You might also like

- Statement 21-NOV-22 AC 03013375 23042820Document3 pagesStatement 21-NOV-22 AC 03013375 23042820Vitor BinghamNo ratings yet

- Congoleum CaseDocument9 pagesCongoleum Casefranco50% (2)

- Business Plan For An Independently Owned Grocery Store A Comprehensive Analysis To The Creation of A Grocery StoreDocument47 pagesBusiness Plan For An Independently Owned Grocery Store A Comprehensive Analysis To The Creation of A Grocery StoreFausto M. Delgado40% (5)

- Your CFO Guy - 7 Chart TemplatesDocument6 pagesYour CFO Guy - 7 Chart TemplatesOaga GutierrezNo ratings yet

- Name: Raymund B. Cawilan Entrepremeurship Quarter 2 Module 10 Grade 11-ADocument1 pageName: Raymund B. Cawilan Entrepremeurship Quarter 2 Module 10 Grade 11-ATana Cristobal100% (1)

- FM Revision File Nitin GuruDocument123 pagesFM Revision File Nitin Gurudeepu deepu100% (1)

- 4.lecture Partnership and Company LawDocument81 pages4.lecture Partnership and Company LawNina RoroNo ratings yet

- BPMN Case StudyDocument7 pagesBPMN Case StudyLeo Putera100% (1)

- PPM Service Catalogue June 2017Document51 pagesPPM Service Catalogue June 2017steveshowman100% (1)

- Four Year Profit ProjectionDocument1 pageFour Year Profit Projectiondamir101No ratings yet

- Four Year Profit Projection: Enter Your Company Name HereDocument1 pageFour Year Profit Projection: Enter Your Company Name HereMisscreant EveNo ratings yet

- Masterclass On EBITDADocument15 pagesMasterclass On EBITDArdttecNo ratings yet

- PDF 5 Income TaxDocument1 pagePDF 5 Income Taxmanishchd81No ratings yet

- Fin460 ExercisesDocument6 pagesFin460 ExercisesNgọc CừuNo ratings yet

- Employee AttritionDocument37 pagesEmployee AttritionChandan Priyadarshi100% (1)

- Template For Financial ProjectionDocument32 pagesTemplate For Financial ProjectionRussel Jess HeyranaNo ratings yet

- Tax Calculator (Salary Format)Document2 pagesTax Calculator (Salary Format)Muhammed Abul Kalam AcmaNo ratings yet

- Partnership ReviewerDocument2 pagesPartnership ReviewerXeleen Elizabeth ArcaNo ratings yet

- 1 Blank Model TemplateDocument28 pages1 Blank Model TemplateMasroor KhanNo ratings yet

- Four Year Profit ProjectionDocument1 pageFour Year Profit ProjectionDebbieNo ratings yet

- Homework4 NAMEDocument1 pageHomework4 NAMEjiaqichangNo ratings yet

- Study Aid - Bonuses, Insufficient Net Income and Net Losses PDFDocument8 pagesStudy Aid - Bonuses, Insufficient Net Income and Net Losses PDFAdolph Christian GonzalesNo ratings yet

- Audit Working Paper (Contoh)Document65 pagesAudit Working Paper (Contoh)Trick1 HahaNo ratings yet

- Fundamentals of Partnership FirmDocument15 pagesFundamentals of Partnership Firmaayush.verma2105No ratings yet

- Pt. Gs Gold Shine Battery: Nama Karyawa: TRI HANDOKO Jabatan: Director Company Perform - Jan 19Document3 pagesPt. Gs Gold Shine Battery: Nama Karyawa: TRI HANDOKO Jabatan: Director Company Perform - Jan 19Nia TjhoaNo ratings yet

- Four Year Profit ProjectionDocument1 pageFour Year Profit Projectionbaderf75No ratings yet

- Continuous Assignment-03 Rakesh Pendyala PGPBL0247: # 4 Different CompaniesDocument1 pageContinuous Assignment-03 Rakesh Pendyala PGPBL0247: # 4 Different CompaniesAISHWARYA SHENOY K P 2127635No ratings yet

- Lampiran A - Template Actual-Perkiraan 2020Document10 pagesLampiran A - Template Actual-Perkiraan 2020Agus BudiluhurNo ratings yet

- Samir Modi Azadi Plan 2.0 - One PagerDocument1 pageSamir Modi Azadi Plan 2.0 - One PagerNitishKumarNo ratings yet

- Factsheet DecDocument11 pagesFactsheet DecRakesh Dey sarkarNo ratings yet

- Page Industries: CMP: ' TP: ' AccumulateDocument6 pagesPage Industries: CMP: ' TP: ' AccumulateAkshit SandoojaNo ratings yet

- Rasivakuma Franchisee ReportDocument9 pagesRasivakuma Franchisee ReportSivakumar AkkariNo ratings yet

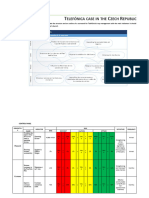

- Telefónica Case in CzechiaDocument7 pagesTelefónica Case in CzechiaScribdTranslationsNo ratings yet

- Venus RemediesDocument3 pagesVenus RemediesbhoomikaNo ratings yet

- Traf Presentation India WebcastDocument48 pagesTraf Presentation India WebcastSwastik GroverNo ratings yet

- Investment Banking ExcelDocument28 pagesInvestment Banking ExcelJohn ChiwaiNo ratings yet

- Nippon Paint Group Medium-Term Plan (FY2021-2023) Update ReportDocument36 pagesNippon Paint Group Medium-Term Plan (FY2021-2023) Update ReportRahiNo ratings yet

- Consolidation of Less-than-Wholly Owned Subsidiary: Douglas CloudDocument32 pagesConsolidation of Less-than-Wholly Owned Subsidiary: Douglas CloudkaniyaNo ratings yet

- Accounting Standards PDFDocument43 pagesAccounting Standards PDFSai Krishna TejaNo ratings yet

- Women in Banking 15m (Empty)Document296 pagesWomen in Banking 15m (Empty)El rincón de las 5 EL RINCÓN DE LAS 5No ratings yet

- Screenshot 2023-03-14 at 11.30.56 AM PDFDocument1 pageScreenshot 2023-03-14 at 11.30.56 AM PDFAbdul AzizNo ratings yet

- Annual Report of IOCL 110Document1 pageAnnual Report of IOCL 110Nikunj ParmarNo ratings yet

- EngEco 6 - CFATDocument29 pagesEngEco 6 - CFATNPCNo ratings yet

- Capital Structure - APVDocument40 pagesCapital Structure - APVGonzalo De CorralNo ratings yet

- Deductions From Gross Total Income 01 - Class Notes - Udesh Regular - Group 1Document9 pagesDeductions From Gross Total Income 01 - Class Notes - Udesh Regular - Group 1Uday TomarNo ratings yet

- Petroleum Economic and ManagementDocument74 pagesPetroleum Economic and ManagementWahid MiaNo ratings yet

- AccountsDocument21 pagesAccountsakash lachhwani100% (1)

- Lec.6Document28 pagesLec.6Hokyee ChanNo ratings yet

- Chapter 2 FormulaDocument1 pageChapter 2 FormulaSean LooNo ratings yet

- 2 - Transfer Pricing CH 9 FE CAFDocument196 pages2 - Transfer Pricing CH 9 FE CAFtejaswani poduguNo ratings yet

- Ch3 Income Statement - DVDocument44 pagesCh3 Income Statement - DVElf CanNo ratings yet

- 2022 Tax ComputationDocument7 pages2022 Tax ComputationGeo Mosaic Diaz (Jiyu)No ratings yet

- HRD, Training Managers and SDFs TrainingDocument3 pagesHRD, Training Managers and SDFs TrainingMr MathipsNo ratings yet

- Kso TugasDocument7 pagesKso TugasRahmat Ramadhan RahmatNo ratings yet

- W5 Topic 4.THEORY OF FIRMDocument56 pagesW5 Topic 4.THEORY OF FIRMongwx-wp22No ratings yet

- Rasivakuma Franchisee ReportDocument9 pagesRasivakuma Franchisee ReportSivakumar AkkariNo ratings yet

- Mandg Ar2021Document328 pagesMandg Ar2021Ganesh RajputNo ratings yet

- Stanmore Question Plus TemplateDocument1 pageStanmore Question Plus TemplateNe PaNo ratings yet

- Annual Report of IOCL 88Document1 pageAnnual Report of IOCL 88Nikunj ParmarNo ratings yet

- Annual Report of IOCL 88Document1 pageAnnual Report of IOCL 88NikunjNo ratings yet

- Statement of Profit and Loss NotesDocument7 pagesStatement of Profit and Loss NotesshadehdavNo ratings yet

- Producers EquilibriumDocument3 pagesProducers EquilibriumShobhit MishraNo ratings yet

- Bajaj PureStock FundDocument1 pageBajaj PureStock FundDeepu CNo ratings yet

- 16 Summer 2018 BT SADocument8 pages16 Summer 2018 BT SApabloescobar11yNo ratings yet

- CCIC DBJ MSME IGNITE Grant Application PDFDocument19 pagesCCIC DBJ MSME IGNITE Grant Application PDFCashyaka McDonaldNo ratings yet

- Pro-Forma Income Statement: RevenueDocument6 pagesPro-Forma Income Statement: Revenuemas kapcaiNo ratings yet

- Silo - Tips A Level Business Paper 3 Specimen Assessment Material Mark SchemeDocument22 pagesSilo - Tips A Level Business Paper 3 Specimen Assessment Material Mark SchemeJohnny PlaysNo ratings yet

- Cara Menghitung Biaya K3Document53 pagesCara Menghitung Biaya K3H. Muhammad Temter GandaNo ratings yet

- EMC Case StudyDocument1 pageEMC Case Studyomar gamalNo ratings yet

- Business Policy 101Document10 pagesBusiness Policy 101Alberto NicholsNo ratings yet

- The Great Eastern Shipping Company Limited - Case Writeup - B19156Document9 pagesThe Great Eastern Shipping Company Limited - Case Writeup - B19156Shourya SardanaNo ratings yet

- GI HandloomsDocument10 pagesGI HandloomsGargi UpadhyayaNo ratings yet

- Armenian Banking Sector OverviewDocument42 pagesArmenian Banking Sector OverviewМисак Давтян100% (1)

- Title:-Home Service at A Click: Presented byDocument14 pagesTitle:-Home Service at A Click: Presented byPooja PujariNo ratings yet

- CH 07 Project ManagementDocument9 pagesCH 07 Project Managementrajlaxmi1001No ratings yet

- Financial Anal PMA EXCEL2222LDocument27 pagesFinancial Anal PMA EXCEL2222LBhavna309100% (1)

- Should A Culture Be Too Strong?Document3 pagesShould A Culture Be Too Strong?Parag AutkarNo ratings yet

- CIPD Profession MapDocument28 pagesCIPD Profession MapPayal MagdaniNo ratings yet

- Final Project KusumgarDocument62 pagesFinal Project KusumgarAvinash SahuNo ratings yet

- FULL Download Ebook PDF International Business by Michael Geringer PDF EbookDocument41 pagesFULL Download Ebook PDF International Business by Michael Geringer PDF Ebookscott.ramirez644100% (36)

- E-GOVERNANCE in BangladeshDocument23 pagesE-GOVERNANCE in BangladeshZafour100% (1)

- Chapter 3 MARKETINGDocument27 pagesChapter 3 MARKETINGMaite Toquero IriarteNo ratings yet

- F004 Bills of Exchange, Sale or Return and ADD Teachers Test 4Document11 pagesF004 Bills of Exchange, Sale or Return and ADD Teachers Test 4bhumikaaNo ratings yet

- Portfolio ReportDocument10 pagesPortfolio Reportsudeshna palitNo ratings yet

- Partnership Dissolution ProblemsDocument2 pagesPartnership Dissolution ProblemsMellanie SerranoNo ratings yet

- Evolution of Management TheoryDocument28 pagesEvolution of Management TheoryDevi TriyadiNo ratings yet

- Meldy Layugan: Career StatementDocument5 pagesMeldy Layugan: Career StatementLynne LayuganNo ratings yet

- Operations Strategy - TESCO - FinalDocument9 pagesOperations Strategy - TESCO - FinalSrujana Gattu100% (1)

- Commercial Property Pricing IndexDocument7 pagesCommercial Property Pricing IndexIvan DidiNo ratings yet