You might also like

- AT.08.03 - The Accountancy ProfessionDocument5 pagesAT.08.03 - The Accountancy ProfessionLovely PanaliganNo ratings yet

- AT.06.03 - The Accountancy ProfessionDocument6 pagesAT.06.03 - The Accountancy ProfessionMaydet MalapitNo ratings yet

- ICARE - AT - PreWeek - Batch 4Document19 pagesICARE - AT - PreWeek - Batch 4john paulNo ratings yet

- Answer Key Assignment For Chapter 3Document8 pagesAnswer Key Assignment For Chapter 3John Lester DungcaNo ratings yet

- Ra 9298Document10 pagesRa 9298Abraham Mayo MakakuaNo ratings yet

- Ra 9298Document6 pagesRa 9298Jane Michelle EmanNo ratings yet

- BruuuDocument4 pagesBruuuMae ValenciaNo ratings yet

- Department of Accountancy: Page - 1Document16 pagesDepartment of Accountancy: Page - 1NoroNo ratings yet

- Philippine Accountancy Act of 2004Document6 pagesPhilippine Accountancy Act of 2004jeromyNo ratings yet

- The Philippine Accountancy Act of 2004Document4 pagesThe Philippine Accountancy Act of 2004Anna ParciaNo ratings yet

- Roque CPA Reviewer Auditing ch2 Final PDFDocument52 pagesRoque CPA Reviewer Auditing ch2 Final PDFSherene Faith Carampatan100% (3)

- AUDIT 2019 - CompilationDocument73 pagesAUDIT 2019 - CompilationKriztle Kate GelogoNo ratings yet

- Auditing Theory: All of TheseDocument7 pagesAuditing Theory: All of TheseKIM RAGANo ratings yet

- Aud Theo Week1 QuizzerDocument6 pagesAud Theo Week1 QuizzerHansNo ratings yet

- PH Accountancy Act of 2004 (RA9298) - Code of EthicsDocument8 pagesPH Accountancy Act of 2004 (RA9298) - Code of EthicsHaks MashtiNo ratings yet

- ATQ1SCBD5Document8 pagesATQ1SCBD5Helios HexNo ratings yet

- At Reviewer PT 1Document18 pagesAt Reviewer PT 1lender kent alicanteNo ratings yet

- AT Quizzer 2 - Profl Practice of Acctg - Summer 2020 PDFDocument12 pagesAT Quizzer 2 - Profl Practice of Acctg - Summer 2020 PDFJohn Carlo CruzNo ratings yet

- CPAR AT - Philippine Accountancy Act of 2004Document4 pagesCPAR AT - Philippine Accountancy Act of 2004John Carlo CruzNo ratings yet

- PRTC - AT1 - The CPA's Professional ResponsibilityDocument4 pagesPRTC - AT1 - The CPA's Professional Responsibilityelle868No ratings yet

- AT Quizzer 2 - Profl Practice of AcctgDocument12 pagesAT Quizzer 2 - Profl Practice of AcctgJimmyChaoNo ratings yet

- Auditing Theory: Cpa Review School of The Philippines ManilaDocument5 pagesAuditing Theory: Cpa Review School of The Philippines ManilaAljur SalamedaNo ratings yet

- ICARE Preweek AT Preweek LectureDocument15 pagesICARE Preweek AT Preweek Lecturejohn paulNo ratings yet

- AT Quizzer 2 Profl Practice of Acctg 2SAY1920 PDFDocument12 pagesAT Quizzer 2 Profl Practice of Acctg 2SAY1920 PDFlouise carino100% (2)

- Professional Practice of Accounting With AnswerDocument12 pagesProfessional Practice of Accounting With AnswerRNo ratings yet

- At Quizzer 2 Profl Practice of Acctg 2SAY1920 PDFDocument12 pagesAt Quizzer 2 Profl Practice of Acctg 2SAY1920 PDFMina MyouiNo ratings yet

- Semi Answered Aud TheoryDocument11 pagesSemi Answered Aud TheoryAbdulmajed Unda MimbantasNo ratings yet

- Z 5Document8 pagesZ 5Helios HexNo ratings yet

- PRTC - AT3 - The Professional Practice of Public AccountingDocument4 pagesPRTC - AT3 - The Professional Practice of Public Accountingelle868No ratings yet

- At 04Document3 pagesAt 04Alrahjie AnsariNo ratings yet

- Z 1Document12 pagesZ 1Helios HexNo ratings yet

- Z 2Document12 pagesZ 2Helios HexNo ratings yet

- Problem 1-3 Multiple Choice (Acp)Document2 pagesProblem 1-3 Multiple Choice (Acp)Jao FloresNo ratings yet

- RA 9298 QuizzerDocument8 pagesRA 9298 QuizzerJennifer RasonabeNo ratings yet

- Approach To A Potential ClientDocument3 pagesApproach To A Potential ClientA. MagnoNo ratings yet

- Poa 2Document3 pagesPoa 2batistillenieNo ratings yet

- ORGANIZATIONSDocument6 pagesORGANIZATIONSjuennaguecoNo ratings yet

- Ra9298 Anas QuestionnaireDocument15 pagesRa9298 Anas QuestionnaireSV Genalo YooNo ratings yet

- PRTC Preweek LectureDocument51 pagesPRTC Preweek LectureKristinelle AragoNo ratings yet

- Chapter 2 PDFDocument25 pagesChapter 2 PDFZi VillarNo ratings yet

- At.3223 - Practice of AccountancyDocument12 pagesAt.3223 - Practice of AccountancyDenny June CraususNo ratings yet

- ATQ1SCBD2Document11 pagesATQ1SCBD2Helios HexNo ratings yet

- Auditing Practice QuestionsDocument49 pagesAuditing Practice QuestionsBeaNo ratings yet

- Summative Assessment-IntactDocument5 pagesSummative Assessment-IntactNhel AlvaroNo ratings yet

- Ra 9298 Quiz Part 2Document2 pagesRa 9298 Quiz Part 2jaypee.bignoNo ratings yet

- Z 4Document9 pagesZ 4Helios HexNo ratings yet

- Accountancy LawDocument33 pagesAccountancy LawJomar Acar GuittoNo ratings yet

- Ra 9298Document14 pagesRa 9298Errah Jenn CajesNo ratings yet

- AT.2823 - Setting Up A Public Accounting Practice PDFDocument15 pagesAT.2823 - Setting Up A Public Accounting Practice PDFMaeNo ratings yet

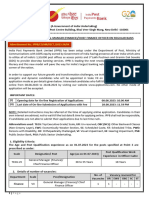

- Advertisement No.: IPPB/CO/HR/RECT./2023-24/04Document5 pagesAdvertisement No.: IPPB/CO/HR/RECT./2023-24/04P S ShahilNo ratings yet

- FAR04-01 - Development of Financial Reporting Framework Standard & Regulation of Accountancy ProfessionDocument4 pagesFAR04-01 - Development of Financial Reporting Framework Standard & Regulation of Accountancy Professionnicole bancoro100% (1)

- c3 ReviewerDocument42 pagesc3 Reviewerrandomlungs121223No ratings yet

- Q1 - Philippine Accountancy Act of 2004, Code of EthicsDocument10 pagesQ1 - Philippine Accountancy Act of 2004, Code of EthicsPrankyJellyNo ratings yet

- Audit Theory - QuizzerDocument36 pagesAudit Theory - QuizzerCharis Marie UrgelNo ratings yet

- Practice Test 2 - Auditing Theory 2023Document57 pagesPractice Test 2 - Auditing Theory 2023April Rose Sobrevilla DimpoNo ratings yet

- Logo Here Auditing Theory Philippine Accountancy Act of 2004Document35 pagesLogo Here Auditing Theory Philippine Accountancy Act of 2004KathleenCusipagNo ratings yet

- Poa 8Document2 pagesPoa 8batistillenieNo ratings yet

- CFP Certification Exam Practice Question Workbook: 1,000 Comprehensive Practice Questions (2018 Edition)From EverandCFP Certification Exam Practice Question Workbook: 1,000 Comprehensive Practice Questions (2018 Edition)Rating: 5 out of 5 stars5/5 (1)

- A Comparative Analysis of Tax Administration in Asia and the Pacific: 2020 EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific: 2020 EditionNo ratings yet

- AFAR Self Test - 9005Document6 pagesAFAR Self Test - 9005King MercadoNo ratings yet

- AFAR Self Test - 9004Document4 pagesAFAR Self Test - 9004King MercadoNo ratings yet

- Practical Research 1: Quarter 3 - Module 2: Characteristics, Processes and Ethics of ResearchDocument26 pagesPractical Research 1: Quarter 3 - Module 2: Characteristics, Processes and Ethics of ResearchKing MercadoNo ratings yet

- AT.03-06 - Transaction CyclesDocument5 pagesAT.03-06 - Transaction CyclesKing MercadoNo ratings yet

- Practical Research 1: Quarter 3 - Module 1: Importance of Research in Daily LivesDocument20 pagesPractical Research 1: Quarter 3 - Module 1: Importance of Research in Daily LivesKing Mercado100% (5)

- AFAR Self Test - 9001Document5 pagesAFAR Self Test - 9001King MercadoNo ratings yet

- AFAR Self Test - 9003Document6 pagesAFAR Self Test - 9003King MercadoNo ratings yet

- MAS-07 Standard Costing (Answers)Document1 pageMAS-07 Standard Costing (Answers)King MercadoNo ratings yet

- Practical Research 1: Quarter 3 - Module 3: Quantitative and Qualitative ResearchDocument24 pagesPractical Research 1: Quarter 3 - Module 3: Quantitative and Qualitative ResearchKing Mercado100% (8)

- Code No. Region School Code Last Name: (001 - R10 - MSU-IIT - Delgado)Document4 pagesCode No. Region School Code Last Name: (001 - R10 - MSU-IIT - Delgado)King MercadoNo ratings yet

- Cpar b86 Preweek - FarDocument16 pagesCpar b86 Preweek - FarKing MercadoNo ratings yet

- Cpar b86 Preweek - at 2Document12 pagesCpar b86 Preweek - at 2King MercadoNo ratings yet

- 1.TRUE 2.TRUE 3.TRUE 4.false 5.TRUE 6.TRUE 7.false 8.TRUE 9.TRUE 10. FalseDocument5 pages1.TRUE 2.TRUE 3.TRUE 4.false 5.TRUE 6.TRUE 7.false 8.TRUE 9.TRUE 10. FalseKing MercadoNo ratings yet

- Cpar b86 Preweek - ApDocument12 pagesCpar b86 Preweek - ApKing MercadoNo ratings yet

- CPAR B86 Preweek - FAR Theories 1Document10 pagesCPAR B86 Preweek - FAR Theories 1King MercadoNo ratings yet

- CPAR B86 Preweek - AP Answer KeyDocument6 pagesCPAR B86 Preweek - AP Answer KeyKing MercadoNo ratings yet

- Reasonable Reasonable Assurance AssuranceDocument26 pagesReasonable Reasonable Assurance AssuranceKing MercadoNo ratings yet

- Aicpa Aud Moderate2015Document25 pagesAicpa Aud Moderate2015King MercadoNo ratings yet

- Cpar b86 Preweek - AfarDocument14 pagesCpar b86 Preweek - AfarKing MercadoNo ratings yet

- FAR Final PB SolutionDocument4 pagesFAR Final PB SolutionKing MercadoNo ratings yet

- CPAR B86 Preweek - MAS Answer KeyDocument1 pageCPAR B86 Preweek - MAS Answer KeyKing MercadoNo ratings yet

- FAR 6704 (Bullet Review)Document8 pagesFAR 6704 (Bullet Review)King MercadoNo ratings yet

- Multiple Choice Questions: 44 Hilton, Managerial Accounting, Seventh EditionDocument36 pagesMultiple Choice Questions: 44 Hilton, Managerial Accounting, Seventh EditionKing MercadoNo ratings yet

- C. A System of Quality ControlsDocument11 pagesC. A System of Quality ControlsMC ExtNo ratings yet

- Tezpur University Application Form For Migration CertificateDocument1 pageTezpur University Application Form For Migration CertificatebishalNo ratings yet

- Evaluation in Education-Educational Evaluation: June 2016Document51 pagesEvaluation in Education-Educational Evaluation: June 2016Elena BluvinNo ratings yet

- Public Relations CourseDocument4 pagesPublic Relations CourseAnisa MohamedNo ratings yet

- AP European History Course and Exam Description, Effective Fall 2020Document294 pagesAP European History Course and Exam Description, Effective Fall 2020BunnyNo ratings yet

- ASL 1 Course GuideDocument12 pagesASL 1 Course GuideNel BorniaNo ratings yet

- Valuing Cultural Heritage: Economic and Cultural Value of The ColosseumDocument49 pagesValuing Cultural Heritage: Economic and Cultural Value of The ColosseumSai KamalaNo ratings yet

- Aqa English Language B A2 Coursework IdeasDocument4 pagesAqa English Language B A2 Coursework Ideasafjwodcfftkccl100% (2)

- 9ST0 A Level Statistics Topic 3 Population and SamplesDocument8 pages9ST0 A Level Statistics Topic 3 Population and SamplesrtyfsghsshfgNo ratings yet

- EPI 3.6 Qualitative ResearchDocument5 pagesEPI 3.6 Qualitative ResearchJoher MendezNo ratings yet

- Grade 09 History 2nd Term Test Paper With Answers 2019 Sinhala Medium Southern ProvinceDocument8 pagesGrade 09 History 2nd Term Test Paper With Answers 2019 Sinhala Medium Southern Provincelalithkumara19791102No ratings yet

- EGR 3713 Syllabus Part A+BDocument4 pagesEGR 3713 Syllabus Part A+BSarah-RuthNo ratings yet

- SSC CGL Tier I Exam 2014 Question Paper 19-10-2014-Evening-Session-Booklet-No-333TL4Document18 pagesSSC CGL Tier I Exam 2014 Question Paper 19-10-2014-Evening-Session-Booklet-No-333TL4SpeculeNo ratings yet

- Instructions For Exam Entry CimaDocument12 pagesInstructions For Exam Entry CimaTauraabNo ratings yet

- Practical Research 1 11 q1 m5Document14 pagesPractical Research 1 11 q1 m5SakusakuNo ratings yet

- 3 SPM Instructions For Speaking Examiners V3Document29 pages3 SPM Instructions For Speaking Examiners V3Nani Hannanika100% (7)

- Baguin - Ge 34 - Mathematics in The Modern World PDFDocument37 pagesBaguin - Ge 34 - Mathematics in The Modern World PDFMayflor Curib Cubos100% (1)

- 15081Document2 pages15081akaNo ratings yet

- 3 B.Tech. ECE FinalDocument140 pages3 B.Tech. ECE FinalBusiness principlezNo ratings yet

- Conducting An Interlaboratory Study To Determine The Precision of A Test MethodDocument22 pagesConducting An Interlaboratory Study To Determine The Precision of A Test MethodMaqsoodUlHassanChaudharyNo ratings yet

- Apela Learners Handbook l3-l7 v.2.0 2024Document41 pagesApela Learners Handbook l3-l7 v.2.0 2024yusri yuninNo ratings yet

- Guide To Conducting An Educational Needs Assessment Beyond The Literature ReviewDocument4 pagesGuide To Conducting An Educational Needs Assessment Beyond The Literature Reviewc5pnw26sNo ratings yet

- 426-Longitudinal Study Checklist For LearnersDocument4 pages426-Longitudinal Study Checklist For LearnersneeNo ratings yet

- PSL49Document2 pagesPSL49benderman1No ratings yet

- Advertisement Admin Staff Daily WagesDocument2 pagesAdvertisement Admin Staff Daily WagesABODE PVT LIMITEDNo ratings yet

- Form PDFDocument2 pagesForm PDFmahavir damakaleNo ratings yet

- Department of Education: Activity DesignDocument6 pagesDepartment of Education: Activity DesignDENNIS AGUDONo ratings yet

- Are Standardized Tests For EveryoneDocument24 pagesAre Standardized Tests For EveryoneAaditi VNo ratings yet

- CBT-II Score-Card Details: Railway Recruitment BoardsDocument1 pageCBT-II Score-Card Details: Railway Recruitment BoardsSeetaramasastry SastryNo ratings yet

- Rapid Assessment of Learning Resources: Lrs From Deped PortalsDocument2 pagesRapid Assessment of Learning Resources: Lrs From Deped Portalsreginald_adia_1No ratings yet