You might also like

- Quiz 2 - Audit Cash - 5ae63b1cb41c4b23e6070f657ddaDocument8 pagesQuiz 2 - Audit Cash - 5ae63b1cb41c4b23e6070f657ddaAlexNo ratings yet

- BANK RECON and PROOF OF CASHDocument2 pagesBANK RECON and PROOF OF CASHJay-an AntipoloNo ratings yet

- Cash Shortage Computation: SolutionDocument4 pagesCash Shortage Computation: SolutionCJ alandyNo ratings yet

- Basic Concepts of PartnershipDocument7 pagesBasic Concepts of PartnershipKhim CortezNo ratings yet

- Cash ProblemsDocument5 pagesCash ProblemsAnna AldaveNo ratings yet

- Audit of Cash - IllustrationDocument6 pagesAudit of Cash - IllustrationRNo ratings yet

- Primo Corporation and Sonia Company Consolidated Financial StatementsDocument2 pagesPrimo Corporation and Sonia Company Consolidated Financial StatementsLabLab ChattoNo ratings yet

- Proof of Cash Cebu CompanyDocument6 pagesProof of Cash Cebu CompanyCJ alandyNo ratings yet

- Practice Set 1 (Modules 1 - 3) 371Document8 pagesPractice Set 1 (Modules 1 - 3) 371Marielle CastañedaNo ratings yet

- Solving partnership problems involving sale of non-current assets and insolvency of partnersDocument5 pagesSolving partnership problems involving sale of non-current assets and insolvency of partnersshudayeNo ratings yet

- Partnership profit distribution and capital accountsDocument9 pagesPartnership profit distribution and capital accountsGarp BarrocaNo ratings yet

- CashDocument7 pagesCashhellohello100% (1)

- Accounting Review and Tutorial Services in San Isidro, Nueva EcijaDocument8 pagesAccounting Review and Tutorial Services in San Isidro, Nueva EcijaEiuol Nhoj Arraeugse100% (3)

- Assignment 3 Prepare A Cash Budget KarununganDocument3 pagesAssignment 3 Prepare A Cash Budget KarununganRenzo KarununganNo ratings yet

- Finals Quiz 2 Buscom Version 2Document3 pagesFinals Quiz 2 Buscom Version 2Kristina Angelina ReyesNo ratings yet

- Quiz No. 2Document5 pagesQuiz No. 2VernnNo ratings yet

- Illustration: Formation of Partnership Valuation of Capital A BDocument2 pagesIllustration: Formation of Partnership Valuation of Capital A BArian AmuraoNo ratings yet

- Tutorial BienDocument2 pagesTutorial BienCarlo Baculo100% (1)

- Cash and Accrual Basis: Topic OverviewDocument20 pagesCash and Accrual Basis: Topic OverviewAngelieNo ratings yet

- 33Document2 pages33yes yesnoNo ratings yet

- Refresher Course: Audit of Cash and Cash EquivalentsDocument4 pagesRefresher Course: Audit of Cash and Cash EquivalentsFery Ann100% (1)

- Cash and Cash EquivalentDocument22 pagesCash and Cash EquivalentDanielle Nicole MarquezNo ratings yet

- Quiz VIII - ARDocument3 pagesQuiz VIII - ARBLACKPINKLisaRoseJisooJennieNo ratings yet

- Ia 2Document2 pagesIa 2Nadine SofiaNo ratings yet

- Auditing Report CASE11Document18 pagesAuditing Report CASE11Coke Aidenry SaludoNo ratings yet

- Intermediate Accounting Iii - Final Examination 2 SEMESTER SY 2019-2020Document7 pagesIntermediate Accounting Iii - Final Examination 2 SEMESTER SY 2019-2020ohmyme sungjaeNo ratings yet

- ACP 311 My Test Bank Problem SolvingDocument22 pagesACP 311 My Test Bank Problem SolvingJamaica DavidNo ratings yet

- Proof of Cash - DiscussionDocument4 pagesProof of Cash - DiscussionJoyce Anne GarduqueNo ratings yet

- Problem set on partnership liquidation and distribution of assetsDocument5 pagesProblem set on partnership liquidation and distribution of assetsHoney OrdoñoNo ratings yet

- DICTIOFORMULA Audit of CashDocument13 pagesDICTIOFORMULA Audit of CashEza Joy ClaveriasNo ratings yet

- Audit Prob Cash AnsDocument7 pagesAudit Prob Cash AnsNoreen BinagNo ratings yet

- Additional Problems On MergerDocument6 pagesAdditional Problems On MergerkakeguruiNo ratings yet

- Recording Transactions in a Property Appraisal Business WorksheetDocument1 pageRecording Transactions in a Property Appraisal Business WorksheetKizaru50% (2)

- Proof of Cash Syria CompanyDocument4 pagesProof of Cash Syria CompanyCJ alandy100% (1)

- Problem 12 27Document4 pagesProblem 12 27Bella RonahNo ratings yet

- SDocument18 pagesSdebate dd0% (1)

- Answer Key - Chapter 5 - 2020 EditionDocument37 pagesAnswer Key - Chapter 5 - 2020 EditionDaniel DialinoNo ratings yet

- LNU-AA-23-02-01-18 ExamDocument13 pagesLNU-AA-23-02-01-18 ExamAmie Jane MirandaNo ratings yet

- 1.1.2.a Assignment - Partnership Formation and OperationDocument14 pages1.1.2.a Assignment - Partnership Formation and OperationGiselle MartinezNo ratings yet

- DocxDocument352 pagesDocxsino akoNo ratings yet

- Midterm ExaminationDocument6 pagesMidterm ExaminationJamie Rose Aragones100% (1)

- Required Ending Allowance For Doubtful AccountsDocument4 pagesRequired Ending Allowance For Doubtful AccountsAngelica SamonteNo ratings yet

- This Study Resource WasDocument1 pageThis Study Resource WasKimberly Claire AtienzaNo ratings yet

- Additional InformationDocument32 pagesAdditional InformationMabel GakoNo ratings yet

- Aud Prob - 2nd PreboardDocument13 pagesAud Prob - 2nd PreboardKim Cristian MaañoNo ratings yet

- Proof of Cash - DrillDocument3 pagesProof of Cash - DrillMark Domingo Mendoza100% (1)

- The Determination and Allocation of Excess ScheduleDocument2 pagesThe Determination and Allocation of Excess ScheduleWawex DavisNo ratings yet

- Proof of Cash Baht CompanyDocument6 pagesProof of Cash Baht CompanyCJ alandy100% (1)

- Chapter 3 Material Procurement, Use and ControlDocument3 pagesChapter 3 Material Procurement, Use and ControlKaren CaelNo ratings yet

- Process of Production For Such Sale or in The Form of Materials or Supplies To Be Consumed in The Production Process or in The Rendering of ServicesDocument11 pagesProcess of Production For Such Sale or in The Form of Materials or Supplies To Be Consumed in The Production Process or in The Rendering of ServicesRyan Prado AndayaNo ratings yet

- General Ledger Would Always Be Current After Every Transaction But The Operating Efficiency May Be Affected Depending On The Size of The Company and The Number of Transactions That Are ProcessedDocument2 pagesGeneral Ledger Would Always Be Current After Every Transaction But The Operating Efficiency May Be Affected Depending On The Size of The Company and The Number of Transactions That Are ProcessedRaca DesuNo ratings yet

- Audit Problems CashDocument18 pagesAudit Problems CashYenelyn Apistar Cambarijan0% (1)

- Cannon Ball Review Part 2 Cash and ReceivablesDocument30 pagesCannon Ball Review Part 2 Cash and ReceivablesLayNo ratings yet

- (P21,000-P12,000) (P20,000 - P2,000)Document8 pages(P21,000-P12,000) (P20,000 - P2,000)Shaine PacsonNo ratings yet

- Ellen Company Cash Bank ReconciliationDocument8 pagesEllen Company Cash Bank ReconciliationShaine PacsonNo ratings yet

- FAR 0 Bank Recon and Proof of Cash Drill ProblemsDocument6 pagesFAR 0 Bank Recon and Proof of Cash Drill Problemsyeeaahh56No ratings yet

- Bank Reconciliation & Proof of CashDocument25 pagesBank Reconciliation & Proof of CashTanya MaxNo ratings yet

- Financial Accounting Part 1: Cash & Cash EquivalentDocument7 pagesFinancial Accounting Part 1: Cash & Cash EquivalentHillary Grace VeronaNo ratings yet

- AACONAPPS2 Quiz No. 01 - Audit of Cash Problem Questions (2022)Document4 pagesAACONAPPS2 Quiz No. 01 - Audit of Cash Problem Questions (2022)Dawson Dela CruzNo ratings yet

- Cash and Cash EquivalentsDocument8 pagesCash and Cash EquivalentsNMCartNo ratings yet

- SMP Aud2Document3 pagesSMP Aud2Shaine PacsonNo ratings yet

- Ellen Company Cash Bank ReconciliationDocument8 pagesEllen Company Cash Bank ReconciliationShaine PacsonNo ratings yet

- Ellen Company Cash Bank ReconciliationDocument8 pagesEllen Company Cash Bank ReconciliationShaine PacsonNo ratings yet

- Ellen Company Cash Bank ReconciliationDocument8 pagesEllen Company Cash Bank ReconciliationShaine PacsonNo ratings yet

- (P21,000-P12,000) (P20,000 - P2,000)Document8 pages(P21,000-P12,000) (P20,000 - P2,000)Shaine PacsonNo ratings yet

- (P21,000-P12,000) (P20,000 - P2,000)Document8 pages(P21,000-P12,000) (P20,000 - P2,000)Shaine PacsonNo ratings yet

- Statement of Account: Summary of Charges and CreditsDocument3 pagesStatement of Account: Summary of Charges and CreditsRye LozadaNo ratings yet

- AMANX FactSheetDocument2 pagesAMANX FactSheetamnoman17No ratings yet

- What are PREMIUMS and how are they paidDocument2 pagesWhat are PREMIUMS and how are they paidRhows BuergoNo ratings yet

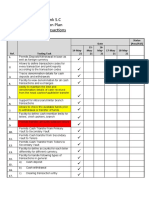

- Zamzam Bank S.C Project Test Action Plan Cash Related TransactionsDocument7 pagesZamzam Bank S.C Project Test Action Plan Cash Related Transactionstofik awelNo ratings yet

- Treasury Challan No: 0200025706 Treasury Challan No: 0200025706 Treasury Challan No: 0200025706Document1 pageTreasury Challan No: 0200025706 Treasury Challan No: 0200025706 Treasury Challan No: 0200025706Mallikarjuna SarmaNo ratings yet

- Gewecke MemoDocument17 pagesGewecke MemoCarrieonicNo ratings yet

- CH 05Document54 pagesCH 05syah RashidNo ratings yet

- Unit Ii Learning Activities Accounting StandardsDocument8 pagesUnit Ii Learning Activities Accounting StandardsChin FiguraNo ratings yet

- Draft SBLC Icbc Akhir-2Document2 pagesDraft SBLC Icbc Akhir-2PT ANUGRAH ENERGY NUSANTARANo ratings yet

- IFRS 7,9, & 32 Financial Instruments: Welcome! July 31, 2019Document55 pagesIFRS 7,9, & 32 Financial Instruments: Welcome! July 31, 2019Andualem ZenebeNo ratings yet

- HIG 2012 - Model Test PromptDocument2 pagesHIG 2012 - Model Test PromptLoïc HalleuxNo ratings yet

- HDFC SLIC OverviewDocument40 pagesHDFC SLIC Overviewprinceramji90No ratings yet

- AccountStatement01-10-2022 To 27-12-2022Document26 pagesAccountStatement01-10-2022 To 27-12-2022Amit KumarNo ratings yet

- 002 Initial Letter To Lender1Document9 pages002 Initial Letter To Lender1Armond TrakarianNo ratings yet

- Activity Ratios: By: Rabindra GouriDocument9 pagesActivity Ratios: By: Rabindra GouriRabindra DasNo ratings yet

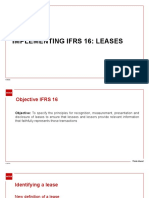

- Implementing Ifrs 16: Leases: © Acca © AccaDocument28 pagesImplementing Ifrs 16: Leases: © Acca © AccadaisyNo ratings yet

- NCC Bank internship report on approval, disbursement & recovery systemDocument74 pagesNCC Bank internship report on approval, disbursement & recovery systemSauron88850% (2)

- BPI US Equity Feeder Fund Latest DisclosureDocument3 pagesBPI US Equity Feeder Fund Latest DisclosureJelor GallegoNo ratings yet

- (CPAR2016) TAX-8014 (+llamado Notes - OTHER PERCENTAGE TAXES)Document12 pages(CPAR2016) TAX-8014 (+llamado Notes - OTHER PERCENTAGE TAXES)jamNo ratings yet

- 6 Receivables ManagementDocument12 pages6 Receivables ManagementShreya BhagavatulaNo ratings yet

- Plantilla Arbitraje FragataDocument11 pagesPlantilla Arbitraje FragataÓscar alvearNo ratings yet

- Banking Decree 1969Document33 pagesBanking Decree 1969Ozim chikaNo ratings yet

- Payday LoansDocument8 pagesPayday LoansChakravarthy Narnindi SharadNo ratings yet

- Jupiter International LimitedDocument6 pagesJupiter International LimitedRahul syalNo ratings yet

- Bond Valuation ProblemsDocument4 pagesBond Valuation ProblemsMary Justine Paquibot100% (1)

- FA1 Chapter 8 EngDocument18 pagesFA1 Chapter 8 Enghahahaha wahahahhaNo ratings yet

- Wire Transfer GuideDocument2 pagesWire Transfer GuideMurdoko RagilNo ratings yet

- The Chicago Plan Revisited - 2d Paper IMFDocument85 pagesThe Chicago Plan Revisited - 2d Paper IMFuser909No ratings yet

- Org ProjectDocument78 pagesOrg Projectsvinduchoodan8614No ratings yet

- What Matters Today How Structured Trade Finance Supports The Global EconomyDocument21 pagesWhat Matters Today How Structured Trade Finance Supports The Global EconomyHicham NedjariNo ratings yet