You might also like

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

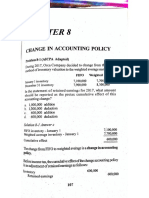

- Week 1 Requirement Introduction To Financial ManagementDocument12 pagesWeek 1 Requirement Introduction To Financial ManagementCarlo B CagampangNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Change in PolicyDocument5 pagesChange in PolicyCarlo B CagampangNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Week 2 RequirementsDocument18 pagesWeek 2 RequirementsCarlo B CagampangNo ratings yet

- Q-2.14.-No AnswerDocument16 pagesQ-2.14.-No AnswerCarlo B CagampangNo ratings yet

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- I Used To Be Black Now I'm WhiteDocument4 pagesI Used To Be Black Now I'm WhiteCarlo B CagampangNo ratings yet

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Make Space For God To FillDocument2 pagesMake Space For God To FillCarlo B CagampangNo ratings yet

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- FC 8 043 Pa Drills and CeremoniesDocument140 pagesFC 8 043 Pa Drills and CeremoniesCarlo B Cagampang100% (1)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- PAS 41 AgricultureDocument4 pagesPAS 41 AgricultureCarlo B Cagampang100% (1)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Application LetterDocument1 pageApplication LetterCarlo B CagampangNo ratings yet

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Linear Programming - MINIMIZATIONDocument3 pagesLinear Programming - MINIMIZATIONCarlo B CagampangNo ratings yet

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Catholic Social TeachingsDocument21 pagesCatholic Social TeachingsCarlo B CagampangNo ratings yet

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- PDF Answers Cost of Capital Exercisesdocdoc - CompressDocument8 pagesPDF Answers Cost of Capital Exercisesdocdoc - CompressCarlo B CagampangNo ratings yet

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- How To Write A Reflection PaperDocument2 pagesHow To Write A Reflection PaperCarlo B Cagampang100% (2)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- 2 Landscape of Financial SystemDocument18 pages2 Landscape of Financial SystemCarlo B CagampangNo ratings yet

- Saint Columban College College of Business Education Acctg 104 - Cost Accounting & Control I Cost Accounting CycleDocument1 pageSaint Columban College College of Business Education Acctg 104 - Cost Accounting & Control I Cost Accounting CycleCarlo B CagampangNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- WALKING IN UNITY (Ephesians 4:1-6)Document3 pagesWALKING IN UNITY (Ephesians 4:1-6)Carlo B CagampangNo ratings yet

- 3 COST Lesson 3Document4 pages3 COST Lesson 3Carlo B Cagampang100% (1)

- The Power of UnityDocument9 pagesThe Power of UnityCarlo B CagampangNo ratings yet

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Financial Accounting Management AccountingDocument4 pagesFinancial Accounting Management AccountingCarlo B CagampangNo ratings yet

- Costs - Concepts and ClassificationsDocument5 pagesCosts - Concepts and ClassificationsCarlo B CagampangNo ratings yet

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- PE Illustrative-Financial-Statements-2022 PEDocument40 pagesPE Illustrative-Financial-Statements-2022 PECalebNo ratings yet

- KraftHeinz 10q 2 2018Document65 pagesKraftHeinz 10q 2 2018Miguel Couto RamosNo ratings yet

- Accounting and Auditing in The PhilippinesDocument15 pagesAccounting and Auditing in The Philippinesman leeNo ratings yet

- FINANCIAL REPORTING - Doc For IKEADocument47 pagesFINANCIAL REPORTING - Doc For IKEAanttheo100% (1)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Intermediate Accounting 17th Edition Kieso Test BankDocument25 pagesIntermediate Accounting 17th Edition Kieso Test BankJenniferWhitebctr100% (53)

- International AccountingDocument4 pagesInternational AccountingCristina Andreea MNo ratings yet

- Fasb 115 PDFDocument2 pagesFasb 115 PDFJosephNo ratings yet

- WEF NES HR4.0 Accounting 2020Document36 pagesWEF NES HR4.0 Accounting 2020RalpNo ratings yet

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- RFBT Reviewer For SalesDocument3 pagesRFBT Reviewer For SalesJerah Marie PepitoNo ratings yet

- Chapter 6 Flowcharting RTRTDocument18 pagesChapter 6 Flowcharting RTRTredearth292950% (2)

- Chapter 1 Financial AccountingDocument41 pagesChapter 1 Financial Accountinge100% (1)

- Capitalization of Software Development CostsDocument50 pagesCapitalization of Software Development CostsGeorge MihailoffNo ratings yet

- Asu 2019-09Document17 pagesAsu 2019-09janineNo ratings yet

- NC1400: Financial Accounting Fundamentals: Section 1: IntroductionDocument50 pagesNC1400: Financial Accounting Fundamentals: Section 1: IntroductionLudmila PeychinovaNo ratings yet

- Part I - Introduction To AISDocument46 pagesPart I - Introduction To AISAgatNo ratings yet

- Audit Mnager With Big 4 and Fortune 500 ExpertiseDocument2 pagesAudit Mnager With Big 4 and Fortune 500 Expertiseapi-77562463No ratings yet

- CS Executive Company Accounts Theory Notes PDFDocument42 pagesCS Executive Company Accounts Theory Notes PDFabhishekNo ratings yet

- What Are Accounting TrendsDocument4 pagesWhat Are Accounting TrendsJena Kryztal TolentinoNo ratings yet

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Isg Ifrs Us Gaap 2022Document593 pagesIsg Ifrs Us Gaap 2022Zain Naqvi50% (2)

- Full Download Test Bank For Essentials of Accounting For Governmental and Not For Profit Organizations 14th Edition Paul Copley PDF Full ChapterDocument36 pagesFull Download Test Bank For Essentials of Accounting For Governmental and Not For Profit Organizations 14th Edition Paul Copley PDF Full Chapterjosephpetersonjaczgqxdsw100% (16)

- Accounting in BusinessDocument46 pagesAccounting in BusinessZachary Jiann Tsong WongNo ratings yet

- Reck 18e Chap001 PPT PDFDocument33 pagesReck 18e Chap001 PPT PDFLojain AlatoomNo ratings yet

- Disclosure Level and Compliance With IASs of Non-Financial Companies in An Emerging Economy A Study BangladeshDocument48 pagesDisclosure Level and Compliance With IASs of Non-Financial Companies in An Emerging Economy A Study BangladeshMonirul Alam HossainNo ratings yet

- PHD Thesis Accounting FinanceDocument7 pagesPHD Thesis Accounting FinancePapersHelpSingapore100% (2)

- SAP Real Estate Management RE FX DigitalDocument16 pagesSAP Real Estate Management RE FX DigitalMichal Duris100% (1)

- Intermediate Accounting - Kieso - Chapter 1Document46 pagesIntermediate Accounting - Kieso - Chapter 1Steffy AmoryNo ratings yet

- Sfac No 6Document91 pagesSfac No 6Riza FebrianNo ratings yet

- HINES - Communicating & Constructing Reality - HighlightedDocument11 pagesHINES - Communicating & Constructing Reality - HighlightedJean S. TheresiaNo ratings yet

- PrelimsDocument27 pagesPrelimsBlairEmrallaf100% (1)