You might also like

- Payroll ProjectDocument16 pagesPayroll ProjectKatrina Rardon-Swoboda68% (25)

- Hynum Greg Angela - 20i - CCDocument76 pagesHynum Greg Angela - 20i - CCAdmin OfficeNo ratings yet

- Mar 2023Document1 pageMar 2023Aditya PLNo ratings yet

- PPT-on-GST Annual-ReturnDocument33 pagesPPT-on-GST Annual-Returnshrutha p jainNo ratings yet

- GST Return Business Process For GSTDocument72 pagesGST Return Business Process For GSTAccounting & Taxation100% (1)

- FORM GSTR-2B - Advisory (Available Under "Advisory" Tab of GSTR-2B) Terms UsedDocument4 pagesFORM GSTR-2B - Advisory (Available Under "Advisory" Tab of GSTR-2B) Terms UsedSachin KNNo ratings yet

- Advisory 2710 2Document20 pagesAdvisory 2710 2Pushpraj SinghNo ratings yet

- Faqs Viewing Form Gstr-2B Form Gstr-2B: TH TH TH THDocument5 pagesFaqs Viewing Form Gstr-2B Form Gstr-2B: TH TH TH THAsh WNo ratings yet

- Cir 170 02 2022 CGSTDocument7 pagesCir 170 02 2022 CGSTTushar AgrawalNo ratings yet

- TaxMarvel - Modifications in Form GSTR 3B and New Disclosure RequirementsDocument5 pagesTaxMarvel - Modifications in Form GSTR 3B and New Disclosure RequirementsAmit AgrawalNo ratings yet

- Difference between GSTR-2A and GSTR-2B auto-generated GST returnsDocument4 pagesDifference between GSTR-2A and GSTR-2B auto-generated GST returnsdevNo ratings yet

- Statement Outwrad SupplyDocument4 pagesStatement Outwrad SupplyTushar GoelNo ratings yet

- Faqs Form Gstr-2ADocument3 pagesFaqs Form Gstr-2AAsh WNo ratings yet

- Latest Updation in GSTN PortalDocument47 pagesLatest Updation in GSTN PortalVenkat BalaNo ratings yet

- Faqs Form Gstr-3B About Form Gstr-3BDocument8 pagesFaqs Form Gstr-3B About Form Gstr-3BAsh WNo ratings yet

- Chapter 11 GST ReturnsDocument18 pagesChapter 11 GST ReturnsDR. PREETI JINDALNo ratings yet

- Returns: FAQ'sDocument25 pagesReturns: FAQ'smun1barejaNo ratings yet

- Action For Difference in ITC Between 3B and 2ADocument46 pagesAction For Difference in ITC Between 3B and 2Aphani raja kumarNo ratings yet

- Insertion of New Tables in GSTR-1Document5 pagesInsertion of New Tables in GSTR-1rvsiddharth054No ratings yet

- GSTR-9 ArticleDocument8 pagesGSTR-9 Articlecihoni1143No ratings yet

- GSTR 9 9C FY 22 23 DUE 31st December 2023 1694345252Document7 pagesGSTR 9 9C FY 22 23 DUE 31st December 2023 1694345252RajatNo ratings yet

- Key Highlights of Simplified Form GSTR 9 and Form GSTR 9c PDFDocument2 pagesKey Highlights of Simplified Form GSTR 9 and Form GSTR 9c PDFPriyanka BahiratNo ratings yet

- Step by Step Compliances Under RCM: How Composition Dealer Will Be Affected by RCM?Document7 pagesStep by Step Compliances Under RCM: How Composition Dealer Will Be Affected by RCM?arpit jainNo ratings yet

- New Functionalities Compilation Aug 2022Document3 pagesNew Functionalities Compilation Aug 2022AmanNo ratings yet

- GST Reports ListsDocument8 pagesGST Reports Listsmandarjejurikar100% (1)

- How To Handle Difference of Itc Availed inDocument5 pagesHow To Handle Difference of Itc Availed inNishanth SrinivasNo ratings yet

- GST Returns and ComplianceDocument11 pagesGST Returns and ComplianceJay PawarNo ratings yet

- Goods & Services Tax (GST) News and Updates 2Document1 pageGoods & Services Tax (GST) News and Updates 2Terin IsaacNo ratings yet

- GST Annual Return and AuditDocument34 pagesGST Annual Return and Auditdasari satishNo ratings yet

- GST Annual Return ClarificationDocument3 pagesGST Annual Return ClarificationMukesh ChhadvaNo ratings yet

- Chapter 8 - Input Tax CreditDocument21 pagesChapter 8 - Input Tax Creditmadaanakansha91No ratings yet

- Record Notebook Faculty of Arts & Commerce Department of Cost & Management Accounting (Cma)Document16 pagesRecord Notebook Faculty of Arts & Commerce Department of Cost & Management Accounting (Cma)Sha dowNo ratings yet

- Cir 183 15 2022 CGSTDocument5 pagesCir 183 15 2022 CGSTAmritesh RaiNo ratings yet

- Press Release Clarification Regarding Annual Returns and Reconciliation StatementDocument3 pagesPress Release Clarification Regarding Annual Returns and Reconciliation StatementSujata OjhaNo ratings yet

- Relief for ITC Claimed in GSTR 2A Circular IssuedDocument3 pagesRelief for ITC Claimed in GSTR 2A Circular Issuedsanket lunkadNo ratings yet

- Circular CGST 123Document4 pagesCircular CGST 123AKSHATANo ratings yet

- GST Annual Return TypesDocument24 pagesGST Annual Return TypesPushpraj SinghNo ratings yet

- GST Circular clarifies ITC rules for Feb-Aug 2020Document3 pagesGST Circular clarifies ITC rules for Feb-Aug 2020Gulrana AlamNo ratings yet

- Instructions ITR5 AY2021 22Document196 pagesInstructions ITR5 AY2021 22Nikhil KumarNo ratings yet

- Circular CGST 197Document5 pagesCircular CGST 197Jaipur-B Gr-2No ratings yet

- GSTR-9 filing guide for FY 2018-19Document25 pagesGSTR-9 filing guide for FY 2018-19nana DuttaNo ratings yet

- GST - GOODS & Service Tax What Is GSTDocument4 pagesGST - GOODS & Service Tax What Is GSTsubbiah kailasamNo ratings yet

- Presentation 09.03.2017 CA - Shivani ShahDocument29 pagesPresentation 09.03.2017 CA - Shivani ShahPARESH KUVADIYANo ratings yet

- Instructions For Filling Out FORM ITR 3Document231 pagesInstructions For Filling Out FORM ITR 3Samantha JNo ratings yet

- Instructions GSTR-9Document9 pagesInstructions GSTR-9pankajNo ratings yet

- GSTR-9 & 9C TrainingDocument2 pagesGSTR-9 & 9C TrainingKavita RanaNo ratings yet

- All About GST Annual ReturnsDocument9 pagesAll About GST Annual ReturnsinfoNo ratings yet

- Instructions For Form GSTR-9Document8 pagesInstructions For Form GSTR-9param.ginniNo ratings yet

- GST Circular-Restriction in Availment of ITC-Rule 36Document3 pagesGST Circular-Restriction in Availment of ITC-Rule 36Tejas RajkotiaNo ratings yet

- Clarification Regarding Annual Returns and Reconciliation StatementDocument4 pagesClarification Regarding Annual Returns and Reconciliation StatementTIRLOK NATH JaggiNo ratings yet

- Goods and Services Tax - Payment of Taxes & Filing of Form GSTR-3B ReturnDocument45 pagesGoods and Services Tax - Payment of Taxes & Filing of Form GSTR-3B ReturnANAND AND COMPANYNo ratings yet

- Form 9C Clarification 3.7.19Document2 pagesForm 9C Clarification 3.7.19ashim1No ratings yet

- GST Automated NoticesDocument6 pagesGST Automated NoticesMaunik ParikhNo ratings yet

- Circular 19 2020Document2 pagesCircular 19 2020rnathNo ratings yet

- File ITR-2 Online User ManualDocument43 pagesFile ITR-2 Online User ManualsrtujyuNo ratings yet

- ITR-7 InstructionsDocument26 pagesITR-7 InstructionsUttam K SharmaNo ratings yet

- Mygov 1445315831190667 PDFDocument72 pagesMygov 1445315831190667 PDFjitendraktNo ratings yet

- Clause by Clause Analysis - Revenue - Outward SupplyDocument18 pagesClause by Clause Analysis - Revenue - Outward SupplyFAB BankNo ratings yet

- Circular No 10 2022Document4 pagesCircular No 10 2022Shobhit ShuklaNo ratings yet

- Claim of ITC As GSTR-2B Is Mandatory W.E.F. 01.01.2022Document3 pagesClaim of ITC As GSTR-2B Is Mandatory W.E.F. 01.01.2022ravindra kumar jainNo ratings yet

- Section 61 of The CGST ActDocument2 pagesSection 61 of The CGST ActBipin DurgapalNo ratings yet

- GSRG 405 PT 1Document17 pagesGSRG 405 PT 1LaLa BanksNo ratings yet

- Industrial Enterprises Act 2020 (2076): A brief Overview and Comparative AnalysisFrom EverandIndustrial Enterprises Act 2020 (2076): A brief Overview and Comparative AnalysisNo ratings yet

- QRMP-All Related Nofications & AmendmentsDocument6 pagesQRMP-All Related Nofications & AmendmentsV RawalNo ratings yet

- Aadhaar AuthenticationDocument14 pagesAadhaar AuthenticationV RawalNo ratings yet

- Hospital Audit Program Guide: For The Year Ended June 30, 2017Document187 pagesHospital Audit Program Guide: For The Year Ended June 30, 2017V RawalNo ratings yet

- Aadhaar AuthenticationDocument14 pagesAadhaar AuthenticationV RawalNo ratings yet

- Health Care Internal AuditDocument5 pagesHealth Care Internal Auditmark gmNo ratings yet

- Healthcare Audit Plan 2020 focuses on safetyDocument13 pagesHealthcare Audit Plan 2020 focuses on safetyV RawalNo ratings yet

- Healthcare Audit Plan 2020 focuses on safetyDocument13 pagesHealthcare Audit Plan 2020 focuses on safetyV RawalNo ratings yet

- Healthcare Audit Plan 2020 focuses on safetyDocument13 pagesHealthcare Audit Plan 2020 focuses on safetyV RawalNo ratings yet

- Health Care Internal AuditDocument5 pagesHealth Care Internal Auditmark gmNo ratings yet

- Hospital Audit Program Guide: For The Year Ended June 30, 2017Document187 pagesHospital Audit Program Guide: For The Year Ended June 30, 2017V RawalNo ratings yet

- Hospital Audit Program Guide: For The Year Ended June 30, 2017Document187 pagesHospital Audit Program Guide: For The Year Ended June 30, 2017V RawalNo ratings yet

- Cash and Accrual Basis ProblemsDocument1 pageCash and Accrual Basis ProblemsCAINo ratings yet

- Yes No: Vat-On Business Services-In General VB010 2,108,277.52 252,993.30 2,108,277.52 252,993.30Document1 pageYes No: Vat-On Business Services-In General VB010 2,108,277.52 252,993.30 2,108,277.52 252,993.30MJ TuliaoNo ratings yet

- Snacks Bill 110321Document1 pageSnacks Bill 110321Brahmananda ChakrabortyNo ratings yet

- Certificate Under Section 13Document5 pagesCertificate Under Section 13DEEPA ignatiusNo ratings yet

- Estate and Transfer Tax Concepts ExplainedDocument19 pagesEstate and Transfer Tax Concepts ExplainedCleah WaskinNo ratings yet

- No Plastic Packaging: Tax InvoiceDocument1 pageNo Plastic Packaging: Tax InvoicePROKLEAR NanoNo ratings yet

- Form 16: Wipro LimitedDocument8 pagesForm 16: Wipro Limitedvishnu reddyNo ratings yet

- Provident Fund InformationDocument2 pagesProvident Fund Informationsk_gazanfarNo ratings yet

- Quiz 3 InclusionsDocument4 pagesQuiz 3 InclusionshotgirlsummerNo ratings yet

- November SalaryDocument1 pageNovember SalarynikhilbNo ratings yet

- Chennai Plant Pricelist 16.05.2023-EmulsionDocument1 pageChennai Plant Pricelist 16.05.2023-EmulsionTeamleader MSV TuticorinNo ratings yet

- Aaak 75 MTDocument3 pagesAaak 75 MTChandresh MarthakNo ratings yet

- Preferential Taxation Module 3Document4 pagesPreferential Taxation Module 3Sophia De GuzmanNo ratings yet

- Solved Your Company Sponsors A 401 K Plan Into Which You DepositDocument1 pageSolved Your Company Sponsors A 401 K Plan Into Which You DepositM Bilal SaleemNo ratings yet

- MObile InvoiceDocument1 pageMObile Invoicechandra kiran KodavatiNo ratings yet

- Noise Watch InvoiceDocument1 pageNoise Watch Invoicenik1522No ratings yet

- Mukesh Electric & Hardware Stores: Tax InvoiceDocument1 pageMukesh Electric & Hardware Stores: Tax Invoiceshafi shaikh100% (1)

- Coi (Ay 22-23)Document2 pagesCoi (Ay 22-23)ParthNo ratings yet

- Like-Kind Exchanges: (And Section 1043 Conflict-Of-Interest Sales)Document2 pagesLike-Kind Exchanges: (And Section 1043 Conflict-Of-Interest Sales)Abdullah TheNo ratings yet

- Income Tax Fundamentals 2014 Whittenburg 32nd Edition Test Bank Chapters 1 5-7-12Document27 pagesIncome Tax Fundamentals 2014 Whittenburg 32nd Edition Test Bank Chapters 1 5-7-12KimberlyThomasknwy100% (40)

- Court of Tax Appeals: VENUE: Second Division Courtroom, 3Document3 pagesCourt of Tax Appeals: VENUE: Second Division Courtroom, 3Aemie JordanNo ratings yet

- SMART BIOMEDICAL SERVICES TAX INVOICEDocument3 pagesSMART BIOMEDICAL SERVICES TAX INVOICESmart BiomedicalNo ratings yet

- Firs Form 1 PDFDocument4 pagesFirs Form 1 PDFLugard WoduNo ratings yet

- ZWS ISO 9001:2008 QUALITY MANAGEMENT SYSTEM PAYE TAX TABLESDocument1 pageZWS ISO 9001:2008 QUALITY MANAGEMENT SYSTEM PAYE TAX TABLESTinovimba MawoyoNo ratings yet

- Solved Jesse Owns A Duplex Used As Residential Rental Property TheDocument1 pageSolved Jesse Owns A Duplex Used As Residential Rental Property TheAnbu jaromiaNo ratings yet

- TRAIN Act reforms aim for progressive taxationDocument3 pagesTRAIN Act reforms aim for progressive taxationRONNEL SECADRONNo ratings yet

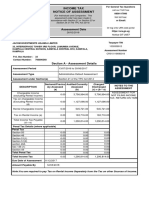

- Assessment Date: Income Tax Notice of AssessmentDocument2 pagesAssessment Date: Income Tax Notice of AssessmentBwana KuubwaNo ratings yet