You might also like

- ADM 3351-Final With SolutionsDocument14 pagesADM 3351-Final With SolutionsGraeme RalphNo ratings yet

- CFA Level 3 2012 Guideline AnswersDocument42 pagesCFA Level 3 2012 Guideline AnswersmerrylmorleyNo ratings yet

- Problem #7: Recording Transactions in A Financial Transaction WorksheetDocument17 pagesProblem #7: Recording Transactions in A Financial Transaction Worksheetfabyunaaa100% (1)

- Valuation of Bonds and SharesDocument45 pagesValuation of Bonds and SharessmsmbaNo ratings yet

- Land Bank ResoDocument1 pageLand Bank ResoErman GaraldaNo ratings yet

- PEZA CITIZENS CHARTER (Rev 10, 31 Mar 2023, 1st Edition) - Compressed PDFDocument458 pagesPEZA CITIZENS CHARTER (Rev 10, 31 Mar 2023, 1st Edition) - Compressed PDFPatrickNo ratings yet

- Bond Valuation NTHMCDocument24 pagesBond Valuation NTHMCAryal LaxmanNo ratings yet

- Case Study BondsDocument5 pagesCase Study BondsAbhijeit BhosaleNo ratings yet

- Bonds ValuationsDocument57 pagesBonds ValuationsarmailgmNo ratings yet

- Commercial Bank Management Midsem NotesDocument12 pagesCommercial Bank Management Midsem NotesWinston WongNo ratings yet

- Bond & Equity ValuationDocument72 pagesBond & Equity ValuationoddjokerNo ratings yet

- 5-Valuation of BondsDocument52 pages5-Valuation of BondsAkansh NuwalNo ratings yet

- Bonds and Their Valuation: Key Features of Bonds Bond Valuation Measuring Yield Assessing RiskDocument37 pagesBonds and Their Valuation: Key Features of Bonds Bond Valuation Measuring Yield Assessing RiskVidhi DoshiNo ratings yet

- Tutorial 3Document5 pagesTutorial 3KÃLÅÏ SMÎLĒYNo ratings yet

- Chapter - Four: Bond and Stock Valuation and The Cost of CapitalDocument10 pagesChapter - Four: Bond and Stock Valuation and The Cost of CapitalWiz Santa0% (1)

- Unit-III Bond Prices, Rates, and YieldsDocument36 pagesUnit-III Bond Prices, Rates, and YieldsAnu ShreyaNo ratings yet

- FIS Assignment 1 Bitan SahaDocument6 pagesFIS Assignment 1 Bitan SahaBitan SahaNo ratings yet

- FIN 440 - Case 5Document11 pagesFIN 440 - Case 5Samiul21100% (2)

- Term-to-Maturity Refers To The Number of Years Remaining For The Bond To Mature. Coupon: Coupon Refers To The Periodic Interest Payments That AreDocument5 pagesTerm-to-Maturity Refers To The Number of Years Remaining For The Bond To Mature. Coupon: Coupon Refers To The Periodic Interest Payments That Arehims_rajaNo ratings yet

- Valuation of Bonds and SharesDocument36 pagesValuation of Bonds and SharesnidhiNo ratings yet

- Bonds: St. Xavier's College (Autonomous), KolkataDocument9 pagesBonds: St. Xavier's College (Autonomous), KolkataIshika AgarwalNo ratings yet

- Bonds and Their ValuationDocument36 pagesBonds and Their ValuationRubab BabarNo ratings yet

- Valuation of BondsDocument49 pagesValuation of BondsSanjit SinhaNo ratings yet

- Fixed Income SecuritiesDocument19 pagesFixed Income SecuritiesShailendraNo ratings yet

- Ch2 Testbank Part 2 (2) .AnswerdDocument8 pagesCh2 Testbank Part 2 (2) .Answerdtarek ahmedNo ratings yet

- FAR Bonds and Present Value TablesDocument3 pagesFAR Bonds and Present Value Tablespoet_in_christNo ratings yet

- Valuation of Bonds and SharesDocument39 pagesValuation of Bonds and Shareskunalacharya5No ratings yet

- Chapter 12 Bond Portfolio MGMTDocument41 pagesChapter 12 Bond Portfolio MGMTsharktale2828No ratings yet

- Bond valuation and yield analysisDocument35 pagesBond valuation and yield analysisTanmay MehtaNo ratings yet

- Managing Interest RateDocument22 pagesManaging Interest RatemahadiparvezNo ratings yet

- Financial Market-Lecture 3Document27 pagesFinancial Market-Lecture 3Krish ShettyNo ratings yet

- Fixed Income Securities GuideDocument8 pagesFixed Income Securities GuideOumer ShaffiNo ratings yet

- Stocks and Bonds ValuationDocument82 pagesStocks and Bonds ValuationRonald MendozaNo ratings yet

- Bond Valuation 1Document37 pagesBond Valuation 1Nitesh SolankiNo ratings yet

- Que 5 - Bond MathematicsDocument25 pagesQue 5 - Bond MathematicsPushkaraj SaveNo ratings yet

- 3 Interest Rate and Security Valuation Part-2Document85 pages3 Interest Rate and Security Valuation Part-2harry1213No ratings yet

- Chapter 7: Interest Rates and Bond ValuationDocument36 pagesChapter 7: Interest Rates and Bond ValuationHins LeeNo ratings yet

- Module #05 - Bonds and Their ValuationDocument9 pagesModule #05 - Bonds and Their ValuationRhesus UrbanoNo ratings yet

- Bond Value - YieldDocument40 pagesBond Value - YieldSheeza AshrafNo ratings yet

- Bond Valuation: Par or Face ValueDocument9 pagesBond Valuation: Par or Face ValueMd. Abdul HaiNo ratings yet

- L2 Money Market (v2)Document27 pagesL2 Money Market (v2)Kruti BhattNo ratings yet

- 3.valuation of BondDocument9 pages3.valuation of BondSabarni ChatterjeeNo ratings yet

- UNIT 4 - Describing Fixed Income Securities (Bonds) and DerivativesDocument16 pagesUNIT 4 - Describing Fixed Income Securities (Bonds) and DerivativesCLIVENo ratings yet

- Valuation of SecuritiesDocument7 pagesValuation of SecuritiesEmmanuelNo ratings yet

- CH 4Document23 pagesCH 4Gizaw BelayNo ratings yet

- BondDocument44 pagesBondSumit VaishNo ratings yet

- Bond ValuatioDocument66 pagesBond ValuatioKanishka SinghNo ratings yet

- Bond Valuation and Yield CalculationsDocument26 pagesBond Valuation and Yield Calculationslibison1No ratings yet

- Batayang Konseptwal at Paradima NG Pag AaralDocument17 pagesBatayang Konseptwal at Paradima NG Pag AaralCassandra ManitoNo ratings yet

- Bond ValuationDocument20 pagesBond ValuationPankaj YaduvanshiNo ratings yet

- Valuation of Fixed Income InvestmentsDocument37 pagesValuation of Fixed Income InvestmentsSanjit SinhaNo ratings yet

- Valuation of Bonds NumericalsDocument30 pagesValuation of Bonds NumericalsankitNo ratings yet

- How to Value BondsDocument36 pagesHow to Value Bondsabhishek dharNo ratings yet

- Financial Management and AccountingDocument8 pagesFinancial Management and AccountingHannahPojaFeriaNo ratings yet

- Determinants of Interest RatesDocument27 pagesDeterminants of Interest RatesraviNo ratings yet

- Time Value of Money Concepts ExplainedDocument22 pagesTime Value of Money Concepts ExplainedmedrekNo ratings yet

- Chapter 5: How To Value Bonds and StocksDocument16 pagesChapter 5: How To Value Bonds and StocksmajorkonigNo ratings yet

- Valuation of SecuritiesDocument53 pagesValuation of SecuritiesGaurav AgarwalNo ratings yet

- Valuation of BondsDocument27 pagesValuation of BondsAbhinav Rajverma100% (1)

- Activity Sheet In: Business FinanceDocument8 pagesActivity Sheet In: Business FinanceCatherine Larce100% (1)

- Pricing Fixed Income SecuritiesDocument3 pagesPricing Fixed Income SecuritiesIrfan Sadique IsmamNo ratings yet

- Valuation of DebenturesDocument28 pagesValuation of DebenturesharmitkNo ratings yet

- Bond ValuationDocument49 pagesBond ValuationMuhammad Saleh AliNo ratings yet

- Investment Analysis & Portfolio Management: Bond Valuation: That Holding Period IsDocument5 pagesInvestment Analysis & Portfolio Management: Bond Valuation: That Holding Period IsNitesh KirarNo ratings yet

- Direction: Buy QTY: 15,000 SHRS Script Name: Microsoft Currrent Makret Price (CMP) : Usd 299.49Document3 pagesDirection: Buy QTY: 15,000 SHRS Script Name: Microsoft Currrent Makret Price (CMP) : Usd 299.49PrakharNo ratings yet

- Cibop29a - Exch & Otc TLCDocument26 pagesCibop29a - Exch & Otc TLCPrakharNo ratings yet

- Long put payoff diagramDocument12 pagesLong put payoff diagramPrakharNo ratings yet

- Cibop 29a Swaps 1Document20 pagesCibop 29a Swaps 1PrakharNo ratings yet

- Forwards: Trade 1Document6 pagesForwards: Trade 1PrakharNo ratings yet

- Cibop29a - Exch TLCDocument14 pagesCibop29a - Exch TLCPrakharNo ratings yet

- Equity Swaps Investmnet Bank Barclays Ny Equity Swap ContractDocument5 pagesEquity Swaps Investmnet Bank Barclays Ny Equity Swap ContractPrakharNo ratings yet

- Forward Contracts Example: Case 1Document8 pagesForward Contracts Example: Case 1PrakharNo ratings yet

- Long Call Examples: Case - 1Document36 pagesLong Call Examples: Case - 1PrakharNo ratings yet

- DIPLOMA IN BANKING & FINANCE Rules 2020Document3 pagesDIPLOMA IN BANKING & FINANCE Rules 2020PrakharNo ratings yet

- Futures ClearingDocument1 pageFutures ClearingPrakharNo ratings yet

- Equity Swap ExamplesDocument50 pagesEquity Swap ExamplesPrakharNo ratings yet

- Cibop29a - Exch & Otc TLCDocument26 pagesCibop29a - Exch & Otc TLCPrakharNo ratings yet

- Diploma in Banking & Finance: Rules&Syllabus2020Document11 pagesDiploma in Banking & Finance: Rules&Syllabus2020PrakharNo ratings yet

- DBF General GuidelinesDocument1 pageDBF General GuidelinesPrakharNo ratings yet

- Accounting & FinanceDocument73 pagesAccounting & FinancePrakharNo ratings yet

- C D S L Excel FormatDocument34 pagesC D S L Excel FormatPrakharNo ratings yet

- Unit 2 - Calculation of Yield To Maturity (YTM)Document7 pagesUnit 2 - Calculation of Yield To Maturity (YTM)PrakharNo ratings yet

- Accounting & FinanceDocument73 pagesAccounting & FinancePrakharNo ratings yet

- C D S L Excel FormatDocument34 pagesC D S L Excel FormatPrakharNo ratings yet

- My CA Articleship Experience of Working at Deloitte (Big 4)Document5 pagesMy CA Articleship Experience of Working at Deloitte (Big 4)Rudrin Das100% (1)

- Kelompok 2 Schedule InvestasiDocument12 pagesKelompok 2 Schedule InvestasiRima WahyuNo ratings yet

- Tariff Order 2010-11Document187 pagesTariff Order 2010-11Nannapaneni P. ChowdaryNo ratings yet

- Qingdao Thundsea Marine Technology Proforma InvoiceDocument1 pageQingdao Thundsea Marine Technology Proforma InvoiceLiu AllieNo ratings yet

- A Project On Camparative Study Between Private Sector and Public Sector BanksDocument75 pagesA Project On Camparative Study Between Private Sector and Public Sector Banksthaheerhauf1234No ratings yet

- How to Generate Outsized Returns Using the Poor Man's Covered Call StrategyDocument4 pagesHow to Generate Outsized Returns Using the Poor Man's Covered Call Strategyblackmoon47100% (1)

- Kendriya Vidyalaya No.1 Kunjaban, Agartala Tripura: Submitted By: Aboya DebbarmaDocument12 pagesKendriya Vidyalaya No.1 Kunjaban, Agartala Tripura: Submitted By: Aboya Debbarmaakash debbarmaNo ratings yet

- Underwriting SOPDocument5 pagesUnderwriting SOPChris JacksonNo ratings yet

- Financial StatementsDocument2 pagesFinancial StatementsRjoshua PlaylistNo ratings yet

- Dev't Planning - I Chap OneDocument20 pagesDev't Planning - I Chap Oneferewe tesfayeNo ratings yet

- Qurr-03/2024: Föföl FüfälDocument7 pagesQurr-03/2024: Föföl Füfälsandeep kumarNo ratings yet

- Solution Manual Advanced Financial Accounting 8th Edition Baker Chap020 PDFDocument26 pagesSolution Manual Advanced Financial Accounting 8th Edition Baker Chap020 PDFYopie ChandraNo ratings yet

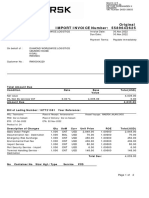

- Original IMPORT INVOICE Number: 5589642625: Total Amount Due Condition Rate Base Value Total (USD)Document2 pagesOriginal IMPORT INVOICE Number: 5589642625: Total Amount Due Condition Rate Base Value Total (USD)AllyNo ratings yet

- Accountancy & Auditing-I Subjective - 1Document4 pagesAccountancy & Auditing-I Subjective - 1zaman virkNo ratings yet

- Financial Education and Invesemtn Awareness Question BankDocument19 pagesFinancial Education and Invesemtn Awareness Question BankSyedNo ratings yet

- A Project Report For: Stitching & Embroidery Work UnitDocument20 pagesA Project Report For: Stitching & Embroidery Work UnitRahul Agrawal100% (1)

- Corporate Finace 1 PDFDocument4 pagesCorporate Finace 1 PDFwafflesNo ratings yet

- Exercise - Dilutive Securities - AdillaikhsaniDocument4 pagesExercise - Dilutive Securities - Adillaikhsaniaidil fikri ikhsan100% (1)

- Mchapter Two Accounting Cycle For Service Giving Business Nature of An AccountDocument12 pagesMchapter Two Accounting Cycle For Service Giving Business Nature of An AccountTIZITAW MASRESHANo ratings yet

- Quiz Number One Without AnswerDocument8 pagesQuiz Number One Without AnswerKpop updates 24/7No ratings yet

- NH Retirement System Pensions 2018Document1,510 pagesNH Retirement System Pensions 2018portsmouthherald33% (3)

- Mathematics of Finance: Faculty of Business Studies (FBS) Bangladesh University of Professionals (BUP)Document52 pagesMathematics of Finance: Faculty of Business Studies (FBS) Bangladesh University of Professionals (BUP)Sadia Afrin ArinNo ratings yet

- Banking DWH Model E-BookDocument37 pagesBanking DWH Model E-BookShekharNo ratings yet

- Cir Vs DlsuDocument2 pagesCir Vs DlsuNLainie Omar50% (2)

- 2014 15 PDFDocument117 pages2014 15 PDFAvichal BhaniramkaNo ratings yet