You might also like

- Qa Audit of Receivables and SalesDocument7 pagesQa Audit of Receivables and SalesAsniah M. RatabanNo ratings yet

- Auditing Presentation EssentialsDocument29 pagesAuditing Presentation Essentials21BCO097 ChelsiANo ratings yet

- Unit IDocument17 pagesUnit IThiri PhwayNo ratings yet

- Material Auditing1 5Document86 pagesMaterial Auditing1 5Akshat RanaNo ratings yet

- Auditing Principles and Practices OverviewDocument46 pagesAuditing Principles and Practices OverviewGetie TigetNo ratings yet

- Audit of Receivables WubexDocument9 pagesAudit of Receivables WubexZelalem HassenNo ratings yet

- Auditing Part 1Document54 pagesAuditing Part 1Deepak NayakNo ratings yet

- AuditDocument54 pagesAuditmadhumithamadhu2003No ratings yet

- Explain Objectives of AuditingDocument44 pagesExplain Objectives of AuditingsdfghjkNo ratings yet

- Auditing Revenue Cycle Processes and ControlsDocument3 pagesAuditing Revenue Cycle Processes and ControlsRatna SariNo ratings yet

- AuditingDocument54 pagesAuditingShreya SinghNo ratings yet

- PRINCIPLES OF AUDITING Bharathiar University III B COM PADocument59 pagesPRINCIPLES OF AUDITING Bharathiar University III B COM PAkalpanaNo ratings yet

- Auditing PresentationDocument54 pagesAuditing PresentationMuzaFarNo ratings yet

- AuditingDocument54 pagesAuditingSuresh ReddyNo ratings yet

- Cfa Books - The Analysis and Use of Financial Statements - Resume - White, Sondhi, WhiteDocument18 pagesCfa Books - The Analysis and Use of Financial Statements - Resume - White, Sondhi, Whiteshare7575100% (3)

- Audit Lec 4&5&6Document8 pagesAudit Lec 4&5&6adelNo ratings yet

- Unit I (A) Notes Meaning of AuditingDocument5 pagesUnit I (A) Notes Meaning of AuditingsdddNo ratings yet

- ????? ?? Chapter 6Document38 pages????? ?? Chapter 6addisyawkal18No ratings yet

- Topic 2-1Document35 pagesTopic 2-1fbicia218No ratings yet

- Xi Acts Ca (2022 23)Document197 pagesXi Acts Ca (2022 23)sara VermaNo ratings yet

- Audit Receivables SalesDocument22 pagesAudit Receivables SalesTesfaye Megiso BegajoNo ratings yet

- Errors & FraudsDocument27 pagesErrors & FraudsmostakNo ratings yet

- Chapter 19 AnswerDocument19 pagesChapter 19 AnswerMjVerbaNo ratings yet

- Acctg. Ed 1 - Unit2 Module 6 Business Transactions and Their AnalysisDocument29 pagesAcctg. Ed 1 - Unit2 Module 6 Business Transactions and Their AnalysisAngel Justine BernardoNo ratings yet

- FINANCIAL STATEMENT LECTUREDocument33 pagesFINANCIAL STATEMENT LECTUREkacaribuantonNo ratings yet

- Unit 1 Meaning and Definition of AuditingDocument88 pagesUnit 1 Meaning and Definition of AuditingsdfghjkNo ratings yet

- Chapter 14 AuditingDocument9 pagesChapter 14 Auditingmeiwin manihing100% (1)

- BCom 6th Sem - AuditingDocument46 pagesBCom 6th Sem - AuditingJibinNo ratings yet

- BCom 6th Sem - AuditingDocument46 pagesBCom 6th Sem - AuditingJibin SamuelNo ratings yet

- AnswersDocument15 pagesAnswersHarmeet KaurNo ratings yet

- Ethics Internal ControlDocument9 pagesEthics Internal ControlEll VNo ratings yet

- Internal Controls For The Accounting Function (Contd.) : 1.examples of Accounting SubsystemsDocument31 pagesInternal Controls For The Accounting Function (Contd.) : 1.examples of Accounting Subsystemsraina mattNo ratings yet

- Auditing 4 Chapter 4Document6 pagesAuditing 4 Chapter 4Mohamed DiabNo ratings yet

- I. Definitions, Standards and PlanningDocument4 pagesI. Definitions, Standards and PlanninglauraoldkwNo ratings yet

- Auditing PDF 1.1Document18 pagesAuditing PDF 1.1anilanitha974No ratings yet

- STANDARD OF AUDITING SUMMARY REVISION WITH CASE STUDIES UPLOADED ON 11th MAY 2017 636302080328521091 PDFDocument48 pagesSTANDARD OF AUDITING SUMMARY REVISION WITH CASE STUDIES UPLOADED ON 11th MAY 2017 636302080328521091 PDFVinoth AnandNo ratings yet

- Unit 1: Two Marks QuestionsDocument35 pagesUnit 1: Two Marks QuestionsabhiNo ratings yet

- Accounting notesDocument71 pagesAccounting noteswaseem ahsanNo ratings yet

- Audit Evidence SummaryDocument14 pagesAudit Evidence SummaryEunice GloriaNo ratings yet

- Year Unit I Introduction To Auditing Meaning and Definition of AuditingDocument53 pagesYear Unit I Introduction To Auditing Meaning and Definition of AuditingTimothy KambuniNo ratings yet

- BAM 1 - Fundamentals of AccountingDocument33 pagesBAM 1 - Fundamentals of AccountingimheziiyyNo ratings yet

- Accounts Receivable Audit ProceduresDocument5 pagesAccounts Receivable Audit ProceduresVivien NaigNo ratings yet

- Principles of Auditing - Chapter - 1Document36 pagesPrinciples of Auditing - Chapter - 1Wijdan Saleem EdwanNo ratings yet

- Sybcom Sem Iv - Audit Chapter 1 & 2Document24 pagesSybcom Sem Iv - Audit Chapter 1 & 2Pravin KharateNo ratings yet

- Financial System & Auditing BBA-3 BB0013Document10 pagesFinancial System & Auditing BBA-3 BB0013Sowdhamini GanesunNo ratings yet

- Mod 5 - AuditingDocument51 pagesMod 5 - AuditingInchara S Dept of MBANo ratings yet

- Auditing Notes.Document55 pagesAuditing Notes.Viraja Guru50% (2)

- Acc231 - CH 1Document16 pagesAcc231 - CH 1alaamabood6No ratings yet

- Auditing NewDocument20 pagesAuditing NewJapjiv SinghNo ratings yet

- ACCT6174 - Introduction To Financial Accounting: Week 6 Fraud, Internal Control, Cash, and Account ReceivableDocument37 pagesACCT6174 - Introduction To Financial Accounting: Week 6 Fraud, Internal Control, Cash, and Account ReceivableNadya NingrumNo ratings yet

- Errors and Irregularities in The Transaction CyclesDocument39 pagesErrors and Irregularities in The Transaction CyclesE.D.J83% (6)

- Existence or Occurrence Completeness Rights and Obligations Valuation or AllocationDocument3 pagesExistence or Occurrence Completeness Rights and Obligations Valuation or AllocationReyes, Jessica R.No ratings yet

- Errors and Irregulari-Ties in The Transaction Cycles of The Business EntityDocument38 pagesErrors and Irregulari-Ties in The Transaction Cycles of The Business EntityClark Regin SimbulanNo ratings yet

- Accounting Period Shareholders DividendsDocument3 pagesAccounting Period Shareholders DividendsAmaranathreddy YgNo ratings yet

- Q1) Objectives of AuditingDocument23 pagesQ1) Objectives of AuditingsdfghjkNo ratings yet

- Audit Complete Notes 5th SemDocument60 pagesAudit Complete Notes 5th Semuchihaakash47No ratings yet

- Concepts and PrinciplesDocument13 pagesConcepts and PrinciplesJonafhel RaguinNo ratings yet

- Internal Control of Fixed Assets: A Controller and Auditor's GuideFrom EverandInternal Control of Fixed Assets: A Controller and Auditor's GuideRating: 4 out of 5 stars4/5 (1)

- "The Language of Business: How Accounting Tells Your Story" "A Comprehensive Guide to Understanding, Interpreting, and Leveraging Financial Statements for Personal and Professional Success"From Everand"The Language of Business: How Accounting Tells Your Story" "A Comprehensive Guide to Understanding, Interpreting, and Leveraging Financial Statements for Personal and Professional Success"No ratings yet

- Member Cooperative in EnglishDocument352 pagesMember Cooperative in Englishums tvishiNo ratings yet

- GR 9 EMS P1 (English) November 2022 Possible AnswersDocument8 pagesGR 9 EMS P1 (English) November 2022 Possible Answerssamanthamachingura45No ratings yet

- How To Start Your Successful: Free GuideDocument24 pagesHow To Start Your Successful: Free GuideElvis BorbaNo ratings yet

- Accounting Entries in Oracle AppsDocument4 pagesAccounting Entries in Oracle Appsjramki100% (3)

- Petty Cash /imprest Reimbursement Post Audit ChecklistDocument2 pagesPetty Cash /imprest Reimbursement Post Audit ChecklistHenry Mapa100% (1)

- Finding Your Hotel in the PhilippinesDocument2 pagesFinding Your Hotel in the PhilippinescanigetaccessNo ratings yet

- RFP Sewa Gudang Adib Feb 2021Document3 pagesRFP Sewa Gudang Adib Feb 2021Sulis SetioriniNo ratings yet

- Fedex Corporation, 2015: Final Group Case StudyDocument97 pagesFedex Corporation, 2015: Final Group Case Studyderbydrive19No ratings yet

- 01 Jan 2021 To 24 Aug 2022 FCMB StatementDocument2 pages01 Jan 2021 To 24 Aug 2022 FCMB StatementOjo StellaNo ratings yet

- Bike Share PresentationDocument71 pagesBike Share PresentationPaul100% (2)

- AmplifierDocument2 pagesAmplifierbalakeresnanramakasnainNo ratings yet

- University of Santo Tomas Alfredo M. Velayo College of AccountancyDocument4 pagesUniversity of Santo Tomas Alfredo M. Velayo College of AccountancyChni Gals0% (1)

- ResumeDocument3 pagesResumeapi-301267735No ratings yet

- 4 Form e Abcd StatementDocument2 pages4 Form e Abcd Statementnee praNo ratings yet

- TP LinkDocument41 pagesTP LinkCARLOS JOHNSONNo ratings yet

- Chapter 2 Fabm1Document19 pagesChapter 2 Fabm1Remilyn Joy Abrazado PecasoNo ratings yet

- AccountingDocument26 pagesAccountingMuhammad Jaafar AbinalNo ratings yet

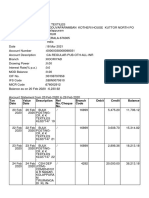

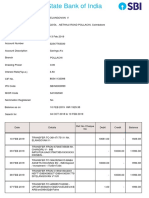

- TXN Date Value Date Description Ref No./Cheque No. Branch Code Debit Credit BalanceDocument4 pagesTXN Date Value Date Description Ref No./Cheque No. Branch Code Debit Credit BalanceJaseem MonuNo ratings yet

- Sir Win ExercisesDocument21 pagesSir Win ExercisesAbigail RososNo ratings yet

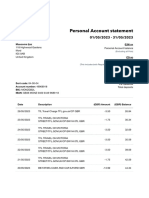

- Account StatementDocument6 pagesAccount Statement41k POLLACHINo ratings yet

- Monzo Bank Statement 2023 05 01-2023 05 31 9229Document5 pagesMonzo Bank Statement 2023 05 01-2023 05 31 9229MasoomaIjazNo ratings yet

- Lending Book PDFDocument335 pagesLending Book PDFSarim ShahidNo ratings yet

- Annex 5-REGISTER OF CASH RECEIPTS, DEPOSITS AND OTHER RELATED FINANCIALDocument3 pagesAnnex 5-REGISTER OF CASH RECEIPTS, DEPOSITS AND OTHER RELATED FINANCIALVermon JayNo ratings yet

- Cross-Border B2B RelationshipsDocument13 pagesCross-Border B2B RelationshipsJainisha KumawatNo ratings yet

- 4113 PDFDocument6 pages4113 PDFDaniel NexNo ratings yet

- FABM2 Module 7 Darl DelimaDocument27 pagesFABM2 Module 7 Darl DelimaFaye LañadaNo ratings yet

- Types of Letter of CreditDocument3 pagesTypes of Letter of CreditMd Abusaied AsikNo ratings yet

- Z Im Wum MEMLHx BAGNDocument15 pagesZ Im Wum MEMLHx BAGNIssac EbbuNo ratings yet

- Debit and Credit Entries for October TransactionsDocument20 pagesDebit and Credit Entries for October TransactionsPatrixia Nikole Mariae Sumabat100% (1)

- Brian Hicks Letters of Credit 4Document23 pagesBrian Hicks Letters of Credit 4habchiNo ratings yet