You might also like

- Excerpts From The Book 'The Lawless State (The Crimes of The U.S. Intelligence Agencies) ' by Morton H. Halperin, Jerry Berman, Robert Borosage, Christine Marwick (1976)Document50 pagesExcerpts From The Book 'The Lawless State (The Crimes of The U.S. Intelligence Agencies) ' by Morton H. Halperin, Jerry Berman, Robert Borosage, Christine Marwick (1976)Anonymous yu09qxYCM100% (1)

- Precedent Transaction Template - NewDocument5 pagesPrecedent Transaction Template - NewAmay SinghNo ratings yet

- 121 - St. Jerome - Commentary On Galatians Translated by Andrew Cain The Fathers of The Church SerieDocument310 pages121 - St. Jerome - Commentary On Galatians Translated by Andrew Cain The Fathers of The Church SerieSciosis HemorrhageNo ratings yet

- Windows Server 2019 Administration CourseDocument590 pagesWindows Server 2019 Administration CourseTrần Trọng Nhân100% (2)

- Translation of Key Passages from the Lotus SutraDocument12 pagesTranslation of Key Passages from the Lotus SutraCharly de TaïNo ratings yet

- Beyond Cutting Heads - Transformational Cost ManagementDocument54 pagesBeyond Cutting Heads - Transformational Cost ManagementLuiz Souza100% (1)

- Negotiable Instruments Act ExplainedDocument28 pagesNegotiable Instruments Act ExplainedShrikant RathodNo ratings yet

- HSBC Employees Union Vs NLRCDocument1 pageHSBC Employees Union Vs NLRCRobertNo ratings yet

- The Pit and The Pendulum and Other StoriesDocument11 pagesThe Pit and The Pendulum and Other Storiesdunae100% (3)

- BS ISO 5057 - Industrial Truck Inspection PDFDocument7 pagesBS ISO 5057 - Industrial Truck Inspection PDFEderNo ratings yet

- 2020-Q1-Closing TimetableDocument10 pages2020-Q1-Closing TimetableAdrian YepesNo ratings yet

- Your CFO Guy - 7 Chart TemplatesDocument6 pagesYour CFO Guy - 7 Chart TemplatesOaga GutierrezNo ratings yet

- Court ObservationDocument2 pagesCourt Observationjobert cortez100% (1)

- For Business CaseDocument4 pagesFor Business CasealuanuNo ratings yet

- A Clean, Well-Lighted Place EssayDocument7 pagesA Clean, Well-Lighted Place EssayAdrianNo ratings yet

- 1-Cost ConceptsDocument1 page1-Cost ConceptsDana Beatrice RoqueNo ratings yet

- Financial Statement AnalysisDocument2 pagesFinancial Statement AnalysisErika Anne JaurigueNo ratings yet

- Audit Working Paper (Contoh)Document65 pagesAudit Working Paper (Contoh)Trick1 HahaNo ratings yet

- Model: C:/Users/Nurkhalis Mahmudah D/Dropbox/Tesis/Evaluasi Saham/Reference/SD/Kaoru Yamaguchi/Chap 3/accounting - VMF View: Income StatementDocument1 pageModel: C:/Users/Nurkhalis Mahmudah D/Dropbox/Tesis/Evaluasi Saham/Reference/SD/Kaoru Yamaguchi/Chap 3/accounting - VMF View: Income StatementKhalis MahmudahNo ratings yet

- Handout Appendix DCF Valuation 2023Document21 pagesHandout Appendix DCF Valuation 2023Akshay SharmaNo ratings yet

- Sample Ctos Score Report CompanyDocument3 pagesSample Ctos Score Report Companyhwyap2022No ratings yet

- Page Industries: CMP: ' TP: ' AccumulateDocument6 pagesPage Industries: CMP: ' TP: ' AccumulateAkshit SandoojaNo ratings yet

- 2-Second Session Presentation FinancialsDocument18 pages2-Second Session Presentation FinancialsAbdul Basit SheikhNo ratings yet

- 3333 GLDocument56 pages3333 GLJyoti BugdeNo ratings yet

- Remanufacturers Overstated EBITDADocument14 pagesRemanufacturers Overstated EBITDAbucentaurNo ratings yet

- CVP ANALYSISDocument1 pageCVP ANALYSISKittenNo ratings yet

- Module 10 Maximizing Service Profitability 2012Document8 pagesModule 10 Maximizing Service Profitability 2012enjoythedocsNo ratings yet

- Business SchemeDocument1 pageBusiness SchemeRatno SusenoNo ratings yet

- 5 - CH 10 Part 3Document37 pages5 - CH 10 Part 3tejaswani poduguNo ratings yet

- Accounting Standards PDFDocument43 pagesAccounting Standards PDFSai Krishna TejaNo ratings yet

- Fundamentals Of Partnership FirmDocument15 pagesFundamentals Of Partnership Firmaayush.verma2105No ratings yet

- Template Trading ComparablesDocument3 pagesTemplate Trading ComparablesAmay SinghNo ratings yet

- LPGDocument13 pagesLPGRathod RituNo ratings yet

- Monthly Progress Report for District Roads in MansehraDocument149 pagesMonthly Progress Report for District Roads in MansehraAmir_Jamal_QureshiNo ratings yet

- The Dupont Chart As An Analysis and Reporting Tool: Click Mouse To View SlidesDocument5 pagesThe Dupont Chart As An Analysis and Reporting Tool: Click Mouse To View SlidesChabala Vinay KumarNo ratings yet

- When You Join Zoom, Your Computer Will Automatically Connect To The Audio StreamDocument51 pagesWhen You Join Zoom, Your Computer Will Automatically Connect To The Audio StreamRammohan PushadapuNo ratings yet

- Bad Debt, Inventory, DepreciationDocument2 pagesBad Debt, Inventory, Depreciationrio_harcanNo ratings yet

- Account & Deposit Processes (Corporate)Document1 pageAccount & Deposit Processes (Corporate)Ram Mohan MishraNo ratings yet

- Reporting Date:-Production Report For:-: Quality Management SystemDocument4 pagesReporting Date:-Production Report For:-: Quality Management SystemsourajpatelNo ratings yet

- Asse T Balance Sheet: Current Assets Non-Current AssetsDocument2 pagesAsse T Balance Sheet: Current Assets Non-Current AssetsSapto PhsNo ratings yet

- Manage Account Conditions (Corporate)Document1 pageManage Account Conditions (Corporate)Ram Mohan MishraNo ratings yet

- Under Armour: Q3 Gains Come at Q4 Expense: Maintain SELLDocument7 pagesUnder Armour: Q3 Gains Come at Q4 Expense: Maintain SELLAnonymous Feglbx5No ratings yet

- Balance Equity: KekayaanDocument5 pagesBalance Equity: KekayaanAndrea NatashaNo ratings yet

- Nueva Vizcaya State University Instructional ModuleDocument15 pagesNueva Vizcaya State University Instructional ModuleInfinity KingNo ratings yet

- Women in Banking 15m (Empty)Document296 pagesWomen in Banking 15m (Empty)El rincón de las 5 EL RINCÓN DE LAS 5No ratings yet

- Annex A-2: Sample Conceptual Framework of Information SystemsDocument1 pageAnnex A-2: Sample Conceptual Framework of Information SystemspetiepanNo ratings yet

- Costs of ProductionDocument5 pagesCosts of ProductionSure ShottNo ratings yet

- NoidaDocument6 pagesNoidaAvnish KumarNo ratings yet

- MAY 24-31 2022 - USDDocument19 pagesMAY 24-31 2022 - USDAmie Jean UmaliNo ratings yet

- MRSUTRIALQ1G08Document2 pagesMRSUTRIALQ1G08Saurav DashNo ratings yet

- 50 BooksDocument2 pages50 BooksFARMAN SHAIKH SAHABNo ratings yet

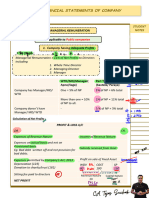

- Financial Statement of company plus class notes (1)Document10 pagesFinancial Statement of company plus class notes (1)Alex FernandoNo ratings yet

- PC - 01-Subcon & Supplier FormatDocument3 pagesPC - 01-Subcon & Supplier FormatnileshNo ratings yet

- 2.define Chart of Accounts and Accounts GroupDocument18 pages2.define Chart of Accounts and Accounts GroupNASEER ULLAHNo ratings yet

- 10%DP18MOS-90 Amaia Land Corp. Amaia Steps Alabang Sample Computation OnlyDocument1 page10%DP18MOS-90 Amaia Land Corp. Amaia Steps Alabang Sample Computation Onlyaize soultierNo ratings yet

- GST ProcessDocument20 pagesGST Processparavaiselvam100% (2)

- A Invoices:: DvanceDocument6 pagesA Invoices:: DvanceAishwarya PillaiNo ratings yet

- Business Reports of The Sector: Period: 4Document5 pagesBusiness Reports of The Sector: Period: 4Aditya SinghNo ratings yet

- Daily Expenses-wps OfficeDocument1 pageDaily Expenses-wps Officejonathan iyusuNo ratings yet

- Name of Company: Bill Register Financial YearDocument8 pagesName of Company: Bill Register Financial YearMubashar HussainNo ratings yet

- CFFM9, CH 03, Slides - 10-14-15Document30 pagesCFFM9, CH 03, Slides - 10-14-15Rinat MaratovNo ratings yet

- Financial Setup:: Chart of Accounts - ConceptsDocument14 pagesFinancial Setup:: Chart of Accounts - ConceptsChadwick E VanieNo ratings yet

- Sap FiDocument19 pagesSap FireneNo ratings yet

- 财务、企业理财、权益、其他Document110 pages财务、企业理财、权益、其他Ariel MengNo ratings yet

- Green Integrationplan Jul 302018 V8Document27 pagesGreen Integrationplan Jul 302018 V8AishwaryaAyyalarajuNo ratings yet

- 3 Year Business Plan TargetsDocument1 page3 Year Business Plan TargetsGirish SalujaNo ratings yet

- Toyota: Request For On-Hand (Roh) AdjustmentDocument1 pageToyota: Request For On-Hand (Roh) AdjustmentKarl CruzNo ratings yet

- Identification by A Static CMR FieldDocument5 pagesIdentification by A Static CMR FieldkvrnageshNo ratings yet

- MRSUQ1D04Document3 pagesMRSUQ1D04Balaji AllupatiNo ratings yet

- HDFC Life Click 2 Invest ULIP illustrationDocument3 pagesHDFC Life Click 2 Invest ULIP illustrationanon_315406837No ratings yet

- Law Enforcement Administration and Police OrganizationDocument102 pagesLaw Enforcement Administration and Police OrganizationAudrey Kristina Maypa0% (1)

- Rizal and His TimesDocument10 pagesRizal and His TimesDaniella Pasilbas SabacNo ratings yet

- Datapage Top-Players2 NewJerseyDocument5 pagesDatapage Top-Players2 NewJerseydarkrain777No ratings yet

- New SEM Socio Economic Segmentation Tool ExplainedDocument3 pagesNew SEM Socio Economic Segmentation Tool ExplainedanzaniNo ratings yet

- Sir Thomas WyattDocument4 pagesSir Thomas WyattNoraNo ratings yet

- I Have Studied Under Many Efficient Teachers and I Have Learnt A Lot From ThemDocument1 pageI Have Studied Under Many Efficient Teachers and I Have Learnt A Lot From ThemSHENNIE WONG PUI CHI MoeNo ratings yet

- Can I Legally Drop Out of School in Switzerland If I Am 16 - Google SucheDocument1 pageCan I Legally Drop Out of School in Switzerland If I Am 16 - Google SucheWilhelm AgenciesNo ratings yet

- Salander Bankruptcy OpinionDocument52 pagesSalander Bankruptcy Opinionmelaniel_coNo ratings yet

- Marketing Planning & Application: Submitted To Sir Bilal KothariDocument20 pagesMarketing Planning & Application: Submitted To Sir Bilal KothariSAIF ULLAHNo ratings yet

- Churchil SpeechDocument5 pagesChurchil Speechchinuuu85br5484No ratings yet

- Air Arabia 2017 Financial StatementsDocument62 pagesAir Arabia 2017 Financial StatementsRatika AroraNo ratings yet

- BCB Dieu Chinh Thong Tin 05 2015Document110 pagesBCB Dieu Chinh Thong Tin 05 2015Quang Hưng VũNo ratings yet

- Dinamika Dan Perkembangan Konstitusi Republik Indonesia: Riski Febria NuritaDocument9 pagesDinamika Dan Perkembangan Konstitusi Republik Indonesia: Riski Febria NuritaIsnaini NikmatulNo ratings yet

- Calawag National High School MAPEH AssessmentDocument2 pagesCalawag National High School MAPEH AssessmentMarbert GarganzaNo ratings yet

- Wa0000.Document3 pagesWa0000.Surya SiddarthNo ratings yet

- GST Invoice Format No. 20Document1 pageGST Invoice Format No. 20email2suryazNo ratings yet

- Bjorn MeioOrc Barbaro Hugo PDFDocument4 pagesBjorn MeioOrc Barbaro Hugo PDFRaphael VenturaNo ratings yet

- CA FINAL First Priority Topics and Questions for MAY-22 ExamsDocument3 pagesCA FINAL First Priority Topics and Questions for MAY-22 ExamsasdNo ratings yet