You might also like

- Assignment # 1 Case Study: KASB Bank Limited: Capital ShortageDocument5 pagesAssignment # 1 Case Study: KASB Bank Limited: Capital Shortagewaqar mansoorNo ratings yet

- Assignment 2 Kashf BankDocument5 pagesAssignment 2 Kashf BankAsad Memon100% (1)

- Assignment # 2 Case Study: From Kashf Foundation To Kashf Microfinance Bank - Changing Organizational IdentitiesDocument5 pagesAssignment # 2 Case Study: From Kashf Foundation To Kashf Microfinance Bank - Changing Organizational Identitieswaqar mansoor100% (1)

- Assignment 4 - Al ShaheerDocument5 pagesAssignment 4 - Al Shaheerwaqar mansoorNo ratings yet

- SFAD Assignment - AkhuwatDocument1 pageSFAD Assignment - AkhuwatAsad MemonNo ratings yet

- Internship Sindh BankDocument34 pagesInternship Sindh BankKR Burki100% (1)

- Bank Al Habib BestDocument74 pagesBank Al Habib BestAbdul Ghafoor100% (1)

- Shan Foods - Group 8 (Consumer Behaviour)Document18 pagesShan Foods - Group 8 (Consumer Behaviour)SYED HARIS HASHMI100% (1)

- Olpers FinalDocument33 pagesOlpers FinalUshnaTahir100% (1)

- Bank Alfalah: A Leading Private Bank in PakistanDocument28 pagesBank Alfalah: A Leading Private Bank in PakistanHamza Butt100% (3)

- Case Study Kashf Bank AssigmnetDocument2 pagesCase Study Kashf Bank AssigmnetabiraNo ratings yet

- Supply Chain Analysis Bisconi Pvt. LTDDocument14 pagesSupply Chain Analysis Bisconi Pvt. LTDKainat BaigNo ratings yet

- National Foods LTDDocument16 pagesNational Foods LTDSufiyan Alaam0% (1)

- Organizational Hierarchy of MCBDocument4 pagesOrganizational Hierarchy of MCBSana Javaid100% (3)

- Strategic Management Final Report Bank Al HabibDocument20 pagesStrategic Management Final Report Bank Al HabibBrave Ali KhatriNo ratings yet

- BCG Matrix - NishatDocument3 pagesBCG Matrix - Nishatbakhoo12No ratings yet

- Management Hierarchy: Askari Bank LimitedDocument14 pagesManagement Hierarchy: Askari Bank LimitedEeshaa MalikNo ratings yet

- Sehrish Khan UBL ProjectDocument62 pagesSehrish Khan UBL Projectsherybalouch100% (1)

- A Complete Report On HBL ManagementDocument21 pagesA Complete Report On HBL ManagementSidra IdreesNo ratings yet

- UBL Operations ManagementDocument18 pagesUBL Operations ManagementSaad HamidNo ratings yet

- Marketing Plan - Unilever PakistanDocument35 pagesMarketing Plan - Unilever PakistanVenkata Sabareesan0% (1)

- Marketing Strategies of DawlanceDocument13 pagesMarketing Strategies of DawlanceUsman AzharNo ratings yet

- Project On National FoodsDocument2 pagesProject On National FoodsMano_Bili8950% (2)

- Punjab Oil Mills LimitedDocument9 pagesPunjab Oil Mills LimitedMuhammadAli AbidNo ratings yet

- Term Report On Engro Foods & Millac Pakistan-Organizational BehaviorDocument75 pagesTerm Report On Engro Foods & Millac Pakistan-Organizational Behaviorfarah_poonawala100% (9)

- Marketing Mix of Bank Al Habib PakistanDocument6 pagesMarketing Mix of Bank Al Habib Pakistankhalid100% (2)

- Ratio Analysis Bank AL Habib Ltd.Document23 pagesRatio Analysis Bank AL Habib Ltd.Hussain M Raza33% (3)

- Milk PakDocument26 pagesMilk PakMaira HassanNo ratings yet

- Pakistan’s First Successful REIT Launch and ChallengesDocument4 pagesPakistan’s First Successful REIT Launch and Challengeswaqar mansoorNo ratings yet

- Word Report of Bank Al HabibDocument22 pagesWord Report of Bank Al HabibAdeel SajjadNo ratings yet

- Askari Bank Marketing Internship ReportDocument74 pagesAskari Bank Marketing Internship Report✬ SHANZA MALIK ✬50% (6)

- SWOT Analysis of PsoDocument2 pagesSWOT Analysis of Psobilalabbasi4674740% (2)

- HBL Swot AnalysisDocument6 pagesHBL Swot AnalysisAzeem Ahmed100% (1)

- Internship Report On Faysal Bank Limited by Naeem AhmedDocument36 pagesInternship Report On Faysal Bank Limited by Naeem AhmedNaeem Ahmed75% (12)

- Bank Alfalah Case Study Presentation by Ali Raza Mi11MBA025Document35 pagesBank Alfalah Case Study Presentation by Ali Raza Mi11MBA025Ali RazaNo ratings yet

- HRMDocument25 pagesHRMAsma Shoaib100% (1)

- National FoodDocument4 pagesNational FoodAdnan Qayum50% (2)

- Shan FoodsDocument21 pagesShan Foodsnoman100% (1)

- Mehran SpiceDocument3 pagesMehran SpiceSYED HARIS HASHMINo ratings yet

- Answer Costs of Al Shaheer Corporation Going PublicDocument3 pagesAnswer Costs of Al Shaheer Corporation Going PublicSyed Saqlain Raza JafriNo ratings yet

- Ismail Industries Limited Case Study Report on Candyland Confectionery CompanyDocument141 pagesIsmail Industries Limited Case Study Report on Candyland Confectionery Companyblueroyal60% (5)

- Ratio Analysis of Bank Alfalah LimitedDocument22 pagesRatio Analysis of Bank Alfalah LimitedAnonymous uDP6XEHs100% (1)

- Shan FoodsDocument13 pagesShan FoodsHaseeb Ahmed100% (1)

- The First Meat Sector IPO CASEDocument3 pagesThe First Meat Sector IPO CASEabiraNo ratings yet

- Meezan Bank - Banking ProductsDocument103 pagesMeezan Bank - Banking Productsskepticalbeing63% (19)

- Mudasir Intership Report 27-10-2019Document33 pagesMudasir Intership Report 27-10-2019Masroor Ali LarikNo ratings yet

- Internship Report on Meezan Bank LimitedDocument24 pagesInternship Report on Meezan Bank LimitedZIA UL REHMANNo ratings yet

- National FoodsDocument47 pagesNational FoodsNabeel Khaliq67% (3)

- EBM's journey to becoming Pakistan's leading biscuit manufacturerDocument32 pagesEBM's journey to becoming Pakistan's leading biscuit manufacturerRehanSheikh50% (2)

- PSO Final ReportDocument38 pagesPSO Final ReportAdnan Ahmed0% (1)

- KASB Bank Capital Shortage AnalysisDocument4 pagesKASB Bank Capital Shortage AnalysisDaniyal MirzaNo ratings yet

- Syed Saqlain Raza Jafri 63598Document4 pagesSyed Saqlain Raza Jafri 63598Syed Saqlain Raza JafriNo ratings yet

- KASB Bank's Capital Shortage and State Bank InterventionDocument4 pagesKASB Bank's Capital Shortage and State Bank InterventionAsad MemonNo ratings yet

- Name: Sonhera Sheikh S.id: 6606 Assignment #1 Course: Strategic Financial Analysis & DesignDocument3 pagesName: Sonhera Sheikh S.id: 6606 Assignment #1 Course: Strategic Financial Analysis & Designsonhera sheikhNo ratings yet

- The KASB Bank Scandal SynopsisDocument6 pagesThe KASB Bank Scandal Synopsisnaeem_309759385No ratings yet

- Nib Bank Merger CaseDocument12 pagesNib Bank Merger CaseRenu Esrani0% (1)

- HBL's Acquisition of Barclays PakistanDocument8 pagesHBL's Acquisition of Barclays PakistanNoor-Us-Sabah GilaniNo ratings yet

- Bank: THE ROYAL BANK OF SCOTLAND LIMITED - Analysis of Financial Statements C Year 2006 - 2003 Q 2009Document4 pagesBank: THE ROYAL BANK OF SCOTLAND LIMITED - Analysis of Financial Statements C Year 2006 - 2003 Q 2009builder007No ratings yet

- Business Standard-The M&M-RBL Bank Saga by Tamal BandyopadhyayDocument1 pageBusiness Standard-The M&M-RBL Bank Saga by Tamal BandyopadhyayGarima ChaudhryNo ratings yet

- Strategic Financial Analysis & Design Assignment # 2Document4 pagesStrategic Financial Analysis & Design Assignment # 2Daniyal MirzaNo ratings yet

- Sheet metal plus simulation improves quality at Volvo CarsDocument8 pagesSheet metal plus simulation improves quality at Volvo Carswaqar mansoorNo ratings yet

- Die Simulation:: Measure, Mitigate, Control, Compensate For SpringbackDocument4 pagesDie Simulation:: Measure, Mitigate, Control, Compensate For Springbackwaqar mansoorNo ratings yet

- Die Simulation:: Measure, Mitigate, Control, Compensate For SpringbackDocument4 pagesDie Simulation:: Measure, Mitigate, Control, Compensate For Springbackwaqar mansoorNo ratings yet

- Tech Update: Springback Prediction Yields Automotive Parts Without Costly Tool RecutsDocument2 pagesTech Update: Springback Prediction Yields Automotive Parts Without Costly Tool RecutstuấnNo ratings yet

- FOCUS ON CAD/CAM SOFTWARE FOR OPTIMIZED TOOL DESIGNDocument3 pagesFOCUS ON CAD/CAM SOFTWARE FOR OPTIMIZED TOOL DESIGNwaqar mansoorNo ratings yet

- Danville Metal'S Forming Success Using Simulation SoftwareDocument1 pageDanville Metal'S Forming Success Using Simulation Softwarewaqar mansoorNo ratings yet

- KASB Bank Limited: Capital Shortage: Muntazar Bashir AhmedDocument22 pagesKASB Bank Limited: Capital Shortage: Muntazar Bashir AhmedSalman sajjad malikNo ratings yet

- Software Solves Springback Issues in Auto Part ManufacturingDocument1 pageSoftware Solves Springback Issues in Auto Part Manufacturingwaqar mansoorNo ratings yet

- FOCUS ON CAD/CAM SOFTWARE FOR OPTIMIZED TOOL DESIGNDocument3 pagesFOCUS ON CAD/CAM SOFTWARE FOR OPTIMIZED TOOL DESIGNwaqar mansoorNo ratings yet

- Pakistan's First Successful Launch of A Real Estate Investment Trust-Dolmen City (REIT) - (Shariah Compliant Rental REIT Scheme)Document18 pagesPakistan's First Successful Launch of A Real Estate Investment Trust-Dolmen City (REIT) - (Shariah Compliant Rental REIT Scheme)waqar mansoorNo ratings yet

- STAMPING Journal - May June 2021Document4 pagesSTAMPING Journal - May June 2021waqar mansoorNo ratings yet

- MetalForming Magazine - 2020 12Document2 pagesMetalForming Magazine - 2020 12waqar mansoorNo ratings yet

- Zulfiqar2017 PDFDocument21 pagesZulfiqar2017 PDFfelizNo ratings yet

- Assignment 5 - Waseela FoundationDocument3 pagesAssignment 5 - Waseela Foundationwaqar mansoorNo ratings yet

- Waseela Foundation: Accounting For Zakat: Junaid Ashraf and Abdul RaufDocument6 pagesWaseela Foundation: Accounting For Zakat: Junaid Ashraf and Abdul Raufwaqar mansoorNo ratings yet

- A Challenge in Governance A Case of Higher Education in PakistanDocument17 pagesA Challenge in Governance A Case of Higher Education in PakistanUmair Malik100% (1)

- Session 21 The First Meat Sector IPO Al Shaheer CorporationDocument23 pagesSession 21 The First Meat Sector IPO Al Shaheer CorporationAnas SohailNo ratings yet

- Akhuwat: Measuring Success For A Non-Profit Organization: Mohsin Bashir Ashar Saleem Ferhana AhmedDocument13 pagesAkhuwat: Measuring Success For A Non-Profit Organization: Mohsin Bashir Ashar Saleem Ferhana Ahmedwaqar mansoorNo ratings yet

- Session 21 The First Meat Sector IPO Al Shaheer CorporationDocument23 pagesSession 21 The First Meat Sector IPO Al Shaheer CorporationAnas SohailNo ratings yet

- Zulfiqar2017 PDFDocument21 pagesZulfiqar2017 PDFfelizNo ratings yet

- Pakistan’s First Successful REIT Launch and ChallengesDocument4 pagesPakistan’s First Successful REIT Launch and Challengeswaqar mansoorNo ratings yet

- Akhuwat: Measuring Success For A Non-Profit Organization: Mohsin Bashir Ashar Saleem Ferhana AhmedDocument13 pagesAkhuwat: Measuring Success For A Non-Profit Organization: Mohsin Bashir Ashar Saleem Ferhana Ahmedwaqar mansoorNo ratings yet

- Zulfiqar2017 PDFDocument21 pagesZulfiqar2017 PDFfelizNo ratings yet

- Assignment # 4 Case Study: A Challenge in Governance: A Case of Higher Education in PakistanDocument6 pagesAssignment # 4 Case Study: A Challenge in Governance: A Case of Higher Education in Pakistanwaqar mansoorNo ratings yet

- A Challenge in Governance A Case of Higher Education in PakistanDocument17 pagesA Challenge in Governance A Case of Higher Education in PakistanUmair Malik100% (1)

- Pakistan's First Successful Launch of A Real Estate Investment Trust-Dolmen City (REIT) - (Shariah Compliant Rental REIT Scheme)Document18 pagesPakistan's First Successful Launch of A Real Estate Investment Trust-Dolmen City (REIT) - (Shariah Compliant Rental REIT Scheme)waqar mansoorNo ratings yet

- Akhuwat: Measuring Success For A Non-Profit Organization: Mohsin Bashir Ashar Saleem Ferhana AhmedDocument13 pagesAkhuwat: Measuring Success For A Non-Profit Organization: Mohsin Bashir Ashar Saleem Ferhana Ahmedwaqar mansoorNo ratings yet

- KASB Bank Limited: Capital Shortage: Muntazar Bashir AhmedDocument22 pagesKASB Bank Limited: Capital Shortage: Muntazar Bashir AhmedSalman sajjad malikNo ratings yet

- Super Procure - Company IntroductionDocument14 pagesSuper Procure - Company IntroductionshadabhashimNo ratings yet

- QualificationDocument536 pagesQualificationrajaa El ansariNo ratings yet

- Equality in The Workplace: A Study of Gender Issues in Indian OrganisationsDocument17 pagesEquality in The Workplace: A Study of Gender Issues in Indian OrganisationsIshangNo ratings yet

- HP Buyside Intermediary Fee AgreementDocument2 pagesHP Buyside Intermediary Fee AgreementLivros juridicosNo ratings yet

- Security Investment Slide Notes W4-W8Document213 pagesSecurity Investment Slide Notes W4-W8priyaNo ratings yet

- Articles of Partnership and Notarial Acknowledgment PDFDocument3 pagesArticles of Partnership and Notarial Acknowledgment PDFAccounterist ShinangNo ratings yet

- Annual Report CurrentDocument19 pagesAnnual Report CurrentMitch MateychukNo ratings yet

- 3 Day Cycle - Day 2. PART 2Document12 pages3 Day Cycle - Day 2. PART 2CristóbalTobalNo ratings yet

- Strategic AnalysisDocument6 pagesStrategic AnalysisAnil KumarNo ratings yet

- Asc Coc Certificate: Controun ODocument3 pagesAsc Coc Certificate: Controun Oaktaruzzaman bethuNo ratings yet

- Modified Du Pont DecompositionDocument7 pagesModified Du Pont DecompositionSurya PrakashNo ratings yet

- ReviewDocument17 pagesReviewSreekanthReddy MangammagariNo ratings yet

- RE Sector IssuesDocument7 pagesRE Sector Issuessahaye.vikramjitNo ratings yet

- Accounting AssignmentDocument17 pagesAccounting AssignmentStrom spiritNo ratings yet

- Quiz Employee Benifits Income TaxDocument2 pagesQuiz Employee Benifits Income TaxMonica MonicaNo ratings yet

- DP Jain Datia Bhander Toll Road Projects 1mar2021Document9 pagesDP Jain Datia Bhander Toll Road Projects 1mar2021Shubham GuptaNo ratings yet

- Union Bank 1Document12 pagesUnion Bank 1bindu mathaiNo ratings yet

- Building A 3 Statement Financial Model: in ExcelDocument85 pagesBuilding A 3 Statement Financial Model: in ExcelSureshNo ratings yet

- Direct Method or Cost of Goods Sold MethodDocument2 pagesDirect Method or Cost of Goods Sold MethodNa Dem DolotallasNo ratings yet

- Bressani Real Estate - Short Sale Listing Presentation 1-12-11Document14 pagesBressani Real Estate - Short Sale Listing Presentation 1-12-11Steve Bressani0% (1)

- Taxguru - in-GST Audit GSTR-9C Practical Checklist Alongwith Audit ProcessDocument3 pagesTaxguru - in-GST Audit GSTR-9C Practical Checklist Alongwith Audit ProcesschetudaveNo ratings yet

- Bank Charter Act 1844 - enDocument15 pagesBank Charter Act 1844 - enMaxBestNo ratings yet

- British Charity Accounting Standards ImpactDocument24 pagesBritish Charity Accounting Standards ImpactTareq Yousef AbualajeenNo ratings yet

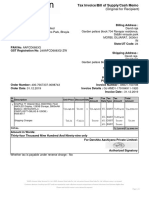

- Invoice 2Document1 pageInvoice 201bhavdip chhaniyaraNo ratings yet

- Case Study ChicoryDocument2 pagesCase Study ChicoryUmar KhattakNo ratings yet

- Axis BankDocument6 pagesAxis Banksamsung1160No ratings yet

- Loss Assessment & GST ImplicationsDocument13 pagesLoss Assessment & GST ImplicationsShiba PadhiNo ratings yet

- Attendance - Inst1 - Batch 1 & 2 (Oct.4,2021-DSF)Document2 pagesAttendance - Inst1 - Batch 1 & 2 (Oct.4,2021-DSF)Aljay LabugaNo ratings yet

- Bescom GSTN No: 29Aaccb1412G1Z5Document2 pagesBescom GSTN No: 29Aaccb1412G1Z5RajkiranaNo ratings yet

- Applied Economics (2) - 091357 - 083214Document88 pagesApplied Economics (2) - 091357 - 083214jerelynborbon22No ratings yet