You might also like

- Schaum's Outline of Basic Business Mathematics, 2edFrom EverandSchaum's Outline of Basic Business Mathematics, 2edRating: 5 out of 5 stars5/5 (1)

- Business Proposal For Fish Farming 3Document21 pagesBusiness Proposal For Fish Farming 3D J Ben Uzee100% (9)

- Business Phrasal VerbsDocument127 pagesBusiness Phrasal VerbsTiago Cuba100% (2)

- Marilyn Victorio-Aquino vs. Pacific Plans, Inc. and Mamerto A. Marcelo, JR DIGESTDocument4 pagesMarilyn Victorio-Aquino vs. Pacific Plans, Inc. and Mamerto A. Marcelo, JR DIGESTroquesa buray100% (1)

- Auditing and AssuranceDocument509 pagesAuditing and AssuranceSrinivasa Rao Bandlamudi80% (10)

- Umali Vs CA DigestDocument2 pagesUmali Vs CA DigestSarah Jane Fabricante Behiga100% (3)

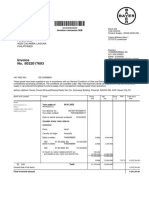

- Invoice No. 8032017603: Bayer Cropscience Inc. 3rd Flr. Bayer House PO Box 4600 4028 Calamba Laguna PhilippinesDocument2 pagesInvoice No. 8032017603: Bayer Cropscience Inc. 3rd Flr. Bayer House PO Box 4600 4028 Calamba Laguna PhilippinesGlezilda LoberianoNo ratings yet

- Financial Performance AnalysisDocument17 pagesFinancial Performance AnalysisIzza Felisilda100% (1)

- Financial AnalysisDocument9 pagesFinancial Analysisgem paolo lagranaNo ratings yet

- Stock Market Technical IndicatorDocument16 pagesStock Market Technical IndicatorRahul MalhotraNo ratings yet

- ITC Financial AnalysisDocument21 pagesITC Financial AnalysisDeepak ChandekarNo ratings yet

- Credit Memo For Gas Authority of IndiaDocument15 pagesCredit Memo For Gas Authority of IndiaKrina ShahNo ratings yet

- Bank of BarodaDocument22 pagesBank of BarodaShivane SivakumarNo ratings yet

- Working File - SIMDocument7 pagesWorking File - SIMmaica G.No ratings yet

- DG Khan Cement Financial StatementsDocument8 pagesDG Khan Cement Financial StatementsAsad BumbiaNo ratings yet

- HORIZON Analytical Procedure AppendixDocument5 pagesHORIZON Analytical Procedure AppendixWinny PoeNo ratings yet

- Oil and Natural Gas CorporationDocument43 pagesOil and Natural Gas CorporationNishant SharmaNo ratings yet

- Daniel John Gabriel FarDocument9 pagesDaniel John Gabriel FarJohn Gabriel DanielNo ratings yet

- Assingment SCM SEM4 - 1Document17 pagesAssingment SCM SEM4 - 1KARTHIYAENI VNo ratings yet

- Financial Modelling ExcelDocument6 pagesFinancial Modelling ExcelAanchal MahajanNo ratings yet

- Ratios and AnalDocument38 pagesRatios and AnalAbhishekKothiaJainNo ratings yet

- PHILEX - V and H AnalysisDocument8 pagesPHILEX - V and H AnalysisHilario, Jana Rizzette C.No ratings yet

- RelianceDocument2 pagesRelianceAADHYA KHANNANo ratings yet

- Ha GSMDocument1 pageHa GSMVenus PalmencoNo ratings yet

- FMUE Group Assignment - Group 4 - Section B2CDDocument42 pagesFMUE Group Assignment - Group 4 - Section B2CDyash jhunjhunuwalaNo ratings yet

- Hexaware Valuation - Group 3 - Sec-ADocument50 pagesHexaware Valuation - Group 3 - Sec-ARahulTiwariNo ratings yet

- FinShiksha Maruti Suzuki UnsolvedDocument12 pagesFinShiksha Maruti Suzuki UnsolvedGANESH JAINNo ratings yet

- FsaDocument13 pagesFsaday6 favorite, loveNo ratings yet

- MaricoDocument13 pagesMaricoRitesh KhobragadeNo ratings yet

- Horizontal AnalysisDocument6 pagesHorizontal AnalysisjohhanaNo ratings yet

- DCF TVSDocument17 pagesDCF TVSSunilNo ratings yet

- UBL Analysis 2018Document4 pagesUBL Analysis 2018Zara ImranNo ratings yet

- sw-1662556454-TANZANIA INSURANCE QUARTERLY PERFORMANCE STATISTICSDocument12 pagessw-1662556454-TANZANIA INSURANCE QUARTERLY PERFORMANCE STATISTICSGEAT MWAISWELONo ratings yet

- New Microsoft Office Excel WorksheetDocument1 pageNew Microsoft Office Excel WorksheetManan SuchakNo ratings yet

- Tata Steel Valuation by BKMNDocument12 pagesTata Steel Valuation by BKMNKp PatelNo ratings yet

- Apollo Hospitals Enterprise LimitedDocument10 pagesApollo Hospitals Enterprise LimitedHemendra GuptaNo ratings yet

- NilkamalDocument14 pagesNilkamalNandish KothariNo ratings yet

- Asian PaintsDocument14 pagesAsian PaintsBiswajit BNo ratings yet

- Fra Wipro AnalysisDocument17 pagesFra Wipro AnalysisApoorv SrivastavaNo ratings yet

- Balance Sheet ParticularsDocument17 pagesBalance Sheet Particularspranav sarawagiNo ratings yet

- Financial Statement: Statement of Cash FlowsDocument6 pagesFinancial Statement: Statement of Cash FlowsdanyalNo ratings yet

- Swot Analysis I. Strenghts: WeaknessesDocument5 pagesSwot Analysis I. Strenghts: WeaknessesNiveditha MNo ratings yet

- Class Work Outs - FSA - MBF2Document67 pagesClass Work Outs - FSA - MBF2Shubham MukherjeeNo ratings yet

- Ratio Analysis of Asian PaintsDocument52 pagesRatio Analysis of Asian PaintsM43CherryAroraNo ratings yet

- Corporate Accounting CIA1BDocument10 pagesCorporate Accounting CIA1Bprince chaudharyNo ratings yet

- Illustration Acc FMDocument22 pagesIllustration Acc FMHEMACNo ratings yet

- Tvs Motor 2019 2018 2017 2016 2015Document108 pagesTvs Motor 2019 2018 2017 2016 2015Rima ParekhNo ratings yet

- Bacolod, Adinrane P. Bsba Finman IiiDocument25 pagesBacolod, Adinrane P. Bsba Finman IiichenlyNo ratings yet

- Oka Corporation BHDDocument3 pagesOka Corporation BHDFagbile TomiwaNo ratings yet

- 1Document1 page1Saray MorenoNo ratings yet

- Three Statement ModelDocument9 pagesThree Statement ModelAnkit SharmaNo ratings yet

- BF1 Package Ratios ForecastingDocument16 pagesBF1 Package Ratios ForecastingBilal Javed JafraniNo ratings yet

- Comparative Income Statement For The Year 17-18 & 18-19 Profit & Loss - Reliance Industries LTDDocument23 pagesComparative Income Statement For The Year 17-18 & 18-19 Profit & Loss - Reliance Industries LTDManan Suchak100% (1)

- Accounts Cia: Submitted By: RISHIKESH DHIR (1923649) PARKHI GUPTA (1923643)Document12 pagesAccounts Cia: Submitted By: RISHIKESH DHIR (1923649) PARKHI GUPTA (1923643)RISHIKESH DHIR 1923649No ratings yet

- Mohammed Ameen PG23174 (Britannia Financial Modelling Assignment)Document20 pagesMohammed Ameen PG23174 (Britannia Financial Modelling Assignment)mameen2906No ratings yet

- Jothikrishna AFD ProjectDocument34 pagesJothikrishna AFD ProjectDebayanNo ratings yet

- Jothikrishna AFD ProjectDocument32 pagesJothikrishna AFD ProjectDebayanNo ratings yet

- Balance Sheet (Crore)Document10 pagesBalance Sheet (Crore)MOHAMMED ARBAZ ABBASNo ratings yet

- Ratio Analysis of Over The Last 5 Years: Power Grid Corporation of India LTDDocument9 pagesRatio Analysis of Over The Last 5 Years: Power Grid Corporation of India LTDKrishna NimmakuriNo ratings yet

- Titan Company TemplateDocument18 pagesTitan Company Templatesejal aroraNo ratings yet

- Rs PPS 28.5 Crores # Shares 1025.93 Crores Market Cap 29,239.01 Crores Cash 5,245.61 Crores Debt 25,364.97 Crores EV 49,358.37Document6 pagesRs PPS 28.5 Crores # Shares 1025.93 Crores Market Cap 29,239.01 Crores Cash 5,245.61 Crores Debt 25,364.97 Crores EV 49,358.37priyanshu14No ratings yet

- FM FS For GlobeDocument5 pagesFM FS For GlobeIngrid garingNo ratings yet

- Ambuja Cements: Profit & Loss AccountDocument15 pagesAmbuja Cements: Profit & Loss Accountwritik sahaNo ratings yet

- Lecture-3 & 4 - Common Size and Comparative AnalysisDocument28 pagesLecture-3 & 4 - Common Size and Comparative AnalysissanyaNo ratings yet

- D489 Abhishek JSWphase 2Document44 pagesD489 Abhishek JSWphase 2Yash KalaNo ratings yet

- Horizontal Vertical Ratio Analysis Problem Soln 16.04.2013Document15 pagesHorizontal Vertical Ratio Analysis Problem Soln 16.04.2013Ojas MaheshwaryNo ratings yet

- Unconsolidated Balance Sheet: As at December 31, 2009 Horizontal Analysis Assets Rs. (I/D) %Document4 pagesUnconsolidated Balance Sheet: As at December 31, 2009 Horizontal Analysis Assets Rs. (I/D) %syedaermaNo ratings yet

- D0683SP Ans2Document18 pagesD0683SP Ans2Tanmay SanchetiNo ratings yet

- Tuntay'sDocument3 pagesTuntay'sLA AlmznNo ratings yet

- PDFDocument22 pagesPDFnylibr100% (1)

- 1366187953binder2Document33 pages1366187953binder2CoolerAdsNo ratings yet

- Stephanie Schneider BK 11 Filing 20-22398, (D.E. 36-4)Document165 pagesStephanie Schneider BK 11 Filing 20-22398, (D.E. 36-4)larry-612445No ratings yet

- Compendium Petitioner AnonymousDocument105 pagesCompendium Petitioner Anonymouspratham mohantyNo ratings yet

- 2012 - Knechel - Non Audit Services and Knowledge Spillovers Evidence From New Zealand PDFDocument22 pages2012 - Knechel - Non Audit Services and Knowledge Spillovers Evidence From New Zealand PDFahmed sharkasNo ratings yet

- Macedonia (Major Banks)Document8 pagesMacedonia (Major Banks)zwrkNo ratings yet

- No Reciept: Jeffrey: GeneratorDocument6 pagesNo Reciept: Jeffrey: GeneratorEJ BenalayoNo ratings yet

- Cost Accumulation For Job-Shop & Batch Production OperationsDocument60 pagesCost Accumulation For Job-Shop & Batch Production Operationstrillion5No ratings yet

- Abbott Annual Report - WebsiteDocument96 pagesAbbott Annual Report - WebsiteFast SwiftNo ratings yet

- Candles UnderstandingDocument12 pagesCandles Understandingsalo saloNo ratings yet

- Punjabi University Patiala FM Assignment - N BDocument8 pagesPunjabi University Patiala FM Assignment - N BVishvesh GargNo ratings yet

- Audit and Internal ReviewDocument6 pagesAudit and Internal Reviewkhengmai100% (1)

- McDonald V Tezos 12/13/17 ComplaintDocument42 pagesMcDonald V Tezos 12/13/17 ComplaintcryptosweepNo ratings yet

- Glorvina Constant Plea AgreementDocument12 pagesGlorvina Constant Plea AgreementmtuccittoNo ratings yet

- Buyback ShareDocument12 pagesBuyback SharemansiaroraskyNo ratings yet

- Mutual Funds - Concept: Mutual Fund Operation Flow ChartDocument17 pagesMutual Funds - Concept: Mutual Fund Operation Flow ChartAnkit ModaniNo ratings yet

- Paper 14Document129 pagesPaper 14dinesh kumarNo ratings yet

- Chapter 14Document24 pagesChapter 14Monal PatelNo ratings yet

- .SEM-3 and 4 (New) 2019 PDFDocument86 pages.SEM-3 and 4 (New) 2019 PDFKrunal PawarNo ratings yet

- BoatDocument2 pagesBoatSreeranjPrakashNo ratings yet

- IAS 2 - InventoriesDocument17 pagesIAS 2 - InventoriesraopraniNo ratings yet