonaNo ratings yet

- Optimal high-frequency trading with predictive informationDocument26 pagesOptimal high-frequency trading with predictive informationFabien GuilbaudNo ratings yet

- PAIRS TRADING MODELDocument7 pagesPAIRS TRADING MODELkabinskyNo ratings yet

- SSRN Id4264823Document48 pagesSSRN Id4264823fermetabouvheNo ratings yet

- Modeling Long-Run Relationships in FinanceDocument43 pagesModeling Long-Run Relationships in FinanceInge AngeliaNo ratings yet

- The FundamentalThe Fundamental Theorem of Derivative Trading - Exposition, Extensions, and Experiments Theorem of Derivative Trading - Exposition, Extensions, and ExperimentsDocument27 pagesThe FundamentalThe Fundamental Theorem of Derivative Trading - Exposition, Extensions, and Experiments Theorem of Derivative Trading - Exposition, Extensions, and ExperimentsNattapat BunyuenyongsakulNo ratings yet

- Entropy 21 00530 v2Document10 pagesEntropy 21 00530 v2Guilherme ChagasNo ratings yet

- 1705.04780 MatlabDocument49 pages1705.04780 MatlabNoureddineLahouelNo ratings yet

- An Investment Strategy Based On Stochastic Unit Root ModelsDocument8 pagesAn Investment Strategy Based On Stochastic Unit Root ModelsHusain SulemaniNo ratings yet

- 10-1108_03074350310768517Document19 pages10-1108_030743503107685171527351362No ratings yet

- Research StatementDocument5 pagesResearch Statementapi-572237590No ratings yet

- EricB Cms ConvexityDocument18 pagesEricB Cms ConvexitycountingNo ratings yet

- Trading Strategy With Stochastic Volatility in A Limit Order Book MarketDocument52 pagesTrading Strategy With Stochastic Volatility in A Limit Order Book MarketNapolnzoNo ratings yet

- Deep Reinforcement Learning For Algorithmic Trading: 1.0.1 Learning in Financial MarketsDocument24 pagesDeep Reinforcement Learning For Algorithmic Trading: 1.0.1 Learning in Financial MarketsQuant TradingNo ratings yet

- Jaksa: Department of Statistics, Columbia University, New York, NYDocument34 pagesJaksa: Department of Statistics, Columbia University, New York, NYaliNo ratings yet

- Optimal Turnover, Liquidity, and Autocorrelation: Bastien Baldacci, Jerome Benveniste and Gordon Ritter January 26, 2022Document11 pagesOptimal Turnover, Liquidity, and Autocorrelation: Bastien Baldacci, Jerome Benveniste and Gordon Ritter January 26, 2022Lexus1SaleNo ratings yet

- Complete Market ModelsDocument16 pagesComplete Market Modelsmeko1986No ratings yet

- Optimal Hedging Using CointegrationDocument23 pagesOptimal Hedging Using CointegrationRICARDONo ratings yet

- Arbitrage and Equilibrium in Economies With Short-Selling and AmbiguityDocument17 pagesArbitrage and Equilibrium in Economies With Short-Selling and AmbiguityNamNo ratings yet

- Teaching Note 00-04: Girsanov'S Theorem in Derivative PricingDocument16 pagesTeaching Note 00-04: Girsanov'S Theorem in Derivative PricingVeeken ChaglassianNo ratings yet

- A Mathematical Analysis of Technical AnalysisDocument30 pagesA Mathematical Analysis of Technical AnalysisAlan GoodridgeNo ratings yet

- A Differential Oligopoly Game With Differentiated Goods and Sticky PricesDocument14 pagesA Differential Oligopoly Game With Differentiated Goods and Sticky PricesDiniMaulinaNo ratings yet

- An Application of Symmetry Approach To Finance - Gauge Symmetry in FinanceDocument13 pagesAn Application of Symmetry Approach To Finance - Gauge Symmetry in FinanceFcking GamerzNo ratings yet

- IntrinsicPricesOfRisk TrucLe LibreDocument11 pagesIntrinsicPricesOfRisk TrucLe LibreMuhammad A. NaeemNo ratings yet

- Modification of Warrants Pricing ModelDocument8 pagesModification of Warrants Pricing ModelTrader CatNo ratings yet

- Monte Carlo Methods in Finance An Introductory TutDocument10 pagesMonte Carlo Methods in Finance An Introductory TutNicolas LeãoNo ratings yet

- Economic Modelling: Miao Zhang, Ping Chen, Haixiang YaoDocument8 pagesEconomic Modelling: Miao Zhang, Ping Chen, Haixiang YaoannyNo ratings yet

- Dealing With The Inventory Risk: A Solution To The Market Making ProblemDocument31 pagesDealing With The Inventory Risk: A Solution To The Market Making Problemluminous blueNo ratings yet

- High-frequency trading in a limit order book strategyDocument13 pagesHigh-frequency trading in a limit order book strategyKwok Chung ChuNo ratings yet

- Asset Pricing (안동현교수님강의노트)Document77 pagesAsset Pricing (안동현교수님강의노트)Tae Hyun HwangNo ratings yet

- Asian Options Under Multiscale Stochastic Volatility: Jean-Pierre Fouque and Chuan-Hsiang HanDocument14 pagesAsian Options Under Multiscale Stochastic Volatility: Jean-Pierre Fouque and Chuan-Hsiang Hanabhishek210585No ratings yet

- Quant Trading as a Mathematical ScienceDocument54 pagesQuant Trading as a Mathematical ScienceKofi Appiah-DanquahNo ratings yet

- Garch ModelDocument3 pagesGarch ModelFaroq OmarNo ratings yet

- SSRN Id593584Document28 pagesSSRN Id593584Loulou DePanamNo ratings yet

- No 76Document44 pagesNo 76eeeeewwwwwwwwNo ratings yet

- JeanninIoriSamuels PinningDocument12 pagesJeanninIoriSamuels PinningginovainmonaNo ratings yet

- Barrier Hedge RevisedDocument33 pagesBarrier Hedge RevisedmpgentNo ratings yet

- Optimal Prediction of Resistance and Support Levels - School of (PDFDrive)Document18 pagesOptimal Prediction of Resistance and Support Levels - School of (PDFDrive)chandansingh45No ratings yet

- Feweco 20030708115600Document16 pagesFeweco 20030708115600Aditya GuptaNo ratings yet

- Whaley+Wilmott TheBestHedgingStrategyDocument5 pagesWhaley+Wilmott TheBestHedgingStrategydlr1949No ratings yet

- Hedging and Portfolio Optimization in Financial Markets With A Large TraderDocument24 pagesHedging and Portfolio Optimization in Financial Markets With A Large TraderJohn DoesNo ratings yet

- C 15000L 1Document2 pagesC 15000L 1เสกสรรค์ จันทร์สุขปลูกNo ratings yet

- Cal TankDocument2 pagesCal Tankเสกสรรค์ จันทร์สุขปลูกNo ratings yet

- Cal T 1Document2 pagesCal T 1เสกสรรค์ จันทร์สุขปลูกNo ratings yet

- Performance Analysis and Optimized Design of BackwDocument29 pagesPerformance Analysis and Optimized Design of BackwashnekNo ratings yet

- Cal T 1Document2 pagesCal T 1เสกสรรค์ จันทร์สุขปลูกNo ratings yet

- Momentum Grid - 1.8+BB Band Usd Midle BandDocument23 pagesMomentum Grid - 1.8+BB Band Usd Midle Bandเสกสรรค์ จันทร์สุขปลูกNo ratings yet

- Zick AnalysisDocument12 pagesZick AnalysisrksahayNo ratings yet

- 3Document1 page3เสกสรรค์ จันทร์สุขปลูกNo ratings yet

- Mean Diameter DDocument2 pagesMean Diameter Dเสกสรรค์ จันทร์สุขปลูกNo ratings yet

- REP Frax 06 11 20Document47 pagesREP Frax 06 11 20เสกสรรค์ จันทร์สุขปลูกNo ratings yet

- Dongfeng: Technical SpecificationsDocument2 pagesDongfeng: Technical Specificationsเสกสรรค์ จันทร์สุขปลูกNo ratings yet

- Conversion of CNG, Liter To KGDocument1 pageConversion of CNG, Liter To KGเสกสรรค์ จันทร์สุขปลูกNo ratings yet

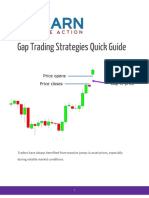

- Gap Trading Strategies Quick GuideDocument9 pagesGap Trading Strategies Quick GuideFauzi BNo ratings yet

- SWB Grid 4.1 CandleDocument14 pagesSWB Grid 4.1 Candleเสกสรรค์ จันทร์สุขปลูก100% (1)

- Bought Bitcoin Last Year? Here's How To Save Money On Your Crypto TaxesDocument6 pagesBought Bitcoin Last Year? Here's How To Save Money On Your Crypto TaxesNikhil SharmaNo ratings yet

- Security Assessment Wault-Finance: May THDocument13 pagesSecurity Assessment Wault-Finance: May THเสกสรรค์ จันทร์สุขปลูกNo ratings yet

- What Is An "Event Driven" Hedge Strategy?: Hypothetical Example: An Educated Bet On A Deal Getting DoneDocument2 pagesWhat Is An "Event Driven" Hedge Strategy?: Hypothetical Example: An Educated Bet On A Deal Getting Doneเสกสรรค์ จันทร์สุขปลูกNo ratings yet

- Sale and Service PointDocument2 pagesSale and Service Pointเสกสรรค์ จันทร์สุขปลูกNo ratings yet

- Mean Reversion Trading Strategies PDFDocument7 pagesMean Reversion Trading Strategies PDFเสกสรรค์ จันทร์สุขปลูกNo ratings yet

- Momentum Trading Strategies Quick GuideDocument11 pagesMomentum Trading Strategies Quick Guideเสกสรรค์ จันทร์สุขปลูกNo ratings yet

- Trading Multiple Mean ReversionDocument37 pagesTrading Multiple Mean Reversionเสกสรรค์ จันทร์สุขปลูก100% (1)

- The Theory and Operation of Pressure Reducing Regulators PDFDocument44 pagesThe Theory and Operation of Pressure Reducing Regulators PDFGabriel ArghiriadeNo ratings yet

- 3Document2 pages3เสกสรรค์ จันทร์สุขปลูกNo ratings yet

- Plant laout - สยามอาภาฟู๊ดDocument1 pagePlant laout - สยามอาภาฟู๊ดเสกสรรค์ จันทร์สุขปลูกNo ratings yet

- FOUNDATION PW-Model PDFDocument1 pageFOUNDATION PW-Model PDFเสกสรรค์ จันทร์สุขปลูกNo ratings yet

- 3054470316F1Document55 pages3054470316F1เสกสรรค์ จันทร์สุขปลูกNo ratings yet

- Parts of System For Sequential Injection of CNG To Engine - PPMDocument1 pageParts of System For Sequential Injection of CNG To Engine - PPMเสกสรรค์ จันทร์สุขปลูกNo ratings yet

- 1perhitungan Soal SPM 2Document37 pages1perhitungan Soal SPM 2RamaNo ratings yet

- Assignment 1Document3 pagesAssignment 1Zhi Jin LouNo ratings yet

- Audit of Accounts Receivable and Related Accounts ComDocument3 pagesAudit of Accounts Receivable and Related Accounts ComCJ alandyNo ratings yet

- RFP Technical Proposal SummaryDocument11 pagesRFP Technical Proposal SummaryJheisson AlvarezNo ratings yet

- Resentettlement PlanDocument185 pagesResentettlement PlanPranoy BaruaNo ratings yet

- The History of Handmade Wooden BowlsDocument7 pagesThe History of Handmade Wooden BowlsLeo BjorkegrenNo ratings yet

- GEKKON GeylDocument12 pagesGEKKON Geylmarcica2100% (2)

- Development Formulation: Face and Décolleté Anti-Ageing Oily Jelly SE0010W With Matrixyl Morphomics™ and Juvinity™ ( )Document2 pagesDevelopment Formulation: Face and Décolleté Anti-Ageing Oily Jelly SE0010W With Matrixyl Morphomics™ and Juvinity™ ( )Widy PjanicNo ratings yet

- List of Scheduled Operator'S Permit HoldersDocument7 pagesList of Scheduled Operator'S Permit Holdersमनीष कुमारNo ratings yet

- Legal Review Draft Subcontract COMINCODocument7 pagesLegal Review Draft Subcontract COMINCOSon PhanNo ratings yet

- 22 XXX XXX TP Cibil ReportDocument5 pages22 XXX XXX TP Cibil ReportMahakaal Digital PointNo ratings yet

- Auditing and Assurance ServicesDocument69 pagesAuditing and Assurance Servicesgilli1tr100% (1)

- The Modern World-System As A Capitalist World-Economy Production, Surplus Value, and PolarizationDocument11 pagesThe Modern World-System As A Capitalist World-Economy Production, Surplus Value, and PolarizationLee ValenzuelaNo ratings yet

- Ballada - Chapters 2-6Document7 pagesBallada - Chapters 2-6Patricia Camille Austria0% (1)

- Survey RequestDocument2 pagesSurvey RequestsunmarineNo ratings yet

- Silicon Valley countersignalling signals tech focus over statusDocument18 pagesSilicon Valley countersignalling signals tech focus over status서은수No ratings yet

- Zonal Values for Municipalities in Mountain ProvinceDocument83 pagesZonal Values for Municipalities in Mountain ProvinceAj TactayNo ratings yet

- What Do TIPS Say About Real Interest Rates and Required ReturnsDocument25 pagesWhat Do TIPS Say About Real Interest Rates and Required ReturnsKamel RamtanNo ratings yet

- Bramall - Industrialization of Rural ChinaDocument437 pagesBramall - Industrialization of Rural ChinaMatthew ChalkNo ratings yet

- Explosion-proof fluorescent lighting fittingsDocument6 pagesExplosion-proof fluorescent lighting fittingsDandi ZulkarnainNo ratings yet

- Cooling - Temperature RegulationDocument12 pagesCooling - Temperature RegulationAlper SakalsizNo ratings yet

- Self Help Complete PDFDocument35 pagesSelf Help Complete PDFSubodh NigamNo ratings yet

- Bill To / Ship To:: Qty Gross Amount Discount Other Charges Taxable Amount CGST SGST/ Ugst Igst Cess Total AmountDocument2 pagesBill To / Ship To:: Qty Gross Amount Discount Other Charges Taxable Amount CGST SGST/ Ugst Igst Cess Total AmountPadma GouteNo ratings yet

- Sandvik CH 660-32-33Document2 pagesSandvik CH 660-32-33Damaris OrtizNo ratings yet

- Homework of Chapter 25 Production and GrowthDocument5 pagesHomework of Chapter 25 Production and GrowthMunkh-Erdene OtgonboldNo ratings yet

- North Lanarkshire Supplier CharterDocument20 pagesNorth Lanarkshire Supplier CharterKav99No ratings yet

- Chapter 4Document5 pagesChapter 4Billy Vince AlquinoNo ratings yet

- Harari LiberalDocument6 pagesHarari LiberalVictor MoliariNo ratings yet

- INTL ECON CHAPTER 1Document20 pagesINTL ECON CHAPTER 1Jubayer 3DNo ratings yet