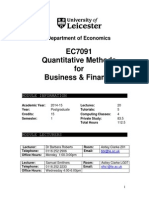

Quantitative Methods For Economists

Quantitative Methods For Economists

You might also like

- Econ 255-Course Outline 2022-2023 Academic YearDocument6 pagesEcon 255-Course Outline 2022-2023 Academic Yearrazak seiduNo ratings yet

- MATHSPRELIMSDocument15 pagesMATHSPRELIMSsalman_nsuNo ratings yet

- EC402 Syllabus 2019Document2 pagesEC402 Syllabus 2019Arjun VarmaNo ratings yet

- Introduction and The Simple Linear Regression ModelDocument35 pagesIntroduction and The Simple Linear Regression ModelNazmul H. PalashNo ratings yet

- Vickers PVB MVB Piston PumpDocument29 pagesVickers PVB MVB Piston Pumppablo cofreNo ratings yet

- Introduction To Quantitative Methods For EconomistsDocument8 pagesIntroduction To Quantitative Methods For EconomistsHenizionNo ratings yet

- BT11803 Syllabus-MQA Format-Revised (SPE Standard)Document4 pagesBT11803 Syllabus-MQA Format-Revised (SPE Standard)Lala Thebunker'sNo ratings yet

- 0 - Introduction PDFDocument3 pages0 - Introduction PDFDan EnzerNo ratings yet

- Applied Statistics and EconometricsDocument149 pagesApplied Statistics and EconometricsglenlcyNo ratings yet

- Economics, Finance, Financial EngineeringDocument147 pagesEconomics, Finance, Financial EngineeringJohn BonJoviNo ratings yet

- Econ 303 OutlineDocument5 pagesEcon 303 OutlineMary Catherine Almonte - EmbateNo ratings yet

- Maths For Macro SyllabusDocument2 pagesMaths For Macro SyllabusAvijit PuriNo ratings yet

- Std11 Maths EM 1Document271 pagesStd11 Maths EM 1Shrey SagarNo ratings yet

- 708-Kaido Class NotesDocument6 pages708-Kaido Class Noteshimanshoo panwarNo ratings yet

- ECON 262-Mathematical Applications in Economics-Kiran AroojDocument4 pagesECON 262-Mathematical Applications in Economics-Kiran AroojHaris Ali0% (1)

- 11 Mathematical Economics CH 1 Lecture 1Document38 pages11 Mathematical Economics CH 1 Lecture 1hanataye37No ratings yet

- Syllabus - Mathematics For Economics - 2021Document3 pagesSyllabus - Mathematics For Economics - 2021oanh nguyen pham oanhNo ratings yet

- Econ 130 C.outline 2023Document3 pagesEcon 130 C.outline 2023gacharagodwinNo ratings yet

- EPM 5131 Course OutlineDocument3 pagesEPM 5131 Course OutlineDivine MunsakaNo ratings yet

- 41 CisDocument2 pages41 CishokhmologNo ratings yet

- Introduction To Matiiematical EconomicsDocument5 pagesIntroduction To Matiiematical EconomicsNeeresh KumarNo ratings yet

- Course Title: Introductory Mathematical Economics Credit Units: 3 Course Code: ECON 603Document3 pagesCourse Title: Introductory Mathematical Economics Credit Units: 3 Course Code: ECON 603rashiNo ratings yet

- ECON 3105 Adv Mathematical EconomicsDocument4 pagesECON 3105 Adv Mathematical Economicsaafaq2003No ratings yet

- Methods for Applied Macroeconomic ResearchFrom EverandMethods for Applied Macroeconomic ResearchRating: 3.5 out of 5 stars3.5/5 (3)

- Kapur J. Mathematical Modelling 1988Document278 pagesKapur J. Mathematical Modelling 1988murat aslan100% (3)

- M.A. Part I Semester I: Four Courses in Each of The Two Semesters For M.A in EconomicsDocument11 pagesM.A. Part I Semester I: Four Courses in Each of The Two Semesters For M.A in EconomicsHolly JohnsonNo ratings yet

- Maths StatsDocument2 pagesMaths StatsAnna KonsulovaNo ratings yet

- 9783110616125.de Gruyter - Algebraic Graph Theory Morphisms, Monoids and Matrices - Jul.2019Document344 pages9783110616125.de Gruyter - Algebraic Graph Theory Morphisms, Monoids and Matrices - Jul.2019Vaan HoolNo ratings yet

- Eco No MetricsDocument6 pagesEco No MetricsSirElwoodNo ratings yet

- EC3120 Mathematical EconomicsDocument2 pagesEC3120 Mathematical Economicsmrudder1999No ratings yet

- Introduction To Quantitative Methods in EconomicsDocument3 pagesIntroduction To Quantitative Methods in EconomicsVenkatesha PrabuNo ratings yet

- Elements of Econometrics Exam CommentariesDocument4 pagesElements of Econometrics Exam CommentariesAlex Absalamov0% (1)

- Mact 12Document2 pagesMact 12Seungho LeeNo ratings yet

- MT3170 Discrete Mathematics and AlgebraDocument2 pagesMT3170 Discrete Mathematics and Algebramrudder1999No ratings yet

- MTH3202 Numerical MethodsDocument3 pagesMTH3202 Numerical MethodsRonald EmanuelNo ratings yet

- QM 1 Course Manual 1013Document40 pagesQM 1 Course Manual 1013williamhoangNo ratings yet

- Statistics For Economist Course OutlineDocument13 pagesStatistics For Economist Course OutlineYishak HesagaNo ratings yet

- Math2099 s2 2014Document11 pagesMath2099 s2 2014AnjewGSNo ratings yet

- EC7091 Module Outine 2014-15Document11 pagesEC7091 Module Outine 2014-15winblacklist1507No ratings yet

- UloopuDocument5 pagesUloopuMystery_HazzNo ratings yet

- Eco 355 - 0 PDFDocument137 pagesEco 355 - 0 PDFbirhan hailieNo ratings yet

- Mathematics CurriculumDocument10 pagesMathematics Curriculumchewe cheweNo ratings yet

- BA Economics Mathematical Economics and Econometry PDFDocument104 pagesBA Economics Mathematical Economics and Econometry PDFSyed Haider Abbas KazmiNo ratings yet

- Econ DC-1Document42 pagesEcon DC-1aleyaray1995No ratings yet

- Econometrics 1Document74 pagesEconometrics 1Anunay ChoudharyNo ratings yet

- EBD Merged Notes-QuizDocument284 pagesEBD Merged Notes-QuizrcybervirusNo ratings yet

- Ecf480 FPD 1 2015 2Document2 pagesEcf480 FPD 1 2015 2richard kapimpaNo ratings yet

- Applications and Interpretations GUIDEDocument95 pagesApplications and Interpretations GUIDELia ChouNo ratings yet

- 05a Cis PDFDocument2 pages05a Cis PDFAnasaziXNo ratings yet

- Slide - MATEMATIKA EKONOMI 2023Document16 pagesSlide - MATEMATIKA EKONOMI 2023uunarjunNo ratings yet

- ECO308 - Week 1 - Lecture - NoteDocument8 pagesECO308 - Week 1 - Lecture - NoteAyinde Taofeeq OlusolaNo ratings yet

- Curriculum Designing and OrganizationDocument18 pagesCurriculum Designing and OrganizationJocelyn GaniaNo ratings yet

- Course Overview ST104ADocument4 pagesCourse Overview ST104A전민건100% (1)

- Mathematics and Statistics For Economics and FinanceDocument2 pagesMathematics and Statistics For Economics and FinanceVu100% (1)

- 14.128 Dynamic Optimization and Economic Applications (Recursive Methods)Document3 pages14.128 Dynamic Optimization and Economic Applications (Recursive Methods)JorgeNo ratings yet

- Stat Syllabus StatisticsDocument26 pagesStat Syllabus StatisticsAryan SinghNo ratings yet

- Math 8 Commom Core SyllabusDocument6 pagesMath 8 Commom Core Syllabusapi-261815606No ratings yet

- An Introduction to Mathematical Analysis for Economic Theory and EconometricsFrom EverandAn Introduction to Mathematical Analysis for Economic Theory and EconometricsNo ratings yet

- Dynamic Optimization, Second Edition: The Calculus of Variations and Optimal Control in Economics and ManagementFrom EverandDynamic Optimization, Second Edition: The Calculus of Variations and Optimal Control in Economics and ManagementRating: 3 out of 5 stars3/5 (3)

- Structural Analysis Intro1Document9 pagesStructural Analysis Intro1adylmaesNo ratings yet

- A227A227M-06 (2011) Standard Specification For Steel Wire, Cold-Drawn For Mechanical SpringsDocument4 pagesA227A227M-06 (2011) Standard Specification For Steel Wire, Cold-Drawn For Mechanical Springstjt4779No ratings yet

- Science Experiment: You Will NeedDocument2 pagesScience Experiment: You Will NeedDANIELA PAEZ SILVANo ratings yet

- MANUAL DE COILED TUBING (Schlumberger) PDFDocument10 pagesMANUAL DE COILED TUBING (Schlumberger) PDFJose Sostenes0% (1)

- 3D Basin and Petroleum System Modelling of Northern North SeaDocument17 pages3D Basin and Petroleum System Modelling of Northern North SeawahyuNo ratings yet

- Service Manual: Outdoor UnitDocument48 pagesService Manual: Outdoor Unitadeelyaseen1No ratings yet

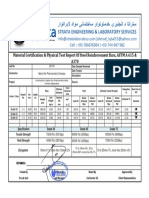

- Material Certification & Physical Test Report of Steel Reinforcement Bars, ASTM A 615 & A370Document1 pageMaterial Certification & Physical Test Report of Steel Reinforcement Bars, ASTM A 615 & A370Nasrullah Fazal AdeebNo ratings yet

- Crown Pillar Optimization For Surface To Underground Mine Transition in Erzincan/Bizmisen Iron MineDocument11 pagesCrown Pillar Optimization For Surface To Underground Mine Transition in Erzincan/Bizmisen Iron MineedwinpenadillomejiaNo ratings yet

- Effectiveness of Moringa Oleifera Seed As CoagulantDocument5 pagesEffectiveness of Moringa Oleifera Seed As CoagulantLuis Hernandez AlvarezNo ratings yet

- Oshas Technical Maual Part 1Document317 pagesOshas Technical Maual Part 1koteshwararaoNo ratings yet

- Etabloc Syt Operating InstructionsDocument50 pagesEtabloc Syt Operating InstructionsFayeez MukadamNo ratings yet

- F4 3systems of Equations (Answer)Document50 pagesF4 3systems of Equations (Answer)yiemetieNo ratings yet

- Probability Tree DiagramsDocument3 pagesProbability Tree DiagramsHaydn BassarathNo ratings yet

- Alcohol PDFDocument12 pagesAlcohol PDFXycca ValdezNo ratings yet

- FhsstmathsDocument201 pagesFhsstmathsMandyNo ratings yet

- LEP01153 - 02 Physics Demonstration Experiments - Magnet Board Mechanics 2Document3 pagesLEP01153 - 02 Physics Demonstration Experiments - Magnet Board Mechanics 2Jose GalvanNo ratings yet

- Physics Experiment - 2Document3 pagesPhysics Experiment - 2Sandipan SamantaNo ratings yet

- Lecture Notes - Optimization and Control PDFDocument405 pagesLecture Notes - Optimization and Control PDFShabih Ul HasanNo ratings yet

- Fourier Theory Made Easy (?)Document30 pagesFourier Theory Made Easy (?)gaurav_juneja_4No ratings yet

- Heat - Thermodynamics Virtual Lab - Physical Sciences - Amrita Vishwa Vidyapeetham Virtual LabDocument1 pageHeat - Thermodynamics Virtual Lab - Physical Sciences - Amrita Vishwa Vidyapeetham Virtual LabjeroldscdNo ratings yet

- GRAFIKDocument5 pagesGRAFIKNia YusNo ratings yet

- Magotteaux - XLIFT PaperDocument11 pagesMagotteaux - XLIFT PaperHamed MostafaNo ratings yet

- Kinametics Part 1Document25 pagesKinametics Part 1ARUNESH PRATAP SINGHNo ratings yet

- Sag and Tension Table For F Drop Wire: Heavy Ice Loading AreasDocument1 pageSag and Tension Table For F Drop Wire: Heavy Ice Loading AreaskikputririzNo ratings yet

- LinkNet ManualDocument38 pagesLinkNet ManualZahid JamilNo ratings yet

- Calculation of Second Moment of AreaDocument6 pagesCalculation of Second Moment of Areasweetpou_04No ratings yet

- Chapter 5: Classic & Smart Styrene: Presentation Petrochemical Production ProcessDocument14 pagesChapter 5: Classic & Smart Styrene: Presentation Petrochemical Production ProcesssamtomNo ratings yet

- PositionDocument5 pagesPositionberemiz009No ratings yet

You might also like

- Econ 255-Course Outline 2022-2023 Academic YearDocument6 pagesEcon 255-Course Outline 2022-2023 Academic Yearrazak seiduNo ratings yet

- MATHSPRELIMSDocument15 pagesMATHSPRELIMSsalman_nsuNo ratings yet

- EC402 Syllabus 2019Document2 pagesEC402 Syllabus 2019Arjun VarmaNo ratings yet

- Introduction and The Simple Linear Regression ModelDocument35 pagesIntroduction and The Simple Linear Regression ModelNazmul H. PalashNo ratings yet

- Vickers PVB MVB Piston PumpDocument29 pagesVickers PVB MVB Piston Pumppablo cofreNo ratings yet

- Introduction To Quantitative Methods For EconomistsDocument8 pagesIntroduction To Quantitative Methods For EconomistsHenizionNo ratings yet

- BT11803 Syllabus-MQA Format-Revised (SPE Standard)Document4 pagesBT11803 Syllabus-MQA Format-Revised (SPE Standard)Lala Thebunker'sNo ratings yet

- 0 - Introduction PDFDocument3 pages0 - Introduction PDFDan EnzerNo ratings yet

- Applied Statistics and EconometricsDocument149 pagesApplied Statistics and EconometricsglenlcyNo ratings yet

- Economics, Finance, Financial EngineeringDocument147 pagesEconomics, Finance, Financial EngineeringJohn BonJoviNo ratings yet

- Econ 303 OutlineDocument5 pagesEcon 303 OutlineMary Catherine Almonte - EmbateNo ratings yet

- Maths For Macro SyllabusDocument2 pagesMaths For Macro SyllabusAvijit PuriNo ratings yet

- Std11 Maths EM 1Document271 pagesStd11 Maths EM 1Shrey SagarNo ratings yet

- 708-Kaido Class NotesDocument6 pages708-Kaido Class Noteshimanshoo panwarNo ratings yet

- ECON 262-Mathematical Applications in Economics-Kiran AroojDocument4 pagesECON 262-Mathematical Applications in Economics-Kiran AroojHaris Ali0% (1)

- 11 Mathematical Economics CH 1 Lecture 1Document38 pages11 Mathematical Economics CH 1 Lecture 1hanataye37No ratings yet

- Syllabus - Mathematics For Economics - 2021Document3 pagesSyllabus - Mathematics For Economics - 2021oanh nguyen pham oanhNo ratings yet

- Econ 130 C.outline 2023Document3 pagesEcon 130 C.outline 2023gacharagodwinNo ratings yet

- EPM 5131 Course OutlineDocument3 pagesEPM 5131 Course OutlineDivine MunsakaNo ratings yet

- 41 CisDocument2 pages41 CishokhmologNo ratings yet

- Introduction To Matiiematical EconomicsDocument5 pagesIntroduction To Matiiematical EconomicsNeeresh KumarNo ratings yet

- Course Title: Introductory Mathematical Economics Credit Units: 3 Course Code: ECON 603Document3 pagesCourse Title: Introductory Mathematical Economics Credit Units: 3 Course Code: ECON 603rashiNo ratings yet

- ECON 3105 Adv Mathematical EconomicsDocument4 pagesECON 3105 Adv Mathematical Economicsaafaq2003No ratings yet

- Methods for Applied Macroeconomic ResearchFrom EverandMethods for Applied Macroeconomic ResearchRating: 3.5 out of 5 stars3.5/5 (3)

- Kapur J. Mathematical Modelling 1988Document278 pagesKapur J. Mathematical Modelling 1988murat aslan100% (3)

- M.A. Part I Semester I: Four Courses in Each of The Two Semesters For M.A in EconomicsDocument11 pagesM.A. Part I Semester I: Four Courses in Each of The Two Semesters For M.A in EconomicsHolly JohnsonNo ratings yet

- Maths StatsDocument2 pagesMaths StatsAnna KonsulovaNo ratings yet

- 9783110616125.de Gruyter - Algebraic Graph Theory Morphisms, Monoids and Matrices - Jul.2019Document344 pages9783110616125.de Gruyter - Algebraic Graph Theory Morphisms, Monoids and Matrices - Jul.2019Vaan HoolNo ratings yet

- Eco No MetricsDocument6 pagesEco No MetricsSirElwoodNo ratings yet

- EC3120 Mathematical EconomicsDocument2 pagesEC3120 Mathematical Economicsmrudder1999No ratings yet

- Introduction To Quantitative Methods in EconomicsDocument3 pagesIntroduction To Quantitative Methods in EconomicsVenkatesha PrabuNo ratings yet

- Elements of Econometrics Exam CommentariesDocument4 pagesElements of Econometrics Exam CommentariesAlex Absalamov0% (1)

- Mact 12Document2 pagesMact 12Seungho LeeNo ratings yet

- MT3170 Discrete Mathematics and AlgebraDocument2 pagesMT3170 Discrete Mathematics and Algebramrudder1999No ratings yet

- MTH3202 Numerical MethodsDocument3 pagesMTH3202 Numerical MethodsRonald EmanuelNo ratings yet

- QM 1 Course Manual 1013Document40 pagesQM 1 Course Manual 1013williamhoangNo ratings yet

- Statistics For Economist Course OutlineDocument13 pagesStatistics For Economist Course OutlineYishak HesagaNo ratings yet

- Math2099 s2 2014Document11 pagesMath2099 s2 2014AnjewGSNo ratings yet

- EC7091 Module Outine 2014-15Document11 pagesEC7091 Module Outine 2014-15winblacklist1507No ratings yet

- UloopuDocument5 pagesUloopuMystery_HazzNo ratings yet

- Eco 355 - 0 PDFDocument137 pagesEco 355 - 0 PDFbirhan hailieNo ratings yet

- Mathematics CurriculumDocument10 pagesMathematics Curriculumchewe cheweNo ratings yet

- BA Economics Mathematical Economics and Econometry PDFDocument104 pagesBA Economics Mathematical Economics and Econometry PDFSyed Haider Abbas KazmiNo ratings yet

- Econ DC-1Document42 pagesEcon DC-1aleyaray1995No ratings yet

- Econometrics 1Document74 pagesEconometrics 1Anunay ChoudharyNo ratings yet

- EBD Merged Notes-QuizDocument284 pagesEBD Merged Notes-QuizrcybervirusNo ratings yet

- Ecf480 FPD 1 2015 2Document2 pagesEcf480 FPD 1 2015 2richard kapimpaNo ratings yet

- Applications and Interpretations GUIDEDocument95 pagesApplications and Interpretations GUIDELia ChouNo ratings yet

- 05a Cis PDFDocument2 pages05a Cis PDFAnasaziXNo ratings yet

- Slide - MATEMATIKA EKONOMI 2023Document16 pagesSlide - MATEMATIKA EKONOMI 2023uunarjunNo ratings yet

- ECO308 - Week 1 - Lecture - NoteDocument8 pagesECO308 - Week 1 - Lecture - NoteAyinde Taofeeq OlusolaNo ratings yet

- Curriculum Designing and OrganizationDocument18 pagesCurriculum Designing and OrganizationJocelyn GaniaNo ratings yet

- Course Overview ST104ADocument4 pagesCourse Overview ST104A전민건100% (1)

- Mathematics and Statistics For Economics and FinanceDocument2 pagesMathematics and Statistics For Economics and FinanceVu100% (1)

- 14.128 Dynamic Optimization and Economic Applications (Recursive Methods)Document3 pages14.128 Dynamic Optimization and Economic Applications (Recursive Methods)JorgeNo ratings yet

- Stat Syllabus StatisticsDocument26 pagesStat Syllabus StatisticsAryan SinghNo ratings yet

- Math 8 Commom Core SyllabusDocument6 pagesMath 8 Commom Core Syllabusapi-261815606No ratings yet

- An Introduction to Mathematical Analysis for Economic Theory and EconometricsFrom EverandAn Introduction to Mathematical Analysis for Economic Theory and EconometricsNo ratings yet

- Dynamic Optimization, Second Edition: The Calculus of Variations and Optimal Control in Economics and ManagementFrom EverandDynamic Optimization, Second Edition: The Calculus of Variations and Optimal Control in Economics and ManagementRating: 3 out of 5 stars3/5 (3)

- Structural Analysis Intro1Document9 pagesStructural Analysis Intro1adylmaesNo ratings yet

- A227A227M-06 (2011) Standard Specification For Steel Wire, Cold-Drawn For Mechanical SpringsDocument4 pagesA227A227M-06 (2011) Standard Specification For Steel Wire, Cold-Drawn For Mechanical Springstjt4779No ratings yet

- Science Experiment: You Will NeedDocument2 pagesScience Experiment: You Will NeedDANIELA PAEZ SILVANo ratings yet

- MANUAL DE COILED TUBING (Schlumberger) PDFDocument10 pagesMANUAL DE COILED TUBING (Schlumberger) PDFJose Sostenes0% (1)

- 3D Basin and Petroleum System Modelling of Northern North SeaDocument17 pages3D Basin and Petroleum System Modelling of Northern North SeawahyuNo ratings yet

- Service Manual: Outdoor UnitDocument48 pagesService Manual: Outdoor Unitadeelyaseen1No ratings yet

- Material Certification & Physical Test Report of Steel Reinforcement Bars, ASTM A 615 & A370Document1 pageMaterial Certification & Physical Test Report of Steel Reinforcement Bars, ASTM A 615 & A370Nasrullah Fazal AdeebNo ratings yet

- Crown Pillar Optimization For Surface To Underground Mine Transition in Erzincan/Bizmisen Iron MineDocument11 pagesCrown Pillar Optimization For Surface To Underground Mine Transition in Erzincan/Bizmisen Iron MineedwinpenadillomejiaNo ratings yet

- Effectiveness of Moringa Oleifera Seed As CoagulantDocument5 pagesEffectiveness of Moringa Oleifera Seed As CoagulantLuis Hernandez AlvarezNo ratings yet

- Oshas Technical Maual Part 1Document317 pagesOshas Technical Maual Part 1koteshwararaoNo ratings yet

- Etabloc Syt Operating InstructionsDocument50 pagesEtabloc Syt Operating InstructionsFayeez MukadamNo ratings yet

- F4 3systems of Equations (Answer)Document50 pagesF4 3systems of Equations (Answer)yiemetieNo ratings yet

- Probability Tree DiagramsDocument3 pagesProbability Tree DiagramsHaydn BassarathNo ratings yet

- Alcohol PDFDocument12 pagesAlcohol PDFXycca ValdezNo ratings yet

- FhsstmathsDocument201 pagesFhsstmathsMandyNo ratings yet

- LEP01153 - 02 Physics Demonstration Experiments - Magnet Board Mechanics 2Document3 pagesLEP01153 - 02 Physics Demonstration Experiments - Magnet Board Mechanics 2Jose GalvanNo ratings yet

- Physics Experiment - 2Document3 pagesPhysics Experiment - 2Sandipan SamantaNo ratings yet

- Lecture Notes - Optimization and Control PDFDocument405 pagesLecture Notes - Optimization and Control PDFShabih Ul HasanNo ratings yet

- Fourier Theory Made Easy (?)Document30 pagesFourier Theory Made Easy (?)gaurav_juneja_4No ratings yet

- Heat - Thermodynamics Virtual Lab - Physical Sciences - Amrita Vishwa Vidyapeetham Virtual LabDocument1 pageHeat - Thermodynamics Virtual Lab - Physical Sciences - Amrita Vishwa Vidyapeetham Virtual LabjeroldscdNo ratings yet

- GRAFIKDocument5 pagesGRAFIKNia YusNo ratings yet

- Magotteaux - XLIFT PaperDocument11 pagesMagotteaux - XLIFT PaperHamed MostafaNo ratings yet

- Kinametics Part 1Document25 pagesKinametics Part 1ARUNESH PRATAP SINGHNo ratings yet

- Sag and Tension Table For F Drop Wire: Heavy Ice Loading AreasDocument1 pageSag and Tension Table For F Drop Wire: Heavy Ice Loading AreaskikputririzNo ratings yet

- LinkNet ManualDocument38 pagesLinkNet ManualZahid JamilNo ratings yet

- Calculation of Second Moment of AreaDocument6 pagesCalculation of Second Moment of Areasweetpou_04No ratings yet

- Chapter 5: Classic & Smart Styrene: Presentation Petrochemical Production ProcessDocument14 pagesChapter 5: Classic & Smart Styrene: Presentation Petrochemical Production ProcesssamtomNo ratings yet

- PositionDocument5 pagesPositionberemiz009No ratings yet