You might also like

- Lesson 1 - 2 Tax On The Self Employed Andor Professional 2Document4 pagesLesson 1 - 2 Tax On The Self Employed Andor Professional 2Aaron HernandezNo ratings yet

- Reporting in EntrepDocument67 pagesReporting in EntrepCarl AndayaNo ratings yet

- RFID Request FormDocument1 pageRFID Request FormJ San DiegoNo ratings yet

- Managerial Accounting:: An Introduction To Concepts, Methods, and UsesDocument22 pagesManagerial Accounting:: An Introduction To Concepts, Methods, and UsesamitbaggausNo ratings yet

- Toaz - Info Module 1 Mathematics in The Modern World PRDocument14 pagesToaz - Info Module 1 Mathematics in The Modern World PRElizabeth GonzagaNo ratings yet

- Saint Vincent College of Cabuyao Brgy. Mamatid, City of Cabuyao, Laguna Job Order Costing Prelim Exam-PART 1 I. True or FalseDocument6 pagesSaint Vincent College of Cabuyao Brgy. Mamatid, City of Cabuyao, Laguna Job Order Costing Prelim Exam-PART 1 I. True or FalseGennelyn Grace PenaredondoNo ratings yet

- Good Governance and Social ResponsibilityDocument26 pagesGood Governance and Social ResponsibilitySeniorb LemhesNo ratings yet

- Unit IiDocument3 pagesUnit IiKim AnaeNo ratings yet

- Corporate Profile: Metropolitan Bank and Trust CompanyDocument54 pagesCorporate Profile: Metropolitan Bank and Trust CompanyAnn Camille Joaquin100% (1)

- Request For Certificate of Compensation/Tax Withheld (BIR FORM NO. 2316)Document1 pageRequest For Certificate of Compensation/Tax Withheld (BIR FORM NO. 2316)CJ GonzalesNo ratings yet

- General PrinciplesDocument84 pagesGeneral PrinciplesHazelNo ratings yet

- Unit - 5 BECG - Corporate Social ResponsibilitiesDocument7 pagesUnit - 5 BECG - Corporate Social ResponsibilitiesrahulNo ratings yet

- Advanced M ADocument276 pagesAdvanced M ATasleem Faraz MinhasNo ratings yet

- Accounting and Its Environment - PowerPoint PresentationDocument30 pagesAccounting and Its Environment - PowerPoint PresentationBhea G. ManaloNo ratings yet

- Accounting For ManagersDocument185 pagesAccounting For ManagersFenny Todarmal100% (1)

- How To Calculate Gross ProfitDocument3 pagesHow To Calculate Gross ProfitQais WaqasNo ratings yet

- Standard Normal DistributionDocument25 pagesStandard Normal DistributionMarcy BoralNo ratings yet

- Reviewer P.I 1Document39 pagesReviewer P.I 1Pabz AgnoNo ratings yet

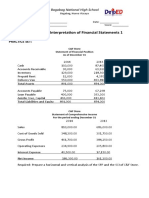

- Practice Set - Analysis of FS1Document1 pagePractice Set - Analysis of FS1marissa casareno almueteNo ratings yet

- Business Law - Corporate Social ResponsibilityDocument20 pagesBusiness Law - Corporate Social ResponsibilityMuhammad Zain ShahidNo ratings yet

- OpMan TQMDocument3 pagesOpMan TQMMia CasasNo ratings yet

- Aishino EnterprisesDocument1 pageAishino EnterprisesTin SoriaNo ratings yet

- GGSR Prelim ReviewerDocument12 pagesGGSR Prelim ReviewerRay MundNo ratings yet

- Ethics: Basic Concepts and IssuesDocument15 pagesEthics: Basic Concepts and IssuesAdam Martinez100% (1)

- ACTBAS 1 Lecture 6 Notes Accounting Cycle of A Service Business Part I: Journalizing, Posting and Trial BalanceDocument22 pagesACTBAS 1 Lecture 6 Notes Accounting Cycle of A Service Business Part I: Journalizing, Posting and Trial BalanceAA Del Rosario AlipioNo ratings yet

- Math of Investment: Name: Joana Lhyn A. Rudas Gr/Sec: 11 HE (D)Document12 pagesMath of Investment: Name: Joana Lhyn A. Rudas Gr/Sec: 11 HE (D)eunha allaybanNo ratings yet

- Accouting PrinciplesDocument5 pagesAccouting PrinciplesPriyanka RawoolNo ratings yet

- Module 10 - Moral DeliberationDocument6 pagesModule 10 - Moral Deliberationseulgi kimNo ratings yet

- AssignmentDocument17 pagesAssignmentDiana BernalNo ratings yet

- Updated Quiz BeeDocument11 pagesUpdated Quiz Beedandy boneteNo ratings yet

- Introduction To Accounting & Branches PDFDocument31 pagesIntroduction To Accounting & Branches PDFBpMolinaTeanoNo ratings yet

- Pa I Chapter 1Document16 pagesPa I Chapter 1Hussen Abdulkadir100% (1)

- Module For Managerial Accounting-Job Order CostingDocument17 pagesModule For Managerial Accounting-Job Order CostingMary De JesusNo ratings yet

- Mirabueno (Activity 1 Essay)Document2 pagesMirabueno (Activity 1 Essay)Jencelle MirabuenoNo ratings yet

- Basic Accounting EquationDocument4 pagesBasic Accounting EquationMuhammad AhmadNo ratings yet

- Accounts Debit Credit: Normal Balance Normal BalanceDocument4 pagesAccounts Debit Credit: Normal Balance Normal BalanceVG R1NG3RNo ratings yet

- Income and Business TaxationDocument69 pagesIncome and Business TaxationMarie CarreraNo ratings yet

- Midterm Income TaxDocument2 pagesMidterm Income TaxChristy BascoNo ratings yet

- Basic Accouting DefnationsDocument6 pagesBasic Accouting DefnationsSyed Amir Waqar100% (1)

- Unit 2: PUP Philosophy, Vision, Mission, Shared Values and Principles, and Ten PillarsDocument3 pagesUnit 2: PUP Philosophy, Vision, Mission, Shared Values and Principles, and Ten PillarsProspero, Elmo Maui R.No ratings yet

- ACC10 L1 01 Fundamentals of Accounting CgomezDocument6 pagesACC10 L1 01 Fundamentals of Accounting CgomezccgomezNo ratings yet

- RPH ManaloDocument4 pagesRPH ManaloAristeia NotesNo ratings yet

- Acctg 1Document8 pagesAcctg 1justineNo ratings yet

- ACCTBA1-Accounting Basics (Lecture)Document12 pagesACCTBA1-Accounting Basics (Lecture)twixterbunnyNo ratings yet

- Accounting For Non Accountant Syllabus PDFDocument8 pagesAccounting For Non Accountant Syllabus PDFJoel JuanzoNo ratings yet

- 1.6salaries and WagesDocument45 pages1.6salaries and WagesJes SitNo ratings yet

- Statement of Comprehensive Income (SCI) : Lesson 2Document20 pagesStatement of Comprehensive Income (SCI) : Lesson 2Rojane L. AlcantaraNo ratings yet

- For Mutual Mistakes of Fact, The Usual Remedy Is That The Courts Declare The Contract Void. The Parties Are Not Bound To Its Terms and Neither Party Has To Perform The Duties Listed in The AgreementDocument6 pagesFor Mutual Mistakes of Fact, The Usual Remedy Is That The Courts Declare The Contract Void. The Parties Are Not Bound To Its Terms and Neither Party Has To Perform The Duties Listed in The AgreementAdmin cNo ratings yet

- Arucio ABPA 3NC (PA318-Ethics and Accountability-In-Public-Service)Document33 pagesArucio ABPA 3NC (PA318-Ethics and Accountability-In-Public-Service)EMMANUELNo ratings yet

- GAAP AssignmentDocument4 pagesGAAP Assignmentmuhammad kashif100% (1)

- MATHDocument6 pagesMATHRheigneNo ratings yet

- CFAS 04 Conceptual Framework - Underlying AssumptionsDocument7 pagesCFAS 04 Conceptual Framework - Underlying AssumptionsAdriana Del rosarioNo ratings yet

- Income StatementDocument32 pagesIncome StatementAllen Ray TraqueñaNo ratings yet

- Managerial Accounting 10th Edition Crosson Test BankDocument65 pagesManagerial Accounting 10th Edition Crosson Test Bankgosaye desalegnNo ratings yet

- MMW Activity 03Document1 pageMMW Activity 03Mark TayagNo ratings yet

- Ethics Chapter1 MergedDocument56 pagesEthics Chapter1 MergedCherrielyn Dela CruzNo ratings yet

- What Is Funds Management?Document2 pagesWhat Is Funds Management?KidMonkey2299No ratings yet

- English Technical Writing SamplesDocument27 pagesEnglish Technical Writing Samplesabaine20% (2)

- BIR ComputationsDocument10 pagesBIR Computationsbull jack100% (1)

- Mixed Income EarnersDocument6 pagesMixed Income EarnersEzi AngelesNo ratings yet

- ADVISORY Conduct of The Training On The Enhanced LGU Integrated Financial Tools LIFT System in Region VI Batch 4Document2 pagesADVISORY Conduct of The Training On The Enhanced LGU Integrated Financial Tools LIFT System in Region VI Batch 4bull jackNo ratings yet

- CONFLICT-MANAGEMENT ExeDevDocument23 pagesCONFLICT-MANAGEMENT ExeDevbull jackNo ratings yet

- Starbucks Case Solution Fred R DavidDocument13 pagesStarbucks Case Solution Fred R Davidbull jackNo ratings yet

- Exe DevelopmentDocument3 pagesExe Developmentbull jackNo ratings yet

- Case Study and FormatDocument6 pagesCase Study and Formatbull jackNo ratings yet

- Executive DevelopmentDocument11 pagesExecutive Developmentbull jackNo ratings yet

- Parental Consent WilsonDocument1 pageParental Consent Wilsonbull jackNo ratings yet

- LCC Batch 95 FINALDocument1 pageLCC Batch 95 FINALbull jackNo ratings yet

- Degree Wheel BasiscsDocument3 pagesDegree Wheel Basiscsbull jackNo ratings yet

- XRM 125 Stock JetsDocument2 pagesXRM 125 Stock Jetsbull jack100% (1)

- Real Property PDFDocument36 pagesReal Property PDFbull jackNo ratings yet

- A Short Paper Explaining What Is ICT.: by Samuel Mandebvu Created: Friday, 20 June 2014Document5 pagesA Short Paper Explaining What Is ICT.: by Samuel Mandebvu Created: Friday, 20 June 2014bull jackNo ratings yet

- Local Taxation - PDFXDocument20 pagesLocal Taxation - PDFXbull jackNo ratings yet

- Coordinating and Communicating Local Treasury Matters With StakeholdersDocument38 pagesCoordinating and Communicating Local Treasury Matters With Stakeholdersbull jack75% (4)

- La Carlota City CollegeDocument6 pagesLa Carlota City Collegebull jackNo ratings yet

- BIR ComputationsDocument10 pagesBIR Computationsbull jack100% (1)

- Velasco v. ComelecDocument3 pagesVelasco v. ComelecBeya AmaroNo ratings yet

- 01-CIR v. Campos Rueda G.R. No. L - 13250 October 29, 1971Document4 pages01-CIR v. Campos Rueda G.R. No. L - 13250 October 29, 1971Jopan SJNo ratings yet

- Santiago v. C.F. SharpDocument6 pagesSantiago v. C.F. SharpRyan Jhay YangNo ratings yet

- Maranaw Hotels V CADocument9 pagesMaranaw Hotels V CACistron ExonNo ratings yet

- IPC Cases For Discussion PDFDocument393 pagesIPC Cases For Discussion PDFDolly Singh OberoiNo ratings yet

- Aya vs. Bigornia Facts: Licuanan vs. Melo FactsDocument2 pagesAya vs. Bigornia Facts: Licuanan vs. Melo FactsKIMbNo ratings yet

- Encarnacion v. AmigoDocument2 pagesEncarnacion v. Amigolouis jansenNo ratings yet

- Salazar v. QuiambaoDocument4 pagesSalazar v. QuiambaoANNA MARIE MENDOZANo ratings yet

- Revenue Memorandum Order No. 25-2020Document1 pageRevenue Memorandum Order No. 25-2020Cliff DaquioagNo ratings yet

- Foia Request Denial (Name Redacted)Document3 pagesFoia Request Denial (Name Redacted)Fuzzy PandaNo ratings yet

- Digest-Tanguilig v. CADocument2 pagesDigest-Tanguilig v. CANamiel Maverick D. Balina100% (1)

- Remedial Law: Civil Procedure: G.R. No. 218235/G.R. No. 218266/G.R. No. 218903/G.R. No. 219162Document3 pagesRemedial Law: Civil Procedure: G.R. No. 218235/G.R. No. 218266/G.R. No. 218903/G.R. No. 219162Keangela LouiseNo ratings yet

- The Andhra Pradesh Buildings (Lease, Rent and Eviction) Control (Amendment) Act, 2005Document7 pagesThe Andhra Pradesh Buildings (Lease, Rent and Eviction) Control (Amendment) Act, 2005Koteswara RaoNo ratings yet

- Corpo DigestsDocument21 pagesCorpo DigestsJf ManejaNo ratings yet

- The Hon'Ble Mr. Justice K.Ravichandrabaabu: W.P.No.26187 of 2019Document10 pagesThe Hon'Ble Mr. Justice K.Ravichandrabaabu: W.P.No.26187 of 2019ACCTLVO 35No ratings yet

- Vda. de San Agustin vs. Commissioner of Internal RevenueDocument11 pagesVda. de San Agustin vs. Commissioner of Internal RevenueMaria Nicole VaneeteeNo ratings yet

- Pinecrest OrdinanceDocument4 pagesPinecrest OrdinanceChris GothnerNo ratings yet

- Subpoena For Depos.-Decues Tecum For Pinellas County Sheriff's Employee Tammy DriverDocument2 pagesSubpoena For Depos.-Decues Tecum For Pinellas County Sheriff's Employee Tammy DriverJames McLynasNo ratings yet

- (U) Daily Activity Report: Marshall DistrictDocument6 pages(U) Daily Activity Report: Marshall DistrictFauquier NowNo ratings yet

- 12 Cuyugan v. Baron FullDocument5 pages12 Cuyugan v. Baron FullJaysieMicabaloNo ratings yet

- Judicial Affidavit YbanezDocument5 pagesJudicial Affidavit YbanezJan Niño100% (3)

- Upreme QI:ourt: 31/epublic of Tbe T) BilippinesDocument9 pagesUpreme QI:ourt: 31/epublic of Tbe T) BilippinescitizenNo ratings yet

- PEOPLE Vs ANDRE MARTI DigestDocument1 pagePEOPLE Vs ANDRE MARTI DigestJC100% (3)

- Repaso de Examen Inglés 6 PrimariaDocument3 pagesRepaso de Examen Inglés 6 PrimariaZSHADISHNo ratings yet

- Petitioners: en BancDocument4 pagesPetitioners: en BancAlisha VergaraNo ratings yet

- 2008 Fall DefenderDocument24 pages2008 Fall DefenderHarris County Criminal Lawyers AssociationNo ratings yet

- Virgin Records America, Inc v. Thomas - Document No. 97Document30 pagesVirgin Records America, Inc v. Thomas - Document No. 97Justia.comNo ratings yet

- Investment AgreementDocument2 pagesInvestment AgreementRodrigo AbanNo ratings yet

- Agape Child Abuse Lawsuit: JP Vs Agape Baptist Church Et AlDocument11 pagesAgape Child Abuse Lawsuit: JP Vs Agape Baptist Church Et AlBrian KentNo ratings yet