You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Caed 7 OutputDocument5 pagesCaed 7 OutputJhonrey BragaisNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Cbme OutputDocument28 pagesCbme OutputJhonrey BragaisNo ratings yet

- Bussiness Plan - FinaleDocument14 pagesBussiness Plan - FinaleJhonrey BragaisNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Cbme 1Document13 pagesCbme 1Jhonrey BragaisNo ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Auditing Power Water and Telecommunication IndustryDocument24 pagesAuditing Power Water and Telecommunication IndustryJhonrey BragaisNo ratings yet

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Caed15 FinalDocument9 pagesCaed15 FinalJhonrey BragaisNo ratings yet

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Introduction To International TradeDocument6 pagesIntroduction To International TradeJhonrey BragaisNo ratings yet

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Banking Financial Institutions.Document18 pagesBanking Financial Institutions.Jhonrey BragaisNo ratings yet

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Ch.2 BudgetProcess. Gr.3Document20 pagesCh.2 BudgetProcess. Gr.3Jhonrey BragaisNo ratings yet

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Audited Financials 2021Document156 pagesAudited Financials 2021Jhonrey BragaisNo ratings yet

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Management Information System 1Document14 pagesManagement Information System 1Jhonrey BragaisNo ratings yet

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- What Type of Auditor You Want To Be .??: The Primary Goals of This Chapter Are As FollowsDocument7 pagesWhat Type of Auditor You Want To Be .??: The Primary Goals of This Chapter Are As FollowsJhonrey BragaisNo ratings yet

- Financial MarketsDocument13 pagesFinancial MarketsJhonrey BragaisNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

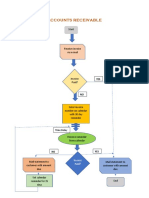

- Accounts ReceivableDocument1 pageAccounts ReceivableJhonrey BragaisNo ratings yet

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Daniel B. Peña Memorial College Foundation, Inc Ziga Avenue, Tabaco CityDocument18 pagesDaniel B. Peña Memorial College Foundation, Inc Ziga Avenue, Tabaco CityJhonrey BragaisNo ratings yet

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Property Plant and EquipmentDocument10 pagesProperty Plant and EquipmentJhonrey BragaisNo ratings yet

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- LiabilitiesDocument7 pagesLiabilitiesJhonrey BragaisNo ratings yet

- Activity 5: Trends in Industry Alcasar Fine WoodsDocument7 pagesActivity 5: Trends in Industry Alcasar Fine WoodsJhonrey BragaisNo ratings yet

- Statement Jun, 2021Document4 pagesStatement Jun, 2021S RNo ratings yet

- AFI Egypt Report AW DigitalDocument12 pagesAFI Egypt Report AW DigitalkamaNo ratings yet

- Bankstatenmmentfromfeb 24 Tomar 264562358 JHDocument6 pagesBankstatenmmentfromfeb 24 Tomar 264562358 JHJc RNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- S&P IBF Vs CBDocument72 pagesS&P IBF Vs CBPT DNo ratings yet

- 20-Year SEC Veteran Tom Sjoblom Sued For Aiding and Abetting in Stanford Financial Group Ponzi SchemeDocument117 pages20-Year SEC Veteran Tom Sjoblom Sued For Aiding and Abetting in Stanford Financial Group Ponzi SchemeStanford Victims Coalition100% (1)

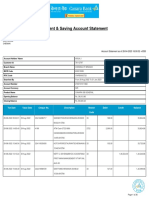

- Current & Saving Account Statement: Arun J Plot No 366 13Th Street Astalakshmi Nagar 3Rd Main RD Alapakkam ChennaiDocument26 pagesCurrent & Saving Account Statement: Arun J Plot No 366 13Th Street Astalakshmi Nagar 3Rd Main RD Alapakkam ChennaiArun Jayaprakash NarayananNo ratings yet

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Reporting Portal FAQs - V5.2Document137 pagesReporting Portal FAQs - V5.2Karthik YadavNo ratings yet

- Bust Top Schools Trial ExamsDocument54 pagesBust Top Schools Trial ExamsGeoffrey ObongoNo ratings yet

- Draft No. 1: Drafting of Legal NoticeDocument2 pagesDraft No. 1: Drafting of Legal NoticeRaghav DhootNo ratings yet

- ISJ016Document108 pagesISJ0162imediaNo ratings yet

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (120)

- KTT - CONTRACT - CDB - AMROCK PETROLEUM LTD - 500m-AaaDocument24 pagesKTT - CONTRACT - CDB - AMROCK PETROLEUM LTD - 500m-AaaRakibul Islam67% (3)

- Adtp Fee 2022 IntiDocument1 pageAdtp Fee 2022 IntiAsma AkterNo ratings yet

- Resume InarDocument3 pagesResume InaresterNo ratings yet

- Assignment No. 1 - Cash and Cash EquivalentsDocument5 pagesAssignment No. 1 - Cash and Cash EquivalentsVincent AbellaNo ratings yet

- Working Capital Management On TATA STEEL 1Document31 pagesWorking Capital Management On TATA STEEL 1Rahul Desu100% (1)

- 165 CamDocument182 pages165 CamHarikrishnan MSNo ratings yet

- Intermediate Accounting 1Document49 pagesIntermediate Accounting 1Harry EvangelistaNo ratings yet

- CH 12Document19 pagesCH 12Ahmed Al EkamNo ratings yet

- Cic2003 Islamic Financial System Assignment 2Document10 pagesCic2003 Islamic Financial System Assignment 2Nur Allieya Aini Binti AzaharNo ratings yet

- RA 7353 Creation of Rural BanksDocument20 pagesRA 7353 Creation of Rural BanksLeah May M. FamorNo ratings yet

- FMI7e ch17Document37 pagesFMI7e ch17lehoangthuchienNo ratings yet

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Cibc Bank Usa Smart Account Agreements and DisclosuresDocument29 pagesCibc Bank Usa Smart Account Agreements and Disclosureshino hinxNo ratings yet

- Roller Coaster Amusement Park Type Design StatusDocument23 pagesRoller Coaster Amusement Park Type Design StatusShaneen AdorableNo ratings yet

- 07 - Cash, Receivables, Inventory Managment ProblemsDocument6 pages07 - Cash, Receivables, Inventory Managment ProblemsMerr Fe PainaganNo ratings yet

- Republic Vs Eugenio DigestDocument4 pagesRepublic Vs Eugenio DigestYul Torrefranca MesaNo ratings yet

- DemoDocument3 pagesDemoEngr Muhammad Khaliq UtroriNo ratings yet

- Insurance Law: Nature, Functions and ChracteristicsDocument17 pagesInsurance Law: Nature, Functions and ChracteristicssanyassandhuNo ratings yet

- Literature Review of Online Payment SystemDocument5 pagesLiterature Review of Online Payment Systemrobin75% (4)

- BBS 4th Year Final WorkDocument48 pagesBBS 4th Year Final WorkNamuna Joshi88% (8)

- Keys VaultsDocument37 pagesKeys VaultsAsfar Khan100% (1)

- Finance Basics (HBR 20-Minute Manager Series)From EverandFinance Basics (HBR 20-Minute Manager Series)Rating: 4.5 out of 5 stars4.5/5 (32)