You might also like

- Pinga V. Heirs of Santiago GR No. 170354 Facts:: Ex ParteDocument11 pagesPinga V. Heirs of Santiago GR No. 170354 Facts:: Ex ParteMikaela PamatmatNo ratings yet

- Bayer Phils. Versus Agana, G.R. No. L38701 April 8, 1975: FactsDocument51 pagesBayer Phils. Versus Agana, G.R. No. L38701 April 8, 1975: FactsMikaela PamatmatNo ratings yet

- SCA CasesDocument33 pagesSCA CasesMikaela PamatmatNo ratings yet

- G Other CasesDocument86 pagesG Other CasesMikaela PamatmatNo ratings yet

- Esteves v. SarmientoDocument34 pagesEsteves v. SarmientoMikaela PamatmatNo ratings yet

- Document. - Whenever An Action or DefenseDocument8 pagesDocument. - Whenever An Action or DefenseMikaela PamatmatNo ratings yet

- Group 4 - Peaceful Concerted ActivitiesDocument15 pagesGroup 4 - Peaceful Concerted ActivitiesMikaela Pamatmat100% (2)

- Digests FinalDocument12 pagesDigests FinalMikaela PamatmatNo ratings yet

- Digest Titan V DavidDocument3 pagesDigest Titan V DavidMikaela PamatmatNo ratings yet

- Rex Castillon For Petitioners. Fortunato A. Padilla For RespondentsDocument8 pagesRex Castillon For Petitioners. Fortunato A. Padilla For RespondentsMikaela PamatmatNo ratings yet

- Labor Reviewer - WagesDocument22 pagesLabor Reviewer - WagesMikaela Pamatmat100% (1)

- Sustainability 11 05819 v2Document23 pagesSustainability 11 05819 v2Mikaela PamatmatNo ratings yet

- 112 Mandanas v. Executive Secretary OchoaDocument2 pages112 Mandanas v. Executive Secretary OchoaMikaela PamatmatNo ratings yet

- CCFOP v. AquinoDocument3 pagesCCFOP v. AquinoMikaela PamatmatNo ratings yet

- Galang v. WallisDocument2 pagesGalang v. WallisMikaela PamatmatNo ratings yet

- CCFOP v. AquinoDocument3 pagesCCFOP v. AquinoMikaela PamatmatNo ratings yet

- Land Bank v. Atlanta IndustriesDocument3 pagesLand Bank v. Atlanta IndustriesMikaela PamatmatNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5810)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (844)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (348)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1092)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- Guidelines For Combined Sales Tax HolidayDocument23 pagesGuidelines For Combined Sales Tax HolidayWSETNo ratings yet

- September 08 - Chapter 6-Capital Gains Taxation (Assignment)Document3 pagesSeptember 08 - Chapter 6-Capital Gains Taxation (Assignment)anitaNo ratings yet

- Document 4Document6 pagesDocument 4Ernie B LabradorNo ratings yet

- DT Marathon PDFDocument161 pagesDT Marathon PDFAbhi JoshiNo ratings yet

- BTEC Level 3 BusinessDocument21 pagesBTEC Level 3 Businesskamoosh2006No ratings yet

- 1Document18 pages1Japheth GofredoNo ratings yet

- TAX PlanningDocument56 pagesTAX PlanningSangram PandaNo ratings yet

- A Study of Investment Objectives of Individual InvestorsDocument12 pagesA Study of Investment Objectives of Individual InvestorsRishabh SangariNo ratings yet

- 1st Meeting - Tax ComplianceDocument39 pages1st Meeting - Tax ComplianceViney VillasorNo ratings yet

- t2sch31 22eDocument12 pagest2sch31 22eiimauditorNo ratings yet

- One Person CorporationDocument3 pagesOne Person CorporationRengie GaloNo ratings yet

- Maxi S Grocery MartDocument28 pagesMaxi S Grocery MartGagan BhatiaNo ratings yet

- Train Law PowerpointDocument82 pagesTrain Law PowerpointPaula May80% (5)

- Mankiw Economics Chapter 12 NotesDocument2 pagesMankiw Economics Chapter 12 Notesnolessthanthree0% (1)

- PackageC SampleDocument11 pagesPackageC SampleAshraf IskandarNo ratings yet

- MG Motor Dealership Application Form.Document14 pagesMG Motor Dealership Application Form.yogeshjpawar001No ratings yet

- Possession DigestsDocument22 pagesPossession DigestsKayeCie RLNo ratings yet

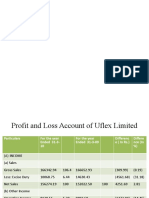

- Friday UFLEXDocument8 pagesFriday UFLEXOnkar TendulkarNo ratings yet

- How Government Agencies Can Use SmsDocument18 pagesHow Government Agencies Can Use SmsChandra SekharNo ratings yet

- 03 27 21Document18 pages03 27 21버니 모지코No ratings yet

- Piperine 2Document1 pagePiperine 2vasavi reddyNo ratings yet

- CA FINAL AMA Nov 14 Guideline Answers 15.11.2014Document16 pagesCA FINAL AMA Nov 14 Guideline Answers 15.11.2014Prateek MadaanNo ratings yet

- Homework Assignment: Module 2 - Process Analysis: Posh NailsDocument49 pagesHomework Assignment: Module 2 - Process Analysis: Posh NailsIisha karmela Alday100% (6)

- Blueprint Portable Smart Trolley FullDocument34 pagesBlueprint Portable Smart Trolley FullAmer Lokhman100% (1)

- IIHMR Question PapersDocument1 pageIIHMR Question PapersRishi TripathiNo ratings yet

- Unit 3: Current Liabilities and ContingenciesDocument22 pagesUnit 3: Current Liabilities and Contingenciesyebegashet100% (1)

- Indian Tax ManagmentDocument242 pagesIndian Tax ManagmentSandeep SandyNo ratings yet

- Resume+Rupesh PrasharDocument5 pagesResume+Rupesh PrasharabhishekatupesNo ratings yet

- Understanding Economic Policy Reform - Dani RodrikDocument33 pagesUnderstanding Economic Policy Reform - Dani RodrikaliaksakalNo ratings yet

- Swathi Final Project AnilDocument100 pagesSwathi Final Project AnilHussainNo ratings yet