You might also like

- Tutorial 7 (Week 9) - Managerial Accounting Concepts and Principles - Cost-Volume-Profit AnalysisDocument7 pagesTutorial 7 (Week 9) - Managerial Accounting Concepts and Principles - Cost-Volume-Profit AnalysisVincent TanNo ratings yet

- EXERCISESDocument32 pagesEXERCISESOlivia Huelamo0% (1)

- Pearl River Valley Flood Control District 2022 BudgetDocument1 pagePearl River Valley Flood Control District 2022 BudgetAnthony WarrenNo ratings yet

- Financial Statement Analysis and Liquidity Ratios QsDocument36 pagesFinancial Statement Analysis and Liquidity Ratios Qsgun attaphanNo ratings yet

- Module 1 - Basics of CostingDocument40 pagesModule 1 - Basics of Costingmaheshbendigeri5945No ratings yet

- Acctg201 IntroductionDocument10 pagesAcctg201 Introductionaaron manacapNo ratings yet

- KMC Constructions Limited: Payslip For November - 2018Document1 pageKMC Constructions Limited: Payslip For November - 2018Srinuvasulu ReddyNo ratings yet

- Cost Accounting Nature of Costs/Cost Volume Profit Analysis IDocument25 pagesCost Accounting Nature of Costs/Cost Volume Profit Analysis IMackenzie Heart Obien0% (1)

- Logistics &SCM - Chap 4,5,7,8Document11 pagesLogistics &SCM - Chap 4,5,7,8srujanakrishna AVULANo ratings yet

- Accounting 2Document5 pagesAccounting 2jessicaong2403No ratings yet

- 3a ACC 15-2-1 Classifying IEXDocument6 pages3a ACC 15-2-1 Classifying IEXSmurtman69 IVNo ratings yet

- Classification of CostDocument1 pageClassification of Costromi naibahoNo ratings yet

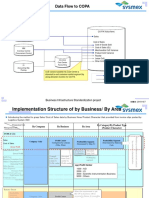

- Data Flow To COPA: Business Infrastructure Standardization ProjectDocument3 pagesData Flow To COPA: Business Infrastructure Standardization ProjectT SAIKIRANNo ratings yet

- Topic 2: Manufacturing Cost Concept and ComponentsDocument7 pagesTopic 2: Manufacturing Cost Concept and ComponentsAnice WongNo ratings yet

- 04-Chap2-Chart of Accounts-2022-2023-S1Document1 page04-Chap2-Chart of Accounts-2022-2023-S1Lilly ChanNo ratings yet

- Cost Concepts and ClassificationDocument8 pagesCost Concepts and ClassificationJericho PagsuguironNo ratings yet

- UntitledDocument16 pagesUntitledMaria Nena LoretoNo ratings yet

- Problems On Profit Prior To IncorporationDocument18 pagesProblems On Profit Prior To Incorporationcsneha0803No ratings yet

- Comparative Analysis of Component of Financial Statement ofDocument20 pagesComparative Analysis of Component of Financial Statement ofRishika GuptaNo ratings yet

- Creation of Different Type of GL AccountDocument6 pagesCreation of Different Type of GL AccountMohammed Nawaz ShariffNo ratings yet

- Assignment 2-Zienab MosabbehDocument3 pagesAssignment 2-Zienab MosabbehZienab MosabbehNo ratings yet

- E&S Business Plan ReportDocument8 pagesE&S Business Plan ReportViknesh VikneshNo ratings yet

- Cost Acc CH 4Document21 pagesCost Acc CH 4DanielNo ratings yet

- Joint Products / by Products: Accounting Decision MakingDocument16 pagesJoint Products / by Products: Accounting Decision MakingKaran KashyapNo ratings yet

- Chart of AccountsDocument1 pageChart of AccountsChips AhoyNo ratings yet

- Cost Terms, Concepts, and ClassificationDocument27 pagesCost Terms, Concepts, and ClassificationParadise VillageNo ratings yet

- Study of Financial Statement Repaired)Document4 pagesStudy of Financial Statement Repaired)sureshprojectsNo ratings yet

- Guia 2 InglesDocument8 pagesGuia 2 InglesaskjdkjasdNo ratings yet

- Chapter 5 Financial ManagementDocument43 pagesChapter 5 Financial ManagementfekaduNo ratings yet

- Mrs.V.Madhu Latha: Assistant Professor Department of Business Management VR Siddhartha Engineering CollegeDocument14 pagesMrs.V.Madhu Latha: Assistant Professor Department of Business Management VR Siddhartha Engineering CollegesushmaNo ratings yet

- Cash From Operations: Cash Flow Statement Notes and DescriptionsDocument2 pagesCash From Operations: Cash Flow Statement Notes and DescriptionsNahom AsamenewNo ratings yet

- Chapter 2 Managerial Accounting and Cost ConceptsDocument49 pagesChapter 2 Managerial Accounting and Cost ConceptsFarihaNo ratings yet

- Chart of AccountDocument1 pageChart of AccountTusshar AhmedNo ratings yet

- Variable Costs: Break-Even Analysis Notes and DescriptionsDocument1 pageVariable Costs: Break-Even Analysis Notes and DescriptionsNahom AsamenewNo ratings yet

- Cost Concepts Classification BehaviorDocument46 pagesCost Concepts Classification BehaviorrhearomefranciscoNo ratings yet

- Managerial Accounting and Cost ConceptsDocument19 pagesManagerial Accounting and Cost ConceptsFarhan RabbehNo ratings yet

- Cost Terms, Concepts, and ClassificationsDocument22 pagesCost Terms, Concepts, and ClassificationsKi xxiNo ratings yet

- Introduction To Cost Accounting: 15.501/516 Spring 2004Document23 pagesIntroduction To Cost Accounting: 15.501/516 Spring 2004scribddmailNo ratings yet

- 10632m Lecture 6 - Full Costing I (Full Version)Document53 pages10632m Lecture 6 - Full Costing I (Full Version)kammiefan215No ratings yet

- Chap002 - Manag Acc & Cost ConceptDocument29 pagesChap002 - Manag Acc & Cost Conceptlilis astriyani sinagaNo ratings yet

- Acctg Terms and Debit CreditDocument3 pagesAcctg Terms and Debit CreditHel LoNo ratings yet

- Acctg Terms and Debit CreditDocument3 pagesAcctg Terms and Debit CreditHel LoNo ratings yet

- Asset Liabilities Equity Revenue Expense: Depreciation Expense Maintenance and Repair ExpensDocument3 pagesAsset Liabilities Equity Revenue Expense: Depreciation Expense Maintenance and Repair ExpensHel LoNo ratings yet

- Asset Liabilities Equity Revenue Expense: Depreciation Expense Maintenance and Repair ExpensDocument3 pagesAsset Liabilities Equity Revenue Expense: Depreciation Expense Maintenance and Repair ExpensediwowNo ratings yet

- Accounting Basic TermsDocument3 pagesAccounting Basic TermsHel LoNo ratings yet

- Assets Liabilitie S Owner'S Equity Income Cost/ Expenses: Figure 1: Elements of Financial StatementsDocument6 pagesAssets Liabilitie S Owner'S Equity Income Cost/ Expenses: Figure 1: Elements of Financial StatementsalexisNo ratings yet

- Accounting Equation - Part 2Document48 pagesAccounting Equation - Part 2Krrish BosamiaNo ratings yet

- Cost Term, Concept and ClassificationsDocument28 pagesCost Term, Concept and ClassificationskumarNo ratings yet

- Lesson 2-Manufacturing AccountDocument20 pagesLesson 2-Manufacturing Accountandrewsamuelhernandez1No ratings yet

- Managerial Accounting and Cost ConceptsDocument18 pagesManagerial Accounting and Cost ConceptsadamNo ratings yet

- Managerial Accounting and Cost ConceptsDocument18 pagesManagerial Accounting and Cost ConceptsrisaNo ratings yet

- 003 03economicDocument5 pages003 03economiceyoboldairNo ratings yet

- Overhead Cost Control: The Operating OfaDocument25 pagesOverhead Cost Control: The Operating OfaLakshmi SNo ratings yet

- Canadian College Of: Business, Science & TechnologyDocument1 pageCanadian College Of: Business, Science & TechnologyAdel LatifNo ratings yet

- Vikram Thermo FinancialsDocument15 pagesVikram Thermo FinancialsUmang ChoudharyNo ratings yet

- Accounting 101Document6 pagesAccounting 101angel luxxNo ratings yet

- I. Cost Terminology: ElementDocument52 pagesI. Cost Terminology: ElementJomar PenaNo ratings yet

- 04 - COA SamplesDocument4 pages04 - COA SamplesJonalyn MalicdanNo ratings yet

- Introduction Cost Concepts Terms and BehaviorDocument43 pagesIntroduction Cost Concepts Terms and BehaviorZACARIAS, Marc Nickson DG.No ratings yet

- Finance NotesDocument23 pagesFinance NoteschamilasNo ratings yet

- Chapter 2-Cost ClassificationDocument66 pagesChapter 2-Cost Classification040404.anniNo ratings yet

- BMT1009 Production and Operations Management BMT1009 Production and Operations ManagementDocument37 pagesBMT1009 Production and Operations Management BMT1009 Production and Operations ManagementYash PathakNo ratings yet

- Ilovepdf MergedDocument34 pagesIlovepdf Mergeddivyanshi singhNo ratings yet

- CPA Financial Accounting and Reporting: Second EditionFrom EverandCPA Financial Accounting and Reporting: Second EditionNo ratings yet

- Consolidation at Acquisition DateDocument18 pagesConsolidation at Acquisition Dategun attaphanNo ratings yet

- Break Even AnalysisDocument16 pagesBreak Even Analysisgun attaphanNo ratings yet

- Drill Problems - ConsolidationDocument6 pagesDrill Problems - Consolidationgun attaphanNo ratings yet

- Comet ExportsDocument1 pageComet Exportspreeti_pariharNo ratings yet

- Mukesh Saini-ResumeDocument3 pagesMukesh Saini-Resumeca.anup.kNo ratings yet

- Chapter 13 Mixed Business TransactionsDocument10 pagesChapter 13 Mixed Business TransactionsGeraldNo ratings yet

- CBDT E-Receipt For E-Tax PaymentDocument1 pageCBDT E-Receipt For E-Tax PaymentSreedhar RaoNo ratings yet

- Huchapter 41 Statement of Cash Flows: Problem 41-1: True or FalseDocument14 pagesHuchapter 41 Statement of Cash Flows: Problem 41-1: True or FalseklairvaughnNo ratings yet

- Monthly Salary & Other Income Statement: 2008-09Document26 pagesMonthly Salary & Other Income Statement: 2008-09api-26910047No ratings yet

- Finance Bill, 2024 E-GazetteDocument27 pagesFinance Bill, 2024 E-GazettecaakhileshvashishthaNo ratings yet

- Financial Statements of Not-for-Profit Organisations: Meaning of Key Terms Used in The ChapterDocument202 pagesFinancial Statements of Not-for-Profit Organisations: Meaning of Key Terms Used in The ChapterVISHNUKUMAR S VNo ratings yet

- Accounting Under GST - An InsightDocument6 pagesAccounting Under GST - An InsightABC 123No ratings yet

- Muhilarasan Kumarasuriyan (VL022) AprDocument1 pageMuhilarasan Kumarasuriyan (VL022) AprRajesh K KNo ratings yet

- Lesson 14 - Maintenance of Registers and RecordsDocument4 pagesLesson 14 - Maintenance of Registers and RecordshemaNo ratings yet

- Abft1024 L14 - LtyDocument3 pagesAbft1024 L14 - Ltylfc778No ratings yet

- 23061500089220SBIN ChallanReceiptDocument2 pages23061500089220SBIN ChallanReceiptSomen Roy SarkarNo ratings yet

- PressRelease Last Date For Linking of PAN Aadhaar Extended 28 3 23Document1 pagePressRelease Last Date For Linking of PAN Aadhaar Extended 28 3 23Faisal SaeedNo ratings yet

- Multi Step IncomeDocument2 pagesMulti Step IncomeRena Rose MalunesNo ratings yet

- IAS 8 - Homework QuestionsDocument2 pagesIAS 8 - Homework QuestionsTsekeNo ratings yet

- Sesión 1 Caso Target Co DatosDocument40 pagesSesión 1 Caso Target Co DatosAida Alvarado EstrellaNo ratings yet

- Practice Question On Capital BudegetingDocument4 pagesPractice Question On Capital Budegetingaditisarkar080No ratings yet

- Chapter 11 Capital Budgeting Cash FlowsDocument33 pagesChapter 11 Capital Budgeting Cash FlowsShahadNo ratings yet

- Unit 18Document20 pagesUnit 18Raja SahilNo ratings yet

- Accounting For Income Tax: LiabilityDocument28 pagesAccounting For Income Tax: Liabilityadmiral spongebobNo ratings yet

- Tutorial EPSDocument3 pagesTutorial EPSRil LlNo ratings yet

- ReportDocument1 pageReportPriyanka DodkeNo ratings yet

- Company Budget Summary Earnings Statement Name of Hotel DateDocument1 pageCompany Budget Summary Earnings Statement Name of Hotel DatePermata Inn Hotel SlawiNo ratings yet

- Leave W/ Pay Leave W/ Pay Holiday Pay Holiday Pay: Total Deductions Total DeductionsDocument1 pageLeave W/ Pay Leave W/ Pay Holiday Pay Holiday Pay: Total Deductions Total DeductionsVic CumpasNo ratings yet

- GST Book PDFDocument606 pagesGST Book PDFsaddamNo ratings yet

- 704 B IRS Partnership AllocationsDocument72 pages704 B IRS Partnership AllocationsAlan PetzoldNo ratings yet