You might also like

- EN WP Home-Lifestyles-2025Document38 pagesEN WP Home-Lifestyles-2025kerryNo ratings yet

- Economic Principles - Tutorial 5 - AnswersDocument12 pagesEconomic Principles - Tutorial 5 - Answersmad EYESNo ratings yet

- Self-Test Problems (Solutions in Appendix B) : LG5 LG2Document6 pagesSelf-Test Problems (Solutions in Appendix B) : LG5 LG2Hamad Gul0% (1)

- Week 7 Workshop Solutions - Long-Term Debt MarketsDocument3 pagesWeek 7 Workshop Solutions - Long-Term Debt MarketsMengdi ZhangNo ratings yet

- Assignment Print View 3.11Document4 pagesAssignment Print View 3.11Zach JaapNo ratings yet

- Web Table 29. The World'S Top 100 Non-Financial TNCS, Ranked by Foreign Assets, 2010Document3 pagesWeb Table 29. The World'S Top 100 Non-Financial TNCS, Ranked by Foreign Assets, 2010Ramona Palaghianu0% (1)

- Solution Manual For Managerial Economics 7th Edition AllenDocument33 pagesSolution Manual For Managerial Economics 7th Edition AllenPrashant GautamNo ratings yet

- Lecture 6 Behavior of Interest RatesDocument33 pagesLecture 6 Behavior of Interest RatesAman Ullah BalochNo ratings yet

- Money and Banking Week 1 CH 5Document5 pagesMoney and Banking Week 1 CH 5Pradipta NarendraNo ratings yet

- 2021 Sept 23 Lec Ch2 Part 4Document27 pages2021 Sept 23 Lec Ch2 Part 4dsfghNo ratings yet

- ch05 Mish11ge EmbfmDocument33 pagesch05 Mish11ge EmbfmRakib HasanNo ratings yet

- Practice Questions FinalDocument3 pagesPractice Questions FinalAman SinghNo ratings yet

- # What Is Demand?Document4 pages# What Is Demand?Rifat RahmanNo ratings yet

- Worked Solutions 3Document7 pagesWorked Solutions 3Zahied MukaddamNo ratings yet

- Course 2 Sample Exam Questions: y Units of BroccoliDocument47 pagesCourse 2 Sample Exam Questions: y Units of BroccoliEden ZapicoNo ratings yet

- DSDocument57 pagesDSDelishaNo ratings yet

- Chapter 2 NotesDocument2 pagesChapter 2 NotesMatt CourchaineNo ratings yet

- Test Bank For Corporate Finance 4th Canadian Edition by BerkDocument37 pagesTest Bank For Corporate Finance 4th Canadian Edition by Berkangelahollandwdeirnczob100% (27)

- Fi AssignmentDocument9 pagesFi Assignmentyohannes kindalem0% (1)

- Worksheet For BondsDocument12 pagesWorksheet For BondsvishalNo ratings yet

- Sample TestDocument9 pagesSample Teststudunt100% (2)

- Final-Exam Macro SOLUTION DisplayDocument10 pagesFinal-Exam Macro SOLUTION DisplayAhmed KharratNo ratings yet

- Module 17 Practice Set 1Document5 pagesModule 17 Practice Set 1Jacqueline LiuNo ratings yet

- Valuation of Bonds and StocksDocument71 pagesValuation of Bonds and Stocksnaag1000No ratings yet

- PS3 MKT Euqil RiskDocument5 pagesPS3 MKT Euqil RiskebbamorkNo ratings yet

- Fiance Exam 2Document8 pagesFiance Exam 2Tien VoNo ratings yet

- Chapter 2Document32 pagesChapter 2josephyoseph97No ratings yet

- 2021 Lecture 4 Cost of International FinanceDocument21 pages2021 Lecture 4 Cost of International FinanceBogdan BNo ratings yet

- 1453975109ch 4 Bond ValuationDocument50 pages1453975109ch 4 Bond ValuationAshutoshNo ratings yet

- Economics Memo Test 1 2017Document14 pagesEconomics Memo Test 1 2017Rearabetswe MositsaNo ratings yet

- ECON 201 - Problem Set 1Document5 pagesECON 201 - Problem Set 1KemalNo ratings yet

- Investment Analysis & Portfolio Management: Bond Valuation: That Holding Period IsDocument5 pagesInvestment Analysis & Portfolio Management: Bond Valuation: That Holding Period IsNitesh KirarNo ratings yet

- Chapter 3Document49 pagesChapter 3Worknesh AmlakuNo ratings yet

- CH 4Document23 pagesCH 4Gizaw BelayNo ratings yet

- Types of Public and Private LoansDocument12 pagesTypes of Public and Private LoansshuvoertizaNo ratings yet

- Interest RatesDocument48 pagesInterest RatesSakshi SharmaNo ratings yet

- Economics NotesDocument80 pagesEconomics Notesgavin_d265No ratings yet

- Valuation of Debt Contracts and Their Price Volatility Characteristics Questions See Answers BelowDocument7 pagesValuation of Debt Contracts and Their Price Volatility Characteristics Questions See Answers Belowevivanco1899No ratings yet

- Ican Revision Class - Bond Valuation (Cap-Ii) : Ca Rajendra Mangal Joshi 1Document16 pagesIcan Revision Class - Bond Valuation (Cap-Ii) : Ca Rajendra Mangal Joshi 1Sushant MaskeyNo ratings yet

- MBA OUM Demo Lecture QuestionsDocument15 pagesMBA OUM Demo Lecture Questionsmup100% (2)

- Bond Valuation: The Present Value ApproachDocument8 pagesBond Valuation: The Present Value Approachpeerawicht247No ratings yet

- Demand and Supply KoDocument41 pagesDemand and Supply Kojoy nietesNo ratings yet

- MicroeconomicsDocument17 pagesMicroeconomicsmohitrameshagrawalNo ratings yet

- Reading 27 Valuation and AnalysisDocument32 pagesReading 27 Valuation and Analysiskiran.malukani26No ratings yet

- BB - 6 - Futures & Options - Hull - Chap - 6Document23 pagesBB - 6 - Futures & Options - Hull - Chap - 6Ibrahim KhatatbehNo ratings yet

- Chap 8 Bond Valuation and RiskDocument37 pagesChap 8 Bond Valuation and RiskYasin ArAthNo ratings yet

- CHP 6 - Time Value of MoneyDocument11 pagesCHP 6 - Time Value of MoneyShahnawaz KhanNo ratings yet

- L - 6 Bond ValuationDocument14 pagesL - 6 Bond ValuationJagrityTalwarNo ratings yet

- Acctng Ed 09 - Financial Management: Page 1 of 3Document3 pagesAcctng Ed 09 - Financial Management: Page 1 of 3LeojelaineIgcoyNo ratings yet

- Accounting Sample 1Document6 pagesAccounting Sample 1AmnaNo ratings yet

- Final S12014 MarkingGuideDocument13 pagesFinal S12014 MarkingGuideYuuki KiryuuNo ratings yet

- Assignment 1Document6 pagesAssignment 1Mayank KumarNo ratings yet

- Chapter 3 (1) Comp. Alt & D 2015Document27 pagesChapter 3 (1) Comp. Alt & D 2015ananiya dawitNo ratings yet

- Chpater 2Document6 pagesChpater 2creative Questions &answerNo ratings yet

- Chapter 6: Interest RatesDocument6 pagesChapter 6: Interest RateskafiNo ratings yet

- FIS Assignment 1 Bitan SahaDocument6 pagesFIS Assignment 1 Bitan SahaBitan SahaNo ratings yet

- RepoDocument132 pagesRepoJiashen Charles GouNo ratings yet

- DaanDocument6 pagesDaanMarc GaoNo ratings yet

- Macroeconomics 9th Edition Mankiw Solutions Manual DownloadDocument20 pagesMacroeconomics 9th Edition Mankiw Solutions Manual DownloadEric Gaitor100% (21)

- International Finance, HedgeDocument7 pagesInternational Finance, HedgeJasmin HallNo ratings yet

- The Volatility Surface: A Practitioner's GuideFrom EverandThe Volatility Surface: A Practitioner's GuideRating: 4 out of 5 stars4/5 (4)

- Modern Portfolio Management: Moving Beyond Modern Portfolio TheoryFrom EverandModern Portfolio Management: Moving Beyond Modern Portfolio TheoryNo ratings yet

- UI Referencing ManualDocument13 pagesUI Referencing Manualayantayo TolulopeNo ratings yet

- Eco 362 Module 2Document26 pagesEco 362 Module 2ayantayo TolulopeNo ratings yet

- Eco 362 Module 1Document42 pagesEco 362 Module 1ayantayo TolulopeNo ratings yet

- The Land Use Act and Land Administration in 21St Century Nigeria: Need For ReformsDocument29 pagesThe Land Use Act and Land Administration in 21St Century Nigeria: Need For Reformsayantayo TolulopeNo ratings yet

- Prototipo v1 14.09Document11 pagesPrototipo v1 14.09D'Shopping PerúNo ratings yet

- Successfully Tested Types of Banknote Handling Machine - Customer-Operated MachinesDocument35 pagesSuccessfully Tested Types of Banknote Handling Machine - Customer-Operated MachinesAdeng Kesuma HNo ratings yet

- Finance Compliance Training Calendar - Current v1Document2 pagesFinance Compliance Training Calendar - Current v1shilpan9166No ratings yet

- What Is A More Useful Measure To Judge A Nation's Economy - GDP (Nominal) or GDP (PPP) and Why - QuoraDocument6 pagesWhat Is A More Useful Measure To Judge A Nation's Economy - GDP (Nominal) or GDP (PPP) and Why - QuoraElite Cleaning ProductsNo ratings yet

- Policy and Regulation Export Coffee IndonesiaDocument12 pagesPolicy and Regulation Export Coffee Indonesiabioaudi10No ratings yet

- An Organisation Study REPORY On: Mamala, ErnakulamDocument12 pagesAn Organisation Study REPORY On: Mamala, ErnakulamJazmal JabbarNo ratings yet

- Akash Flight BookingDocument3 pagesAkash Flight BookingAkash GuptaNo ratings yet

- Reading Extracts - Vietnam's EconomyDocument5 pagesReading Extracts - Vietnam's EconomyAkuno HanaNo ratings yet

- Congratulations! You Saved This Month.: One Airtel Bill SummaryDocument8 pagesCongratulations! You Saved This Month.: One Airtel Bill SummarysrinuvaradamcaNo ratings yet

- Ride Details Bill Details: Mohammad GaushulDocument3 pagesRide Details Bill Details: Mohammad GaushulTathagataNo ratings yet

- UntitledDocument65 pagesUntitledShaira MejaresNo ratings yet

- Sample Questions - Life Cycle Costing and Target CostingDocument2 pagesSample Questions - Life Cycle Costing and Target Costingzohashafqat31No ratings yet

- Upgrad PayslipDocument1 pageUpgrad PayslipSantanu SauNo ratings yet

- Factors Causing Cost Overruns in Constru PDFDocument10 pagesFactors Causing Cost Overruns in Constru PDFcindrelNo ratings yet

- FINE 6800 - Assignment 2 Fall 2023Document4 pagesFINE 6800 - Assignment 2 Fall 2023Rishabh ValechaNo ratings yet

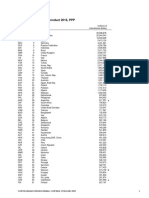

- Gross Domestic Product 2018, PPP: Ranking EconomyDocument4 pagesGross Domestic Product 2018, PPP: Ranking Economydory punisherNo ratings yet

- Subhiksha Marketing ManagementDocument17 pagesSubhiksha Marketing Managementpranav_khNo ratings yet

- Partnership Dissolution Learning ExercisesDocument32 pagesPartnership Dissolution Learning ExercisesAndrea Beverly TanNo ratings yet

- Error CorrectionDocument2 pagesError CorrectionArnyl ReyesNo ratings yet

- Origin of Customs DutyDocument45 pagesOrigin of Customs DutyJayagokul SaravananNo ratings yet

- Cost Accounting: T I C A PDocument4 pagesCost Accounting: T I C A PShehrozSTNo ratings yet

- Quotation 0045 NBGDocument1 pageQuotation 0045 NBGswwpi.cosicoNo ratings yet

- GFI 2019 IFF Update Report 1.29.18Document56 pagesGFI 2019 IFF Update Report 1.29.18Abdoulahi Y MAIGANo ratings yet

- Cambridge International AS & A Level: Economics 9708/23 May/June 2020Document6 pagesCambridge International AS & A Level: Economics 9708/23 May/June 2020Saaren SawmyNo ratings yet

- Digital Marketing Agency Business Plan ExampleDocument31 pagesDigital Marketing Agency Business Plan ExampleShafique Ur RehmanNo ratings yet

- B2C Cross-Border E-Commerce Export Logistics ModeDocument7 pagesB2C Cross-Border E-Commerce Export Logistics ModeVoiceover SpotNo ratings yet