You might also like

- Receivable ManagementDocument40 pagesReceivable ManagementrenudhingraNo ratings yet

- Account Receivables Management & Credit Policy: Presented byDocument37 pagesAccount Receivables Management & Credit Policy: Presented byKhalid Khan100% (1)

- Financial Services Firms: Governance, Regulations, Valuations, Mergers, and AcquisitionsFrom EverandFinancial Services Firms: Governance, Regulations, Valuations, Mergers, and AcquisitionsNo ratings yet

- Receivables Management Techniques and Factoring DecisionsDocument26 pagesReceivables Management Techniques and Factoring DecisionsSarthak MattaNo ratings yet

- Chapter 2Document8 pagesChapter 2Pradeep RajNo ratings yet

- Accounts Receivable and Inventory ManagementDocument15 pagesAccounts Receivable and Inventory ManagementYesha TenorNo ratings yet

- Unit 4 Receivables - ManagementDocument27 pagesUnit 4 Receivables - ManagementrehaarocksNo ratings yet

- FFM1-Ch 3. Receivables ManagementDocument49 pagesFFM1-Ch 3. Receivables ManagementQuỳnhNo ratings yet

- B4U2mcs 035Document15 pagesB4U2mcs 035Ts'epo MochekeleNo ratings yet

- Working Capital ManagementDocument5 pagesWorking Capital Managementmanique_abeyratneNo ratings yet

- Accounts ReceivableDocument52 pagesAccounts Receivablemarget100% (3)

- CMCP Chapter 12Document48 pagesCMCP Chapter 12Angelina GamboaNo ratings yet

- Chapter 24 - Working Capital Management - Current Assets and Current LiabilitiesDocument44 pagesChapter 24 - Working Capital Management - Current Assets and Current LiabilitiesKashif Ahmed SaeedNo ratings yet

- Receivables Management & FactoringDocument20 pagesReceivables Management & FactoringYusuf TakliwalaNo ratings yet

- Module 2-Receivables ManagementDocument36 pagesModule 2-Receivables Managementgaurav shettyNo ratings yet

- Credit and Collection Policy Basics: Essential Elements for Managing Accounts ReceivableDocument10 pagesCredit and Collection Policy Basics: Essential Elements for Managing Accounts ReceivablePranjul SahuNo ratings yet

- TOPIC 9 Chapter 19 Accounts Receivable and Inventory ManagementDocument17 pagesTOPIC 9 Chapter 19 Accounts Receivable and Inventory ManagementIrene KimNo ratings yet

- Cash and Liquidity Management (MAIB FIN 101Document26 pagesCash and Liquidity Management (MAIB FIN 101Wgt ChampNo ratings yet

- Supply Chain FinanceDocument3 pagesSupply Chain FinanceThuý NgaNo ratings yet

- Unit 3 - Receivable ManagementDocument18 pagesUnit 3 - Receivable Managementharish100% (1)

- SWOT AnalysisDocument5 pagesSWOT AnalysisFranz Kylle PocsonNo ratings yet

- Working Capital, Credit and Accounts Receivable ManagementDocument31 pagesWorking Capital, Credit and Accounts Receivable ManagementAnkit AgarwalNo ratings yet

- Sessions 25, 26 and 27Document23 pagesSessions 25, 26 and 27Deedra ColeNo ratings yet

- Credit Management FundamentalsDocument40 pagesCredit Management FundamentalsJoseph PoNo ratings yet

- Accounts Receivable ManagementDocument12 pagesAccounts Receivable ManagementAlinah AquinoNo ratings yet

- Credit PolicyDocument84 pagesCredit PolicyDan John Karikottu100% (6)

- Credit and Collection Chap1Document39 pagesCredit and Collection Chap1Nick Jagolino90% (10)

- FM Management NotesDocument96 pagesFM Management NotesGovindh200178% (9)

- Account Receivable: Gloria Concordia N. Reyes Judy S. Reyes Cresia Reyes Mha Pcu Paramount Saturday GroupDocument12 pagesAccount Receivable: Gloria Concordia N. Reyes Judy S. Reyes Cresia Reyes Mha Pcu Paramount Saturday GroupGloria Naguit-ReyesNo ratings yet

- A Study On Receivables ManagementDocument3 pagesA Study On Receivables ManagementShameem AnwarNo ratings yet

- Five Cs of Credit FactorsDocument6 pagesFive Cs of Credit FactorsiftikharchughtaiNo ratings yet

- Chapter 03 Receivable MGTDocument8 pagesChapter 03 Receivable MGTNitesh BansodeNo ratings yet

- FINMNN1 Chapter 4 Short Term Financial PlanningDocument16 pagesFINMNN1 Chapter 4 Short Term Financial Planningkissmoon732No ratings yet

- Notes in Fi3Document5 pagesNotes in Fi3Gray JavierNo ratings yet

- Working Captal ManagementDocument42 pagesWorking Captal Managementjonna mae rapanutNo ratings yet

- ACC-501 Final Term Subjective: Inventory TypesDocument8 pagesACC-501 Final Term Subjective: Inventory TypesbaniNo ratings yet

- Development of Credit and Collection Policy PDFDocument35 pagesDevelopment of Credit and Collection Policy PDFJimuel Faigao100% (1)

- Handout. WCM - Receivable ManagementDocument16 pagesHandout. WCM - Receivable ManagementNaia SNo ratings yet

- Module 2 - Is My Customer Credit WorthyDocument11 pagesModule 2 - Is My Customer Credit Worthyiacpa.aialmeNo ratings yet

- Chapter 7 Primer On Cash Flow ValuationDocument37 pagesChapter 7 Primer On Cash Flow ValuationK60 Phạm Thị Phương AnhNo ratings yet

- SCFaprocurementstrategy v2Document22 pagesSCFaprocurementstrategy v2VikiNo ratings yet

- 5.1 Receivable ManagementDocument18 pages5.1 Receivable ManagementJoshua Cabinas100% (1)

- Receivable ManagementDocument14 pagesReceivable Managementbharath_skumar0% (1)

- CH 7 Account Receivable ManagementDocument12 pagesCH 7 Account Receivable ManagementMichelle Davinna Michael HerryNo ratings yet

- BP Dividend Valuation FinancingDocument31 pagesBP Dividend Valuation FinancingTowhidul IslamNo ratings yet

- Assignment of Receivables ManagementDocument6 pagesAssignment of Receivables ManagementHarsh ChauhanNo ratings yet

- 7e - Chapter 16Document65 pages7e - Chapter 16Lindsay SummersNo ratings yet

- Receivable MNGMNTDocument17 pagesReceivable MNGMNTMary Lyn DatuinNo ratings yet

- Agenda Item 5 - PWC Issue Paper On Loans and BorrowingsDocument23 pagesAgenda Item 5 - PWC Issue Paper On Loans and BorrowingsAKANKWASA ERASMUSNo ratings yet

- Types of Borrowers-Lending ProcessDocument39 pagesTypes of Borrowers-Lending ProcessEr YogendraNo ratings yet

- Receivable & Payable Management PDFDocument7 pagesReceivable & Payable Management PDFa0mittal7No ratings yet

- Advantages of Trade CreditDocument22 pagesAdvantages of Trade CredityadavgunwalNo ratings yet

- FM Intro and Financing Capital BudetingDocument54 pagesFM Intro and Financing Capital BudetingMusangabu EarnestNo ratings yet

- Accounts Receivable Management: 2005 by Thomson Learning, IncDocument31 pagesAccounts Receivable Management: 2005 by Thomson Learning, IncTahmid SadatNo ratings yet

- FIN Case Study + TheoryDocument6 pagesFIN Case Study + Theoryraufun huda dipNo ratings yet

- Moodys - Sample Questions 3Document16 pagesMoodys - Sample Questions 3ivaNo ratings yet

- What Is Credit and Its Risk Management ProcessDocument15 pagesWhat Is Credit and Its Risk Management ProcessJorge NANo ratings yet

- Chapter 5: Option Pricing Models: The Black-Scholes-Merton ModelDocument7 pagesChapter 5: Option Pricing Models: The Black-Scholes-Merton ModelDUY LE NHAT TRUONGNo ratings yet

- Human Resource Management Midterm Exam: Margin: 3 CM Right Margin: 2,5 CM Header: 1.5 CM Footer: 1.5 CMDocument3 pagesHuman Resource Management Midterm Exam: Margin: 3 CM Right Margin: 2,5 CM Header: 1.5 CM Footer: 1.5 CMDUY LE NHAT TRUONGNo ratings yet

- Chapter 8: Structure of Forward and Futures MarketsDocument7 pagesChapter 8: Structure of Forward and Futures MarketsAbracadabraGoonerLincol'otu0% (1)

- Dividend Discount Model - DDM Is A Quantitative Method Used ForDocument4 pagesDividend Discount Model - DDM Is A Quantitative Method Used ForDUY LE NHAT TRUONGNo ratings yet

- Chap 9Document7 pagesChap 9GinanjarSaputra0% (1)

- Lecture Introductory Econometrics For Finance: Chapter 4 - Chris BrooksDocument52 pagesLecture Introductory Econometrics For Finance: Chapter 4 - Chris BrooksDuy100% (1)

- Daily stock price data 2020-2021Document8 pagesDaily stock price data 2020-2021DUY LE NHAT TRUONGNo ratings yet

- Chapter 3: Principles of Option PricingDocument7 pagesChapter 3: Principles of Option PricingDUY LE NHAT TRUONGNo ratings yet

- Introductory Econometrics For Finance © Chris Brooks 2014 1Document21 pagesIntroductory Econometrics For Finance © Chris Brooks 2014 1Thanh TanNo ratings yet

- CMGDocument10 pagesCMGDUY LE NHAT TRUONGNo ratings yet

- Occupancy DataDocument5 pagesOccupancy Dataphewphewphew200No ratings yet

- Chapter 4: Option Pricing Models: The Binomial ModelDocument9 pagesChapter 4: Option Pricing Models: The Binomial ModelDUY LE NHAT TRUONGNo ratings yet

- Annual Balance Sheet ComparisonDocument28 pagesAnnual Balance Sheet ComparisonDUY LE NHAT TRUONGNo ratings yet

- A Brief Overview of The Classical Linear Regression Model: Introductory Econometrics For Finance' © Chris Brooks 2013 1Document80 pagesA Brief Overview of The Classical Linear Regression Model: Introductory Econometrics For Finance' © Chris Brooks 2013 1sdfasdgNo ratings yet

- Mathematical and Statistical FoundationsDocument60 pagesMathematical and Statistical FoundationsderghalNo ratings yet

- Chapter 8: Structure of Forward and Futures MarketsDocument7 pagesChapter 8: Structure of Forward and Futures MarketsAbracadabraGoonerLincol'otu0% (1)

- Chapter 3: Principles of Option PricingDocument7 pagesChapter 3: Principles of Option PricingDUY LE NHAT TRUONGNo ratings yet

- Samsung Marketing Strategies AnalyzedDocument20 pagesSamsung Marketing Strategies AnalyzedDUY LE NHAT TRUONGNo ratings yet

- Chapter 07 Optimal Risky Portfolios: Answer KeyDocument44 pagesChapter 07 Optimal Risky Portfolios: Answer KeyDUY LE NHAT TRUONGNo ratings yet

- Balance Sheet (Annual Detail) : Cash and Cash Equivalent Accounts Receivable Inventory Other Current AssetsDocument28 pagesBalance Sheet (Annual Detail) : Cash and Cash Equivalent Accounts Receivable Inventory Other Current AssetsDUY LE NHAT TRUONGNo ratings yet

- Making Capital Investment DecisionsDocument8 pagesMaking Capital Investment DecisionsDUY LE NHAT TRUONGNo ratings yet

- Key Concepts and Skills: Mcgraw-Hill/IrwinDocument6 pagesKey Concepts and Skills: Mcgraw-Hill/IrwinDUY LE NHAT TRUONGNo ratings yet

- Chapter 5: Option Pricing Models: The Black-Scholes-Merton ModelDocument7 pagesChapter 5: Option Pricing Models: The Black-Scholes-Merton ModelDUY LE NHAT TRUONGNo ratings yet

- Chapter 5: Option Pricing Models: The Black-Scholes-Merton ModelDocument7 pagesChapter 5: Option Pricing Models: The Black-Scholes-Merton ModelDUY LE NHAT TRUONGNo ratings yet

- Capital Structure - Basic ConceptsDocument10 pagesCapital Structure - Basic ConceptsDUY LE NHAT TRUONGNo ratings yet

- Discounted Cash Flow ValuationDocument10 pagesDiscounted Cash Flow ValuationDUY LE NHAT TRUONGNo ratings yet

- Financial Statements Analysis and Financial ModelsDocument48 pagesFinancial Statements Analysis and Financial ModelsDUY LE NHAT TRUONGNo ratings yet

- Financial Statements and Cash FlowDocument43 pagesFinancial Statements and Cash FlowDUY LE NHAT TRUONGNo ratings yet

- Net Present Value and Other Investment RulesDocument6 pagesNet Present Value and Other Investment RulesDUY LE NHAT TRUONGNo ratings yet

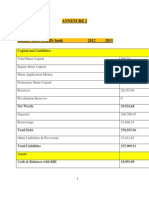

- Annexure 2Document13 pagesAnnexure 2Shalini SrivastavNo ratings yet

- Project Finance: Valuing Unlevered ProjectsDocument32 pagesProject Finance: Valuing Unlevered ProjectsKelsey GaoNo ratings yet

- Chapter 6 Solutions Interest Rates and Bond ValuationDocument7 pagesChapter 6 Solutions Interest Rates and Bond ValuationTuvden Ts100% (1)

- Akuntansi Penyusutan: Novendi Arkham Mubtadi, M.AkunDocument11 pagesAkuntansi Penyusutan: Novendi Arkham Mubtadi, M.AkunAlvita Rahma ZuhaidaNo ratings yet

- Consolidated Bank (Ghana) Limited: Unaudited Summary Financial StatementsDocument2 pagesConsolidated Bank (Ghana) Limited: Unaudited Summary Financial StatementsFuaad DodooNo ratings yet

- Ashoka BuildconDocument523 pagesAshoka Buildconpgp38332No ratings yet

- Stock Market HomeworkDocument6 pagesStock Market Homeworkers57e8s100% (1)

- 01 - Cash and Cash Equivalents (P1 - 13)Document9 pages01 - Cash and Cash Equivalents (P1 - 13)Earl ENo ratings yet

- Buyback and Delisting of SharesDocument42 pagesBuyback and Delisting of SharesSahil SinglaNo ratings yet

- ch12 Test Bank For Intermediate Accounting Ifrs Edition 3eDocument42 pagesch12 Test Bank For Intermediate Accounting Ifrs Edition 3eQuỳnh Châu100% (1)

- Mas TestbanksDocument25 pagesMas TestbanksKristine Esplana ToraldeNo ratings yet

- EACC 1614 - Test 1Document7 pagesEACC 1614 - Test 1sandilefanelehlongwaneNo ratings yet

- PT SURYA PERTIWI Q1 2019 Financial StatementsDocument80 pagesPT SURYA PERTIWI Q1 2019 Financial Statementssiput_lembekNo ratings yet

- NPV, IRR, Payback Period AnalysisDocument4 pagesNPV, IRR, Payback Period AnalysisAyesha SohailNo ratings yet

- Generally Accepted Accounting Principles and Accounting StandardsDocument32 pagesGenerally Accepted Accounting Principles and Accounting StandardsDileepkumar K DiliNo ratings yet

- Sol. Man. - Chapter 8 - Inventory Estimation - Ia Part 1aDocument5 pagesSol. Man. - Chapter 8 - Inventory Estimation - Ia Part 1aYamateNo ratings yet

- A211 MC4 MFRS108 Mfrs110-StudentDocument6 pagesA211 MC4 MFRS108 Mfrs110-StudentGui Xue ChingNo ratings yet

- Module 1Document25 pagesModule 1Gowri MahadevNo ratings yet

- Tender OfferDocument5 pagesTender OfferkiranaishaNo ratings yet

- IFRS for SMEs FAQsDocument5 pagesIFRS for SMEs FAQsMelicent FaithNo ratings yet

- The United States of Bed Bath & Beyond - Epsilon TheoryDocument70 pagesThe United States of Bed Bath & Beyond - Epsilon TheoryHenri GolionoNo ratings yet

- Diageo AnalysisDocument2 pagesDiageo Analysisgckodali0% (1)

- Leasing ProblemsDocument11 pagesLeasing ProblemsAbhishek AbhiNo ratings yet

- 2023-0042-Policy-SEBI Master Circular On Surveillance of Securities MarketDocument28 pages2023-0042-Policy-SEBI Master Circular On Surveillance of Securities MarketmrpankajjainetahNo ratings yet

- Corporations Issuance of StocksDocument8 pagesCorporations Issuance of StocksYoussef NabilNo ratings yet

- PROJECTED FINANCIAL STATEMENTSDocument3 pagesPROJECTED FINANCIAL STATEMENTSNouman BaigNo ratings yet

- Startup Financial Planning - PPT DownloadDocument7 pagesStartup Financial Planning - PPT DownloadhomsomNo ratings yet

- Accounting For Income TaxDocument5 pagesAccounting For Income TaxMa. Kristine GarciaNo ratings yet

- Working Capital and Cash Conversion Cycle AnalysisDocument11 pagesWorking Capital and Cash Conversion Cycle Analysisits4krishna3776No ratings yet

- ATH Technologies: Case-3 Strategic ImplementationDocument8 pagesATH Technologies: Case-3 Strategic ImplementationSumit RajNo ratings yet