You might also like

- How To Buy A HouseDocument4 pagesHow To Buy A Housejosephjohnmzc4649No ratings yet

- Lodge Officers Duties of The LodgeDocument2 pagesLodge Officers Duties of The LodgeKeny DrescherNo ratings yet

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNo ratings yet

- IEEE STD 56-2016Document86 pagesIEEE STD 56-2016RoySnk100% (2)

- Nomination ScriptDocument2 pagesNomination ScriptLorenzo CuestaNo ratings yet

- National Budget's New FaceDocument12 pagesNational Budget's New FaceraineydaysNo ratings yet

- My 10-Day Work Immerssion Sample JournalDocument10 pagesMy 10-Day Work Immerssion Sample Journaltaylor swiftyyy73% (11)

- Awareness on Drawing Control ProceduresDocument16 pagesAwareness on Drawing Control ProceduresVinod R MenonNo ratings yet

- Drug Awareness and Prevention Program PDFDocument6 pagesDrug Awareness and Prevention Program PDFMarcos Bulay OgNo ratings yet

- United Polyresins v. PinuelaDocument3 pagesUnited Polyresins v. PinuelaIge OrtegaNo ratings yet

- Financial PlanningDocument22 pagesFinancial Planningangshu002085% (13)

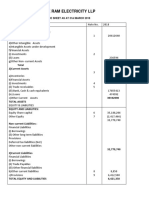

- Shree Ram Electricity LLP: 1) Non-Current AssetsDocument5 pagesShree Ram Electricity LLP: 1) Non-Current AssetsSaba MullaNo ratings yet

- Requirements For Fundamentals of Accountancy, Busines S,& ManagementDocument15 pagesRequirements For Fundamentals of Accountancy, Busines S,& ManagementRichard John Ilagan DioknoNo ratings yet

- AFM Project Report FinalDocument19 pagesAFM Project Report FinalRitu KumariNo ratings yet

- Fma (Repaired)Document12 pagesFma (Repaired)pappunaagraajNo ratings yet

- Financial Statement Analysis ToolsDocument32 pagesFinancial Statement Analysis ToolsVISHNU SATHEESHNo ratings yet

- CHB Mar19 PDFDocument14 pagesCHB Mar19 PDFSajeetha MadhavanNo ratings yet

- A Study On The Analysis of Financial Performance With Special Reference To Ramco Cement LTDDocument8 pagesA Study On The Analysis of Financial Performance With Special Reference To Ramco Cement LTDTJPRC PublicationsNo ratings yet

- 1 (A) - As Compared To The Year 2019, The Owners' Equity Has Decreased in The Year 2020. What Is The Most Important Reason For The Same?Document5 pages1 (A) - As Compared To The Year 2019, The Owners' Equity Has Decreased in The Year 2020. What Is The Most Important Reason For The Same?Akshat BansalNo ratings yet

- US GAAP - Financials Dec'2021Document50 pagesUS GAAP - Financials Dec'2021ashokdb2kNo ratings yet

- Reliance Industries LTD.: Balance SheetDocument10 pagesReliance Industries LTD.: Balance SheetAayush PeriwalNo ratings yet

- Cocoaland Holdings 2Q19 resultsDocument14 pagesCocoaland Holdings 2Q19 resultsSajeetha MadhavanNo ratings yet

- LG Chem, Ltd. and Subsidiaries: Consolidated Interim Financial Statements June 30, 2018 and 2017Document72 pagesLG Chem, Ltd. and Subsidiaries: Consolidated Interim Financial Statements June 30, 2018 and 2017enrique serrano100% (1)

- CHB Sep19 PDFDocument14 pagesCHB Sep19 PDFSajeetha MadhavanNo ratings yet

- Nuru Ethiopia Final Audit Report 2019Document22 pagesNuru Ethiopia Final Audit Report 2019Elias Abubeker AhmedNo ratings yet

- Cocoaland Holdings Berhad: (Incorporated in Malaysia)Document15 pagesCocoaland Holdings Berhad: (Incorporated in Malaysia)Sajeetha MadhavanNo ratings yet

- Basic Accounts Ca1Document5 pagesBasic Accounts Ca1shivanigas morwaNo ratings yet

- IFRS - Financials Mar'2022Document72 pagesIFRS - Financials Mar'2022Aashish TiwariNo ratings yet

- Financial Ratio AnalysisDocument31 pagesFinancial Ratio AnalysisKeisha Kaye SaleraNo ratings yet

- Accounting & Financial Reporting CarrefourDocument26 pagesAccounting & Financial Reporting Carrefouryasser massryNo ratings yet

- Cocoland Holdings 4Q 2018 Results SummaryDocument15 pagesCocoland Holdings 4Q 2018 Results SummarySajeetha MadhavanNo ratings yet

- A. Objective or Purpose of The StudyDocument55 pagesA. Objective or Purpose of The Studymgp 1601No ratings yet

- Liquidation Basis AccountsDocument18 pagesLiquidation Basis AccountsUsman AliNo ratings yet

- Cash Flows Statement - Two ExamplesDocument4 pagesCash Flows Statement - Two Examplesakash srivastavaNo ratings yet

- Ferreycorp Audited Financial Statements 2020Document84 pagesFerreycorp Audited Financial Statements 2020Eduardo ArcosNo ratings yet

- Financial Reporting and Analysis PDFDocument2 pagesFinancial Reporting and Analysis PDFTushar VatsNo ratings yet

- IN Financial Management 1: Leyte CollegesDocument20 pagesIN Financial Management 1: Leyte CollegesJeric LepasanaNo ratings yet

- Case Study RE AgroDocument3 pagesCase Study RE Agroamatuer3293No ratings yet

- Lucky Cement Final Project Report On: Financial Statement AnalysisDocument25 pagesLucky Cement Final Project Report On: Financial Statement AnalysisPrecious BarbieNo ratings yet

- FA Balance Sheet Analysis of CEAT Ltd and JK Tyre IndustriesDocument2 pagesFA Balance Sheet Analysis of CEAT Ltd and JK Tyre IndustriesSaichinNo ratings yet

- Screenshot 2023-12-04 at 6.26.08 PMDocument25 pagesScreenshot 2023-12-04 at 6.26.08 PMdokaniavedikaNo ratings yet

- B Sheet 14-15Document106 pagesB Sheet 14-15Gagan Soni deaf100% (1)

- Hindalco Case StudyDocument21 pagesHindalco Case StudyShrey KashyapNo ratings yet

- A Wholly-Owned Subsidiary of Philippine National Oil CompanyDocument4 pagesA Wholly-Owned Subsidiary of Philippine National Oil CompanyLolita CalaycayNo ratings yet

- 2013 Financial ReportDocument36 pages2013 Financial Reportvijay dharmavaramNo ratings yet

- SM Report G3Document29 pagesSM Report G3SriSaraswathyNo ratings yet

- CPG Annual Report 2014Document56 pagesCPG Annual Report 2014Anonymous 2vtxh4No ratings yet

- Learners'+Sheet_Final_Dec+Cohort (1)Document23 pagesLearners'+Sheet_Final_Dec+Cohort (1)pre.meh21No ratings yet

- Forecasting ProblemsDocument7 pagesForecasting ProblemsJoel Pangisban0% (3)

- Financial Accounting Analysis for Godfrey Phillips India LimitedDocument8 pagesFinancial Accounting Analysis for Godfrey Phillips India LimitedSOURAV ACHARJEENo ratings yet

- Chap 003Document80 pagesChap 003Châu Anh ĐàoNo ratings yet

- 8 Session 20 Pillar 02 Finance Management Part 1Document13 pages8 Session 20 Pillar 02 Finance Management Part 1Azfah AliNo ratings yet

- K. V. Pendharkar College of Arts, Scienceand Commerce (Autonomous)Document12 pagesK. V. Pendharkar College of Arts, Scienceand Commerce (Autonomous)Nayna PanigrahiNo ratings yet

- Introduction of MTM: StatementDocument23 pagesIntroduction of MTM: StatementALI SHER HaidriNo ratings yet

- Discounted Cash FlowDocument9 pagesDiscounted Cash FlowAditya JandialNo ratings yet

- Chapter 3. Finance Department 3.1 Essar Steel LTD.: 3.1.1 P&L AccountDocument7 pagesChapter 3. Finance Department 3.1 Essar Steel LTD.: 3.1.1 P&L AccountT.Y.B68PATEL DHRUVNo ratings yet

- Itlog Ni JanDocument10 pagesItlog Ni JanAlejandro Javellana Paras IVNo ratings yet

- Ratio Analysis of Bajaj AllianzDocument9 pagesRatio Analysis of Bajaj AllianzAkshat JainNo ratings yet

- RMH Interim ResultsDocument37 pagesRMH Interim ResultsaalalalNo ratings yet

- Performance Evaluation and Ratio Analysis - Meghna Cement - R1Document11 pagesPerformance Evaluation and Ratio Analysis - Meghna Cement - R1Sayed Abu Sufyan100% (1)

- ACCG305-Auditing and Assurance Services Case Study AssignmentDocument8 pagesACCG305-Auditing and Assurance Services Case Study AssignmentZee ZaidiNo ratings yet

- POSCO Consolidated FY15Q4 Final (Signed)Document125 pagesPOSCO Consolidated FY15Q4 Final (Signed)SAMUEL PATRICK LELINo ratings yet

- AGL Financial Analysis ReportDocument13 pagesAGL Financial Analysis ReportMohamed NaieemNo ratings yet

- Hul Ratio AnalysisDocument14 pagesHul Ratio Analysisvviek100% (1)

- Term PaperDocument11 pagesTerm PaperSarose ThapaNo ratings yet

- Ifrs (Usd) (En)Document49 pagesIfrs (Usd) (En)Ameya KulkarniNo ratings yet

- CDC-R3 Es2015Document3 pagesCDC-R3 Es2015Aram PetrosyanNo ratings yet

- Ifrs Gapp InfosysDocument21 pagesIfrs Gapp Infosysashishsuman0% (1)

- Merit Scholarship FormDocument2 pagesMerit Scholarship FormBechlor StudyNo ratings yet

- WCE Application FormDocument1 pageWCE Application FormMarianneNo ratings yet

- P7 Questions R. KIT 4Document95 pagesP7 Questions R. KIT 4Haider MalikNo ratings yet

- Assignment For Week 10 - 2022Document7 pagesAssignment For Week 10 - 2022Rajveer deepNo ratings yet

- 02.spouses Firme v. Bukal Enterprises and Development Corp., G.R. No. 146608, October 23, 2003Document20 pages02.spouses Firme v. Bukal Enterprises and Development Corp., G.R. No. 146608, October 23, 2003HNo ratings yet

- Branch JointDocument2 pagesBranch Jointskipina74No ratings yet

- Accounts Project ComprehensiveDocument17 pagesAccounts Project ComprehensiveArsh khan100% (1)

- Java Software Solutions 8th Edition Lewis Test BankDocument25 pagesJava Software Solutions 8th Edition Lewis Test BankSarahDavidsoniqsn100% (53)

- Grounds of AppealDocument2 pagesGrounds of AppealThia NizamNo ratings yet

- Doctrine of State Continuity: October 2, 2018Document3 pagesDoctrine of State Continuity: October 2, 2018Japoy Regodon EsquilloNo ratings yet

- United States v. Richard Alvin Woodring, AKA Carlton D. Woodring, AKA Dee Burke, 446 F.2d 733, 10th Cir. (1971)Document7 pagesUnited States v. Richard Alvin Woodring, AKA Carlton D. Woodring, AKA Dee Burke, 446 F.2d 733, 10th Cir. (1971)Scribd Government DocsNo ratings yet

- Fee Notification For The Academic Year 2023-24Document15 pagesFee Notification For The Academic Year 2023-24Makrand DeouskarNo ratings yet

- Building certification literature review under Malaysia's CCC systemDocument6 pagesBuilding certification literature review under Malaysia's CCC systemHiew fuxiangNo ratings yet

- Government Motion For Protective Order in Raymond "Shrimp Boy" Chow CaseDocument18 pagesGovernment Motion For Protective Order in Raymond "Shrimp Boy" Chow CaseSan Francisco ExaminerNo ratings yet

- Retail Issues and ChallengesDocument23 pagesRetail Issues and ChallengesJohn ZackNo ratings yet

- Hospital Controlled Drug ProceduresDocument3 pagesHospital Controlled Drug ProceduresvaniyaNo ratings yet

- Statement Nov 20 XXXXXXXX1452Document11 pagesStatement Nov 20 XXXXXXXX1452Rohit raagNo ratings yet

- Rizal's Dramatic Last HoursDocument2 pagesRizal's Dramatic Last HoursErrol LopezNo ratings yet

- Compal Confidential: VALEA/VALEB Schematics DocumentDocument52 pagesCompal Confidential: VALEA/VALEB Schematics Documentkolargol72No ratings yet

- Guide to Analyzing and Interpreting Financial InformationDocument80 pagesGuide to Analyzing and Interpreting Financial InformationBoogy Grim100% (1)

- Transfer of Property Act, 1882 Definition and Scope of Immovable PropertyDocument4 pagesTransfer of Property Act, 1882 Definition and Scope of Immovable PropertyHARSH KUMARNo ratings yet