You might also like

- YOKOGAWA DCS Training Power Point For System EngineeringDocument689 pagesYOKOGAWA DCS Training Power Point For System EngineeringSerdar Aksoy92% (24)

- 10969742-Kyocera Taskalfa 250ci 300ci 400c I500ci Service ManualDocument586 pages10969742-Kyocera Taskalfa 250ci 300ci 400c I500ci Service Manualhpatel_714706100% (3)

- Vapour Liquid Equilibrium ExpDocument5 pagesVapour Liquid Equilibrium ExpAakash Sharma100% (1)

- Grade 11 - Statistics and ProbabilityDocument9 pagesGrade 11 - Statistics and ProbabilityaminM197769% (36)

- Mathematics Paper Form 2 Term 1 Exam 2018Document8 pagesMathematics Paper Form 2 Term 1 Exam 2018Fook Long WongNo ratings yet

- Ekr 500 Web Guiding ControllerDocument101 pagesEkr 500 Web Guiding Controllermmolina_256079No ratings yet

- General Background Paper On Nord Stream 10 20131128 1Document5 pagesGeneral Background Paper On Nord Stream 10 20131128 1Jerry KleinNo ratings yet

- EWI WP 10-07 Nabucco-And-South-Stream 1201 01Document32 pagesEWI WP 10-07 Nabucco-And-South-Stream 1201 01enderikuNo ratings yet

- Eprs Bri (2021) 690705 enDocument12 pagesEprs Bri (2021) 690705 enZestyCableNo ratings yet

- Eprs Bri (2021) 690705 enDocument20 pagesEprs Bri (2021) 690705 en20070304 Nguyễn Thị PhươngNo ratings yet

- ELIAMEP Thesis No 2Document0 pagesELIAMEP Thesis No 2ioannisgrigoriadisNo ratings yet

- Project Background: Nord Stream 2 AG - Feb-21Document7 pagesProject Background: Nord Stream 2 AG - Feb-21aqua2376No ratings yet

- 3 The Role of Hydrogen in The Transition From A Petroleum EconomyDocument14 pages3 The Role of Hydrogen in The Transition From A Petroleum EconomyDamian Huitzil Cedillo0% (1)

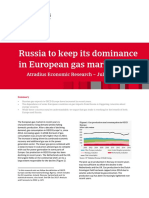

- Atradius Economic Research European Gas July 2018 Ern180710Document3 pagesAtradius Economic Research European Gas July 2018 Ern180710aliNo ratings yet

- Thermodynamic and Technical Issues of Hydrogen and Methane-Hydrogen Mixtures Pipeline TransmissionDocument22 pagesThermodynamic and Technical Issues of Hydrogen and Methane-Hydrogen Mixtures Pipeline TransmissionRoy JudeNo ratings yet

- "Southern Gas Corridor: The Geopolitical and Geo-Economic Implications of An Energy Mega-Project" by Lee MorrisonDocument42 pages"Southern Gas Corridor: The Geopolitical and Geo-Economic Implications of An Energy Mega-Project" by Lee MorrisonThe International Research Center for Energy and Economic Development (ICEED)100% (1)

- 1 s2.0 S2211467X13001028 MainDocument16 pages1 s2.0 S2211467X13001028 Mainwaciy70505No ratings yet

- Case Study - Europe Energy Crisis - WorkDocument7 pagesCase Study - Europe Energy Crisis - WorkJuan Sebastian Buitrago RNo ratings yet

- 2005-IPPE-Water and Hydrogen in Heavy Liquid Metal Coolant TechnologyDocument12 pages2005-IPPE-Water and Hydrogen in Heavy Liquid Metal Coolant Technologycqc2318273994No ratings yet

- Assessment of Existing Steel Structures - Reccomendations For Estimation of Exisitng Fatigue LifeDocument109 pagesAssessment of Existing Steel Structures - Reccomendations For Estimation of Exisitng Fatigue LifeFabrizio BisernaNo ratings yet

- Energy Strategy Reviews: Anton OrlovDocument10 pagesEnergy Strategy Reviews: Anton OrlovMario DavilaNo ratings yet

- Fenrg 08 00191Document12 pagesFenrg 08 00191Petra Margot PedrazaNo ratings yet

- Hydrogen-Natural Gas Mixture Compression in Case of Transporting Thorugh HP PipelinesDocument12 pagesHydrogen-Natural Gas Mixture Compression in Case of Transporting Thorugh HP Pipelinestopspeed1No ratings yet

- DocumentDocument1 pageDocumentAhmadNo ratings yet

- European Nuclear Supply ChainDocument11 pagesEuropean Nuclear Supply ChainJulien VillertNo ratings yet

- Dudau-Gusilov - The Caspian Gas ContestDocument4 pagesDudau-Gusilov - The Caspian Gas ContestRazvan BeluNo ratings yet

- Analysis of Hydrogen Gas Injection at Various Compositions in An Existing Natural Gas PipelineDocument13 pagesAnalysis of Hydrogen Gas Injection at Various Compositions in An Existing Natural Gas PipelineGMSNo ratings yet

- NOx and SO2 Emission Factors For Serbian Lignite K PDFDocument17 pagesNOx and SO2 Emission Factors For Serbian Lignite K PDFElmi KonjushaNo ratings yet

- NOx and SO2 Emission Factors For Serbian Lignite KDocument17 pagesNOx and SO2 Emission Factors For Serbian Lignite KElmi KonjushaNo ratings yet

- Effects of O2 Addition On The DischargeDocument14 pagesEffects of O2 Addition On The Dischargeanthonychoong9No ratings yet

- Europea Centrala Si de Est CEEP - PP - 2022 - MOD3Document38 pagesEuropea Centrala Si de Est CEEP - PP - 2022 - MOD3Gabriel AvacariteiNo ratings yet

- Consequences of Nord Stream 2 For UkraineDocument3 pagesConsequences of Nord Stream 2 For UkraineАнна ВисоцькаNo ratings yet

- Depressurization of Carbon Dioxide in Pipelines-MoDocument9 pagesDepressurization of Carbon Dioxide in Pipelines-MoAmmarul NafikNo ratings yet

- 70 Years of LD Steelmaking - Quo VadisDocument24 pages70 Years of LD Steelmaking - Quo VadisGabriel MáximoNo ratings yet

- Ship Emissions Logistics and Other TradeoffsDocument19 pagesShip Emissions Logistics and Other Tradeoffsfmartins.engNo ratings yet

- Prospective Scenarios On Energy Efficiency and CO2 Emissions in TheDocument16 pagesProspective Scenarios On Energy Efficiency and CO2 Emissions in TheSanny BorgesNo ratings yet

- Surging Liquefied Natural Gas TradeDocument28 pagesSurging Liquefied Natural Gas TradeThe Atlantic CouncilNo ratings yet

- A Complementarity Model For The European Natural Gas MarketDocument30 pagesA Complementarity Model For The European Natural Gas MarketWenfeng ZhangNo ratings yet

- BE3942R15Document26 pagesBE3942R15hrabiecNo ratings yet

- Leporini 2017 J. Phys.: Conf. Ser. 923 012023Document10 pagesLeporini 2017 J. Phys.: Conf. Ser. 923 012023chemsac2No ratings yet

- Pile Foundation For River BridgesDocument27 pagesPile Foundation For River BridgeskaushikrejaNo ratings yet

- Vertical Lift Models Substantiated by Statfjord Field Data: January 2012Document18 pagesVertical Lift Models Substantiated by Statfjord Field Data: January 2012Wilder GanozaNo ratings yet

- Pipelines PresentationDocument35 pagesPipelines PresentationJitendra SurveNo ratings yet

- Concept Project of Zero Energy BuildingDocument10 pagesConcept Project of Zero Energy BuildingChaithanyaNo ratings yet

- BidenDocument3 pagesBidenFaith Van WartNo ratings yet

- Numerical Calculation of Tertiary Air Duct in The Cement Kiln InstallationDocument3 pagesNumerical Calculation of Tertiary Air Duct in The Cement Kiln Installationfilu786No ratings yet

- Euracoal Prognos 2007 EnglDocument8 pagesEuracoal Prognos 2007 EnglYuri Carvalho FerreiraNo ratings yet

- Energy Reports: Huachun He, Hongjun Guan, Xiang Zhu, Haiyu LeeDocument8 pagesEnergy Reports: Huachun He, Hongjun Guan, Xiang Zhu, Haiyu LeeHenna CorpuzNo ratings yet

- 2017RP03 LNG WepDocument39 pages2017RP03 LNG WepJithinNo ratings yet

- Power To Gas Linking Electricity and Gas in A Decarbonising World Insight 39Document17 pagesPower To Gas Linking Electricity and Gas in A Decarbonising World Insight 39Aminos MaNo ratings yet

- The Future of Energy Consumption Security and Natural Gas LNG in The Baltic Sea Region 1St Ed 2022 Edition Kari Liuhto Editor Full ChapterDocument57 pagesThe Future of Energy Consumption Security and Natural Gas LNG in The Baltic Sea Region 1St Ed 2022 Edition Kari Liuhto Editor Full Chapterisaac.flores643100% (5)

- Towards A Transport Infrastructure For Large-Scale CCS in EuropeDocument51 pagesTowards A Transport Infrastructure For Large-Scale CCS in EuropeJonson CaoNo ratings yet

- Hydrogen Import Options For Germany by AgoraDocument18 pagesHydrogen Import Options For Germany by AgoraMarcos Martínez SánchezNo ratings yet

- Chapter 12: Energy Security For The Baltic RegionDocument24 pagesChapter 12: Energy Security For The Baltic RegionShubhangi SinghNo ratings yet

- A Tutorial On Pipe Flow EquationsDocument21 pagesA Tutorial On Pipe Flow Equationsmaminu1No ratings yet

- Norway As A Battery For The Future European Power System-Impacts On The Hydropower SystemDocument25 pagesNorway As A Battery For The Future European Power System-Impacts On The Hydropower SystemSeffds LmlmqsdmlNo ratings yet

- 8aoter 2014 0008Document25 pages8aoter 2014 0008Elias RomeroNo ratings yet

- EASAC Future of Gas WebDocument92 pagesEASAC Future of Gas WebBalintGiliczeNo ratings yet

- 1 Project Summary 1.1 MotivationDocument10 pages1 Project Summary 1.1 MotivationMir AamirNo ratings yet

- European Gas Policy in TroubleDocument4 pagesEuropean Gas Policy in TroubleGerman Marshall Fund of the United StatesNo ratings yet

- Energies 16 01407 v2Document30 pagesEnergies 16 01407 v2Badreddine EssaidiNo ratings yet

- EU China Energy Magazine 2022 November Issue: 2022, #10From EverandEU China Energy Magazine 2022 November Issue: 2022, #10No ratings yet

- EU China Energy Magazine 2022 October Issue: 2022, #8From EverandEU China Energy Magazine 2022 October Issue: 2022, #8No ratings yet

- Scientific American Supplement No. 819, September 12, 1891From EverandScientific American Supplement No. 819, September 12, 1891Rating: 1 out of 5 stars1/5 (1)

- EU China Energy Magazine 2023 October Issue: 2023, #9From EverandEU China Energy Magazine 2023 October Issue: 2023, #9No ratings yet

- Innovation in Electric Arc Furnaces: Scientific Basis for SelectionFrom EverandInnovation in Electric Arc Furnaces: Scientific Basis for SelectionNo ratings yet

- Drugs BALKANS 2020 WebDocument16 pagesDrugs BALKANS 2020 WebDImiskoNo ratings yet

- Human Trafficking in The Central MiddleDocument8 pagesHuman Trafficking in The Central MiddleDImiskoNo ratings yet

- The Archduke's Assassination Came Close To Being Just Another Killing - The Globe and MailDocument6 pagesThe Archduke's Assassination Came Close To Being Just Another Killing - The Globe and MailDImiskoNo ratings yet

- From Medical AstrologyDocument25 pagesFrom Medical AstrologyDImiskoNo ratings yet

- OLAF Investigation Uncovers Research Funding Fraud in Greece - European Anti-Fraud OfficeDocument3 pagesOLAF Investigation Uncovers Research Funding Fraud in Greece - European Anti-Fraud OfficeDImiskoNo ratings yet

- Political Thought in Bosnia and Herzegovina During Austro-Hungarian Rule, 1878-1918Document34 pagesPolitical Thought in Bosnia and Herzegovina During Austro-Hungarian Rule, 1878-1918DImiskoNo ratings yet

- Repeating The Unrepeated Allusions To HoDocument40 pagesRepeating The Unrepeated Allusions To HoDImiskoNo ratings yet

- Russia As An Alternative Security ProvidDocument37 pagesRussia As An Alternative Security ProvidDImiskoNo ratings yet

- Public Transportation and COVID 19Document11 pagesPublic Transportation and COVID 19DImiskoNo ratings yet

- Greeces Elusive Quest For Security ProviDocument14 pagesGreeces Elusive Quest For Security ProviDImiskoNo ratings yet

- Critical Geopolitics and Regional Re ConDocument52 pagesCritical Geopolitics and Regional Re ConDImiskoNo ratings yet

- Russian Influence in Latin America A Response To NDocument27 pagesRussian Influence in Latin America A Response To NDImiskoNo ratings yet

- Trauma GenerationsDocument18 pagesTrauma GenerationsDImiskoNo ratings yet

- 03 2013 Boznia and HerzegovinaDocument2 pages03 2013 Boznia and HerzegovinaDImiskoNo ratings yet

- A Gas Hub Benefits Need and RisksDocument83 pagesA Gas Hub Benefits Need and RisksDImiskoNo ratings yet

- Turkeys EU Cross Border Cooperation ExpeDocument29 pagesTurkeys EU Cross Border Cooperation ExpeDImiskoNo ratings yet

- Legal TyrannicideDocument42 pagesLegal TyrannicideDImiskoNo ratings yet

- Sarajevo 1914: An Examination of The Context by Which Austria-Hungary Responded To The Assassination of Archduke Franz FerdinandDocument33 pagesSarajevo 1914: An Examination of The Context by Which Austria-Hungary Responded To The Assassination of Archduke Franz FerdinandDImiskoNo ratings yet

- Biomolecules ChartDocument2 pagesBiomolecules ChartKelvin Patrick EnriquezNo ratings yet

- Coinco Quantum - Four Tube Operation and Service ManualDocument25 pagesCoinco Quantum - Four Tube Operation and Service ManualVending & Servicios Integrales TecnologíaNo ratings yet

- Physics Extended WritingDocument68 pagesPhysics Extended Writingabu imaanNo ratings yet

- Improvement in Estimating The Population Mean Using Dual To Ratio-Cum-Product Estimator in Simple Random SamplingDocument13 pagesImprovement in Estimating The Population Mean Using Dual To Ratio-Cum-Product Estimator in Simple Random SamplingScience DirectNo ratings yet

- Christiana Rini Indrati - Sufficient Conditions of The Equibalencey Between The Kunugi Integral and The Henstock-Kuzweil IntegralDocument33 pagesChristiana Rini Indrati - Sufficient Conditions of The Equibalencey Between The Kunugi Integral and The Henstock-Kuzweil IntegralValentin MotocNo ratings yet

- Coordination CompoundsDocument97 pagesCoordination CompoundsAnant SharmaNo ratings yet

- Lab BGP CiscoDocument15 pagesLab BGP Ciscocru55er100% (1)

- REPORT - Water DesalinationDocument35 pagesREPORT - Water DesalinationAhmed SalmanNo ratings yet

- K Design-Criteria V00Document80 pagesK Design-Criteria V00Иван РистићNo ratings yet

- AnwanaDocument16 pagesAnwanaHiongyiiNo ratings yet

- Ai Cat IDocument3 pagesAi Cat Ijeff omangaNo ratings yet

- Experiment BioDocument29 pagesExperiment BioQin Jamil100% (1)

- Instructions For Appropriate HandlingDocument4 pagesInstructions For Appropriate HandlingAlioune Badara DioufNo ratings yet

- Inelastic (Creep) Behaviour of ConductorsDocument43 pagesInelastic (Creep) Behaviour of ConductorsHemantha BalasuriyaNo ratings yet

- Variable Displacement Compressor - How It WorksDocument7 pagesVariable Displacement Compressor - How It WorksAbdulmajeed Al KhouriNo ratings yet

- How To Fix and Resolve Quickbooks Error 15106?Document5 pagesHow To Fix and Resolve Quickbooks Error 15106?andrewmoore01No ratings yet

- John Chirillo - Hack Attacks Testing - How To Conduct Your Own Security AuditDocument6 pagesJohn Chirillo - Hack Attacks Testing - How To Conduct Your Own Security AuditShaneNo ratings yet

- A Comparative Study On Software Development ModelsDocument9 pagesA Comparative Study On Software Development ModelsInternational Journal of Application or Innovation in Engineering & ManagementNo ratings yet

- Keyboard Removal Guide: Dell Inspiron 15R (N5010)Document3 pagesKeyboard Removal Guide: Dell Inspiron 15R (N5010)kiranascNo ratings yet

- 11.7 Autocorrelation, Statistical Errors: 2V X T X X 2 T X X T X XDocument4 pages11.7 Autocorrelation, Statistical Errors: 2V X T X X 2 T X X T X XmursalinNo ratings yet

- LogDocument58 pagesLogMuh Akbar24No ratings yet

- Micha Inception ReportDocument37 pagesMicha Inception ReportZoleNo ratings yet

- Grade 3 Theory of Carnatic MusicDocument3 pagesGrade 3 Theory of Carnatic MusicHarey VigneswaranNo ratings yet