You might also like

- DQ Cost Acctg Semi-FinalsDocument9 pagesDQ Cost Acctg Semi-FinalsKurt dela TorreNo ratings yet

- Chapter 20 The Computer EnvironmentDocument13 pagesChapter 20 The Computer EnvironmentClar Aaron Bautista100% (1)

- Chapter 3 & 4 Tax ProblemsDocument3 pagesChapter 3 & 4 Tax ProblemsCorazon Lim LeeNo ratings yet

- AT-06 (FS Audit Processs - Pre-Engagement)Document2 pagesAT-06 (FS Audit Processs - Pre-Engagement)Bernadette PanicanNo ratings yet

- Estate Tax Return PreparationDocument1 pageEstate Tax Return PreparationJoongNo ratings yet

- Quiz - Act 07A: I. Theories: ProblemsDocument2 pagesQuiz - Act 07A: I. Theories: ProblemsShawn Organo0% (1)

- AT Preweek (B44)Document7 pagesAT Preweek (B44)Haydy AntonioNo ratings yet

- Government Accounting: 2019 EditionDocument5 pagesGovernment Accounting: 2019 EditionCJNo ratings yet

- Transaction Processing and Financial Reporting Systems OverviewDocument75 pagesTransaction Processing and Financial Reporting Systems Overviewaldwin006No ratings yet

- Quiz BeeDocument15 pagesQuiz BeeRudolf Christian Oliveras UgmaNo ratings yet

- Objectives and Phases of Operational AuditsDocument12 pagesObjectives and Phases of Operational AuditsJacqueline Ortega100% (2)

- Acc110p2quiz 2answers Construction Contracts 1 PDF FreeDocument10 pagesAcc110p2quiz 2answers Construction Contracts 1 PDF FreeMichael Brian TorresNo ratings yet

- Midterms Quiz 1 GdocsDocument41 pagesMidterms Quiz 1 GdocsIris FenelleNo ratings yet

- Allowable Deductions Part 1Document3 pagesAllowable Deductions Part 1John Rich GamasNo ratings yet

- Further Audit Procedures Course at University of BaguioDocument4 pagesFurther Audit Procedures Course at University of BaguioJohn Paul SiodacalNo ratings yet

- Completing the Audit ReportsDocument66 pagesCompleting the Audit ReportsDieter LudwigNo ratings yet

- Quiz No. 2 - AISDocument2 pagesQuiz No. 2 - AISSharjaaahNo ratings yet

- Quiz On Transaction CyclesDocument3 pagesQuiz On Transaction CyclesJelyn SolitoNo ratings yet

- Instructions D. Advanced Financial Accounting and Reporting AFAR.3101 Partnership DrillDocument1 pageInstructions D. Advanced Financial Accounting and Reporting AFAR.3101 Partnership Drillvane rondinaNo ratings yet

- Audit Theory Case AnalysisDocument2 pagesAudit Theory Case AnalysisSheila Mary GregorioNo ratings yet

- RFBT 5-PDIC, Bank Secrecy, and AMLA Pre-TestDocument6 pagesRFBT 5-PDIC, Bank Secrecy, and AMLA Pre-TestCharles D. FloresNo ratings yet

- Audit of Current LiabilitiesDocument4 pagesAudit of Current LiabilitiesMark Anthony TibuleNo ratings yet

- RFBT03-19 - Banking LawsDocument41 pagesRFBT03-19 - Banking LawsWesNo ratings yet

- Final Preboard ExamsDocument5 pagesFinal Preboard ExamsRandy PaderesNo ratings yet

- AUDITING IN CIS ENVIRONMENT Reviewer Chap 1 3Document11 pagesAUDITING IN CIS ENVIRONMENT Reviewer Chap 1 3Michaela De guzmanNo ratings yet

- Audit of Receivables Problems and SolutionsDocument4 pagesAudit of Receivables Problems and SolutionsJai BacalsoNo ratings yet

- Summative Assessment 2 ITDocument9 pagesSummative Assessment 2 ITJoana Trinidad100% (1)

- Quiz 3 - Business Combination and Consolidated Financial StatementsDocument3 pagesQuiz 3 - Business Combination and Consolidated Financial StatementsMaria LopezNo ratings yet

- CPD TRAINING CENTER FINAL PREBOARD EXAMSDocument5 pagesCPD TRAINING CENTER FINAL PREBOARD EXAMSRandy PaderesNo ratings yet

- Auditing Theory - 090: Cis Environment & Completing An Audit CMP The Computer EnvironmentDocument7 pagesAuditing Theory - 090: Cis Environment & Completing An Audit CMP The Computer EnvironmentLeny Joy DupoNo ratings yet

- 7.3.1 Topic Test Questions AnswersDocument34 pages7.3.1 Topic Test Questions AnswersliamdrlnNo ratings yet

- ICARE - MAS - PreWeek - Batch 4Document18 pagesICARE - MAS - PreWeek - Batch 4john paulNo ratings yet

- Accounting policies, estimates and errors quizDocument2 pagesAccounting policies, estimates and errors quizkim cheNo ratings yet

- QuizDocument13 pagesQuizPearl Morni AlbanoNo ratings yet

- Specialized Industries Final ExamDocument8 pagesSpecialized Industries Final Examlois martinNo ratings yet

- Intermediate Accounting Volume 2 by Robles and Empleo 2017 (book) chapterDocument13 pagesIntermediate Accounting Volume 2 by Robles and Empleo 2017 (book) chapterAbraham ChinNo ratings yet

- ACCTG 13 - Quiz 1Document3 pagesACCTG 13 - Quiz 1NEstandaNo ratings yet

- Conversion CycleDocument27 pagesConversion CycleChristine FerrerasNo ratings yet

- Cis Psa 401Document74 pagesCis Psa 401Angela PaduaNo ratings yet

- CL Cup 2018 (AUD, TAX, RFBT)Document4 pagesCL Cup 2018 (AUD, TAX, RFBT)sophiaNo ratings yet

- Valued Added Tax Problems SolvingDocument3 pagesValued Added Tax Problems SolvingLouiseNo ratings yet

- Consignment Sales AccountingDocument5 pagesConsignment Sales AccountingAman SinayaNo ratings yet

- Introduction To Business TaxationDocument12 pagesIntroduction To Business TaxationMariel CadayonaNo ratings yet

- Activity1 JournalizingDocument3 pagesActivity1 JournalizingLightNo ratings yet

- An Introduction To Assurance, Auditing, and Related ServicesDocument18 pagesAn Introduction To Assurance, Auditing, and Related ServicesCristine Bolos0% (1)

- Aaconapps2 00-C91pb2aDocument21 pagesAaconapps2 00-C91pb2aJane DizonNo ratings yet

- Practice Final PB PartialDocument25 pagesPractice Final PB PartialBenedict BoacNo ratings yet

- ToA Quizzer 1 - Intro To PFRS (3TAY1617)Document6 pagesToA Quizzer 1 - Intro To PFRS (3TAY1617)Kyle ParisNo ratings yet

- Chapter 7 - InventoriesDocument16 pagesChapter 7 - InventoriesVanessa VelascoNo ratings yet

- Pre104: Auditing and Assurance: Specialized Industries 1. Overview of Auditing in Specialized IndustriesDocument2 pagesPre104: Auditing and Assurance: Specialized Industries 1. Overview of Auditing in Specialized IndustriesCristina ElizaldeNo ratings yet

- Chapter 10 Vat Still DueDocument7 pagesChapter 10 Vat Still DueHazel Jane EsclamadaNo ratings yet

- FAR 1 - Module 2.2 (Land, Building, and Machinery)Document6 pagesFAR 1 - Module 2.2 (Land, Building, and Machinery)Kin LeeNo ratings yet

- Management of Public Accounting PracticeDocument32 pagesManagement of Public Accounting PracticeClar Aaron Bautista100% (3)

- Financial Accounting and Reporting TheoryDocument58 pagesFinancial Accounting and Reporting TheoryAngelie De LeonNo ratings yet

- MS B45 First PB With AnswersDocument13 pagesMS B45 First PB With AnswersSophia RabacalNo ratings yet

- BanksDocument58 pagesBanksgraceNo ratings yet

- Auditing utilities, power, water and telecom industriesDocument21 pagesAuditing utilities, power, water and telecom industriesCalagui JadeNo ratings yet

- Module 5Document59 pagesModule 5Joanne Michelle B. DueroNo ratings yet

- L01 Introduction To Deregulation 1Document28 pagesL01 Introduction To Deregulation 1Samarendu BaulNo ratings yet

- Hydroelectric PowerDocument8 pagesHydroelectric PowerDiana Isis VelascoNo ratings yet

- Cbme OutputDocument28 pagesCbme OutputJhonrey BragaisNo ratings yet

- Bussiness Plan - FinaleDocument14 pagesBussiness Plan - FinaleJhonrey BragaisNo ratings yet

- Caed15 FinalDocument9 pagesCaed15 FinalJhonrey BragaisNo ratings yet

- Daniel B. Peña Memorial College Foundation operations management course materialDocument13 pagesDaniel B. Peña Memorial College Foundation operations management course materialJhonrey BragaisNo ratings yet

- Caed 7 OutputDocument5 pagesCaed 7 OutputJhonrey BragaisNo ratings yet

- The National Budget ProcessDocument20 pagesThe National Budget ProcessJhonrey BragaisNo ratings yet

- Banking Financial Institutions.Document18 pagesBanking Financial Institutions.Jhonrey BragaisNo ratings yet

- Audited Financials 2021Document156 pagesAudited Financials 2021Jhonrey BragaisNo ratings yet

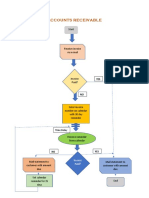

- Accounts ReceivableDocument1 pageAccounts ReceivableJhonrey BragaisNo ratings yet

- Introduction To International TradeDocument6 pagesIntroduction To International TradeJhonrey BragaisNo ratings yet

- Property Plant and EquipmentDocument10 pagesProperty Plant and EquipmentJhonrey BragaisNo ratings yet

- Financial MarketsDocument13 pagesFinancial MarketsJhonrey BragaisNo ratings yet

- Group 1 MIS ProjectDocument14 pagesGroup 1 MIS ProjectJhonrey BragaisNo ratings yet

- Activity 5: Trends in Industry Alcasar Fine WoodsDocument7 pagesActivity 5: Trends in Industry Alcasar Fine WoodsJhonrey BragaisNo ratings yet

- Daniel B. Peña Memorial College Foundation, Inc Ziga Avenue, Tabaco CityDocument18 pagesDaniel B. Peña Memorial College Foundation, Inc Ziga Avenue, Tabaco CityJhonrey BragaisNo ratings yet

- LiabilitiesDocument7 pagesLiabilitiesJhonrey BragaisNo ratings yet

- Thrift Bank FunctionsDocument14 pagesThrift Bank FunctionsJhonrey BragaisNo ratings yet

- What Type of Auditor You Want To Be .??: The Primary Goals of This Chapter Are As FollowsDocument7 pagesWhat Type of Auditor You Want To Be .??: The Primary Goals of This Chapter Are As FollowsJhonrey BragaisNo ratings yet

- Compact Eng PDFDocument44 pagesCompact Eng PDFHarold Antonio Coello AvilaNo ratings yet

- GAIA Green Solar Home SystemDocument55 pagesGAIA Green Solar Home SystemSuryo BrahmantioNo ratings yet

- 1 s2.0 S0306261918311140 MainDocument11 pages1 s2.0 S0306261918311140 MainAllal BouzidNo ratings yet

- DA in Air Separation UnitDocument13 pagesDA in Air Separation UnitRADHESHYAMNo ratings yet

- 11th Integrated Rating 230410 133522Document369 pages11th Integrated Rating 230410 133522soumya sethyNo ratings yet

- Vacon NXP Grid Converter ARFIFF03V164 Manual DPD01599C UK - V001Document185 pagesVacon NXP Grid Converter ARFIFF03V164 Manual DPD01599C UK - V001hunt huntNo ratings yet

- Philippine Distribution Code 2014 Edition 2014 EDITIONDocument117 pagesPhilippine Distribution Code 2014 Edition 2014 EDITIONmanish367No ratings yet

- CV Inghon Update May 21Document6 pagesCV Inghon Update May 21Inghon SilalahiNo ratings yet

- Epira LawDocument40 pagesEpira LawBrentNo ratings yet

- Growth of Solar Energy in IndiaDocument6 pagesGrowth of Solar Energy in Indias_banerjeeNo ratings yet

- Tender Specification No. Cpriblr17Muad25C Annexure - 1 Smart Grid Test Bed Project BackgroundDocument3 pagesTender Specification No. Cpriblr17Muad25C Annexure - 1 Smart Grid Test Bed Project BackgroundElect ronoNo ratings yet

- Prepper & Shooter Issue 02.2014Document80 pagesPrepper & Shooter Issue 02.2014Magdalena Pawłowska100% (2)

- Communication and Control in Electric Power Systems Applications of Parallel and Distributed Processing PDFDocument2 pagesCommunication and Control in Electric Power Systems Applications of Parallel and Distributed Processing PDFMonica0% (1)

- HVDC Transmission - The Solution for Transporting Power Long DistancesDocument1 pageHVDC Transmission - The Solution for Transporting Power Long DistancesSuparna KhamaruNo ratings yet

- FinalDocument21 pagesFinalMohammed Arshad AliNo ratings yet

- Img 20181211 0001Document6 pagesImg 20181211 0001sharmaNo ratings yet

- Renewable Energy: Muhammad Talha, S.R.S. Raihan, N Abd RahimDocument16 pagesRenewable Energy: Muhammad Talha, S.R.S. Raihan, N Abd RahimsharvinNo ratings yet

- Assessing Voltage Stability and Harmonics in Distribution NetworksDocument12 pagesAssessing Voltage Stability and Harmonics in Distribution NetworksGurmessa soressaNo ratings yet

- Model Validation Test TR4 German Method With DIgSILENT GridCode PDFDocument25 pagesModel Validation Test TR4 German Method With DIgSILENT GridCode PDFbubo28No ratings yet

- TNB Tech Guidebook For The Connection of Generation To The Distn Network PDFDocument188 pagesTNB Tech Guidebook For The Connection of Generation To The Distn Network PDFckwei0910No ratings yet

- Generating Hope For A Brighter Future: Bringing Electricity To Arua, UgandaDocument36 pagesGenerating Hope For A Brighter Future: Bringing Electricity To Arua, UgandasedianpoNo ratings yet

- MRN3Document28 pagesMRN3maheshNo ratings yet

- OnGrid - Off.hybrid - Solutions (1) .PDF Version 1Document8 pagesOnGrid - Off.hybrid - Solutions (1) .PDF Version 1Reymart ManablugNo ratings yet

- Operation Manual of KPD100 Controller 20130731 PDFDocument29 pagesOperation Manual of KPD100 Controller 20130731 PDFRamon Palacios83% (6)

- Smart Grid ProposalDocument5 pagesSmart Grid Proposalali farooqNo ratings yet

- Generac Install Manual PWRcell 7 6kW Invetrer APKE00014Document40 pagesGenerac Install Manual PWRcell 7 6kW Invetrer APKE00014Alexandre Maria MullerNo ratings yet

- Presentation On Commissioning of CFBC BoilerDocument26 pagesPresentation On Commissioning of CFBC Boilergaol_bird009100% (2)

- Development of Grid Code For Wind Power Generation in India PowerpointDocument37 pagesDevelopment of Grid Code For Wind Power Generation in India PowerpointgopiNo ratings yet

- Model User Guide For Generic Renewable Energy System ModelsDocument74 pagesModel User Guide For Generic Renewable Energy System ModelsRitesh StanleyNo ratings yet

- Estimating Revenue from Energy Storage in Market AreasDocument30 pagesEstimating Revenue from Energy Storage in Market AreasNeethu Elizabeth MichaelNo ratings yet