You might also like

- 156Document2 pages156Swapnil MahantaNo ratings yet

- Assignmnet 5.5Document2 pagesAssignmnet 5.5chrislupinjrNo ratings yet

- AA RevisionDocument20 pagesAA RevisionBhone ThantNo ratings yet

- SD20 MJ19Document4 pagesSD20 MJ19Bhone ThantNo ratings yet

- Q 213 Venus PDFDocument2 pagesQ 213 Venus PDFboke layNo ratings yet

- Audit Risks and ResponsesDocument5 pagesAudit Risks and ResponsesAvinash AcharyaNo ratings yet

- Audit HURLING CO (B)Document5 pagesAudit HURLING CO (B)GOH SZE MENG JOYCELYNE100% (1)

- Audit Risk Auditor'S ResponseDocument7 pagesAudit Risk Auditor'S ResponsePink GirlNo ratings yet

- 202Document2 pages202MR.diwash PokhrelNo ratings yet

- 154Document1 page154Swapnil MahantaNo ratings yet

- HurlingDocument6 pagesHurlingMansoor SharifNo ratings yet

- Planning and Risk AssessmentDocument19 pagesPlanning and Risk AssessmentMeta ShresthaNo ratings yet

- Sitia Sparkle Co Purchases Its Raw Material From Africa Which Remains in Transit For Three WeeksDocument2 pagesSitia Sparkle Co Purchases Its Raw Material From Africa Which Remains in Transit For Three WeeksTashfeenNo ratings yet

- AA - Revision: Dec 2011 Q3 - Lincoln CoDocument4 pagesAA - Revision: Dec 2011 Q3 - Lincoln CoTapiwa K NgungunyaniNo ratings yet

- Audit Risk NotesDocument8 pagesAudit Risk NotesAditya KanabarNo ratings yet

- 152Document1 page152Swapnil MahantaNo ratings yet

- Assignment 4Document6 pagesAssignment 4chrislupinjrNo ratings yet

- Audit risks and responses for Sleeptight and RecorderDocument3 pagesAudit risks and responses for Sleeptight and RecorderTashfeenNo ratings yet

- Sep Dec20218Document3 pagesSep Dec20218AliNo ratings yet

- F8 (AA) Kit - Que 82 - Blackberry CoDocument3 pagesF8 (AA) Kit - Que 82 - Blackberry CoChrisNo ratings yet

- ACCA F8 -AUDIT RISK by Alan Biju Palak ACCADocument5 pagesACCA F8 -AUDIT RISK by Alan Biju Palak ACCAkasimranjhaNo ratings yet

- Drafting Type 1 Answers On EvidenceDocument12 pagesDrafting Type 1 Answers On EvidenceAzhar RahamathullaNo ratings yet

- Stephen f8 Question and AnswerDocument8 pagesStephen f8 Question and AnswerStephen FrancisNo ratings yet

- Audit ReportDocument5 pagesAudit ReportAmir ArifNo ratings yet

- Audit Risk NotesDocument14 pagesAudit Risk NotesRana NadeemNo ratings yet

- Audit Risk 1Document2 pagesAudit Risk 1Sanjay PradhanNo ratings yet

- Substantive Procedures - Anuj Manoj Kumar - 23-01-2022Document9 pagesSubstantive Procedures - Anuj Manoj Kumar - 23-01-2022Lishika PasariNo ratings yet

- Audit, Assurance and Related Services: Page 1 of 10Document10 pagesAudit, Assurance and Related Services: Page 1 of 10ANo ratings yet

- Account Reconciliations - Corporate Guidelines - FinalDocument7 pagesAccount Reconciliations - Corporate Guidelines - FinalEunice WongNo ratings yet

- Compliance Checklist - PlantDocument36 pagesCompliance Checklist - Plantsaji kumarNo ratings yet

- Hart CoDocument4 pagesHart CoSITI SARAH JAUHARINo ratings yet

- Audit risk response - conciseDocument8 pagesAudit risk response - conciseAtka FahimNo ratings yet

- UCSB Campus Information & Procedure Manual Reviewing & Reconciling TheDocument6 pagesUCSB Campus Information & Procedure Manual Reviewing & Reconciling Themansoor2685No ratings yet

- AAA Question PracticeDocument8 pagesAAA Question PracticenishantsayshiNo ratings yet

- Session 3 - Practice Exercise 1 - Check Co - Audit Risks Respones - Question AnsDocument4 pagesSession 3 - Practice Exercise 1 - Check Co - Audit Risks Respones - Question AnsKim NgânNo ratings yet

- M.Fahad 18U00151 Sec E Assignment 1 AuditingDocument2 pagesM.Fahad 18U00151 Sec E Assignment 1 Auditingmuhammad fahadNo ratings yet

- Audit tt6Document11 pagesAudit tt6CHYE CHING OOINo ratings yet

- Francis GroupDocument2 pagesFrancis GroupAjith GeorgeNo ratings yet

- Overall F/S Level (OFSL) Risk (What & Why? 3x) : Note 1 Note 2Document4 pagesOverall F/S Level (OFSL) Risk (What & Why? 3x) : Note 1 Note 24ever.loveNo ratings yet

- Hart Co Audit Risk Auditors ResponseDocument4 pagesHart Co Audit Risk Auditors Responsenajihah zakariaNo ratings yet

- Audit Risk CompilationDocument25 pagesAudit Risk Compilation5mh8cyfgt4No ratings yet

- Questions: Liabilities, and Equity. These ElementsDocument38 pagesQuestions: Liabilities, and Equity. These ElementssiaaswanNo ratings yet

- Johnson Medical Case - CPA Core 1Document5 pagesJohnson Medical Case - CPA Core 1bushrasaleem5699No ratings yet

- Audit Substantive Procedures f8 CompressDocument39 pagesAudit Substantive Procedures f8 CompressApoorv jainNo ratings yet

- FabmDocument68 pagesFabmAllyzza Jayne Abelido100% (1)

- Important Question For Substantive ProceduresDocument4 pagesImportant Question For Substantive ProceduresMansoor SharifNo ratings yet

- Risk and ResponsesDocument10 pagesRisk and ResponsesAbdullahNo ratings yet

- Substantive Procedures SheetDocument28 pagesSubstantive Procedures SheetMohanrajNo ratings yet

- Verification of Assets and LiabilitiesDocument62 pagesVerification of Assets and Liabilitiesanon_672065362No ratings yet

- AARS Test 4 Solution FinalDocument7 pagesAARS Test 4 Solution FinalShahzaib VirkNo ratings yet

- Chap-6-Verification of Assets and LiabilitiesDocument48 pagesChap-6-Verification of Assets and LiabilitiesAkash GuptaNo ratings yet

- Revenue Recognition, Deferred Income Risks for Island Co AuditDocument6 pagesRevenue Recognition, Deferred Income Risks for Island Co AuditNiharika LuthraNo ratings yet

- CAF 08 Test 7 - Suggested SolutionDocument3 pagesCAF 08 Test 7 - Suggested SolutionUsama TariqNo ratings yet

- Suggested Solutions To Chapter 6 Discussion QuestionsDocument8 pagesSuggested Solutions To Chapter 6 Discussion QuestionsGajan SelvaNo ratings yet

- Audit RevisionDocument53 pagesAudit Revisionmalachibroomes1No ratings yet

- Extracted Chapter 1Document103 pagesExtracted Chapter 1PalisthaNo ratings yet

- Q - 204 - Peony CompnayDocument4 pagesQ - 204 - Peony CompnayhusseinNo ratings yet

- Auditing Theories and Problems Quiz WEEK 2Document16 pagesAuditing Theories and Problems Quiz WEEK 2Van MateoNo ratings yet

- Tackling Multiple Choice Case QuestionsDocument1 pageTackling Multiple Choice Case QuestionsTashfeenNo ratings yet

- Discussions in Section B QuestionsDocument1 pageDiscussions in Section B QuestionsTashfeenNo ratings yet

- Making The Most of Question Practice: 2017 For Detailed Coverage of The Topics Covered in QuestionsDocument1 pageMaking The Most of Question Practice: 2017 For Detailed Coverage of The Topics Covered in QuestionsTashfeenNo ratings yet

- MJ16 Hybrid F8 QP Clean ProofDocument5 pagesMJ16 Hybrid F8 QP Clean ProofjoelvalentinorNo ratings yet

- Sitia Sparkle Co Purchases Its Raw Material From Africa Which Remains in Transit For Three WeeksDocument2 pagesSitia Sparkle Co Purchases Its Raw Material From Africa Which Remains in Transit For Three WeeksTashfeenNo ratings yet

- F8 Revision Notes Table of ContentsDocument169 pagesF8 Revision Notes Table of ContentsArbab JhangirNo ratings yet

- Assertion For InventoryDocument1 pageAssertion For InventoryTashfeenNo ratings yet

- The Sales Staff Have Monthly Sales Targets and Are Able To Use Their Discretion in Granting Sales Discounts Up To A Maximum of 10Document2 pagesThe Sales Staff Have Monthly Sales Targets and Are Able To Use Their Discretion in Granting Sales Discounts Up To A Maximum of 10TashfeenNo ratings yet

- F8uk 2011 Dec A PDFDocument14 pagesF8uk 2011 Dec A PDFNaleeNo ratings yet

- Inventory Valuation:: Revaluation of Property, Plant and Equipment (PPE)Document2 pagesInventory Valuation:: Revaluation of Property, Plant and Equipment (PPE)TashfeenNo ratings yet

- Audit and Assurance Exam QuestionsDocument5 pagesAudit and Assurance Exam QuestionsIan Bob WilliamsNo ratings yet

- Business Mathematics - Model PaperDocument4 pagesBusiness Mathematics - Model PaperTashfeenNo ratings yet

- F8uk 2011 Dec A PDFDocument14 pagesF8uk 2011 Dec A PDFNaleeNo ratings yet

- LixingcunDocument7 pagesLixingcunTashfeenNo ratings yet

- Question f8 Audit RiskDocument4 pagesQuestion f8 Audit RiskTashfeenNo ratings yet

- Sept / Dec 15 Q1Document5 pagesSept / Dec 15 Q1TashfeenNo ratings yet

- Tags 1-50Document2 pagesTags 1-50TashfeenNo ratings yet

- 0 - KPBTE Exam Admission FormDocument2 pages0 - KPBTE Exam Admission FormTashfeenNo ratings yet

- Financial AccountingDocument314 pagesFinancial AccountingGunjan MaheshwariNo ratings yet

- Overview of Enterprise Resource Planning (Erp) System in Higher Education Institutions (Heis)Document21 pagesOverview of Enterprise Resource Planning (Erp) System in Higher Education Institutions (Heis)TashfeenNo ratings yet

- Boards of Technical Education Pakistan: Statistics DBA - I (Approved Syllabus For ACCA Students)Document2 pagesBoards of Technical Education Pakistan: Statistics DBA - I (Approved Syllabus For ACCA Students)TashfeenNo ratings yet

- SBTE Dec 2017-Jan 2018 exam dates & proceduresDocument1 pageSBTE Dec 2017-Jan 2018 exam dates & proceduresTashfeenNo ratings yet

- Statistics - Model PaperDocument2 pagesStatistics - Model PaperTashfeenNo ratings yet

- Ab1 PDFDocument192 pagesAb1 PDFTashfeenNo ratings yet

- Boards of Technical Education Pakistan: Statistics DBA - I (Approved Syllabus For ACCA Students)Document2 pagesBoards of Technical Education Pakistan: Statistics DBA - I (Approved Syllabus For ACCA Students)TashfeenNo ratings yet

- Courier - Capstone Round 1Document14 pagesCourier - Capstone Round 1Khanh MaiNo ratings yet

- Group 5 Monetary Central BankingDocument19 pagesGroup 5 Monetary Central BankingAurea Espinosa ErazoNo ratings yet

- International Financial SystemDocument19 pagesInternational Financial Systemnavya782003No ratings yet

- 1 Blockchain Babble FinalDocument3 pages1 Blockchain Babble Finalapi-610726438No ratings yet

- Micro Finance ProjectDocument38 pagesMicro Finance ProjectmanojrengarNo ratings yet

- PlumHQ Aims To Solve India's Missing Middle Puzzle in Digital InsuranceDocument9 pagesPlumHQ Aims To Solve India's Missing Middle Puzzle in Digital InsuranceShatir LaundaNo ratings yet

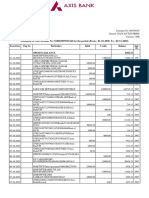

- Statement of Axis Account No:918010099547443 For The Period (From: 01-10-2020 To: 02-11-2020)Document5 pagesStatement of Axis Account No:918010099547443 For The Period (From: 01-10-2020 To: 02-11-2020)minniNo ratings yet

- CARD - Case Analysis SampleDocument51 pagesCARD - Case Analysis SampleCatherine Mae MacailaoNo ratings yet

- Microfinance Paper PresentationDocument8 pagesMicrofinance Paper Presentationtulasinad123No ratings yet

- International Banking Statistics OverviewDocument139 pagesInternational Banking Statistics Overviewbaburavula4756No ratings yet

- Unifi - Invoice Bulan 2020Document25 pagesUnifi - Invoice Bulan 2020Mich SpikeNo ratings yet

- The Elements Directly Related To The Measurement of Financial Position AreDocument8 pagesThe Elements Directly Related To The Measurement of Financial Position AreKim Patrice NavarraNo ratings yet

- GHSHZHXHDocument88 pagesGHSHZHXHbishwajitNo ratings yet

- BMBA Media Presentation July 2012Document4 pagesBMBA Media Presentation July 2012ShakilNo ratings yet

- Jepi 03.23.22Document3 pagesJepi 03.23.22physicallen1791No ratings yet

- Intermediate Accounting 2 Second Grading Examination: Name: Date: Professor: Section: ScoreDocument25 pagesIntermediate Accounting 2 Second Grading Examination: Name: Date: Professor: Section: ScoreNah Hamza100% (1)

- The Role of Financial Markets and Institutions in Supporting The Global Economy During The COVID 19 PandemicDocument60 pagesThe Role of Financial Markets and Institutions in Supporting The Global Economy During The COVID 19 PandemicHanaSuhanaNo ratings yet

- TOPIC 2 NOTES and LOANS PAYABLEDocument4 pagesTOPIC 2 NOTES and LOANS PAYABLEDustinEarth Buyo MontebonNo ratings yet

- Aviva Life Insurance: Aviva Mainly Have Two Major Kind of Products: 1. Aviva Individual Products 2. Aviva Group ProductsDocument33 pagesAviva Life Insurance: Aviva Mainly Have Two Major Kind of Products: 1. Aviva Individual Products 2. Aviva Group ProductsBasavaraja K JNo ratings yet

- A Comparison Between Reporting of Conventional Leasing and Islamic LeasingDocument23 pagesA Comparison Between Reporting of Conventional Leasing and Islamic LeasingNosh HashmiNo ratings yet

- Far Volume 1, 2 and 3 TheoryDocument17 pagesFar Volume 1, 2 and 3 TheoryKimberly Etulle CelonaNo ratings yet

- RBI Grade B 2023 Guide Book Updated SyllabusDocument22 pagesRBI Grade B 2023 Guide Book Updated SyllabusPunith kumarNo ratings yet

- Unique Document Identification NumberDocument3 pagesUnique Document Identification Numberniravtrivedi72No ratings yet

- Macefits Consulting Services CC (Drawing Timetables)Document2 pagesMacefits Consulting Services CC (Drawing Timetables)Hasani Oriel MaphopheNo ratings yet

- Unit 5 Andhra Pradesh.Document18 pagesUnit 5 Andhra Pradesh.Charu ModiNo ratings yet

- Cashflow SheetDocument1 pageCashflow SheetFrank Ferrao100% (6)

- Acctg7 - CH 8Document22 pagesAcctg7 - CH 8Jao FloresNo ratings yet

- Final SK Invitation To SiargaoDocument1 pageFinal SK Invitation To SiargaoMary Joy MagbanuaNo ratings yet

- VG937HD6: M-Pesa StatementDocument47 pagesVG937HD6: M-Pesa Statementeliteprinters2018No ratings yet

- Accounting EquationDocument6 pagesAccounting EquationFayaz MohammedNo ratings yet