You might also like

- 313 314 Financing Cycle CORNEL-MannelleDocument3 pages313 314 Financing Cycle CORNEL-MannelleFaker MejiaNo ratings yet

- Financial Accounting n 6 Test Mg 2nd Semester 2017 (1)Document8 pagesFinancial Accounting n 6 Test Mg 2nd Semester 2017 (1)professional accountantsNo ratings yet

- Grade 10 Provincial Exam Accounting p1 AnswersDocument7 pagesGrade 10 Provincial Exam Accounting p1 AnswershobyanevisionNo ratings yet

- Item (A) Type of Adjustment (B) Accounts Before AdjustmentDocument11 pagesItem (A) Type of Adjustment (B) Accounts Before Adjustmentsuci monalia putriNo ratings yet

- Grade 11 Test On AdjustmentsDocument6 pagesGrade 11 Test On AdjustmentsENKK 25No ratings yet

- General Journal GJ1 Date Particulars Debit ($) Credit ($)Document25 pagesGeneral Journal GJ1 Date Particulars Debit ($) Credit ($)Jennifer ChandraNo ratings yet

- Accounting Assigment 1 WordDocument7 pagesAccounting Assigment 1 WordlemisiatulihaleniNo ratings yet

- KC Toyland WorksheetDocument13 pagesKC Toyland WorksheettakycabrejasNo ratings yet

- 2007-02 (Code2606) MalaysiaDocument12 pages2007-02 (Code2606) MalaysiaHyc TcNo ratings yet

- Acc AssignmentDocument4 pagesAcc AssignmentBianca BenNo ratings yet

- Kelly Consulting - Assignment1Document14 pagesKelly Consulting - Assignment1krystallanedenice.manansalaNo ratings yet

- 2019 Vol 1 CH 5 AnswersDocument23 pages2019 Vol 1 CH 5 AnswersDummy Number 2No ratings yet

- BT C1 - kttcqt1Document13 pagesBT C1 - kttcqt1Thảo NguyễnNo ratings yet

- ACCOUNTING P1 GR10 MEMO NOV2020 - EnglishDocument6 pagesACCOUNTING P1 GR10 MEMO NOV2020 - EnglishMolemo mabeleNo ratings yet

- Solution Example 3Document2 pagesSolution Example 3ashish panwarNo ratings yet

- QuizDocument41 pagesQuizbar barNo ratings yet

- PART 4 - Opening BalancesDocument2 pagesPART 4 - Opening BalancesTabani RobertNo ratings yet

- Worksheet-The Brilliant CompanyDocument15 pagesWorksheet-The Brilliant Companytristan ignatiusNo ratings yet

- 2019 Vol 1 CH 5 AnswersDocument21 pages2019 Vol 1 CH 5 AnswersArkhie Davocol80% (5)

- Week 3 Topic Tutorial Solutions CB2100 - 1920ADocument12 pagesWeek 3 Topic Tutorial Solutions CB2100 - 1920ALily TsengNo ratings yet

- FINANCIAL ACCOUNTING FUNDAMENTALSDocument7 pagesFINANCIAL ACCOUNTING FUNDAMENTALSabhaymvyas1144No ratings yet

- Grade 10 Provincial Case Study QP 2023Document5 pagesGrade 10 Provincial Case Study QP 2023kwazy dlaminiNo ratings yet

- Jawaban Soal UTS Akuntansi Keu - MenengahDocument4 pagesJawaban Soal UTS Akuntansi Keu - MenengahJessinthaNo ratings yet

- Grade 10 Provincial Exam Accounting P1 (English) November 2019 Possible Answers - 050305Document6 pagesGrade 10 Provincial Exam Accounting P1 (English) November 2019 Possible Answers - 050305hobyanevisionNo ratings yet

- Take Home Examination Bdfa1103Document7 pagesTake Home Examination Bdfa1103zul arifNo ratings yet

- Adjusted Trial BalanceDocument9 pagesAdjusted Trial BalanceashaNo ratings yet

- 9706 Accounting: MARK SCHEME For The May/June 2008 Question PaperDocument8 pages9706 Accounting: MARK SCHEME For The May/June 2008 Question PaperShona MaheshwariNo ratings yet

- Tutorial Chapter 5Document8 pagesTutorial Chapter 5Aisyah SafiNo ratings yet

- CH 005 AIA 5eDocument20 pagesCH 005 AIA 5eNadine MillaminaNo ratings yet

- Acc Gr11 May 2009 PaperDocument13 pagesAcc Gr11 May 2009 PaperSam ChristieNo ratings yet

- INTERMEDIATE TECHNICAL CERTIFICATE EXAMINATION JUNE 2022Document12 pagesINTERMEDIATE TECHNICAL CERTIFICATE EXAMINATION JUNE 2022serge folegweNo ratings yet

- Acc G11 Ec Nov 2022 P2 MGDocument8 pagesAcc G11 Ec Nov 2022 P2 MGTshenoloNo ratings yet

- 2022 Grade 10 Controlled Test 3 QP EngDocument5 pages2022 Grade 10 Controlled Test 3 QP EngkellzylesediNo ratings yet

- REVIEW QUESTIONS IAS 1 & IAS 7Document7 pagesREVIEW QUESTIONS IAS 1 & IAS 7hajiraj504No ratings yet

- Acctng FinalsDocument27 pagesAcctng FinalsErika Mae LegaspiNo ratings yet

- Acc 1Document4 pagesAcc 1Nurul Hidayatul IznieNo ratings yet

- Workshop 5 QsDocument7 pagesWorkshop 5 QsNaresh SehdevNo ratings yet

- Screenshot 2023-12-02 at 6.15.54 PMDocument5 pagesScreenshot 2023-12-02 at 6.15.54 PMn8zn5278y9No ratings yet

- Accounting PaperDocument7 pagesAccounting PaperMuhammad akhtarNo ratings yet

- BAC 211 Group AssDocument12 pagesBAC 211 Group AssStephan Mpundu (T4 enick)No ratings yet

- Chun Ling Trial Exam 2022 - P2 (Answers)Document9 pagesChun Ling Trial Exam 2022 - P2 (Answers)Wei WenNo ratings yet

- Solution Chapter 20 Intermediate Accounting ValixDocument5 pagesSolution Chapter 20 Intermediate Accounting Valixnameless0% (1)

- Fa Templete HomeworkDocument5 pagesFa Templete Homework李斯琪No ratings yet

- PYQ January 2018Document4 pagesPYQ January 2018Nur Amira NadiaNo ratings yet

- General JournalDocument4 pagesGeneral JournalBey IturaldeNo ratings yet

- Book 2Document8 pagesBook 2May ManseNo ratings yet

- Additional Illustrations-20Document16 pagesAdditional Illustrations-20Gulneer LambaNo ratings yet

- 06 Single Entry PQ SolDocument30 pages06 Single Entry PQ Soltyagivansh1200No ratings yet

- Grade 10 Provincial Case Study MG 2023Document3 pagesGrade 10 Provincial Case Study MG 2023kwazy dlaminiNo ratings yet

- Consolidated Financial Statements of Mache BhdDocument8 pagesConsolidated Financial Statements of Mache BhdNUR ATHIRAH SUKAIMINo ratings yet

- Summer ExamDocument17 pagesSummer Examoliverchukwudi97No ratings yet

- Accountancy & Auditing-IDocument4 pagesAccountancy & Auditing-Izaman virkNo ratings yet

- P64571RA Lcci Level 4 Certificate in Financial Accounting ASE20101 RB Sep 2020Document8 pagesP64571RA Lcci Level 4 Certificate in Financial Accounting ASE20101 RB Sep 2020Musthari KhanNo ratings yet

- GR10 Accounting Practice Exam Memorandum November Paper 1Document7 pagesGR10 Accounting Practice Exam Memorandum November Paper 1morukakgothatso5No ratings yet

- ADVANCED ACCOUNTING 2EDocument3 pagesADVANCED ACCOUNTING 2EHarusiNo ratings yet

- Final Accounts ProblemsDocument6 pagesFinal Accounts Problemsbhanu.chandu100% (1)

- Financial AccountingDocument8 pagesFinancial AccountingSri AnishNo ratings yet

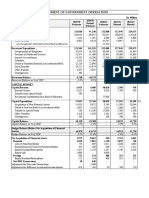

- Statement of Government Operations: O/w Exceptional Contribution From Bank of Mauritius 33,000Document2 pagesStatement of Government Operations: O/w Exceptional Contribution From Bank of Mauritius 33,000Yashas SridatNo ratings yet

- 2019 Unit 3 Outcome 2 Solution BookDocument10 pages2019 Unit 3 Outcome 2 Solution BookLachlan McFarlandNo ratings yet

- Using Economic Indicators to Improve Investment AnalysisFrom EverandUsing Economic Indicators to Improve Investment AnalysisRating: 3.5 out of 5 stars3.5/5 (1)

- Computer PracticeDocument35 pagesComputer PracticeemgnNo ratings yet

- Cfs n5 Study Guide s1Document101 pagesCfs n5 Study Guide s1emgnNo ratings yet

- BasicTrigonometric FunctionsDocument34 pagesBasicTrigonometric FunctionsEdwin QuintoNo ratings yet

- PRLD5111 LU2 Act2 2 2 ProposedsolutionsDocument6 pagesPRLD5111 LU2 Act2 2 2 ProposedsolutionsemgnNo ratings yet

- ReviewDocument17 pagesReviewSreekanthReddy MangammagariNo ratings yet

- Mr. Sumit Sharma: Rs 1,230.74 Rs 0.00 Rs - 593.01 Rs 0.00 Rs 737.73Document3 pagesMr. Sumit Sharma: Rs 1,230.74 Rs 0.00 Rs - 593.01 Rs 0.00 Rs 737.73sumit sharmaNo ratings yet

- Goodwill: Multiple Choices - ComputationalDocument32 pagesGoodwill: Multiple Choices - ComputationalLove FreddyNo ratings yet

- Yard Fencing KSEB 2Document6 pagesYard Fencing KSEB 2isan.structural TjsvgalavanNo ratings yet

- Resources, Conservation and RecyclingDocument9 pagesResources, Conservation and RecyclingAsma Hairulla JaafarNo ratings yet

- Accounting of DepreciationDocument9 pagesAccounting of DepreciationPrasad BhanageNo ratings yet

- Toward Circular Transition in Building Retrofitting - Practitioner's Manual 2020Document34 pagesToward Circular Transition in Building Retrofitting - Practitioner's Manual 2020CirEkonNo ratings yet

- Fundamentals of Accountancy, Business and Management 1Document28 pagesFundamentals of Accountancy, Business and Management 1Marlyn Lotivio40% (10)

- Parkin Econ SM CH06Document21 pagesParkin Econ SM CH06Quang VinhNo ratings yet

- Shelton Gallery Had The Following Petty Cash Transactions in FebDocument1 pageShelton Gallery Had The Following Petty Cash Transactions in FebAmit PandeyNo ratings yet

- WK 8-Case 6: Frenkel's Forensics: John Frenkel Qualified As An Accountant in 1978, and He Has AlwaysDocument2 pagesWK 8-Case 6: Frenkel's Forensics: John Frenkel Qualified As An Accountant in 1978, and He Has AlwaysShehryar KhanNo ratings yet

- Amazon Order FormatDocument4 pagesAmazon Order FormatAlok S YadavNo ratings yet

- Attendance - Inst1 - Batch 1 & 2 (Oct.4,2021-DSF)Document2 pagesAttendance - Inst1 - Batch 1 & 2 (Oct.4,2021-DSF)Aljay LabugaNo ratings yet

- 3 Day Cycle - Day 2. PART 2Document12 pages3 Day Cycle - Day 2. PART 2CristóbalTobalNo ratings yet

- T0 2022-2023 MS FA - WorkbookDocument18 pagesT0 2022-2023 MS FA - WorkbookZhuozhi WuNo ratings yet

- British Charity Accounting Standards ImpactDocument24 pagesBritish Charity Accounting Standards ImpactTareq Yousef AbualajeenNo ratings yet

- Mas 9303 - Standard Costs and Variance AnalysisDocument21 pagesMas 9303 - Standard Costs and Variance AnalysisJowel BernabeNo ratings yet

- Analisis SWOT Pemasaran Produk Kerupuk Buah Di UD. Sukma Kecamatan Takisung Kabupaten Tanah LautDocument11 pagesAnalisis SWOT Pemasaran Produk Kerupuk Buah Di UD. Sukma Kecamatan Takisung Kabupaten Tanah Lautrohmatul sahriNo ratings yet

- Basic Financial Statements Chapter Number 2Document2 pagesBasic Financial Statements Chapter Number 2Muhammad UsamaNo ratings yet

- Deloitte Localisation in Africas Oil & Gas Industry Oct 2015Document18 pagesDeloitte Localisation in Africas Oil & Gas Industry Oct 2015Jim BabanNo ratings yet

- A Complete Project On RBI PDFDocument109 pagesA Complete Project On RBI PDFNiharNo ratings yet

- Chapter 10 HKAS 38 Intangible Assets: 1. ObjectivesDocument19 pagesChapter 10 HKAS 38 Intangible Assets: 1. ObjectivesAmrita TamangNo ratings yet

- Web Order Acknowledgement: Adjusted Tax and Freight Will Appear On Invoice Based On Items ShippedDocument1 pageWeb Order Acknowledgement: Adjusted Tax and Freight Will Appear On Invoice Based On Items ShippedJackNo ratings yet

- Both Parties Filed Separate Recourses To The CADocument2 pagesBoth Parties Filed Separate Recourses To The CANiajhan PalattaoNo ratings yet

- Research Proposal Event StudyDocument5 pagesResearch Proposal Event StudyTheodor Octavian GhineaNo ratings yet

- Globalization ExplainedDocument17 pagesGlobalization ExplainedDino DizonNo ratings yet

- Compound AmountDocument68 pagesCompound AmountKEYDAVE ARNADONo ratings yet

- Final Black Book GST in ResturentsDocument66 pagesFinal Black Book GST in Resturentsirfan khan100% (2)

- CA CFAP 1 NotesDocument350 pagesCA CFAP 1 NotesMoiz Adil0% (1)

- Bafl Q1 23Document86 pagesBafl Q1 23Hassaan AhmedNo ratings yet