100% found this document useful (1 vote)

161 views21 pagesVariance Analysis for Marketing Performance

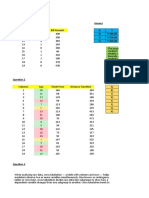

This document discusses variance analysis, which compares actual performance to expected performance. It defines key variances like volume, contribution, and fixed cost variances. Volume variances measure differences in market size and market share from expectations. Contribution variances measure differences in price and unit costs. Fixed cost variances measure differences in expenses like marketing and overhead costs. The purpose is to identify reasons for performance gaps so managers can address factors within their control, like costs. This leads to process improvements. An example variance analysis spreadsheet is provided to illustrate the approach.

Uploaded by

Andy OcegueraCopyright

© © All Rights Reserved

We take content rights seriously. If you suspect this is your content, claim it here.

Available Formats

Download as XLS, PDF, TXT or read online on Scribd

100% found this document useful (1 vote)

161 views21 pagesVariance Analysis for Marketing Performance

This document discusses variance analysis, which compares actual performance to expected performance. It defines key variances like volume, contribution, and fixed cost variances. Volume variances measure differences in market size and market share from expectations. Contribution variances measure differences in price and unit costs. Fixed cost variances measure differences in expenses like marketing and overhead costs. The purpose is to identify reasons for performance gaps so managers can address factors within their control, like costs. This leads to process improvements. An example variance analysis spreadsheet is provided to illustrate the approach.

Uploaded by

Andy OcegueraCopyright

© © All Rights Reserved

We take content rights seriously. If you suspect this is your content, claim it here.

Available Formats

Download as XLS, PDF, TXT or read online on Scribd