You might also like

- Review of Some Online Banks and Visa/Master Cards IssuersFrom EverandReview of Some Online Banks and Visa/Master Cards IssuersNo ratings yet

- Special Features and Advantages of Online BankingDocument5 pagesSpecial Features and Advantages of Online Bankingjay kawathiaNo ratings yet

- Anking Ervices: Presented By: Narayan GaonkarDocument22 pagesAnking Ervices: Presented By: Narayan Gaonkargirish kulkarniNo ratings yet

- E-banking and transaction conceptsDocument17 pagesE-banking and transaction conceptssumedh narwadeNo ratings yet

- Computer Application in Business - III Unit 4Document11 pagesComputer Application in Business - III Unit 4maanu124No ratings yet

- Ecom 3Document20 pagesEcom 3bholaNo ratings yet

- Introduction of E BankingDocument31 pagesIntroduction of E BankingMehul ChauhanNo ratings yet

- E-Banking or Online BankingDocument35 pagesE-Banking or Online BankingMohan kumar K.SNo ratings yet

- Project ReportDocument14 pagesProject ReportKritika PanwarNo ratings yet

- National Law Institute University, Bhopal: Basics of E-BankingDocument21 pagesNational Law Institute University, Bhopal: Basics of E-BankingDikshaNo ratings yet

- CA Project On Internet BankingDocument18 pagesCA Project On Internet BankingTejal KirpekarNo ratings yet

- 3RD SemDocument34 pages3RD SemMohan kumar K.SNo ratings yet

- NET BANKINGDocument3 pagesNET BANKINGparktianeNo ratings yet

- Online Banking (Or Internet Banking) Allows Customers To Conduct Financial Transactions OnDocument9 pagesOnline Banking (Or Internet Banking) Allows Customers To Conduct Financial Transactions OnJamshed AlamNo ratings yet

- Online Banking (Or Internet Banking) Allows Customers To Conduct Financial Transactions OnDocument4 pagesOnline Banking (Or Internet Banking) Allows Customers To Conduct Financial Transactions OnJamshed AlamNo ratings yet

- Internet BankingDocument3 pagesInternet BankingIshita DasNo ratings yet

- Essential Guide to E-BankingDocument64 pagesEssential Guide to E-BankingRkenterpriseNo ratings yet

- E-Banking Opportunities and GuidelinesDocument14 pagesE-Banking Opportunities and GuidelinesAnonymous 22GBLsme1No ratings yet

- DSB PodcastDocument4 pagesDSB Podcastswathi kiran kumar DODDINo ratings yet

- Recent in BankingDocument25 pagesRecent in BankingSrividya SNo ratings yet

- E Banking e PaymentsDocument7 pagesE Banking e Paymentsgarima424582638No ratings yet

- Banking Services GuideDocument28 pagesBanking Services GuideHarmandeep SinghNo ratings yet

- Internet banking in India: services, security and advantagesDocument6 pagesInternet banking in India: services, security and advantagesRohan Freako RawalNo ratings yet

- Internet Banking in PakistanDocument9 pagesInternet Banking in PakistankhalidNo ratings yet

- PPT18Document27 pagesPPT18Dev KumarNo ratings yet

- Internet BankingDocument25 pagesInternet BankingTaranjit Singh vijNo ratings yet

- Online and Mobile Banking Services in 40 CharactersDocument5 pagesOnline and Mobile Banking Services in 40 CharactersFrancisOgosiNo ratings yet

- Electronic Banking SystemDocument4 pagesElectronic Banking SystemshababNo ratings yet

- Internet Banking in India:) Information Only SystemDocument6 pagesInternet Banking in India:) Information Only SystemSwati SharmaNo ratings yet

- E BankingDocument8 pagesE BankingJanani BharathiNo ratings yet

- Internet Banking in India:) Information Only SystemDocument4 pagesInternet Banking in India:) Information Only Systemjagreti17No ratings yet

- Report of Internet BankingDocument40 pagesReport of Internet BankingFILESONICNo ratings yet

- Recent BankingDocument8 pagesRecent BankingRAYSPEARNo ratings yet

- Group 11Document6 pagesGroup 11asma.abdulqadir20No ratings yet

- Article - Advantages of Online BankingDocument2 pagesArticle - Advantages of Online BankingTijana DoberšekNo ratings yet

- Advantages of E-BankingDocument3 pagesAdvantages of E-Bankingbenjie monasqueNo ratings yet

- Project Content CorrectDocument11 pagesProject Content CorrectAthiya KhanNo ratings yet

- ecomm ass1Document9 pagesecomm ass1SimbisoNo ratings yet

- Tele BankingDocument12 pagesTele BankingSakib TalukdarNo ratings yet

- Internet BankingDocument38 pagesInternet Bankingsonalikhande100% (1)

- What Is The Definition of E-BankingDocument2 pagesWhat Is The Definition of E-Bankingdivyangamin100% (1)

- Unit III PDFDocument14 pagesUnit III PDFPrameela KNo ratings yet

- The Indian Internet Banking JourneyDocument4 pagesThe Indian Internet Banking JourneySandeep MishraNo ratings yet

- Essentials of Bank Computerization Payment Systems and Electronic BankingDocument7 pagesEssentials of Bank Computerization Payment Systems and Electronic Bankingvijayadarshini vNo ratings yet

- Assainment of Online BankingDocument21 pagesAssainment of Online BankingMOHAMMAD SAIFUL ISLAM100% (1)

- Electronic BankingDocument5 pagesElectronic Bankingrakibul islam rakibNo ratings yet

- How Technology Is Helping in Increasing Operational Efficiency in Service OrganizationDocument2 pagesHow Technology Is Helping in Increasing Operational Efficiency in Service OrganizationAroon KumarNo ratings yet

- Anywhere Banking: BY, Rony Mathew YohannanDocument14 pagesAnywhere Banking: BY, Rony Mathew YohannanNikhil Thomas AbrahamNo ratings yet

- Bodhi International JournalDocument5 pagesBodhi International JournalZine El Abidine MohamedNo ratings yet

- I-Banking CKTA PersentationDocument5 pagesI-Banking CKTA PersentationHan MyoNo ratings yet

- Banking Customer SatisfactionDocument34 pagesBanking Customer SatisfactionMohan kumar K.SNo ratings yet

- E BankingDocument3 pagesE BankingSumedhaa Srivastava 34 Sem-1,CNo ratings yet

- Unit-I of E-BankingDocument15 pagesUnit-I of E-BankingRoyal JasleenNo ratings yet

- E-Banking: by Gaurav SinghDocument23 pagesE-Banking: by Gaurav SinghDeepak SharmaNo ratings yet

- Introduction To DigitalizationDocument11 pagesIntroduction To Digitalizationdolly guptaNo ratings yet

- Electronic BankingDocument8 pagesElectronic BankingBatch 27No ratings yet

- Nat Hi YaDocument8 pagesNat Hi Yaanon-275306100% (1)

- U U U U U: Online Banking Internet Banking E-Banking Virtual BankingDocument1 pageU U U U U: Online Banking Internet Banking E-Banking Virtual BankingDẽo DẽoNo ratings yet

- E Banking Project... P...Document69 pagesE Banking Project... P...Rohit Patil100% (1)

- Unit 5 Banking LawDocument16 pagesUnit 5 Banking LawRoy Stephen RodriguesNo ratings yet

- Cardcentre ChargesDocument5 pagesCardcentre Chargesw.chathura nuwan ranasingheNo ratings yet

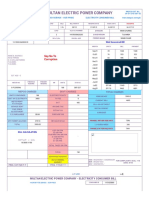

- MEPCO GST No. Electricity BillDocument2 pagesMEPCO GST No. Electricity BillAsad faridNo ratings yet

- SAP Accounts Payable Tables ListDocument3 pagesSAP Accounts Payable Tables ListJames WattsNo ratings yet

- Settlement DetailDocument12 pagesSettlement DetailHamza ELNo ratings yet

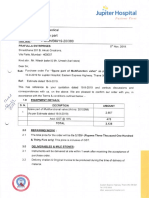

- Jupiter Thane PODocument4 pagesJupiter Thane POAnonymous SXTKyUsNo ratings yet

- EUtvt QPZ 3 C183 A 5 SDocument3 pagesEUtvt QPZ 3 C183 A 5 SSyed100% (1)

- Ebill 12 19 2018Document1 pageEbill 12 19 2018Ace MereriaNo ratings yet

- SITE ANALYSIS OF SINDHI CAMP BUS TERMINUSDocument24 pagesSITE ANALYSIS OF SINDHI CAMP BUS TERMINUSAbhidha JainNo ratings yet

- Statement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocument15 pagesStatement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalancesrisailamsriNo ratings yet

- PUP - Assignment No. 3 - Income Taxation - 2nd Sem AY 2020-2021: RequiredDocument12 pagesPUP - Assignment No. 3 - Income Taxation - 2nd Sem AY 2020-2021: RequiredGabrielle Marie RiveraNo ratings yet

- Summary of Mercantile Law Bar Exam QuestionsDocument5 pagesSummary of Mercantile Law Bar Exam QuestionsRusty NomadNo ratings yet

- AirtelDocument4 pagesAirtelHari Ram KumarNo ratings yet

- Answer To Case 1 - Smith's Market (p.243-244)Document3 pagesAnswer To Case 1 - Smith's Market (p.243-244)Joe CastroNo ratings yet

- Introduction To Taxation-UCTDocument41 pagesIntroduction To Taxation-UCTArvish RamseebaluckNo ratings yet

- Chart of Accounts Example Gray Electronic Repair Services Chart of Accounts ASSETS (1000-1999)Document50 pagesChart of Accounts Example Gray Electronic Repair Services Chart of Accounts ASSETS (1000-1999)Richard Dan Ilao ReyesNo ratings yet

- PSPCL: (Pgbillpay - Aspx) (Pgbillpay - Aspx)Document2 pagesPSPCL: (Pgbillpay - Aspx) (Pgbillpay - Aspx)Surya Prakash100% (1)

- Flow ICM - STDocument7 pagesFlow ICM - STPatrícia Martins Gonçalves CunhaNo ratings yet

- JPIA Review S3 Installment 2 (Business Tax)Document30 pagesJPIA Review S3 Installment 2 (Business Tax)rylNo ratings yet

- Tax Invoice: Service Details: Customer DetailsDocument5 pagesTax Invoice: Service Details: Customer DetailsIT MalurNo ratings yet

- Draft 2019 New Law Transportation Funding Concept Summary Needs & NexusDocument8 pagesDraft 2019 New Law Transportation Funding Concept Summary Needs & NexusThe UrbanistNo ratings yet

- Fraud, Internal Controls and Bank ReconciliationDocument15 pagesFraud, Internal Controls and Bank ReconciliationSadia ShithyNo ratings yet

- IRCTC booking confirmation for train 03244 from GAYA to PATNADocument1 pageIRCTC booking confirmation for train 03244 from GAYA to PATNAfahim siddiquiNo ratings yet

- JNLive - Savings Transaction HistoryDocument1 pageJNLive - Savings Transaction HistoryAndrew HenryNo ratings yet

- Swift 103-202Document2 pagesSwift 103-202Akhmad Zaeny100% (11)

- Canara - Epassbook - 2023-08-07 21:13:55.177708Document13 pagesCanara - Epassbook - 2023-08-07 21:13:55.177708muhammedashfin0No ratings yet

- Online ChallanDocument1 pageOnline ChallanKalpesh DeoraNo ratings yet

- Tax Revenue Regulation Illustrative Problems Compilation iCPA NotesDocument13 pagesTax Revenue Regulation Illustrative Problems Compilation iCPA Notesmendoza.adrianeNo ratings yet

- AWS January 2022 InvoiceDocument3 pagesAWS January 2022 InvoiceDeewan E YaarNo ratings yet

- ACC1701X ACC1002X AY2019 Sem 2 Mock Test Answers PDFDocument8 pagesACC1701X ACC1002X AY2019 Sem 2 Mock Test Answers PDFTenerezzaNo ratings yet

- List of Hotels Near UiTM Pulau Pinang CampusDocument1 pageList of Hotels Near UiTM Pulau Pinang Campusbadai_utmNo ratings yet