You might also like

- Eurekahedge May 2011 Key Trends in Fund of Hedge Funds - AbridgedDocument1 pageEurekahedge May 2011 Key Trends in Fund of Hedge Funds - AbridgedEurekahedgeNo ratings yet

- V-Shaped Recovery in PerspectiveDocument5 pagesV-Shaped Recovery in PerspectiveJaphyNo ratings yet

- Macro-Economic Case of The PhilippinesDocument21 pagesMacro-Economic Case of The PhilippinesMichaelAngeloBattungNo ratings yet

- Document 1083870621Document5 pagesDocument 1083870621Okan AladağNo ratings yet

- PricelistDocument94 pagesPricelistkalpeshpotdarNo ratings yet

- Waterfall Chart TemplateDocument3 pagesWaterfall Chart TemplateMichael GarciaNo ratings yet

- Investment Function: ImportanceDocument5 pagesInvestment Function: ImportanceHades RiegoNo ratings yet

- Hospital Supply Inc Background of The Case PDF FreeDocument35 pagesHospital Supply Inc Background of The Case PDF Freewho sinoNo ratings yet

- CEO Presentation of Q2 2008 ResultsDocument49 pagesCEO Presentation of Q2 2008 ResultsSwedbank AB (publ)No ratings yet

- Volvo Car Group Financial Report Fy 2014Document15 pagesVolvo Car Group Financial Report Fy 2014Ishank SinghNo ratings yet

- NIPA vs. S&P 500 - Yardeni - 03aug2022Document10 pagesNIPA vs. S&P 500 - Yardeni - 03aug2022scribbugNo ratings yet

- The Economic Foundations of Imperialism: Guglielmo Carchedi and Michael Roberts HM London November 2019Document28 pagesThe Economic Foundations of Imperialism: Guglielmo Carchedi and Michael Roberts HM London November 2019MrWaratahsNo ratings yet

- Sample Slides - Unit 2Document23 pagesSample Slides - Unit 2RinNo ratings yet

- Target 2 OversightDocument14 pagesTarget 2 OversightHidayati WitimNo ratings yet

- Bubble ChartDocument2 pagesBubble ChartRalph Brandon BulusanNo ratings yet

- ch01 2Document21 pagesch01 2Jigar PatelNo ratings yet

- TP, MP, MC CurvesDocument13 pagesTP, MP, MC Curvesnihma100% (2)

- Financial Services Co BudgetsDocument21 pagesFinancial Services Co BudgetsAlexandru VasilescuNo ratings yet

- San AntonioDocument1 pageSan AntonioDolo GarciaNo ratings yet

- Indoneisa 2013Document36 pagesIndoneisa 2013Iam IbadNo ratings yet

- RES 1S Layout1Document1 pageRES 1S Layout1Nyel ArmstrongNo ratings yet

- BRS Review2018 01 ShipbuildingDocument14 pagesBRS Review2018 01 Shipbuildingarunkumar17No ratings yet

- MR. Ali Denah Lt.2lDocument1 pageMR. Ali Denah Lt.2lnengay.putriNo ratings yet

- Calculate The MPSDocument4 pagesCalculate The MPSMinahill AkramNo ratings yet

- Q1 Exports: Bed Wear Cotton ClothDocument10 pagesQ1 Exports: Bed Wear Cotton ClothSaqib RehanNo ratings yet

- United States of America, Including Puerto Rico and U.S.v.I.2013Document2 pagesUnited States of America, Including Puerto Rico and U.S.v.I.2013Camilo Estiven P GomezNo ratings yet

- National School of Business Management 19.2 Batch: I I I IDocument8 pagesNational School of Business Management 19.2 Batch: I I I IshanuxNo ratings yet

- Worldwide ICT Spending by Technology FactorDocument1 pageWorldwide ICT Spending by Technology FactorRodr-No ratings yet

- BQ ProposalDocument1 pageBQ ProposalOjebola AyobamiNo ratings yet

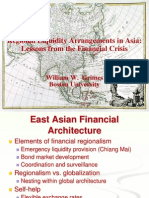

- Regional Liquidity Arrangements in Asia: Lessons From The Financial CrisisDocument12 pagesRegional Liquidity Arrangements in Asia: Lessons From The Financial CrisisblondedahliaNo ratings yet

- Detail Pembuangan Septic TankDocument1 pageDetail Pembuangan Septic TankMuhammad DjuandaNo ratings yet

- Chartbook of The IGWT20 Gold Conquering New Record HighsDocument68 pagesChartbook of The IGWT20 Gold Conquering New Record HighsTFMetals100% (1)

- Assignment: Saqib Rehan 11310Document11 pagesAssignment: Saqib Rehan 11310Saqib RehanNo ratings yet

- Cerdeñola, Jane Paula C. 1798 BEPMC 311: TB-TC ApproachDocument4 pagesCerdeñola, Jane Paula C. 1798 BEPMC 311: TB-TC ApproachGamers HubNo ratings yet

- Combined Pad Foundation: Key Section XXDocument6 pagesCombined Pad Foundation: Key Section XXparth bhujadeNo ratings yet

- CH 2Document7 pagesCH 2华邦盛No ratings yet

- Financial ManagementDocument35 pagesFinancial ManagementNipuna WijeruwanNo ratings yet

- 2009 ReportDocument1 page2009 Reportosem73No ratings yet

- Annual Report2017Document47 pagesAnnual Report2017eliasNo ratings yet

- Wholesale Market Overview: Energy Security Project (ESP)Document10 pagesWholesale Market Overview: Energy Security Project (ESP)Andrey PerevertaevNo ratings yet

- Makeen Energy - Ebook - 6 Profit Eating Flaws in Your Filling System - 8pages - A5Document5 pagesMakeen Energy - Ebook - 6 Profit Eating Flaws in Your Filling System - 8pages - A5shawmailNo ratings yet

- Tarification Western Union PDFDocument3 pagesTarification Western Union PDFGNINESSNo ratings yet

- Can Putinomics Survive 3Document10 pagesCan Putinomics Survive 3AslanZeynalovNo ratings yet

- Little Kaiya European Sales ReportDocument1 pageLittle Kaiya European Sales Reportapi-404356514No ratings yet

- Eu 011 PDFDocument4 pagesEu 011 PDFempower93 empower93No ratings yet

- OSC Business Case For Robi, Bangladesh: 14 Sept, 2012Document24 pagesOSC Business Case For Robi, Bangladesh: 14 Sept, 2012Kr RavindraNo ratings yet

- Assignment IMB2020024 IMB2020036Document8 pagesAssignment IMB2020024 IMB2020036Nirbhay Kumar MishraNo ratings yet

- Air Condition Size Calculator (1.1.19)Document5 pagesAir Condition Size Calculator (1.1.19)Costy45No ratings yet

- Main Trends in International MigrationDocument42 pagesMain Trends in International MigrationNina KondićNo ratings yet

- Unlocking Esg Opportunies Explore How Esg Impacts enDocument18 pagesUnlocking Esg Opportunies Explore How Esg Impacts enSajid KhanNo ratings yet

- Liquidity in The Banking SystemDocument2 pagesLiquidity in The Banking SystemPovon Chandra SutradarNo ratings yet

- Tesla For Supply ChainDocument65 pagesTesla For Supply Chain趙坤信No ratings yet

- Buildu Office Layout1Document1 pageBuildu Office Layout1Mary Francine DoctoNo ratings yet

- Stock Market Indicators: S&P 500 Buybacks & Dividends: Yardeni Research, IncDocument11 pagesStock Market Indicators: S&P 500 Buybacks & Dividends: Yardeni Research, IncchristiansmilawNo ratings yet

- QL PWH Pwh2 200 100 380 400 150 320 600 200 250 800 250 180 1000 290 100Document2 pagesQL PWH Pwh2 200 100 380 400 150 320 600 200 250 800 250 180 1000 290 100Eduardo Carrera Enesto ArenasNo ratings yet

- 026 Exercise-Part-FourDocument7 pages026 Exercise-Part-FourMi TvNo ratings yet

- T C M E R U S: HE Olombian Onetary AND Xchange Egime Nder TressDocument13 pagesT C M E R U S: HE Olombian Onetary AND Xchange Egime Nder Tressapi-26091012No ratings yet

- Chapter4 5 LectureNotes (Rev02152011)Document76 pagesChapter4 5 LectureNotes (Rev02152011)Cazuto LandNo ratings yet

- Common Size Statement, Comparative Balance SheetDocument5 pagesCommon Size Statement, Comparative Balance SheetshubhcplNo ratings yet

- U M ' E U: Nderstanding Exico S Conomic NderperformanceDocument21 pagesU M ' E U: Nderstanding Exico S Conomic NderperformanceFungsional PenilaiNo ratings yet

- Tugas 4 Tpai - Kelompok 1Document21 pagesTugas 4 Tpai - Kelompok 1Fungsional PenilaiNo ratings yet

- Investment ExamplesDocument25 pagesInvestment Exampleschethan626No ratings yet

- Regulatory Approaches To The Tokenisation of AssetsDocument56 pagesRegulatory Approaches To The Tokenisation of AssetsFungsional Penilai0% (1)

- Mexico: OECD Economic SurveysDocument46 pagesMexico: OECD Economic SurveysFungsional PenilaiNo ratings yet

- Mexico 2019 OECD Economic Survey OverviewDocument80 pagesMexico 2019 OECD Economic Survey OverviewFungsional PenilaiNo ratings yet

- EEI2019 Mexico enDocument9 pagesEEI2019 Mexico enFungsional PenilaiNo ratings yet

- Library of Congress - Federal Research Division Country Profile: Mexico, July 2008Document28 pagesLibrary of Congress - Federal Research Division Country Profile: Mexico, July 2008Izzum PatifoNo ratings yet

- Mexico - OECD DataDocument11 pagesMexico - OECD DataFungsional PenilaiNo ratings yet

- The COVID-19 Crisis and Banking System Resilience: Simulation of Losses On Non-Performing Loans and Policy ImplicationsDocument52 pagesThe COVID-19 Crisis and Banking System Resilience: Simulation of Losses On Non-Performing Loans and Policy ImplicationsFungsional PenilaiNo ratings yet

- Cross-Country Analysis - Bringing Foundations and Governments CloserDocument20 pagesCross-Country Analysis - Bringing Foundations and Governments CloserFungsional PenilaiNo ratings yet

- Central Bank Digital Currencies in The Interconnected Future - On The LevelDocument6 pagesCentral Bank Digital Currencies in The Interconnected Future - On The LevelFungsional PenilaiNo ratings yet

- The Effects of Wage Flexibility On Activity and Employment in SpainDocument21 pagesThe Effects of Wage Flexibility On Activity and Employment in SpaintutroNo ratings yet

- Test Bank For Financial Markets and Institutions 7th Edition Frederic S MishkinDocument33 pagesTest Bank For Financial Markets and Institutions 7th Edition Frederic S MishkinChristianLeonardqgsm100% (15)

- Don't Let The Euro-Area Crisis Go EastDocument7 pagesDon't Let The Euro-Area Crisis Go EastBruegelNo ratings yet

- Anglo Interim Report 2011Document84 pagesAnglo Interim Report 2011grumpyfeckerNo ratings yet

- Van Hoisington Q3Document6 pagesVan Hoisington Q3ZerohedgeNo ratings yet

- Orbe Brazil Fund - Dec2012Document7 pagesOrbe Brazil Fund - Dec2012José Enrique MorenoNo ratings yet

- 2022 12 12 Global Debt MonitorDocument7 pages2022 12 12 Global Debt MonitorGulboddin MuradiNo ratings yet

- Sharekhan's Research Report On JSW Steel-JSW-Steel-26-03-2021-khanDocument10 pagesSharekhan's Research Report On JSW Steel-JSW-Steel-26-03-2021-khansaran21No ratings yet

- Chapter 8-1 PDFDocument12 pagesChapter 8-1 PDFkingme157No ratings yet

- Emerging Trends in US Real EstateDocument102 pagesEmerging Trends in US Real EstateShreePanickerNo ratings yet

- Zurich Insurance Malaysia Investment-Linked Foreign Edge FundsDocument39 pagesZurich Insurance Malaysia Investment-Linked Foreign Edge Fundsnantah2299No ratings yet

- Still Searching For Optimal Capital StructureDocument26 pagesStill Searching For Optimal Capital Structureserpent222No ratings yet

- Stock Market Crash Survival GuideDocument18 pagesStock Market Crash Survival GuideFlorian MlNo ratings yet

- ECO4199 - SyllabusDocument11 pagesECO4199 - SyllabusKareemNo ratings yet

- T&T Construction Market Survey 2021Document72 pagesT&T Construction Market Survey 2021Fedir Mieshkov100% (2)

- Cwo Citations and BibliographyDocument60 pagesCwo Citations and BibliographyMark AngeloNo ratings yet

- 04 Financial CrisesDocument54 pages04 Financial Crisesheh92No ratings yet

- Tatas To Take Complete Control of Airasia India: Bharti, Bajaj, Rilgroupstop M-CapchartsDocument12 pagesTatas To Take Complete Control of Airasia India: Bharti, Bajaj, Rilgroupstop M-CapchartsGodha KiranaNo ratings yet

- The Scotts Miracle-Gro Company, Q4 2022 Earnings Call, Nov 02, 2022Document23 pagesThe Scotts Miracle-Gro Company, Q4 2022 Earnings Call, Nov 02, 2022Cesar AugustoNo ratings yet

- Weight Watchers Business Plan 2019Document71 pagesWeight Watchers Business Plan 2019mhetfield100% (1)

- Banking Crisis Memos 250209Document262 pagesBanking Crisis Memos 250209mainman1010100% (1)

- Fragmentation and Monetary Policy in The Euro AreaDocument31 pagesFragmentation and Monetary Policy in The Euro AreaAdolfNo ratings yet

- Global Economic OutlookDocument164 pagesGlobal Economic OutlookAnnieSmithNo ratings yet

- Assignment of ET NEWS ECO3Document72 pagesAssignment of ET NEWS ECO3SakshiNo ratings yet

- Michael Woodford 2010 Financial Intermediation and Macroeconomic AnalysisDocument25 pagesMichael Woodford 2010 Financial Intermediation and Macroeconomic AnalysisOscar Neira CuadraNo ratings yet

- Mckinsey Report October 2012Document52 pagesMckinsey Report October 2012manharlkoNo ratings yet

- 2011 Equity Derivatives OutlookDocument70 pages2011 Equity Derivatives OutlookleetNo ratings yet

- RES Essay Competition 2014 Judges Report & Winning EssaysDocument38 pagesRES Essay Competition 2014 Judges Report & Winning EssaysAxelNo ratings yet

- Centrum Private Credit Fund - Annual NewsLetterDocument17 pagesCentrum Private Credit Fund - Annual NewsLettersuraj211198No ratings yet

- BCG Back To MesopotamiaDocument15 pagesBCG Back To MesopotamiaZerohedgeNo ratings yet

- Finance Basics (HBR 20-Minute Manager Series)From EverandFinance Basics (HBR 20-Minute Manager Series)Rating: 4.5 out of 5 stars4.5/5 (32)

- These are the Plunderers: How Private Equity Runs—and Wrecks—AmericaFrom EverandThese are the Plunderers: How Private Equity Runs—and Wrecks—AmericaRating: 4.5 out of 5 stars4.5/5 (14)

- The Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingFrom EverandThe Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingRating: 4.5 out of 5 stars4.5/5 (17)

- Value: The Four Cornerstones of Corporate FinanceFrom EverandValue: The Four Cornerstones of Corporate FinanceRating: 4.5 out of 5 stars4.5/5 (18)

- The Caesars Palace Coup: How a Billionaire Brawl Over the Famous Casino Exposed the Power and Greed of Wall StreetFrom EverandThe Caesars Palace Coup: How a Billionaire Brawl Over the Famous Casino Exposed the Power and Greed of Wall StreetRating: 5 out of 5 stars5/5 (2)

- Ready, Set, Growth hack:: A beginners guide to growth hacking successFrom EverandReady, Set, Growth hack:: A beginners guide to growth hacking successRating: 4.5 out of 5 stars4.5/5 (93)

- Venture Deals, 4th Edition: Be Smarter than Your Lawyer and Venture CapitalistFrom EverandVenture Deals, 4th Edition: Be Smarter than Your Lawyer and Venture CapitalistRating: 4.5 out of 5 stars4.5/5 (73)

- Summary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisFrom EverandSummary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisRating: 5 out of 5 stars5/5 (6)

- Joy of Agility: How to Solve Problems and Succeed SoonerFrom EverandJoy of Agility: How to Solve Problems and Succeed SoonerRating: 4 out of 5 stars4/5 (1)

- 7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelFrom Everand7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelNo ratings yet

- Financial Risk Management: A Simple IntroductionFrom EverandFinancial Risk Management: A Simple IntroductionRating: 4.5 out of 5 stars4.5/5 (7)

- Financial Modeling and Valuation: A Practical Guide to Investment Banking and Private EquityFrom EverandFinancial Modeling and Valuation: A Practical Guide to Investment Banking and Private EquityRating: 4.5 out of 5 stars4.5/5 (4)

- The Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursFrom EverandThe Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursRating: 4.5 out of 5 stars4.5/5 (8)

- Burn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialFrom EverandBurn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialRating: 4.5 out of 5 stars4.5/5 (32)

- Startup CEO: A Field Guide to Scaling Up Your Business (Techstars)From EverandStartup CEO: A Field Guide to Scaling Up Your Business (Techstars)Rating: 4.5 out of 5 stars4.5/5 (4)

- Mastering Private Equity: Transformation via Venture Capital, Minority Investments and BuyoutsFrom EverandMastering Private Equity: Transformation via Venture Capital, Minority Investments and BuyoutsNo ratings yet

- How to Measure Anything: Finding the Value of Intangibles in BusinessFrom EverandHow to Measure Anything: Finding the Value of Intangibles in BusinessRating: 3.5 out of 5 stars3.5/5 (4)

- Financial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanFrom EverandFinancial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanRating: 4.5 out of 5 stars4.5/5 (79)

- 2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNFrom Everand2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNRating: 4.5 out of 5 stars4.5/5 (3)

- Burn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialFrom EverandBurn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialNo ratings yet

- The Synergy Solution: How Companies Win the Mergers and Acquisitions GameFrom EverandThe Synergy Solution: How Companies Win the Mergers and Acquisitions GameNo ratings yet

- Creating Shareholder Value: A Guide For Managers And InvestorsFrom EverandCreating Shareholder Value: A Guide For Managers And InvestorsRating: 4.5 out of 5 stars4.5/5 (8)

- Value: The Four Cornerstones of Corporate FinanceFrom EverandValue: The Four Cornerstones of Corporate FinanceRating: 5 out of 5 stars5/5 (2)