You might also like

- Weekly Ship Recycling Report Week 38pdfDocument7 pagesWeekly Ship Recycling Report Week 38pdfSandesh Tukaram GhandatNo ratings yet

- Weekly Ship Recycling Report W40 21Document7 pagesWeekly Ship Recycling Report W40 21Sandesh Tukaram GhandatNo ratings yet

- Weekly Ship Recycling Report 33Document7 pagesWeekly Ship Recycling Report 33Sandesh Tukaram GhandatNo ratings yet

- Weekly Ship Recycling Report WEEK35Document7 pagesWeekly Ship Recycling Report WEEK35Sandesh Tukaram GhandatNo ratings yet

- Weekly Ship Recycling ReportDocument7 pagesWeekly Ship Recycling ReportMohammed FaruqueNo ratings yet

- Weekly Ship Recycling Report WEEK37Document7 pagesWeekly Ship Recycling Report WEEK37Sandesh Tukaram GhandatNo ratings yet

- Weekly-Ship-Recycling-Report W42 - 21Document7 pagesWeekly-Ship-Recycling-Report W42 - 21Sandesh Tukaram GhandatNo ratings yet

- Weekly-Ship-Recycling-Report W41 - 21Document7 pagesWeekly-Ship-Recycling-Report W41 - 21Sandesh Tukaram GhandatNo ratings yet

- Weekly-Ship-Recycling-Report 16 September 2022Document9 pagesWeekly-Ship-Recycling-Report 16 September 2022THNo ratings yet

- ShippingSectorReport-29 Sep 2010Document95 pagesShippingSectorReport-29 Sep 2010ureachmadhu3042No ratings yet

- Coal Trader International: Asian Thermal Coal Prices Edge Lower On Demand Pullback From China BuyersDocument17 pagesCoal Trader International: Asian Thermal Coal Prices Edge Lower On Demand Pullback From China BuyersClief SurentuNo ratings yet

- Report 200Document6 pagesReport 200Sandesh GhandatNo ratings yet

- Report 202Document6 pagesReport 202Sandesh GhandatNo ratings yet

- 2022-3964 Pulsation DampenersDocument1 page2022-3964 Pulsation DampenersZakNo ratings yet

- AIDA-COSTA Ghilizan Marian 3rd EngineerDocument4 pagesAIDA-COSTA Ghilizan Marian 3rd EngineerStefan MarianNo ratings yet

- International Coal Prices: Port Port (In Kcal) GCV ($/MT) Freight ($/MT) (RS/MT)Document4 pagesInternational Coal Prices: Port Port (In Kcal) GCV ($/MT) Freight ($/MT) (RS/MT)SANDESH GHANDATNo ratings yet

- Intermodal Report Week 26 2021Document8 pagesIntermodal Report Week 26 2021Nguyen Le Thu HaNo ratings yet

- Monitoring Kuat Tekan UPDATEDocument45 pagesMonitoring Kuat Tekan UPDATERifky RaffaNo ratings yet

- Master Booking 09-05-2022Document2 pagesMaster Booking 09-05-2022Saiful Idham Bin Mohd HusainNo ratings yet

- Coalfax 6 Sep 2019Document4 pagesCoalfax 6 Sep 2019Muhammet Ali VELİOĞLUNo ratings yet

- Compass Maritime Weekly Market ReportDocument6 pagesCompass Maritime Weekly Market ReportJoel SegoviaNo ratings yet

- Demurrage & MiscDocument4 pagesDemurrage & Misctanvirmahabub IslamNo ratings yet

- SeptemberDocument2 pagesSeptemberNora Aircond channelNo ratings yet

- DMT 219004 AbDocument518 pagesDMT 219004 AbCiprian MariusNo ratings yet

- Road EquipmentDocument2 pagesRoad EquipmentL V Laxmipathi RaoNo ratings yet

- Bank Invoice 0105 REVISEDDocument1 pageBank Invoice 0105 REVISEDFarah GoganNo ratings yet

- Purachase RequisitionDocument38 pagesPurachase RequisitionSA WOWNo ratings yet

- Lube Sale - Barrels (September 2019) : Date Client Details Product Packing Size Quantity Purchase Price (INR)Document4 pagesLube Sale - Barrels (September 2019) : Date Client Details Product Packing Size Quantity Purchase Price (INR)Najam KhanNo ratings yet

- Chief Engineer Tanker FleetDocument3 pagesChief Engineer Tanker FleetYuryNo ratings yet

- Chief Engineer Tanker FleetDocument3 pagesChief Engineer Tanker FleetYuryNo ratings yet

- Advanced Market Report Week 4Document10 pagesAdvanced Market Report Week 4Mai PhamNo ratings yet

- 72% L. Oliva On Jan 23rd 2020 Montanaso Lombardo: INOXFUCINE SPA (Conaco Division)Document2 pages72% L. Oliva On Jan 23rd 2020 Montanaso Lombardo: INOXFUCINE SPA (Conaco Division)DonArmanNo ratings yet

- Us Coal Down Fall Start 1637121506Document15 pagesUs Coal Down Fall Start 1637121506Abdillah AkbarNo ratings yet

- WK 41 - 20 Carriers - S&P Market ReportDocument2 pagesWK 41 - 20 Carriers - S&P Market ReportFotini HalouvaNo ratings yet

- Bom and Costing For Walvoil - 6.4.2022Document14 pagesBom and Costing For Walvoil - 6.4.2022aryankhati9No ratings yet

- Ict 20231115Document18 pagesIct 20231115Budi HeryantoNo ratings yet

- Catalog Product Kapal Pt. Prime GlobalDocument16 pagesCatalog Product Kapal Pt. Prime GloballinkwidodoNo ratings yet

- Report 05 01 2024Document3 pagesReport 05 01 2024bill duanNo ratings yet

- Advanced Market Report Week 44Document10 pagesAdvanced Market Report Week 44Mai PhamNo ratings yet

- Job Information: Job No Sheet No RevDocument3 pagesJob Information: Job No Sheet No RevAlexander SNo ratings yet

- Group Fleet List and Contact Details: Global BWDocument1 pageGroup Fleet List and Contact Details: Global BWTEJAS SARMANo ratings yet

- Coal Trader International: Asian Thermal Coal Prices Swing Lower On Tepid Buying ResponseDocument1 pageCoal Trader International: Asian Thermal Coal Prices Swing Lower On Tepid Buying ResponseClief SurentuNo ratings yet

- LNG & LPG Shipping Fundamentals PDFDocument15 pagesLNG & LPG Shipping Fundamentals PDFRafi Algawi100% (1)

- Updated Information Noted in Bold Print: Diamond Offshore Drilling, Inc. Rig Status Report February 10, 2020Document2 pagesUpdated Information Noted in Bold Print: Diamond Offshore Drilling, Inc. Rig Status Report February 10, 2020Sipa1109No ratings yet

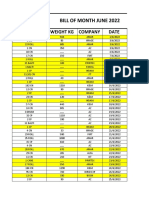

- Bill June 2022Document8 pagesBill June 2022SanaNo ratings yet

- 11.04.20 FSR-vFinalDocument4 pages11.04.20 FSR-vFinalفؤاد ابوزيدNo ratings yet

- Invoice: Dolsey LTD 863 West 44Th Street NORFOLK, VA 23508Document1 pageInvoice: Dolsey LTD 863 West 44Th Street NORFOLK, VA 23508Chris FendiNo ratings yet

- Headwise Expenses Format OCT - 2019MMMMMDocument8 pagesHeadwise Expenses Format OCT - 2019MMMMMtearstainedheartNo ratings yet

- Indonesia Offshore OutlookDocument1 pageIndonesia Offshore OutlookLaras RyuNo ratings yet

- Lampiran 10 G Biaya / Bulan Biaya Fuel Oprasional AlatDocument1 pageLampiran 10 G Biaya / Bulan Biaya Fuel Oprasional AlatFaishol Amir VR-BangkalanNo ratings yet

- ALNOORDocument8 pagesALNOORgulaabrai95No ratings yet

- WK 42 - 20 CARRIERS - S&P MARKET REPORTdraftDocument2 pagesWK 42 - 20 CARRIERS - S&P MARKET REPORTdraftFotini HalouvaNo ratings yet

- U Nit of M Ea Su Re Quantity Ordered Quantity OpenDocument2 pagesU Nit of M Ea Su Re Quantity Ordered Quantity OpenSharad DunghavNo ratings yet

- Co 8910Document1 pageCo 8910shanNo ratings yet

- Dbs2009jun9asia Dry BulkDocument12 pagesDbs2009jun9asia Dry BulkmarineinfoNo ratings yet

- Advanced Market Report Week 2Document10 pagesAdvanced Market Report Week 2Mai PhamNo ratings yet

- THE DETERMINANTS OF PRICES OF NEWBUILDING IN THE VERY LARGE CRUDE CARRIERS (VLCC) SECTORFrom EverandTHE DETERMINANTS OF PRICES OF NEWBUILDING IN THE VERY LARGE CRUDE CARRIERS (VLCC) SECTORNo ratings yet

- Giignl The LNG Industry 2008Document26 pagesGiignl The LNG Industry 2008Sandesh Tukaram GhandatNo ratings yet

- Cygnus Energy LNG News Weekly 27th November 20Document10 pagesCygnus Energy LNG News Weekly 27th November 20Sandesh Tukaram GhandatNo ratings yet

- Cygnus Energy LNG News Weekly 29th October 2021Document10 pagesCygnus Energy LNG News Weekly 29th October 2021Sandesh Tukaram GhandatNo ratings yet

- Cygnus Energy LNG News Weekly 17th SEPTEMBER 2021Document14 pagesCygnus Energy LNG News Weekly 17th SEPTEMBER 2021Sandesh Tukaram GhandatNo ratings yet

- Cygnus Energy LNG News Weekly 12th Feb 2021Document19 pagesCygnus Energy LNG News Weekly 12th Feb 2021Sandesh Tukaram GhandatNo ratings yet

- Cygnus Energy LNG News Weekly 23rd April 2021Document15 pagesCygnus Energy LNG News Weekly 23rd April 2021Sandesh Tukaram GhandatNo ratings yet

- Cygnus Energy LNG News Weekly 03rd SEPTEMBER 2021Document16 pagesCygnus Energy LNG News Weekly 03rd SEPTEMBER 2021Sandesh Tukaram GhandatNo ratings yet

- Cygnus Energy LNG News Weekly 21th May 2021Document11 pagesCygnus Energy LNG News Weekly 21th May 2021Sandesh Tukaram GhandatNo ratings yet

- Cygnus Energy LNG News Weekly 26th March 2021Document14 pagesCygnus Energy LNG News Weekly 26th March 2021Sandesh Tukaram GhandatNo ratings yet

- Cygnus Energy LNG News Weekly 26th Feb 2021Document10 pagesCygnus Energy LNG News Weekly 26th Feb 2021Sandesh Tukaram GhandatNo ratings yet

- Cygnus Energy LNG News Weekly 19th Feb 2021Document21 pagesCygnus Energy LNG News Weekly 19th Feb 2021Sandesh Tukaram GhandatNo ratings yet

- Cygnus Energy LNG News Weekly 05th March 2021Document14 pagesCygnus Energy LNG News Weekly 05th March 2021Sandesh Tukaram GhandatNo ratings yet

- Cygnus Energy LNG News Weekly 02nd April 2021Document16 pagesCygnus Energy LNG News Weekly 02nd April 2021Sandesh Tukaram GhandatNo ratings yet

- Cygnus Energy LNG News Weekly 16th April 2021Document14 pagesCygnus Energy LNG News Weekly 16th April 2021Sandesh Tukaram GhandatNo ratings yet

- Cygnus Energy LNG News Weekly 01th October 2021Document22 pagesCygnus Energy LNG News Weekly 01th October 2021Sandesh Tukaram GhandatNo ratings yet

- Cygnus Energy LNG News Weekly 05th February 2021Document15 pagesCygnus Energy LNG News Weekly 05th February 2021Sandesh Tukaram GhandatNo ratings yet

- Cygnus Energy LNG News Weekly 04th June 2021Document20 pagesCygnus Energy LNG News Weekly 04th June 2021Sandesh Tukaram GhandatNo ratings yet

- Cygnus Energy LNG News Weekly 05TH NOVEMBER 2021Document17 pagesCygnus Energy LNG News Weekly 05TH NOVEMBER 2021Sandesh Tukaram GhandatNo ratings yet

- Cygnus Energy LNG News Weekly 11th June 2021Document17 pagesCygnus Energy LNG News Weekly 11th June 2021Sandesh Tukaram GhandatNo ratings yet

- Cygnus Energy LNG News Weekly 18th June 2021Document17 pagesCygnus Energy LNG News Weekly 18th June 2021Sandesh Tukaram GhandatNo ratings yet

- Cygnus Energy LNG News Weekly 10th SEPTEMBER 2021Document16 pagesCygnus Energy LNG News Weekly 10th SEPTEMBER 2021Sandesh Tukaram GhandatNo ratings yet

- Cygnus Energy LNG News Weekly 19th Feb 2021Document21 pagesCygnus Energy LNG News Weekly 19th Feb 2021Sandesh Tukaram GhandatNo ratings yet

- Unit - Ii Currency RulesDocument6 pagesUnit - Ii Currency RulesAmazon BitsNo ratings yet

- X SF STD InvDocument1 pageX SF STD InvABDUL GHAFARNo ratings yet

- Sutlej Cotton Mills Ltd. v. CITDocument18 pagesSutlej Cotton Mills Ltd. v. CITSaksham ShrivastavNo ratings yet

- APPLICATION FORM PHASE-4 Latest 19-11-2022-2Document3 pagesAPPLICATION FORM PHASE-4 Latest 19-11-2022-2Zahara AliNo ratings yet

- E-Statement - ElectricalDocument6 pagesE-Statement - Electricalimrandynamicsolution777No ratings yet

- Projected Profit Rates Feb 2023Document14 pagesProjected Profit Rates Feb 2023adeelNo ratings yet

- PTS FormDocument5 pagesPTS FormAbdullah ShakirNo ratings yet

- Application-Form AwaranDocument4 pagesApplication-Form Awaransuleman shahNo ratings yet

- State Bank of Pakistan: Domestic Markets & Monetary Management DepartmentDocument1 pageState Bank of Pakistan: Domestic Markets & Monetary Management DepartmentMeeroButtNo ratings yet

- ChalanDocument1 pageChalanMohsin AliNo ratings yet

- X SF STD Inv 14Document1 pageX SF STD Inv 14allamaaiou02No ratings yet

- Foreign CurrencyDocument71 pagesForeign CurrencyNoor fatimaNo ratings yet

- Icore 14Document10 pagesIcore 14Dr-Najmunnisa KhanNo ratings yet

- Investment GuideDocument72 pagesInvestment Guideaqibaziz76No ratings yet

- Fxrate 06 06 2023Document2 pagesFxrate 06 06 2023ShohanNo ratings yet

- Important : Allama Iqbal Open University Islamabad Allama Iqbal Open University IslamabadDocument1 pageImportant : Allama Iqbal Open University Islamabad Allama Iqbal Open University IslamabadMuhammad Sohail0% (1)

- JS Bank Swot AnalysisDocument21 pagesJS Bank Swot AnalysisToHeed Shah50% (2)

- DAS ChallanFormDocument1 pageDAS ChallanFormSaim AliNo ratings yet

- Sigma Purchase Order TempDocument2 pagesSigma Purchase Order TempusmanitecNo ratings yet

- 234 Executive Board Meeting of NHADocument33 pages234 Executive Board Meeting of NHAHamid NaveedNo ratings yet

- Invoice: Summary of ChargesDocument2 pagesInvoice: Summary of ChargesSiddique BhattiNo ratings yet

- FINANCIAL STATEMENTS AND H&V ANALYSIS of Shekk PakistanDocument20 pagesFINANCIAL STATEMENTS AND H&V ANALYSIS of Shekk PakistanMaheen GulalaiNo ratings yet

- Energy Crises in Pakistan 26-08-2023 Lecture 1 (Current Affairs)Document5 pagesEnergy Crises in Pakistan 26-08-2023 Lecture 1 (Current Affairs)aqsaNo ratings yet

- English PB 23Document2 pagesEnglish PB 23Sheeraz Rasheed33% (3)

- Pakistani RupeeDocument19 pagesPakistani RupeeScarlett Lewis100% (1)

- Faysal Bank PDFDocument21 pagesFaysal Bank PDFMuzahir Hussain JoyiaNo ratings yet

- Paradox Plan-1 PDFDocument2 pagesParadox Plan-1 PDFSuleman AliNo ratings yet

- IBNS - Journal - Volume 39 Issue 4Document68 pagesIBNS - Journal - Volume 39 Issue 4Aumair MalikNo ratings yet

- 6 Plus Price in Pakistan - Google SearchDocument1 page6 Plus Price in Pakistan - Google SearchZeeshan UmraniNo ratings yet

- Proforma Invoice: 68, Tipu Road, Fauji Towers, Chaklala Cantt. Rawalpindi NTN # 0787426-0Document1 pageProforma Invoice: 68, Tipu Road, Fauji Towers, Chaklala Cantt. Rawalpindi NTN # 0787426-0MUHAMMAD HASAN ANISNo ratings yet