You might also like

- TVM Concepts: Introduction to Time Value of Money CalculationsDocument38 pagesTVM Concepts: Introduction to Time Value of Money CalculationsAbhay AgarwalNo ratings yet

- Unit 2 Time Value of MoneyDocument34 pagesUnit 2 Time Value of MoneyPrachi PragyaNo ratings yet

- Chapter 4Document40 pagesChapter 4SyedAunRazaRizviNo ratings yet

- Chapter 4Document40 pagesChapter 4SyedAunRazaRizviNo ratings yet

- Chapter 4Document51 pagesChapter 4Hiền LươngNo ratings yet

- Chap 004Document46 pagesChap 004Ngân PhạmNo ratings yet

- Chap 004Document46 pagesChap 004NazifahNo ratings yet

- Module 1 - 2 Y8at1gDocument21 pagesModule 1 - 2 Y8at1gMuhammad Ihza MahendraNo ratings yet

- Module-1: Calculating the Time Value of MoneyDocument376 pagesModule-1: Calculating the Time Value of Moneyrohit BindNo ratings yet

- Week 4: Discounted Cash Flow ValuationDocument32 pagesWeek 4: Discounted Cash Flow ValuationASAD ULLAHNo ratings yet

- Introduction to Valuation: Key ConceptsDocument22 pagesIntroduction to Valuation: Key ConceptsPrachi PragyaNo ratings yet

- Chap04 FMDocument43 pagesChap04 FMDil RRNo ratings yet

- Time Value of MoneyDocument67 pagesTime Value of MoneyGarvish GangwalNo ratings yet

- Time Value of MoneyDocument16 pagesTime Value of MoneyAnkush PatraNo ratings yet

- Net Present Value: Corporate FinanceDocument38 pagesNet Present Value: Corporate FinanceNguyễn Thùy LinhNo ratings yet

- Present Value, Annuity, and PerpetuityDocument42 pagesPresent Value, Annuity, and PerpetuityEdwin OctorizaNo ratings yet

- Chap4 ModifiedDocument66 pagesChap4 ModifiedRuba AwwadNo ratings yet

- FIN3001 Present Value RecapDocument26 pagesFIN3001 Present Value RecapManton YeungNo ratings yet

- TVMDocument38 pagesTVMbenjamin.labayenNo ratings yet

- Cash Flow NPV, IRRDocument75 pagesCash Flow NPV, IRRDinesh KumarNo ratings yet

- Mishkin and Serletis 8ce Chapter 4Document42 pagesMishkin and Serletis 8ce Chapter 4김승현No ratings yet

- Lecture 3rd Time Value of MoneyDocument26 pagesLecture 3rd Time Value of MoneyBahrawar saidNo ratings yet

- BCH-503-SM04time ValueDocument67 pagesBCH-503-SM04time Valuesugandh bajaj100% (1)

- Time Value of Money: DR. Mohamed SamehDocument22 pagesTime Value of Money: DR. Mohamed SamehRamadan IbrahemNo ratings yet

- Discounted Cash Flow ValuationDocument35 pagesDiscounted Cash Flow ValuationRemonNo ratings yet

- Busn 233 CH 4Document27 pagesBusn 233 CH 4Abreham SolomonNo ratings yet

- Time Value of MoneyDocument25 pagesTime Value of MoneyJeffrey YoungNo ratings yet

- RWJ Chapter 4 DCF ValuationDocument47 pagesRWJ Chapter 4 DCF ValuationAshekin MahadiNo ratings yet

- Corporate Finance: Net Present ValueDocument31 pagesCorporate Finance: Net Present ValueMahfuzur RahmanNo ratings yet

- Future Value, Present Value and Interest Rates: Mcgraw-Hill/IrwinDocument44 pagesFuture Value, Present Value and Interest Rates: Mcgraw-Hill/IrwinYasser AlmishalNo ratings yet

- Time Value of MoneyDocument10 pagesTime Value of MoneyMary Ann MarianoNo ratings yet

- Chapter 3 - Capital BugetingDocument32 pagesChapter 3 - Capital BugetingNguyễn Ngàn NgânNo ratings yet

- FM Unit 4 Lecture Notes - Time Value of MoneyDocument4 pagesFM Unit 4 Lecture Notes - Time Value of MoneyDebbie DebzNo ratings yet

- 02 - TVMDocument18 pages02 - TVMYOGINDRE V PAINo ratings yet

- Chapter 4 Corporate FinanceDocument54 pagesChapter 4 Corporate Financedia100% (1)

- Topic 1-PV, FV, Annunities, Perpetuities - No SolutionsDocument47 pagesTopic 1-PV, FV, Annunities, Perpetuities - No SolutionsJorge Alberto HerreraNo ratings yet

- Lecture 3 - Time Value of MoneyDocument22 pagesLecture 3 - Time Value of MoneyJason LuximonNo ratings yet

- 4-Time Value of MoneyDocument35 pages4-Time Value of Moneysherif_awad100% (1)

- Unit 4Document22 pagesUnit 4SAI GANESH M S 2127321No ratings yet

- Fin 254 - Chapter 5 CorrectedDocument61 pagesFin 254 - Chapter 5 CorrectedsajedulNo ratings yet

- Ch04 Stu - PPT EditedDocument39 pagesCh04 Stu - PPT EditedGaurav ahir pharmacyNo ratings yet

- Discounted CashflowDocument47 pagesDiscounted CashflowAlfred WijayaNo ratings yet

- Discounted Cash Flow ValuationDocument33 pagesDiscounted Cash Flow ValuationShadow IpNo ratings yet

- Seminar 4 DCF Valuation, NPV, and Other Investment RulesDocument79 pagesSeminar 4 DCF Valuation, NPV, and Other Investment RulesPoun GerrNo ratings yet

- Gitman pmf13 ppt05Document79 pagesGitman pmf13 ppt05moonaafreenNo ratings yet

- Topic Two - A Review of Financial MathematicsDocument39 pagesTopic Two - A Review of Financial MathematicsPhương Anh ĐỗNo ratings yet

- CF Lecture 2 Time Value of Money v1Document50 pagesCF Lecture 2 Time Value of Money v1Tâm NhưNo ratings yet

- CH - 4 - Time Value of MoneyDocument49 pagesCH - 4 - Time Value of Moneyak sNo ratings yet

- Chapter 4Document50 pagesChapter 422GayeonNo ratings yet

- Time Value2023Document68 pagesTime Value2023Geethika NayanaprabhaNo ratings yet

- IBF Time Value Problems With SolutionsDocument41 pagesIBF Time Value Problems With SolutionsasaandNo ratings yet

- Time Value of Money: All Rights ReservedDocument79 pagesTime Value of Money: All Rights ReservedBilal SahuNo ratings yet

- Time Value of Money ExplainedDocument8 pagesTime Value of Money ExplainedAngelo DomingoNo ratings yet

- CH 4 - The Meaning of Interest RatesDocument46 pagesCH 4 - The Meaning of Interest RatesAysha KamalNo ratings yet

- Corporate Finance 3Document3 pagesCorporate Finance 3Mujtaba AhmadNo ratings yet

- Lecture 4 - Discounted Cash Flow ValuationDocument18 pagesLecture 4 - Discounted Cash Flow ValuationTrịnh Lê HuyềnNo ratings yet

- Business Finance Module 5Document10 pagesBusiness Finance Module 5CESTINA, KIM LIANNE, B.No ratings yet

- Bonds and Their Valuation: Key Features of Bonds Bond Valuation Measuring Yield Assessing RiskDocument49 pagesBonds and Their Valuation: Key Features of Bonds Bond Valuation Measuring Yield Assessing Risk-Angelzz Lg Gila-No ratings yet

- Applied Corporate Finance. What is a Company worth?From EverandApplied Corporate Finance. What is a Company worth?Rating: 3 out of 5 stars3/5 (2)

- Chapter 8: Structure of Forward and Futures MarketsDocument7 pagesChapter 8: Structure of Forward and Futures MarketsAbracadabraGoonerLincol'otu0% (1)

- Chapter 5: Option Pricing Models: The Black-Scholes-Merton ModelDocument7 pagesChapter 5: Option Pricing Models: The Black-Scholes-Merton ModelDUY LE NHAT TRUONGNo ratings yet

- Chap 9Document7 pagesChap 9GinanjarSaputra0% (1)

- Human Resource Management Midterm Exam: Margin: 3 CM Right Margin: 2,5 CM Header: 1.5 CM Footer: 1.5 CMDocument3 pagesHuman Resource Management Midterm Exam: Margin: 3 CM Right Margin: 2,5 CM Header: 1.5 CM Footer: 1.5 CMDUY LE NHAT TRUONGNo ratings yet

- Chapter 3: Principles of Option PricingDocument7 pagesChapter 3: Principles of Option PricingDUY LE NHAT TRUONGNo ratings yet

- Daily stock price data 2020-2021Document8 pagesDaily stock price data 2020-2021DUY LE NHAT TRUONGNo ratings yet

- Introductory Econometrics For Finance © Chris Brooks 2014 1Document21 pagesIntroductory Econometrics For Finance © Chris Brooks 2014 1Thanh TanNo ratings yet

- Mathematical and Statistical FoundationsDocument60 pagesMathematical and Statistical FoundationsderghalNo ratings yet

- CMGDocument10 pagesCMGDUY LE NHAT TRUONGNo ratings yet

- Chapter 8: Structure of Forward and Futures MarketsDocument7 pagesChapter 8: Structure of Forward and Futures MarketsAbracadabraGoonerLincol'otu0% (1)

- A Brief Overview of The Classical Linear Regression Model: Introductory Econometrics For Finance' © Chris Brooks 2013 1Document80 pagesA Brief Overview of The Classical Linear Regression Model: Introductory Econometrics For Finance' © Chris Brooks 2013 1sdfasdgNo ratings yet

- Dividend Discount Model - DDM Is A Quantitative Method Used ForDocument4 pagesDividend Discount Model - DDM Is A Quantitative Method Used ForDUY LE NHAT TRUONGNo ratings yet

- Chapter 5: Option Pricing Models: The Black-Scholes-Merton ModelDocument7 pagesChapter 5: Option Pricing Models: The Black-Scholes-Merton ModelDUY LE NHAT TRUONGNo ratings yet

- Lecture Introductory Econometrics For Finance: Chapter 4 - Chris BrooksDocument52 pagesLecture Introductory Econometrics For Finance: Chapter 4 - Chris BrooksDuy100% (1)

- Annual Balance Sheet ComparisonDocument28 pagesAnnual Balance Sheet ComparisonDUY LE NHAT TRUONGNo ratings yet

- Chapter 3: Principles of Option PricingDocument7 pagesChapter 3: Principles of Option PricingDUY LE NHAT TRUONGNo ratings yet

- Occupancy DataDocument5 pagesOccupancy Dataphewphewphew200No ratings yet

- Chapter 4: Option Pricing Models: The Binomial ModelDocument9 pagesChapter 4: Option Pricing Models: The Binomial ModelDUY LE NHAT TRUONGNo ratings yet

- Chapter 07 Optimal Risky Portfolios: Answer KeyDocument44 pagesChapter 07 Optimal Risky Portfolios: Answer KeyDUY LE NHAT TRUONGNo ratings yet

- Samsung Marketing Strategies AnalyzedDocument20 pagesSamsung Marketing Strategies AnalyzedDUY LE NHAT TRUONGNo ratings yet

- Chapter 5: Option Pricing Models: The Black-Scholes-Merton ModelDocument7 pagesChapter 5: Option Pricing Models: The Black-Scholes-Merton ModelDUY LE NHAT TRUONGNo ratings yet

- Credit and Inventory ManagementDocument9 pagesCredit and Inventory ManagementDUY LE NHAT TRUONGNo ratings yet

- Balance Sheet (Annual Detail) : Cash and Cash Equivalent Accounts Receivable Inventory Other Current AssetsDocument28 pagesBalance Sheet (Annual Detail) : Cash and Cash Equivalent Accounts Receivable Inventory Other Current AssetsDUY LE NHAT TRUONGNo ratings yet

- Financial Statements Analysis and Financial ModelsDocument48 pagesFinancial Statements Analysis and Financial ModelsDUY LE NHAT TRUONGNo ratings yet

- Capital Structure - Basic ConceptsDocument10 pagesCapital Structure - Basic ConceptsDUY LE NHAT TRUONGNo ratings yet

- Key Concepts and Skills: Mcgraw-Hill/IrwinDocument6 pagesKey Concepts and Skills: Mcgraw-Hill/IrwinDUY LE NHAT TRUONGNo ratings yet

- Financial Statements and Cash FlowDocument43 pagesFinancial Statements and Cash FlowDUY LE NHAT TRUONGNo ratings yet

- Net Present Value and Other Investment RulesDocument6 pagesNet Present Value and Other Investment RulesDUY LE NHAT TRUONGNo ratings yet

- Making Capital Investment DecisionsDocument8 pagesMaking Capital Investment DecisionsDUY LE NHAT TRUONGNo ratings yet

- Activity 1 and 2 Allyssa Marie Gascon GA 2ADocument5 pagesActivity 1 and 2 Allyssa Marie Gascon GA 2AAlyssum MarieNo ratings yet

- RTC - 16Document17 pagesRTC - 16api-729618602No ratings yet

- Bailment and PledgeDocument9 pagesBailment and PledgeSaanvi LuniaNo ratings yet

- 04 Institutional Assessment ToolsDocument11 pages04 Institutional Assessment ToolsJerson Mejares ViagedorNo ratings yet

- Money MangementDocument11 pagesMoney Mangementapi-560277524No ratings yet

- Prepare Trading, P&L and Balance SheetDocument4 pagesPrepare Trading, P&L and Balance SheetShreya ShrivastavaNo ratings yet

- Gratuitous Define As Given or Done With Free Charge. Inofficious Contrary To Moral Obligation, As The Disinheritance of A Child by His Parents: AnDocument5 pagesGratuitous Define As Given or Done With Free Charge. Inofficious Contrary To Moral Obligation, As The Disinheritance of A Child by His Parents: Ankristine torresNo ratings yet

- Assignment - 02 Business Finance (Bm70005) Name: Subhradeep Maitra Roll No: 21Bm91R07 PHD, Autumn SemesterDocument13 pagesAssignment - 02 Business Finance (Bm70005) Name: Subhradeep Maitra Roll No: 21Bm91R07 PHD, Autumn SemesterMainak GhoshNo ratings yet

- Garcia v. Thio (G.R. No. 154878, March 16, 2007)Document3 pagesGarcia v. Thio (G.R. No. 154878, March 16, 2007)Lorie Jean UdarbeNo ratings yet

- Tutorial 7Document74 pagesTutorial 7Dylan Rabin PereiraNo ratings yet

- ) Under The Correct Heading To Show Whether The Item: For Examiner's UseDocument13 pages) Under The Correct Heading To Show Whether The Item: For Examiner's UseAung Zaw HtweNo ratings yet

- Answer: Q4 / P22 / N20 - Analysis and InterpretationDocument1 pageAnswer: Q4 / P22 / N20 - Analysis and InterpretationHaziqah JainiNo ratings yet

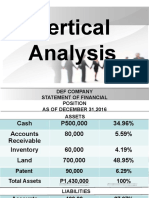

- Vertical analysis of DEF Company's financial statementsDocument8 pagesVertical analysis of DEF Company's financial statementsHannah Mae BautistaNo ratings yet

- Metropol (Bacolod) Financing vs. Sambok MotorsDocument1 pageMetropol (Bacolod) Financing vs. Sambok MotorsThoughts and More ThoughtsNo ratings yet

- Local Media8011400976913649007Document16 pagesLocal Media8011400976913649007Ivan dela CruzNo ratings yet

- Final Account of Sole Trading ConcernDocument7 pagesFinal Account of Sole Trading ConcernAMIN BUHARI ABDUL KHADER50% (2)

- Answer 2Document4 pagesAnswer 2asdfNo ratings yet

- Power of Attorney: LimitedDocument3 pagesPower of Attorney: LimitedRed YoungNo ratings yet

- Transactions List - Service and MerchandisingDocument7 pagesTransactions List - Service and MerchandisingRavann Codera NañolaNo ratings yet

- CFM - 29october Intimation PDFDocument1 pageCFM - 29october Intimation PDFLakshay SharmaNo ratings yet

- Chattel Mortgage CauilanDocument2 pagesChattel Mortgage CauilanHannahQuilangNo ratings yet

- Section ACCA Study HubDocument1 pageSection ACCA Study HublaaybaNo ratings yet

- Business Credit ApplicationDocument4 pagesBusiness Credit ApplicationRocketLawyerNo ratings yet

- B.A.LL.B 2017-22, 8th SemesterDocument3 pagesB.A.LL.B 2017-22, 8th SemesterAnkit KumarNo ratings yet

- London Biscuits Berhad (LBB)Document5 pagesLondon Biscuits Berhad (LBB)Asif ArmanNo ratings yet

- Page 9 Accountinf AfarDocument3 pagesPage 9 Accountinf Afarelsana philipNo ratings yet

- Experienced Sri Lankan Accountant Seeking New OpportunityDocument1 pageExperienced Sri Lankan Accountant Seeking New Opportunityayesha siddiquiNo ratings yet

- Can Fin Homes Ltd. at A Glance: Information To InvestorsDocument21 pagesCan Fin Homes Ltd. at A Glance: Information To InvestorsDhrubajyoti DattaNo ratings yet

- Understanding Due Dates and NPA ClassificationDocument2 pagesUnderstanding Due Dates and NPA ClassificationAFFII MARKETINGNo ratings yet

- Form 26AS: Annual Tax Statement Under Section 203AA of The Income Tax Act, 1961Document4 pagesForm 26AS: Annual Tax Statement Under Section 203AA of The Income Tax Act, 1961flippodynamicsNo ratings yet