You might also like

- Dividend Policy of Reliance Industries Itd.Document24 pagesDividend Policy of Reliance Industries Itd.rohit280273% (11)

- Dividend Policy of Reliance Industries SwatiDocument24 pagesDividend Policy of Reliance Industries SwatiYashasvi KothariNo ratings yet

- Varun Kumar Project ReportDocument7 pagesVarun Kumar Project Reportvarun kumar Verma100% (1)

- Module 2Document10 pagesModule 2rajiNo ratings yet

- Dividend Is That Portion of Profits of A Company Which Is DistributableDocument25 pagesDividend Is That Portion of Profits of A Company Which Is DistributableCma Pushparaj KulkarniNo ratings yet

- Vivek Project ReportDocument23 pagesVivek Project ReportvivekNo ratings yet

- Dividend DecisionDocument5 pagesDividend DecisionRishika SinghNo ratings yet

- Advance Financial Management Sunday - Cycle 2 Dr. Donatila San JuanDocument5 pagesAdvance Financial Management Sunday - Cycle 2 Dr. Donatila San JuanRonalyn MainitNo ratings yet

- Chapter - 2 Conceptual Framework of DividendDocument36 pagesChapter - 2 Conceptual Framework of DividendMadhavasadasivan PothiyilNo ratings yet

- Assignment: Financial Management: Dividend - MeaningDocument4 pagesAssignment: Financial Management: Dividend - MeaningSiddhant gudwaniNo ratings yet

- Factors Affecting Divident Policy DeciDocument26 pagesFactors Affecting Divident Policy DeciVj AutiNo ratings yet

- RM Assignment-3: Q1. Dividend Policy Can Be Used To Maximize The Wealth of The Shareholder. Explain. AnswerDocument4 pagesRM Assignment-3: Q1. Dividend Policy Can Be Used To Maximize The Wealth of The Shareholder. Explain. AnswerSiddhant gudwaniNo ratings yet

- FM H Chapter 1 0 2Document23 pagesFM H Chapter 1 0 2MOLALIGNNo ratings yet

- Dividend PolicyDocument9 pagesDividend PolicyrutujachoudeNo ratings yet

- Notes of Dividend PolicyDocument16 pagesNotes of Dividend PolicyVineet VermaNo ratings yet

- Types of Divedend PolicyDocument5 pagesTypes of Divedend PolicyPrajakta BhideNo ratings yet

- Impact of Dividend Policy On Value of The Final)Document40 pagesImpact of Dividend Policy On Value of The Final)finesaqibNo ratings yet

- Corporate Finance BasicsDocument27 pagesCorporate Finance BasicsAhimbisibwe BenyaNo ratings yet

- Special Topics - Written ReportDocument5 pagesSpecial Topics - Written ReportMary Maddie JenningsNo ratings yet

- PDF Document CF 4-2Document42 pagesPDF Document CF 4-2Sarath kumar CNo ratings yet

- Unit 18 Dividend Decisions: ObjectivesDocument10 pagesUnit 18 Dividend Decisions: ObjectivesShriniwash MishraNo ratings yet

- Unit - 3: Dividend DecisionDocument34 pagesUnit - 3: Dividend DecisionChethan.sNo ratings yet

- Dividend DecisionzxDocument0 pagesDividend Decisionzxsaravana saravanaNo ratings yet

- Dividend DecisionsDocument32 pagesDividend DecisionstekleyNo ratings yet

- Advanced Financial Management - 20MBAFM306: Department of Management Studies, JNNCE, ShivamoggaDocument16 pagesAdvanced Financial Management - 20MBAFM306: Department of Management Studies, JNNCE, ShivamoggaDrusti M S100% (1)

- Dividend PolicyDocument8 pagesDividend PolicyCaptainVipro YTNo ratings yet

- FM II Chapter 1Document12 pagesFM II Chapter 1Addisu TadesseNo ratings yet

- Unit 5 Financial Management Complete NotesDocument17 pagesUnit 5 Financial Management Complete Notesvaibhav shuklaNo ratings yet

- Dividend Decision by OrganizationsDocument16 pagesDividend Decision by OrganizationsMohitNo ratings yet

- Dividend Policy 1Document56 pagesDividend Policy 1hardika jadav100% (1)

- PDF 1 - DividendDocument11 pagesPDF 1 - Dividendrahul bhilalaNo ratings yet

- Dividend PolicyDocument35 pagesDividend PolicyVic100% (3)

- Major Decisions in Finance ManagementDocument33 pagesMajor Decisions in Finance ManagementNandita ChouhanNo ratings yet

- Different Types of DividendDocument7 pagesDifferent Types of DividendAnshul Mehrotra100% (1)

- 10 Chapter UGLEDocument26 pages10 Chapter UGLEMahek AroraNo ratings yet

- Orion PharmaDocument20 pagesOrion PharmaShamsun NaharNo ratings yet

- Chapter 4 Financial Management IV BbaDocument3 pagesChapter 4 Financial Management IV BbaSuchetana AnthonyNo ratings yet

- Finance Term Paper (Ratio Analysis)Document13 pagesFinance Term Paper (Ratio Analysis)UtshoNo ratings yet

- Unit Iv-1Document8 pagesUnit Iv-1Archi VarshneyNo ratings yet

- Corporate Dividend Policy (L-9)Document39 pagesCorporate Dividend Policy (L-9)Mega capitalmarketNo ratings yet

- FM - Dividend Policy and Dividend Decision Models (Cir On 25.3.2017)Document117 pagesFM - Dividend Policy and Dividend Decision Models (Cir On 25.3.2017)Sarvar PathanNo ratings yet

- Unit - 3 Dividend PolicyDocument8 pagesUnit - 3 Dividend Policyetebark h/michaleNo ratings yet

- Dividend PolicyDocument8 pagesDividend PolicyBhavya GuptaNo ratings yet

- Dividend PolicyDocument26 pagesDividend PolicyAnup Verma100% (1)

- Financial Management II 2020: Aims and Objectives After Completing This Chapter, You Should Have A Good Understanding ofDocument15 pagesFinancial Management II 2020: Aims and Objectives After Completing This Chapter, You Should Have A Good Understanding ofSintu TalefeNo ratings yet

- FM Ii Handout-2Document85 pagesFM Ii Handout-2Fãhâd Õró ÂhmédNo ratings yet

- FM - Dividend Policy and Dividend Decision Models (Cir 18.3.2020)Document129 pagesFM - Dividend Policy and Dividend Decision Models (Cir 18.3.2020)Rohit PanpatilNo ratings yet

- Assignment - VALIDITY OF THE LINTNER MODEL ON MAURITIAN CAPITAL MARKET PDFDocument25 pagesAssignment - VALIDITY OF THE LINTNER MODEL ON MAURITIAN CAPITAL MARKET PDFSamba BahNo ratings yet

- Chapter 6 - Dividend DecisionDocument3 pagesChapter 6 - Dividend DecisionAngelica Joy ManaoisNo ratings yet

- Unit 6Document39 pagesUnit 6Hemanta PahariNo ratings yet

- Dividend Policy2Document21 pagesDividend Policy2Priya UllasNo ratings yet

- Dividend Is The Portion of Earnings Available To Equity Shareholders That Equally (Per Share Bias) Is Distributed Among The ShareholdersDocument21 pagesDividend Is The Portion of Earnings Available To Equity Shareholders That Equally (Per Share Bias) Is Distributed Among The ShareholdersKusum YadavNo ratings yet

- Dividend Ch-1 (Repaired)Document8 pagesDividend Ch-1 (Repaired)mengistuNo ratings yet

- Factors Affecting Dividend PolicyDocument3 pagesFactors Affecting Dividend PolicyAarti TawaNo ratings yet

- Dividend Policy - 072 - MBS - 1st - Year PDFDocument5 pagesDividend Policy - 072 - MBS - 1st - Year PDFRasna ShakyaNo ratings yet

- Corporate Finance MBA20022013Document244 pagesCorporate Finance MBA20022013Ibrahim ShareefNo ratings yet

- ICM Text Book UpdateDocument78 pagesICM Text Book UpdatemariposaNo ratings yet

- FM 5Document10 pagesFM 5Rohini rs nairNo ratings yet

- Dividend Investing: Passive Income and Growth Investing for BeginnersFrom EverandDividend Investing: Passive Income and Growth Investing for BeginnersNo ratings yet

- Dividend Growth Investing: A Step-by-Step Guide to Building a Dividend Portfolio for Early RetirementFrom EverandDividend Growth Investing: A Step-by-Step Guide to Building a Dividend Portfolio for Early RetirementNo ratings yet

- Dividend Investing for Beginners & DummiesFrom EverandDividend Investing for Beginners & DummiesRating: 5 out of 5 stars5/5 (1)

- Cibil RetailDocument14 pagesCibil Retailchristous p kNo ratings yet

- EF5142 - data - 20220331 - 副本Document49 pagesEF5142 - data - 20220331 - 副本dNo ratings yet

- Mba 5500 Integrative Assignment 3 Sap SD Jaye Mcfadden Jason BellDocument10 pagesMba 5500 Integrative Assignment 3 Sap SD Jaye Mcfadden Jason BellJared OkatchNo ratings yet

- Organizational ChartDocument1 pageOrganizational ChartAdrian HilarioNo ratings yet

- Badan Pengurusan Bersama Binjai 8Document4 pagesBadan Pengurusan Bersama Binjai 8JagdieshNo ratings yet

- Practice Discussion QuestionDocument9 pagesPractice Discussion QuestionJam PotutanNo ratings yet

- Room 205Document1 pageRoom 205Hotel EkasNo ratings yet

- Clva 4 OVi 5 P LBEk HSDocument14 pagesClva 4 OVi 5 P LBEk HSpiyush takkarNo ratings yet

- Cooperative BankingDocument13 pagesCooperative BankingwubeNo ratings yet

- Session 5 - Colgate Palmolive India and DaburDocument23 pagesSession 5 - Colgate Palmolive India and DaburxzeekNo ratings yet

- Regulasi Anti Dumping Sebagai UpayaDocument13 pagesRegulasi Anti Dumping Sebagai UpayaNurmadiaNo ratings yet

- Virginia Last Will and Testament: Pursuant To Title 64.2 (Wills, Trusts, and Fiduciaries)Document5 pagesVirginia Last Will and Testament: Pursuant To Title 64.2 (Wills, Trusts, and Fiduciaries)david pohanNo ratings yet

- Genmathattempt 1Document6 pagesGenmathattempt 1John Dexter LanotNo ratings yet

- Promissory Note TemplateDocument1 pagePromissory Note TemplateJhoana Parica FranciscoNo ratings yet

- FIN448-Final-Exam-Fall2020-Review - MCDocument85 pagesFIN448-Final-Exam-Fall2020-Review - MCMay ChenNo ratings yet

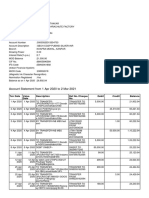

- Account Details and Transaction History: Air Asia SaverDocument4 pagesAccount Details and Transaction History: Air Asia SaverSeema KhanNo ratings yet

- Kelompok 1 - Channel BasicsDocument54 pagesKelompok 1 - Channel BasicsmarioyubileoNo ratings yet

- Airline Passenger Satisfaction Prediction: Sheila Fitria Al'asqalaniDocument22 pagesAirline Passenger Satisfaction Prediction: Sheila Fitria Al'asqalaniAhza AzrNo ratings yet

- MKTG Analysis Toolkit - Situation Analysis - 26.8.2020Document3 pagesMKTG Analysis Toolkit - Situation Analysis - 26.8.2020GAYATRI K SHENOY IPM 2017-22 BatchNo ratings yet

- Fed ExDocument11 pagesFed ExAruzhan UkanovaNo ratings yet

- The Political Power of Finance: The Institute of International Finance in The Greek Debt CrisisDocument26 pagesThe Political Power of Finance: The Institute of International Finance in The Greek Debt Crisisihda0farhatun0nisakNo ratings yet

- MCQ ProductionDocument4 pagesMCQ ProductionSandy AHNo ratings yet

- Inventory Models For Probabilistic Demand:: Cost & Service Trade-OffsDocument41 pagesInventory Models For Probabilistic Demand:: Cost & Service Trade-OffsSakline MinarNo ratings yet

- National Savings and Economic Growth-AnalysisDocument21 pagesNational Savings and Economic Growth-AnalysisOlubunmi SolomonNo ratings yet

- Certificate of Conformity of The Factory Production Control: Notified Body No. 1725 FM Approvals LimitedDocument1 pageCertificate of Conformity of The Factory Production Control: Notified Body No. 1725 FM Approvals LimitedYoul SilvaNo ratings yet

- Investment Banking, 3E: Valuation, Lbos, M&A, and IposDocument3 pagesInvestment Banking, 3E: Valuation, Lbos, M&A, and IposBook SittiwatNo ratings yet

- Aggregate Planning and MRPDocument68 pagesAggregate Planning and MRPJanarthanan Siva KumarNo ratings yet

- Lease TheoryDocument10 pagesLease TheorySyeda AtikNo ratings yet

- IQSK Issue 31 - April - June 2021 Journal EditionDocument50 pagesIQSK Issue 31 - April - June 2021 Journal Editionbenson njihiaNo ratings yet