You might also like

- Gamma Trade OptionsDocument40 pagesGamma Trade Optionssnowbash50% (2)

- Assignment Questions - Suggested Answers (M13-6, M13-7, E6-3, E6-18, E6-21, E6-24, P6-3, P6-7)Document8 pagesAssignment Questions - Suggested Answers (M13-6, M13-7, E6-3, E6-18, E6-21, E6-24, P6-3, P6-7)Ivy KwokNo ratings yet

- Financial Management: IBA, Main CampusDocument69 pagesFinancial Management: IBA, Main CampusumarNo ratings yet

- 100 BaggersDocument15 pages100 Baggersmilandeep100% (2)

- MULTIPLE CHOICE - Capital BudgetingDocument9 pagesMULTIPLE CHOICE - Capital BudgetingMarcuz AizenNo ratings yet

- Bad Debts Structured 2019 PDFDocument16 pagesBad Debts Structured 2019 PDFArshad ChaudharyNo ratings yet

- Trading The Forex Market: by Vince StanzioneDocument51 pagesTrading The Forex Market: by Vince StanzioneTiavina Rakotomalala43% (7)

- English Grammar BookDocument7 pagesEnglish Grammar BookTiaNắngNgọtNo ratings yet

- Accounts Form 4 - 2021Document51 pagesAccounts Form 4 - 2021gangstar sippas100% (1)

- IGCSE Accounting Year 10 AssessmentDocument9 pagesIGCSE Accounting Year 10 AssessmentVoon Chen WeiNo ratings yet

- ACC1701X Mock Exam 2 SolutionDocument13 pagesACC1701X Mock Exam 2 SolutionShaunny Bravo100% (1)

- AR Practice Problems Solution PDFDocument7 pagesAR Practice Problems Solution PDFLorraine Mae RobridoNo ratings yet

- Financial Statements Analysis: Prof. Dr. Bernd Grottel Certified Public Accountant & Tax AdvisorDocument181 pagesFinancial Statements Analysis: Prof. Dr. Bernd Grottel Certified Public Accountant & Tax Advisornhat quang100% (1)

- Financial Accounting in An Economic Context 8Th Edition Pratt Solutions Manual Full Chapter PDFDocument48 pagesFinancial Accounting in An Economic Context 8Th Edition Pratt Solutions Manual Full Chapter PDFthomasowens1asz100% (9)

- Solution Manual For Financial Accounting in An Economic Context Pratt 9th EditionDocument26 pagesSolution Manual For Financial Accounting in An Economic Context Pratt 9th EditionArielCooperbzqsp100% (82)

- Last Final-Enter Openning Balance SQ3Document9 pagesLast Final-Enter Openning Balance SQ3BUNKHY LEMNo ratings yet

- Chapter 8: Self - Study 5 SolutionsDocument4 pagesChapter 8: Self - Study 5 SolutionssqhaaNo ratings yet

- 2021 Accounting Examination PaperDocument38 pages2021 Accounting Examination Paperzacrasheed2No ratings yet

- Error Question 4Document3 pagesError Question 4Rimmy's BrainNo ratings yet

- Wa0040.Document12 pagesWa0040.ibbbi shkhNo ratings yet

- Chapter 7 SolutionsDocument12 pagesChapter 7 SolutionsDrm BluNo ratings yet

- CT 2 BRS & Control Accounts 1Document6 pagesCT 2 BRS & Control Accounts 1sangeeta.jumaniNo ratings yet

- Abt - 3Document3 pagesAbt - 3dhruvNo ratings yet

- IG June 25 Paper 1Document18 pagesIG June 25 Paper 1May Myat Noe KyawNo ratings yet

- Cambridge O Level: ACCOUNTING 7707/21Document20 pagesCambridge O Level: ACCOUNTING 7707/21Fred SaneNo ratings yet

- ACCT 3110 CH 7 Homework E 4 8 13 19 20 27Document7 pagesACCT 3110 CH 7 Homework E 4 8 13 19 20 27John Job100% (1)

- Practice BookDocument20 pagesPractice Booktamim haqueNo ratings yet

- Cambridge IGCSE: ACCOUNTING 0452/22Document20 pagesCambridge IGCSE: ACCOUNTING 0452/22Lavanya GoleNo ratings yet

- The Adjusted Trial Balance of ZHILIK COMPANY Appears BelowDocument1 pageThe Adjusted Trial Balance of ZHILIK COMPANY Appears BelowJahid RahmanNo ratings yet

- Midterm Test - Code 37 - FA - Sem 2 - 21.22Document5 pagesMidterm Test - Code 37 - FA - Sem 2 - 21.22Đoàn Tài ĐứcNo ratings yet

- Busi 3111 Group - hw1Document3 pagesBusi 3111 Group - hw1Hakkı Anıl AksoyNo ratings yet

- Cambridge O Level: ACCOUNTING 7707/22Document16 pagesCambridge O Level: ACCOUNTING 7707/22Syeda Malika AnjumNo ratings yet

- Financial Accounting Information For Decisions 7Th Edition Wild Solutions Manual Full Chapter PDFDocument61 pagesFinancial Accounting Information For Decisions 7Th Edition Wild Solutions Manual Full Chapter PDFthomasowens1asz100% (10)

- Error Question 3Document4 pagesError Question 3Rimmy's BrainNo ratings yet

- CHAPTER 6 - PPTDocument42 pagesCHAPTER 6 - PPTmeahangela.labadan.23No ratings yet

- Cash Budgeting Notes and QuestionsDocument39 pagesCash Budgeting Notes and Questions邹尧No ratings yet

- Cambridge IGCSE: ACCOUNTING 0452/21Document24 pagesCambridge IGCSE: ACCOUNTING 0452/21Tamer AhmedNo ratings yet

- Financial Statements and Accounting Concepts/Principles: Category Financial Statement(s)Document7 pagesFinancial Statements and Accounting Concepts/Principles: Category Financial Statement(s)cialeeNo ratings yet

- Financial Accounting Fundamentals 5th Edition Wild Solutions ManualDocument39 pagesFinancial Accounting Fundamentals 5th Edition Wild Solutions Manualruchingmezcalwzf2p100% (14)

- Ffa Exam PackDocument36 pagesFfa Exam Packqas4476pubNo ratings yet

- Financial Accounting 9Th Edition Harrison Solutions Manual Full Chapter PDFDocument36 pagesFinancial Accounting 9Th Edition Harrison Solutions Manual Full Chapter PDFphyllis.horan125100% (10)

- Chapter 17 AnswersDocument5 pagesChapter 17 AnswersJennifer Cooper100% (1)

- BHMH2101 Financial Accounting Reinforcement Exercise - Chapter 7 (2) Part ADocument3 pagesBHMH2101 Financial Accounting Reinforcement Exercise - Chapter 7 (2) Part APy CNo ratings yet

- Accounting Process With AnsDocument6 pagesAccounting Process With AnsMichael BongalontaNo ratings yet

- Current Liabilities and Payroll Accounting: QuestionsDocument56 pagesCurrent Liabilities and Payroll Accounting: QuestionsChu Thị Thủy100% (1)

- June 2021 Question Paper 21Document24 pagesJune 2021 Question Paper 21Md Al bdNo ratings yet

- Quarter 2 Module 8Document13 pagesQuarter 2 Module 8Domenah Anarfi EmmanuelNo ratings yet

- TUGAS DASAR AKUNTANSI 4 - Samuel S Purba - 141200193Document24 pagesTUGAS DASAR AKUNTANSI 4 - Samuel S Purba - 141200193Samuel PurbaNo ratings yet

- CH 10 - End of Chapter Exercises SolutionsDocument57 pagesCH 10 - End of Chapter Exercises SolutionssaraNo ratings yet

- Solution Ch04Document146 pagesSolution Ch04Harmanjot 03No ratings yet

- Chapter 9 Solutions PDFDocument7 pagesChapter 9 Solutions PDFAA BB MMNo ratings yet

- Financial Accounting For Decision Making (FADM) : ISB 2020-21 Additional Problems For Sessions 1-5Document32 pagesFinancial Accounting For Decision Making (FADM) : ISB 2020-21 Additional Problems For Sessions 1-5Anyone SomeoneNo ratings yet

- Irfan Gaffar Adnan's Financial Leverage CalculationsDocument5 pagesIrfan Gaffar Adnan's Financial Leverage CalculationsirfanNo ratings yet

- Practice Statement of Cash FlowsDocument3 pagesPractice Statement of Cash FlowsSid NairNo ratings yet

- Chapter 7 BE EX SolutionsDocument30 pagesChapter 7 BE EX SolutionsThu Ngan NguyenNo ratings yet

- Ch10 ExercisesDocument15 pagesCh10 Exercisesjamiahamdard001No ratings yet

- Chapter 7Document11 pagesChapter 7Justin ManaogNo ratings yet

- Mock Exam 2Document9 pagesMock Exam 2Katinaa PrasannaaNo ratings yet

- Intermediate Accounting Volume 1 Canadian 7Th Edition Beechy Solutions Manual Full Chapter PDFDocument67 pagesIntermediate Accounting Volume 1 Canadian 7Th Edition Beechy Solutions Manual Full Chapter PDFDianeWhiteicyf100% (8)

- Cu 7en L¿?o Ne: Ti? P Yauc UyteDocument5 pagesCu 7en L¿?o Ne: Ti? P Yauc UyteIan BurnieNo ratings yet

- Correction of errors journal entriesDocument54 pagesCorrection of errors journal entriesSameerNo ratings yet

- Week 15 Class Activity POA 22022023 035925pmDocument2 pagesWeek 15 Class Activity POA 22022023 035925pmMinahil KhanNo ratings yet

- Delta congregation accounts sheetDocument2 pagesDelta congregation accounts sheetMichael WestNo ratings yet

- Worksheet 4.1 Introducing Bank ReconciliationDocument4 pagesWorksheet 4.1 Introducing Bank ReconciliationHan Nwe Oo100% (1)

- Akuntansi DCBA - TK1-W3-S4-R2 - TEAM7Document5 pagesAkuntansi DCBA - TK1-W3-S4-R2 - TEAM7davina elvinaNo ratings yet

- CC BalanceDocument4 pagesCC BalanceNovena TrimuktiNo ratings yet

- Economic & Budget Forecast Workbook: Economic workbook with worksheetFrom EverandEconomic & Budget Forecast Workbook: Economic workbook with worksheetNo ratings yet

- The Boston Institute of Finance Mutual Fund Advisor Course: Series 6 and Series 63 Test PrepFrom EverandThe Boston Institute of Finance Mutual Fund Advisor Course: Series 6 and Series 63 Test PrepNo ratings yet

- 20210301152331information On Publication During CandidatureDocument5 pages20210301152331information On Publication During CandidatureVoon Chen WeiNo ratings yet

- iGCSE Chemistry Section 4 Lesson 2.1Document79 pagesiGCSE Chemistry Section 4 Lesson 2.1Voon Chen WeiNo ratings yet

- Seafood PRICE LIST Dec 2021 Updated VersionDocument17 pagesSeafood PRICE LIST Dec 2021 Updated VersionVoon Chen WeiNo ratings yet

- Cambridge International Examinations: Chemistry 5070/21 May/June 2017Document11 pagesCambridge International Examinations: Chemistry 5070/21 May/June 2017Voon Chen WeiNo ratings yet

- University of Cambridge International Examinations International General Certificate of Secondary EducationDocument20 pagesUniversity of Cambridge International Examinations International General Certificate of Secondary EducationVoon Chen WeiNo ratings yet

- Whitepaper PDFDocument8 pagesWhitepaper PDFDEVESH BHOLENo ratings yet

- 2018 Specimen Paper Mark Scheme 6Document4 pages2018 Specimen Paper Mark Scheme 6Voon Chen WeiNo ratings yet

- BOOK LIST 2021-2022 - YEAR 6: Straits International SchoolDocument2 pagesBOOK LIST 2021-2022 - YEAR 6: Straits International SchoolVoon Chen WeiNo ratings yet

- Tan Sri Azman Hashim (Profile)Document1 pageTan Sri Azman Hashim (Profile)Voon Chen WeiNo ratings yet

- IGCSE 2016 Specimen Paper 6Document12 pagesIGCSE 2016 Specimen Paper 6ashathtNo ratings yet

- Igcse Yr 10 Paper 2 Nov 2020 AssessmentDocument9 pagesIgcse Yr 10 Paper 2 Nov 2020 AssessmentVoon Chen WeiNo ratings yet

- (A) Define (I) Electric Field.: Physics Paper 2 Sf026/2 PSPM Semester 2 Session 2015/2016 1Document13 pages(A) Define (I) Electric Field.: Physics Paper 2 Sf026/2 PSPM Semester 2 Session 2015/2016 1Voon Chen WeiNo ratings yet

- Cambridge IGCSE™: Accounting 0452/22 October/November 2020Document14 pagesCambridge IGCSE™: Accounting 0452/22 October/November 2020Voon Chen WeiNo ratings yet

- Physics Paper 2 Sf026/2 PSPM Semester 2 Session 2016/2017Document13 pagesPhysics Paper 2 Sf026/2 PSPM Semester 2 Session 2016/2017Voon Chen WeiNo ratings yet

- Immune System NewDocument36 pagesImmune System NewMaic Audolin SihombingNo ratings yet

- IGCSE Chemistry Section 4 Lesson 1Document66 pagesIGCSE Chemistry Section 4 Lesson 1Voon Chen WeiNo ratings yet

- P1 Chapter 11 :: Vectors - An IntroductionDocument29 pagesP1 Chapter 11 :: Vectors - An IntroductiondnaielNo ratings yet

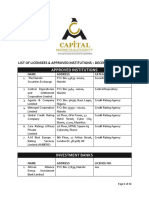

- List of Licensees As at December 29 2021Document13 pagesList of Licensees As at December 29 2021Annette NgangaNo ratings yet

- Chapter 7—International Arbitrage and Interest Rate ParityDocument11 pagesChapter 7—International Arbitrage and Interest Rate ParityRim RimNo ratings yet

- UGB253 Management Accounting Business FinalDocument15 pagesUGB253 Management Accounting Business FinalMohamed AzmalNo ratings yet

- Chapter 6 Managing Your Money: Personal Finance, 6e (Madura)Document22 pagesChapter 6 Managing Your Money: Personal Finance, 6e (Madura)Huỳnh Lữ Thị NhưNo ratings yet

- Portfolio Report PDFDocument7 pagesPortfolio Report PDFAnonymous kjeBVVlobNo ratings yet

- Cases&Exercises - Chapter 4Document3 pagesCases&Exercises - Chapter 4Barbara AraujoNo ratings yet

- Ninepoint Alternative Income: Product ComparisonDocument3 pagesNinepoint Alternative Income: Product ComparisonleminhptnkNo ratings yet

- Rapport de MadioDocument88 pagesRapport de Madioroni jeufoNo ratings yet

- Assignment - 8-Contemporary Engineering EconomicsDocument3 pagesAssignment - 8-Contemporary Engineering EconomicsDhiraj NayakNo ratings yet

- GTU Syllabus for Financial Derivatives (FDDocument5 pagesGTU Syllabus for Financial Derivatives (FDSagar ModiNo ratings yet

- Analyze Financial Performance with Ratio AnalysisDocument4 pagesAnalyze Financial Performance with Ratio AnalysisKartikeyaDwivediNo ratings yet

- Unit IDocument5 pagesUnit ISatya KumarNo ratings yet

- Day 7 Profit & Loss 02 (Foundation Batch)Document2 pagesDay 7 Profit & Loss 02 (Foundation Batch)Deepak ShahNo ratings yet

- Vertex Free PlaybookDocument10 pagesVertex Free PlaybookThero RaseasalaNo ratings yet

- Times: ApproachDocument312 pagesTimes: ApproachNishit VermaNo ratings yet

- 2.3inventory - Cost Flow MethodsDocument12 pages2.3inventory - Cost Flow Methodsnermeen alaaeldeinMNo ratings yet

- CM Comprehensive AssignmentDocument2 pagesCM Comprehensive AssignmentShivamNo ratings yet

- PT Gudang Buku Balance SheetDocument1 pagePT Gudang Buku Balance Sheetlisna hikmahdianiNo ratings yet

- ROAD TO BASEL III - An International Banking Event - EgyptDocument4 pagesROAD TO BASEL III - An International Banking Event - Egyptديفولوبرز للإستشارات والتدريبNo ratings yet

- Stock Statement by BorrowerDocument4 pagesStock Statement by BorrowerDiksha GangwaniNo ratings yet

- Potential Risks For McDonaldDocument1 pagePotential Risks For McDonaldDianne CantiverosNo ratings yet

- Managerial Accounting 9Th Edition Crosson Test Bank Full Chapter PDFDocument67 pagesManagerial Accounting 9Th Edition Crosson Test Bank Full Chapter PDFKimberlyLinesrb100% (11)

- Group 7 - Homework Chapter 2 - Project SelectionDocument10 pagesGroup 7 - Homework Chapter 2 - Project SelectionThuỷ VươngNo ratings yet

- Cash Flow Analysis: ReviewDocument50 pagesCash Flow Analysis: ReviewDiich Tiari RachmadaniNo ratings yet