You might also like

- Capital Budgeting HDFCDocument68 pagesCapital Budgeting HDFCKasiraju Saiprathap43% (7)

- Financial Statement AnalysisDocument6 pagesFinancial Statement AnalysisValtteri Itäranta0% (2)

- Capital Budgeting of Coca ColaDocument7 pagesCapital Budgeting of Coca Colasomyajain2298_345069No ratings yet

- "A Study On Credit Card": (The Plastic Money)Document86 pages"A Study On Credit Card": (The Plastic Money)Gaurav Gaba100% (1)

- British Gas - OldDocument2 pagesBritish Gas - Oldky139396No ratings yet

- 04b Receivables (Part 2)Document6 pages04b Receivables (Part 2)JEFFERSON CUTE100% (1)

- Capital Budgeting Project ReportDocument24 pagesCapital Budgeting Project Reportnishiit92% (12)

- Capital BudgetingDocument68 pagesCapital BudgetingPranay GNo ratings yet

- Corporate Finance: Capital BudgetingDocument17 pagesCorporate Finance: Capital BudgetingpayataNo ratings yet

- Capital Budgeting NotesDocument5 pagesCapital Budgeting NotesDipin LohiyaNo ratings yet

- Ajith ProjectDocument89 pagesAjith ProjectAnonymous MhCdtwxQINo ratings yet

- Scope/Elements: Page - 1Document11 pagesScope/Elements: Page - 1amit2981987No ratings yet

- Need and Importance of Capital BudgetingDocument4 pagesNeed and Importance of Capital BudgetingSrinidhi PnaNo ratings yet

- Managers.: Investment Decisions Are Made by Investors and InvestmentDocument5 pagesManagers.: Investment Decisions Are Made by Investors and InvestmentRe KhanNo ratings yet

- Capital Budjeting NagarjunaDocument73 pagesCapital Budjeting NagarjunaSanthosh Soma100% (2)

- Financial Management Notes SRK UNIT 2Document13 pagesFinancial Management Notes SRK UNIT 2Pruthvi RajNo ratings yet

- Prof. (DR.) Nagendra Kumar Jha: Topic: Concept and Significance of Capital BudgetingDocument3 pagesProf. (DR.) Nagendra Kumar Jha: Topic: Concept and Significance of Capital BudgetingNisha BhardwajNo ratings yet

- Financial ManagementDocument42 pagesFinancial Managementnimala maniNo ratings yet

- Capital Budgeting MeaningDocument13 pagesCapital Budgeting MeaningHarihara PuthiranNo ratings yet

- FM I - CH 6 NoteDocument22 pagesFM I - CH 6 NoteEtsub SamuelNo ratings yet

- A Study On Capital Budgeting.Document15 pagesA Study On Capital Budgeting.Kumar SwamyNo ratings yet

- 8.capital BudgetingDocument82 pages8.capital BudgetingOblivion OblivionNo ratings yet

- Capital BudgetingDocument64 pagesCapital BudgetingNiaz AhmedNo ratings yet

- 19752ipcc FM Vol1 Cp6Document0 pages19752ipcc FM Vol1 Cp6M Waqas PkNo ratings yet

- 54 Capital BudgetingDocument4 pages54 Capital BudgetingCA Gourav JashnaniNo ratings yet

- Abstract CAPITAL BUDGETING UltratechDocument12 pagesAbstract CAPITAL BUDGETING UltratechraghunathreddychallaNo ratings yet

- MFDocument6 pagesMFJS Gowri NandiniNo ratings yet

- Investment Appraisal MethodsDocument15 pagesInvestment Appraisal MethodsFaruk Hossain100% (1)

- 2015@FM I CH 6-Capital BudgetingDocument16 pages2015@FM I CH 6-Capital BudgetingALEMU TADESSENo ratings yet

- Capital BudgetingDocument50 pagesCapital Budgetinghimanshujoshi7789No ratings yet

- Unit 5 EEFMDocument9 pagesUnit 5 EEFMGayathri Bhupathi rajuNo ratings yet

- CH 5 6 Capital BudgetingDocument94 pagesCH 5 6 Capital BudgetingNikita AggarwalNo ratings yet

- Chapter9 Financial Management BusinessStudies Class12 LearnKaroClassesDocument53 pagesChapter9 Financial Management BusinessStudies Class12 LearnKaroClassesUpendra RajagopalanNo ratings yet

- Capital BudgetingDocument38 pagesCapital BudgetingTaha MadniNo ratings yet

- Capital Budgeting PDFDocument10 pagesCapital Budgeting PDFSenthil KumarNo ratings yet

- FM 1 CH 4 (Lti) My MLC ExtDocument19 pagesFM 1 CH 4 (Lti) My MLC ExtMELAT ROBELNo ratings yet

- Capital BudgetingDocument93 pagesCapital BudgetingKhadar100% (3)

- KC Financial DecisionsDocument111 pagesKC Financial DecisionsSatish PatilNo ratings yet

- Unit 03Document69 pagesUnit 03Shah Maqsumul Masrur TanviNo ratings yet

- Capital BudgetingDocument65 pagesCapital Budgetingarjunmba119624No ratings yet

- Capital BudgetingDocument35 pagesCapital Budgetinggkvimal nathan100% (3)

- Chapter-3: Capital Budgeting Chapter-Three Capital Budgeting/Investment Decision 3.1. Definition of Capital BudgetingDocument12 pagesChapter-3: Capital Budgeting Chapter-Three Capital Budgeting/Investment Decision 3.1. Definition of Capital Budgetingmalik macNo ratings yet

- FM Group AssignmentDocument11 pagesFM Group AssignmentHailemelekot TerefeNo ratings yet

- Capital Budgeting MainDocument11 pagesCapital Budgeting MainriddhiNo ratings yet

- Capital Budgeting Decision: NPV Vs Irr Conflicts and ResolutionDocument18 pagesCapital Budgeting Decision: NPV Vs Irr Conflicts and Resolutionnasir abdulNo ratings yet

- Capital Budgeting NotesDocument46 pagesCapital Budgeting NotesShilpa Arora NarangNo ratings yet

- Chapter One: Capital Budgeting Decisions: 1.2. Classification of Projects Independent Verses Mutually Exclusive ProjectsDocument25 pagesChapter One: Capital Budgeting Decisions: 1.2. Classification of Projects Independent Verses Mutually Exclusive ProjectsezanaNo ratings yet

- Unit 6 EditedDocument22 pagesUnit 6 Editedtibebu yacobNo ratings yet

- Investment Decisions Core Document For Investors 1698274685Document16 pagesInvestment Decisions Core Document For Investors 1698274685Anonymous knightNo ratings yet

- Long Term Inv + FundamentalsDocument13 pagesLong Term Inv + Fundamentalssamuel kebedeNo ratings yet

- The Basics of Capital Budgeting: Should We Build This Plant?Document217 pagesThe Basics of Capital Budgeting: Should We Build This Plant?CV CVNo ratings yet

- Financial NotesDocument23 pagesFinancial NotesrahulNo ratings yet

- Define Capital Budgeting: Qualitative CriteriaDocument12 pagesDefine Capital Budgeting: Qualitative Criteriastannis69420No ratings yet

- Importance of Capital BudgetingDocument4 pagesImportance of Capital BudgetingSauhard AlungNo ratings yet

- Lec5. Capital BudgetingDocument78 pagesLec5. Capital Budgetingvivek patelNo ratings yet

- Capital Budgeting: Presented by AglaiaDocument12 pagesCapital Budgeting: Presented by AglaiaVishal AsijaNo ratings yet

- Capital BudgetingDocument94 pagesCapital Budgetingrobinkapoor100% (9)

- Capital Budgeting - THEORYDocument9 pagesCapital Budgeting - THEORYAarti PandeyNo ratings yet

- Project Hemanth EditDocument70 pagesProject Hemanth Editajaykumar royalNo ratings yet

- Financial Decision Making: MCCOM2005C04Document72 pagesFinancial Decision Making: MCCOM2005C04GLBM LEVEL 1No ratings yet

- Study Note - 7: Capital BudgetingDocument36 pagesStudy Note - 7: Capital Budgetingshivam kumarNo ratings yet

- Investments Profitability, Time Value & Risk Analysis: Guidelines for Individuals and CorporationsFrom EverandInvestments Profitability, Time Value & Risk Analysis: Guidelines for Individuals and CorporationsNo ratings yet

- Analytical Corporate Valuation: Fundamental Analysis, Asset Pricing, and Company ValuationFrom EverandAnalytical Corporate Valuation: Fundamental Analysis, Asset Pricing, and Company ValuationNo ratings yet

- One Track Minds. The Surprising Psychology of The InternetDocument292 pagesOne Track Minds. The Surprising Psychology of The InternetArt Marr100% (2)

- Paper - 1: Principles & Practice of Accounting Questions True and FalseDocument29 pagesPaper - 1: Principles & Practice of Accounting Questions True and FalseMayur bhujadeNo ratings yet

- Chapter 15 PPT - Holthausen & Zmijewski 2019Document100 pagesChapter 15 PPT - Holthausen & Zmijewski 2019royNo ratings yet

- Internet BillDocument4 pagesInternet BillKanchan Asnani0% (1)

- Echallan MH010490649202223 EDocument1 pageEchallan MH010490649202223 EPramod PawarNo ratings yet

- Liquidation Based ValuationDocument45 pagesLiquidation Based ValuationMagic ShopNo ratings yet

- Cutomer and Banker RelationshipDocument23 pagesCutomer and Banker RelationshipSamridhiNo ratings yet

- Merchant BankingDocument93 pagesMerchant BankingSaadhana MuthuNo ratings yet

- c73s1ch48 PDFDocument2 pagesc73s1ch48 PDFChandra JacksonNo ratings yet

- NMIMS - SBM: Teaching Plan Financial Management Academic Year: 2017-18 Course Code Course Title Course Instructor/sDocument3 pagesNMIMS - SBM: Teaching Plan Financial Management Academic Year: 2017-18 Course Code Course Title Course Instructor/sManav ManochaNo ratings yet

- Digital EnvironmentDocument13 pagesDigital EnvironmentPrathameshNo ratings yet

- The Venus ProjectDocument27 pagesThe Venus Projectapi-252242159100% (1)

- International Financial Reporting and Analysis 7th Edition Alexander Solutions ManualDocument13 pagesInternational Financial Reporting and Analysis 7th Edition Alexander Solutions Manualcrastzfeiej100% (15)

- Final Intermediate 1 2015 2016Document10 pagesFinal Intermediate 1 2015 2016ZeeNo ratings yet

- The Basics of Accounting For Derivatives and Hedge AccountingDocument7 pagesThe Basics of Accounting For Derivatives and Hedge AccountingRENU BALANo ratings yet

- Treasury Code: The Andhra PradeshDocument104 pagesTreasury Code: The Andhra PradeshacesrspNo ratings yet

- MSF LCR Fallcr Tools For LRM in The Banks 1626896525Document6 pagesMSF LCR Fallcr Tools For LRM in The Banks 1626896525G GNo ratings yet

- Nike FInancial ResourceDocument2 pagesNike FInancial ResourceهانيNo ratings yet

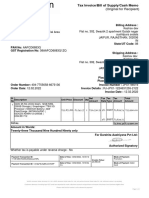

- Tax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Document1 pageTax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)erjasdNo ratings yet

- XL EnergyDocument18 pagesXL EnergyvishalNo ratings yet

- Kfs Credit CardsDocument4 pagesKfs Credit CardsVijayakumar C SNo ratings yet

- NPO MidtermDocument4 pagesNPO MidtermPatrick Ferdinand AlvarezNo ratings yet

- Module 1 - Financial Statement AnalysisDocument15 pagesModule 1 - Financial Statement AnalysisSiddhesh Kolgaonkar100% (1)

- Tax.3201-2 Classification of TaxesDocument3 pagesTax.3201-2 Classification of TaxesMira Louise HernandezNo ratings yet

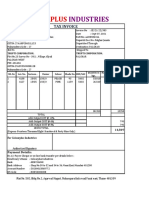

- Colourplus GST Invoice - 2020-2021 - TruptiDocument1 pageColourplus GST Invoice - 2020-2021 - TruptiSRJOFFICIAL7No ratings yet

- On Bank AuditDocument101 pagesOn Bank Auditrinky123123100% (4)