You might also like

- Prelims Ia3 Key-Answers PDFDocument19 pagesPrelims Ia3 Key-Answers PDFLalaland Acads54% (13)

- Midterm Partnership Liquidation AssignmentDocument6 pagesMidterm Partnership Liquidation AssignmentLee Suarez0% (1)

- AFAR Self Test - 9002Document7 pagesAFAR Self Test - 9002Jennifer RueloNo ratings yet

- Activity 1 Partnership OperationsDocument5 pagesActivity 1 Partnership OperationsClaire Barba100% (1)

- (Solved) Galaxy Corporation Acquired 80% of The Outstanding Shares of United... - Course HeroDocument6 pages(Solved) Galaxy Corporation Acquired 80% of The Outstanding Shares of United... - Course Heroadulusman501No ratings yet

- PR Proposal Letter of TransmittalDocument2 pagesPR Proposal Letter of TransmittalKris Shaw100% (4)

- QHSE002 QHSE Manual Rev 0.0 PDFDocument41 pagesQHSE002 QHSE Manual Rev 0.0 PDFRafeeq rahman100% (1)

- Advanced Accounting Part 1 Dayag 2015 Chapter 6Document19 pagesAdvanced Accounting Part 1 Dayag 2015 Chapter 6trisha sacramentoNo ratings yet

- Numbers 19, 20 and 21 (Corporate Liquidation)Document2 pagesNumbers 19, 20 and 21 (Corporate Liquidation)Tk KimNo ratings yet

- Discussions About Contracts With Customer Other IssuesDocument14 pagesDiscussions About Contracts With Customer Other Issuestrisha0% (1)

- Assignment Open Ended QuestionsDocument11 pagesAssignment Open Ended QuestionsRina Mae Sismar Lawi-an100% (1)

- Chapter 1 Intermediate 1Document58 pagesChapter 1 Intermediate 1Rez Judiel Aramigo AnchetaNo ratings yet

- ACC 110 RemedialDocument11 pagesACC 110 RemedialGiner Mabale StevenNo ratings yet

- Accounting For Special Transactions and Cost Accounting and ControlDocument12 pagesAccounting For Special Transactions and Cost Accounting and ControlRNo ratings yet

- Joint Arrangements Answer Key Chapter 10 Problems 4 To 7Document3 pagesJoint Arrangements Answer Key Chapter 10 Problems 4 To 7Jeane Mae BooNo ratings yet

- Chapter 17 - Consol. Fs Part 2Document6 pagesChapter 17 - Consol. Fs Part 2PutmehudgJasdNo ratings yet

- Activity Ans KeyDocument2 pagesActivity Ans KeyJuly LumantasNo ratings yet

- Ac8dccd2 1613019594275Document7 pagesAc8dccd2 1613019594275Emey CalbayNo ratings yet

- Module 2 Foundation ProblemDocument4 pagesModule 2 Foundation ProblemasdasdaNo ratings yet

- Advacc 1 Quiz VIIIDocument4 pagesAdvacc 1 Quiz VIIIJason GubatanNo ratings yet

- Balbin, Ma. Margarette P. Assignment #1Document7 pagesBalbin, Ma. Margarette P. Assignment #1Margaveth P. BalbinNo ratings yet

- Consignment True or False: Page Rferrer/Rlaco/Atang/DejesusDocument6 pagesConsignment True or False: Page Rferrer/Rlaco/Atang/DejesusNicoleNo ratings yet

- Unit 3 Long Term Construction ContractDocument20 pagesUnit 3 Long Term Construction ContractTrixie Hicalde0% (1)

- Chapter 16 Advacc2Document60 pagesChapter 16 Advacc2AnneShannenBambaDabuNo ratings yet

- Corporate Liquidation: Question #11 Page 100Document2 pagesCorporate Liquidation: Question #11 Page 100lanimfa dela cruzNo ratings yet

- UntitledDocument9 pagesUntitledJanna Mari FriasNo ratings yet

- The Balance Sheet For The Partnership of JJ CC and TTDocument1 pageThe Balance Sheet For The Partnership of JJ CC and TTdagohoy kennethNo ratings yet

- Revenue Recognition: Long Term ConstructionDocument3 pagesRevenue Recognition: Long Term ConstructionLee SuarezNo ratings yet

- 10Document4 pages10kyla christineNo ratings yet

- Midterm ExamDocument9 pagesMidterm ExamElla TuratoNo ratings yet

- Additional ProblemsDocument3 pagesAdditional Problems가 푸 레멜 린 메No ratings yet

- AST FinalsDocument20 pagesAST FinalsMica Ella San DiegoNo ratings yet

- Mga Dambieee!!!!: Complete Answer Pleaseee. Thank Youuu NO. Questions Answer 1 Answer 2 If Unsure Answer 1Document12 pagesMga Dambieee!!!!: Complete Answer Pleaseee. Thank Youuu NO. Questions Answer 1 Answer 2 If Unsure Answer 1Hannah Jane UmbayNo ratings yet

- P2 06Document9 pagesP2 06Darrel100% (1)

- Mas 1 QuizDocument7 pagesMas 1 Quizsean justin EspinaNo ratings yet

- Answer KEY PPEDocument6 pagesAnswer KEY PPExjammerNo ratings yet

- Module 3.1 Licenses, Royalties & Franchise Part 1Document18 pagesModule 3.1 Licenses, Royalties & Franchise Part 1NCTNo ratings yet

- Home Office and Branch HandoutsDocument4 pagesHome Office and Branch HandoutsbangtansonyeondaNo ratings yet

- Chapter 10Document9 pagesChapter 10chan.charanchan100% (1)

- Revenue Recognition: Long Term ConstructionDocument2 pagesRevenue Recognition: Long Term ConstructionLee SuarezNo ratings yet

- Solution Chapter 18Document61 pagesSolution Chapter 18xxxxxxxxx100% (3)

- Problem: I - Statement of Affairs and Deficiency AccountDocument1 pageProblem: I - Statement of Affairs and Deficiency AccountAnn Marie GabayNo ratings yet

- Notes - Conso FS (Subsequent To Acquisition Date)Document35 pagesNotes - Conso FS (Subsequent To Acquisition Date)Joana TrinidadNo ratings yet

- Big Picture in Focus: Ulob. Account For Branch and Home Office Transactions and Prepare Financial Statements Let'S AnalyzeDocument3 pagesBig Picture in Focus: Ulob. Account For Branch and Home Office Transactions and Prepare Financial Statements Let'S AnalyzeJean Rose Tabagay BustamanteNo ratings yet

- Problem II A. 1. A. P87,725Document5 pagesProblem II A. 1. A. P87,725MckenzieNo ratings yet

- Chapter 7Document18 pagesChapter 7Yenelyn Apistar CambarijanNo ratings yet

- Cost Accounting Guerrero Franchises Chap06Document17 pagesCost Accounting Guerrero Franchises Chap06AlexanNo ratings yet

- Adv Acc Chapter4Document13 pagesAdv Acc Chapter4Reanne Claudine LagunaNo ratings yet

- HOBADocument9 pagesHOBAJulie Mae Caling MalitNo ratings yet

- Lesson Title: Home Office, Branch and Agency: AccountingDocument14 pagesLesson Title: Home Office, Branch and Agency: AccountingFeedback Or BawiNo ratings yet

- Chapter 18 Cost Accounting.Document19 pagesChapter 18 Cost Accounting.Kheng BinuyaNo ratings yet

- ACTIVITY 1 Capital BudgetingDocument12 pagesACTIVITY 1 Capital BudgetingkmarisseeNo ratings yet

- Long Term Contracts Percentage of Completion MethodDocument3 pagesLong Term Contracts Percentage of Completion MethodRifi ANo ratings yet

- CH 10 Long Term ContractsDocument6 pagesCH 10 Long Term ContractsMerr Fe PainaganNo ratings yet

- Mary Joy Asis QUIZ 1Document6 pagesMary Joy Asis QUIZ 1Joseph AsisNo ratings yet

- Auditing ProblemsDocument29 pagesAuditing ProblemsPrincesNo ratings yet

- Cpa Review School of The Philippines ManilaDocument2 pagesCpa Review School of The Philippines ManilaAlliah Mae ArbastoNo ratings yet

- Lagura - Ass04 Statement of Comprehensive IncomeDocument7 pagesLagura - Ass04 Statement of Comprehensive IncomeShane LaguraNo ratings yet

- Interim Financial Reporting and Operating Segment Discussion Problems and Answer KeyDocument4 pagesInterim Financial Reporting and Operating Segment Discussion Problems and Answer Keyprincess QNo ratings yet

- AaaaDocument11 pagesAaaaJessica JaroNo ratings yet

- AA1 Ass 3 LTCCDocument4 pagesAA1 Ass 3 LTCCangel caoNo ratings yet

- MAF551 - Exercise 3 - Answer Question 1 - RIdzuan Bin Saharun 2017700141 - NACAB5CDocument4 pagesMAF551 - Exercise 3 - Answer Question 1 - RIdzuan Bin Saharun 2017700141 - NACAB5CRIDZUAN SAHARUNNo ratings yet

- IA3 - REVIEWER - Internediate 3Document38 pagesIA3 - REVIEWER - Internediate 3Mujahad QuirinoNo ratings yet

- FeasibDocument138 pagesFeasibMarinella LosaNo ratings yet

- Income Tax Seat WorkDocument16 pagesIncome Tax Seat WorkMarinella LosaNo ratings yet

- MR Fortaleza Nov. 30,2021: Materials Measurement 3inch 2x3 2x6 2x3 2x6Document2 pagesMR Fortaleza Nov. 30,2021: Materials Measurement 3inch 2x3 2x6 2x3 2x6Marinella LosaNo ratings yet

- Financial InstrumentsDocument1 pageFinancial InstrumentsMarinella LosaNo ratings yet

- Statement of Financial PositionDocument2 pagesStatement of Financial PositionMarinella LosaNo ratings yet

- Income Tax Seat WorkDocument16 pagesIncome Tax Seat WorkMarinella LosaNo ratings yet

- Chapter 5 Fina Man - Marinella A LosaDocument19 pagesChapter 5 Fina Man - Marinella A LosaMarinella LosaNo ratings yet

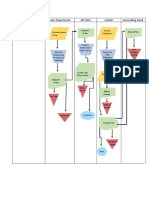

- Production Department Sales Department AR Clerk Cashier Accounting HeadDocument1 pageProduction Department Sales Department AR Clerk Cashier Accounting HeadMarinella LosaNo ratings yet

- Presentation - InterAccDocument11 pagesPresentation - InterAccMarinella LosaNo ratings yet

- Chapter 5 Fina Man - Marinella A LosaDocument19 pagesChapter 5 Fina Man - Marinella A LosaMarinella LosaNo ratings yet

- Activity 2 Auditing - Marinella A. LosaDocument14 pagesActivity 2 Auditing - Marinella A. LosaMarinella LosaNo ratings yet

- NAMEDocument7 pagesNAMEMarinella LosaNo ratings yet

- ARB 51: Consolidated Financial StatementsDocument20 pagesARB 51: Consolidated Financial Statementspijej25153No ratings yet

- InterAcc 14-33Document11 pagesInterAcc 14-33Marinella LosaNo ratings yet

- Orca Share Media1532943158075Document2 pagesOrca Share Media1532943158075Marinella LosaNo ratings yet

- Chapter 5 Fina Man - Marinella A LosaDocument19 pagesChapter 5 Fina Man - Marinella A LosaMarinella LosaNo ratings yet

- Activityu 4Document1 pageActivityu 4Marinella LosaNo ratings yet

- Activity 7Document1 pageActivity 7Marinella LosaNo ratings yet

- Activity 8Document1 pageActivity 8Marinella LosaNo ratings yet

- The Satisfaction Rate of Students in Gordon College (Senior High School Department) in Various Fast Food Chains in Olongapo CityDocument3 pagesThe Satisfaction Rate of Students in Gordon College (Senior High School Department) in Various Fast Food Chains in Olongapo CityMarinella LosaNo ratings yet

- Us Memorial Day: The Following Is FromDocument2 pagesUs Memorial Day: The Following Is FromMarinella LosaNo ratings yet

- Activity 7Document1 pageActivity 7Marinella LosaNo ratings yet

- Behind The Woods: Modernang MariaclaraDocument1 pageBehind The Woods: Modernang MariaclaraMarinella LosaNo ratings yet

- Activity 8Document1 pageActivity 8Marinella LosaNo ratings yet

- Activityu 4Document1 pageActivityu 4Marinella LosaNo ratings yet

- Tokyo's Housing - Sheryl Anne JaimeDocument2 pagesTokyo's Housing - Sheryl Anne JaimeMarinella LosaNo ratings yet

- Activity 9Document1 pageActivity 9Marinella LosaNo ratings yet

- Activity 5Document1 pageActivity 5Marinella LosaNo ratings yet

- Tokyo's Academe and Job Opportunities - Vina Mae DeleonDocument2 pagesTokyo's Academe and Job Opportunities - Vina Mae DeleonMarinella LosaNo ratings yet

- U2-05 - Example of Potential Client For The Curious Beetle - ENDocument4 pagesU2-05 - Example of Potential Client For The Curious Beetle - ENRosy RuizNo ratings yet

- MCQs BPEMDocument13 pagesMCQs BPEMhridyansh kainNo ratings yet

- ObjectivesDocument2 pagesObjectivesAdiza BaduaNo ratings yet

- Ebook Cornerstones of Cost Management 2Nd Edition Hansen Solutions Manual Full Chapter PDFDocument67 pagesEbook Cornerstones of Cost Management 2Nd Edition Hansen Solutions Manual Full Chapter PDFriaozgas3023100% (10)

- TOMS Case Study Aishath Shanasa 1191402196Document8 pagesTOMS Case Study Aishath Shanasa 1191402196BushraNo ratings yet

- Multinational StrategyDocument2 pagesMultinational StrategyThị Ninh DươngNo ratings yet

- Objectives of Marketing ProcessDocument6 pagesObjectives of Marketing ProcessMamta VermaNo ratings yet

- Cau Hoi Unit1Document3 pagesCau Hoi Unit1Hiền HiềnNo ratings yet

- Completed AssignmentDocument85 pagesCompleted AssignmentJulianaJamilNo ratings yet

- Quiz 7 (HRM 2022)Document6 pagesQuiz 7 (HRM 2022)Sandipan DawnNo ratings yet

- 419-Article Text-1018-1-10-20191118Document12 pages419-Article Text-1018-1-10-20191118Rejjal As-SaqqāfNo ratings yet

- Additional Funds Needed - Exercises - QuestionsDocument2 pagesAdditional Funds Needed - Exercises - QuestionsDANE MATTHEW PILAPILNo ratings yet

- Coca Cola (KO) Financial RatiosDocument4 pagesCoca Cola (KO) Financial RatiosKhmao SrosNo ratings yet

- Broadband Bill AugustDocument1 pageBroadband Bill AugustkarthikNo ratings yet

- Microsoft Buys SkypeDocument3 pagesMicrosoft Buys SkypePuffyTeddyNo ratings yet

- BCG Matrix of Nestle in A Simplified Way - Business MavericksDocument1 pageBCG Matrix of Nestle in A Simplified Way - Business MavericksAyanNo ratings yet

- Group Assignment For The Course Introduction To Economics May 9Document4 pagesGroup Assignment For The Course Introduction To Economics May 9yohannes lemiNo ratings yet

- SUPPLY CHAIN MANAGEMENT - PD-02-DipDocument2 pagesSUPPLY CHAIN MANAGEMENT - PD-02-DipFred ChinsingaNo ratings yet

- Ch. 5 in Class Exercises 1 PDFDocument5 pagesCh. 5 in Class Exercises 1 PDFRasab AhmedNo ratings yet

- Controlling RobbinsDocument30 pagesControlling RobbinsDantaPlayzNo ratings yet

- Sample 2 Aircraft PurchaseDocument4 pagesSample 2 Aircraft PurchaseApril mitaNo ratings yet

- Role of NCLT - IbcDocument23 pagesRole of NCLT - IbcVicky D67% (3)

- MSC Personal StatementDocument2 pagesMSC Personal StatementDrew JoanNo ratings yet

- K - GRP 7 - Report On Aviation SectorDocument47 pagesK - GRP 7 - Report On Aviation SectorApoorva PattnaikNo ratings yet

- Case Study:: How I Generated N310K in 7 Days Using WhatsappDocument12 pagesCase Study:: How I Generated N310K in 7 Days Using WhatsappCollins felixNo ratings yet

- Sunzi Art of War AssignmentDocument11 pagesSunzi Art of War AssignmentEveliaNo ratings yet

- Sri Lanka Media Audience Study 2019Document64 pagesSri Lanka Media Audience Study 2019methlalNo ratings yet

- Akg Exim Limited Akg Exim Limited Akg Exim Limited: Annual Report Annual Report 2019-2020Document80 pagesAkg Exim Limited Akg Exim Limited Akg Exim Limited: Annual Report Annual Report 2019-2020Nihit SandNo ratings yet