You might also like

- Millets: Future of Food & FarmingDocument16 pagesMillets: Future of Food & FarmingKIRAN100% (2)

- Sol. Man. - Chapter 1 - The Accounting Process - Ia Part 1aDocument6 pagesSol. Man. - Chapter 1 - The Accounting Process - Ia Part 1aKaisser Niel Mari FormentoNo ratings yet

- Sem Plang Merchandising Perpetual Problem With AnswersDocument21 pagesSem Plang Merchandising Perpetual Problem With AnswersJayson Miranda100% (1)

- Sol. Man. - Chapter 2 - Cash & Cash Equivalents - Ia Part 1aDocument6 pagesSol. Man. - Chapter 2 - Cash & Cash Equivalents - Ia Part 1aMiguel AmihanNo ratings yet

- Quizzes - Chapter 6 - Business Transactions & Their AnalysisDocument6 pagesQuizzes - Chapter 6 - Business Transactions & Their AnalysisAmie Jane Miranda67% (3)

- Account ReceivableDocument13 pagesAccount ReceivableAndrea FontiverosNo ratings yet

- Sol. Man. - Chapter 4 - Accounts Receivable - Ia Part 1aDocument19 pagesSol. Man. - Chapter 4 - Accounts Receivable - Ia Part 1aMiguel AmihanNo ratings yet

- Sol. Man. - Chapter 5 - Notes Receivable - Ia Part 1aDocument11 pagesSol. Man. - Chapter 5 - Notes Receivable - Ia Part 1aKaisser Niel Mari FormentoNo ratings yet

- Sol. Man. - Chapter 13 - Basic Derivatives - Ia Part 1aDocument21 pagesSol. Man. - Chapter 13 - Basic Derivatives - Ia Part 1aJamie Rose Aragones100% (1)

- Sol. Man. - Chapter 13 - Basic Derivatives - Ia Part 1aDocument21 pagesSol. Man. - Chapter 13 - Basic Derivatives - Ia Part 1aJamie Rose Aragones100% (1)

- Equity Valuation: Models from Leading Investment BanksFrom EverandEquity Valuation: Models from Leading Investment BanksJan ViebigNo ratings yet

- Sol. Man. - Chapter 3 - Bank Reconciliation - Ia PartDocument15 pagesSol. Man. - Chapter 3 - Bank Reconciliation - Ia PartMike Joseph E. Moran100% (3)

- Sol. Man. - Chapter 7 - Inventories - Ia Part 1aDocument19 pagesSol. Man. - Chapter 7 - Inventories - Ia Part 1aRezzan Joy Camara MejiaNo ratings yet

- Sol. Man. - Chapter 7 - Inventories - Ia Part 1aDocument19 pagesSol. Man. - Chapter 7 - Inventories - Ia Part 1aRezzan Joy Camara MejiaNo ratings yet

- CDCS Self-Study Guide 2011Document21 pagesCDCS Self-Study Guide 2011armamut100% (2)

- Timing the Market: How to Profit in the Stock Market Using the Yield Curve, Technical Analysis, and Cultural IndicatorsFrom EverandTiming the Market: How to Profit in the Stock Market Using the Yield Curve, Technical Analysis, and Cultural IndicatorsNo ratings yet

- FABM 2 HANDOUTS 1st QRTRDocument17 pagesFABM 2 HANDOUTS 1st QRTRDanise PorrasNo ratings yet

- Accounting Cycle of A Merchandising BusinessDocument31 pagesAccounting Cycle of A Merchandising BusinessAresta, Novie Mae100% (1)

- IA Activity 2 Chapter 4&5Document9 pagesIA Activity 2 Chapter 4&5Sunghoon SsiNo ratings yet

- Sol. Man. - Chapter 8 - Inventory Estimation - Ia Part 1aDocument6 pagesSol. Man. - Chapter 8 - Inventory Estimation - Ia Part 1aRezzan Joy Camara MejiaNo ratings yet

- Accounting 1 FinalsDocument5 pagesAccounting 1 FinalsJohn Rey Bantay RodriguezNo ratings yet

- Computer Graphics Mini ProjectDocument25 pagesComputer Graphics Mini ProjectGautam Singh78% (81)

- Quizzes - Chapter 6 - Business Transactions & Their AnalysisDocument6 pagesQuizzes - Chapter 6 - Business Transactions & Their AnalysisAmie Jane MirandaNo ratings yet

- Sol. Man. - Chapter 11 - Investments - Additional ConceptsDocument10 pagesSol. Man. - Chapter 11 - Investments - Additional ConceptsChristian James RiveraNo ratings yet

- Chap 11Document6 pagesChap 11Shiela DimaculanganNo ratings yet

- Chapter 10 - Installment Sales MethodDocument13 pagesChapter 10 - Installment Sales MethodMohammad Allem AlegreNo ratings yet

- December 31, 20x1 January 2, 20x1: 1. A. Fob Shipping Point, Freight CollectDocument8 pagesDecember 31, 20x1 January 2, 20x1: 1. A. Fob Shipping Point, Freight CollectIvy MaximoNo ratings yet

- Asistensi AK-2 Week 9Document15 pagesAsistensi AK-2 Week 9haikal.abiyu.w41No ratings yet

- Solutions:: I. In-Transit ItemDocument6 pagesSolutions:: I. In-Transit ItemMary EdsylleNo ratings yet

- Business Transactions Their Analysis With Answers by AlagangwencyDocument4 pagesBusiness Transactions Their Analysis With Answers by AlagangwencyHello KittyNo ratings yet

- Inventory 1Document8 pagesInventory 1Ren AikawaNo ratings yet

- Working Papers in InventoriesDocument17 pagesWorking Papers in InventoriesTrisha VillegasNo ratings yet

- FAChapter 12Document3 pagesFAChapter 12zZl3Ul2NNINGZzNo ratings yet

- Preparing WorksheetDocument4 pagesPreparing Worksheet6z5qstn8wsNo ratings yet

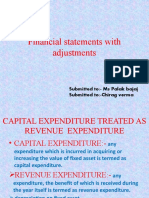

- Financial Statements With Adjustments: Submitted To:-Ms. Palak Bajaj Submitted By:-Chirag VermaDocument15 pagesFinancial Statements With Adjustments: Submitted To:-Ms. Palak Bajaj Submitted By:-Chirag VermaChiragNo ratings yet

- Adobe Scan Mar 16, 2023Document20 pagesAdobe Scan Mar 16, 2023Renalyn Ps MewagNo ratings yet

- P6Document15 pagesP6lakshmananrm2005No ratings yet

- A3 Example NotesDocument8 pagesA3 Example NotesMuyano, Mira Joy M.No ratings yet

- Accounting Cycle of A Merchandising BusinessDocument34 pagesAccounting Cycle of A Merchandising BusinessTariga, Dharen Joy J.No ratings yet

- Chapter 5 Exercises-Exercise BankDocument9 pagesChapter 5 Exercises-Exercise BankPATRICIUS ALAN WIRAYUDHA KUSUMNo ratings yet

- Intercompany Sale of PropertyDocument6 pagesIntercompany Sale of PropertyClauie BarsNo ratings yet

- Adobe Scan Mar 31, 2023Document20 pagesAdobe Scan Mar 31, 2023Renalyn Ps MewagNo ratings yet

- Quizzes - Chapter 6 - Business Transactions & Their AnalysisDocument6 pagesQuizzes - Chapter 6 - Business Transactions & Their AnalysisClint Abenoja100% (1)

- 2018-0232 Beldia, Pitchie Mae G. ACT142: Auditing and Assurance: Concepts and Application 1Document8 pages2018-0232 Beldia, Pitchie Mae G. ACT142: Auditing and Assurance: Concepts and Application 1Melanie SamsonaNo ratings yet

- Intermediate Accounting Unit4 - Topic4Document8 pagesIntermediate Accounting Unit4 - Topic4Lea Polinar100% (1)

- Prelim Answer Key: Redemption of Certificates Lapse of CertificatesDocument8 pagesPrelim Answer Key: Redemption of Certificates Lapse of CertificatesNikky Bless LeonarNo ratings yet

- Assignment - Cash FlowsDocument9 pagesAssignment - Cash FlowsArshad ChaudharyNo ratings yet

- Financial Accounting & AnalysisDocument2 pagesFinancial Accounting & AnalysisTangerine Ila TomarNo ratings yet

- Quizzes - Chapter 6 - Accounting Books - Journal and LedgerDocument5 pagesQuizzes - Chapter 6 - Accounting Books - Journal and LedgerAmie Jane MirandaNo ratings yet

- FM 1 Assignment 1Document3 pagesFM 1 Assignment 1Jelly Ann AndresNo ratings yet

- 04 Accounts Receivable - (PS)Document2 pages04 Accounts Receivable - (PS)kyle mandaresioNo ratings yet

- AR Sample ProbDocument9 pagesAR Sample ProbCix SorcheNo ratings yet

- Inventories&Inventoryestimation GAPASINAODocument25 pagesInventories&Inventoryestimation GAPASINAOGerly GapasinaoNo ratings yet

- Intermediate Accounting Unit4 - Topic5Document7 pagesIntermediate Accounting Unit4 - Topic5Lea PolinarNo ratings yet

- IA Practice Problems InvestmentsDocument6 pagesIA Practice Problems InvestmentsbiancavitasaNo ratings yet

- Financial Statements With Adjustments: Submitted To:-Ms Palak Bajaj Submitted To:-Chirag VermaDocument15 pagesFinancial Statements With Adjustments: Submitted To:-Ms Palak Bajaj Submitted To:-Chirag VermaChiragNo ratings yet

- Cash Flow Statement With Solution 5Document12 pagesCash Flow Statement With Solution 5Kaytise profNo ratings yet

- Comprehensive Income & NcahsDocument6 pagesComprehensive Income & NcahsNuarin JJ67% (3)

- Merchandising Business - Sample Problem (Answers)Document4 pagesMerchandising Business - Sample Problem (Answers)Eana MabalotNo ratings yet

- Cuenca 4Document31 pagesCuenca 4Daphn CuencaNo ratings yet

- Solutions:: Problem 3: Exercises 1Document2 pagesSolutions:: Problem 3: Exercises 1Stephen JohnNo ratings yet

- CBSE Class 12 Accountancy Cash Flow Statement Set BDocument14 pagesCBSE Class 12 Accountancy Cash Flow Statement Set BJenneil CarmichaelNo ratings yet

- PDF Chapter 2 CompressDocument33 pagesPDF Chapter 2 CompressRonel GaviolaNo ratings yet

- Sol. Man. - Chapter 7 - Inventories - Ia Part 1a - 2020 EditionDocument24 pagesSol. Man. - Chapter 7 - Inventories - Ia Part 1a - 2020 EditionJapon, Jenn RossNo ratings yet

- Financial Accounting and Reporting - Trade and Other Receivables (Recognition, Measurement, Estimation and Valuation)Document6 pagesFinancial Accounting and Reporting - Trade and Other Receivables (Recognition, Measurement, Estimation and Valuation)LuisitoNo ratings yet

- 12Document24 pages12Maria G. BernardinoNo ratings yet

- Quizzes - Chapter 6 - Business Transactions & Their AnalysisDocument6 pagesQuizzes - Chapter 6 - Business Transactions & Their AnalysisAmie Jane MirandaNo ratings yet

- Chapter 10 - Problem 2Document5 pagesChapter 10 - Problem 2Christy HabelNo ratings yet

- Accounts ReceivableDocument8 pagesAccounts ReceivableFireworks PHNo ratings yet

- HintDocument6 pagesHintAppleNo ratings yet

- Cash and AccrualDocument3 pagesCash and Accrual夜晨曦No ratings yet

- Capital and Revenue TransactionsDocument7 pagesCapital and Revenue Transactionscarolm790No ratings yet

- Accounts Paper 1 November 2008Document9 pagesAccounts Paper 1 November 2008Munashe BinhaNo ratings yet

- Accounting Research Proposal Defense 2023 - 2024 (Edited)Document7 pagesAccounting Research Proposal Defense 2023 - 2024 (Edited)Kaisser Niel Mari FormentoNo ratings yet

- 04.2 - Data Privacy ActDocument17 pages04.2 - Data Privacy ActKaisser Niel Mari FormentoNo ratings yet

- 03.1 - Bouncing ChequesDocument2 pages03.1 - Bouncing ChequesKaisser Niel Mari FormentoNo ratings yet

- 01.1 - Maceda LawDocument2 pages01.1 - Maceda LawKaisser Niel Mari FormentoNo ratings yet

- 01.4 - Lemon LawDocument7 pages01.4 - Lemon LawKaisser Niel Mari FormentoNo ratings yet

- 04.1 - AmlaDocument11 pages04.1 - AmlaKaisser Niel Mari FormentoNo ratings yet

- 04.3 - Anti-Red TapeDocument19 pages04.3 - Anti-Red TapeKaisser Niel Mari FormentoNo ratings yet

- Chapter 10 - Inv. in Debt SecuritiesDocument19 pagesChapter 10 - Inv. in Debt SecuritiesIramae NavarroNo ratings yet

- 06 - Secrecy of Bank DepositsDocument2 pages06 - Secrecy of Bank DepositsKaisser Niel Mari FormentoNo ratings yet

- 05 - Negotiable InstrumentsDocument12 pages05 - Negotiable InstrumentsKaisser Niel Mari FormentoNo ratings yet

- 06 - Anti-Red TapeDocument5 pages06 - Anti-Red TapeKaisser Niel Mari FormentoNo ratings yet

- 06 - Intellectual PropertyDocument8 pages06 - Intellectual PropertyKaisser Niel Mari FormentoNo ratings yet

- 06 - AmlaDocument12 pages06 - AmlaKaisser Niel Mari FormentoNo ratings yet

- Chapter 9 Investments Ia Part 1aDocument9 pagesChapter 9 Investments Ia Part 1arobinady dollagaNo ratings yet

- Sol. Man. - Chapter 11 - Investments - Additional ConceptsDocument10 pagesSol. Man. - Chapter 11 - Investments - Additional ConceptsKaisser Niel Mari FormentoNo ratings yet

- Sol. Man. - Chapter 12 - Other Long-Term Investments - Ia Part 1aDocument3 pagesSol. Man. - Chapter 12 - Other Long-Term Investments - Ia Part 1aJamie Rose AragonesNo ratings yet

- Sol. Man. - Chapter 6 - Receivables Addtl Concept - Ia Part 1aDocument7 pagesSol. Man. - Chapter 6 - Receivables Addtl Concept - Ia Part 1aJenny Joy Alcantara0% (1)

- Chapter 10 - Inv. in Debt SecuritiesDocument19 pagesChapter 10 - Inv. in Debt SecuritiesIramae NavarroNo ratings yet

- Chapter 9 Investments Ia Part 1aDocument9 pagesChapter 9 Investments Ia Part 1arobinady dollagaNo ratings yet

- Sol. Man. - Chapter 12 - Other Long-Term Investments - Ia Part 1aDocument3 pagesSol. Man. - Chapter 12 - Other Long-Term Investments - Ia Part 1aJamie Rose AragonesNo ratings yet

- 3.1-7 Printer Deployment - Copy (Full Permission)Document18 pages3.1-7 Printer Deployment - Copy (Full Permission)Hanzel NietesNo ratings yet

- 671 - BP Well Control Tool Kit 2002Document19 pages671 - BP Well Control Tool Kit 2002Ibama MirillaNo ratings yet

- Hood Design Using NX Cad: HOOD: The Hood Is The Cover of The Engine in The Vehicles With An Engine at Its FrontDocument3 pagesHood Design Using NX Cad: HOOD: The Hood Is The Cover of The Engine in The Vehicles With An Engine at Its FrontHari TejNo ratings yet

- Enabling Trade Report 2013, World Trade ForumDocument52 pagesEnabling Trade Report 2013, World Trade ForumNancy Islam100% (1)

- Nepal CountryReport PDFDocument64 pagesNepal CountryReport PDFnickdash09No ratings yet

- Lecture 3 - Marriage and Marriage PaymentsDocument11 pagesLecture 3 - Marriage and Marriage PaymentsGrace MguniNo ratings yet

- Panch ShilDocument118 pagesPanch ShilSohel BangiNo ratings yet

- Stryker Endoscopy SDC Pro 2 DVDDocument2 pagesStryker Endoscopy SDC Pro 2 DVDWillemNo ratings yet

- Imp121 1isDocument6 pagesImp121 1isErnesto AyzenbergNo ratings yet

- TC 9-237 Welding 1993Document680 pagesTC 9-237 Welding 1993enricoNo ratings yet

- Evaluating The Policy Outcomes For Urban Resiliency in Informal Settlements Since Independence in Dhaka, Bangladesh: A ReviewDocument14 pagesEvaluating The Policy Outcomes For Urban Resiliency in Informal Settlements Since Independence in Dhaka, Bangladesh: A ReviewJaber AbdullahNo ratings yet

- On The Backward Problem For Parabolic Equations With MemoryDocument19 pagesOn The Backward Problem For Parabolic Equations With MemorykamranNo ratings yet

- T53 L 13 Turboshaft EngineDocument2 pagesT53 L 13 Turboshaft EngineEagle1968No ratings yet

- Module 2 Lesson 2 Communication and TechnologyDocument7 pagesModule 2 Lesson 2 Communication and TechnologyClarence EscopeteNo ratings yet

- SMPLEDocument2 pagesSMPLEKla AlvarezNo ratings yet

- All About Ignition Coils: Technical InformationDocument15 pagesAll About Ignition Coils: Technical InformationTrương Ngọc ThắngNo ratings yet

- Formula Retail and Large Controls Planning Department ReportDocument235 pagesFormula Retail and Large Controls Planning Department ReportMissionLocalNo ratings yet

- O-CNN: Octree-Based Convolutional Neural Networks For 3D Shape AnalysisDocument11 pagesO-CNN: Octree-Based Convolutional Neural Networks For 3D Shape AnalysisJose Angel Duarte MartinezNo ratings yet

- PDFDocument18 pagesPDFDental LabNo ratings yet

- Guide On Multiple RegressionDocument29 pagesGuide On Multiple RegressionLucyl MendozaNo ratings yet

- New VLSIDocument2 pagesNew VLSIRanjit KumarNo ratings yet

- Item No. 6 Diary No 6856 2024 ConsolidatedDocument223 pagesItem No. 6 Diary No 6856 2024 Consolidatedisha NagpalNo ratings yet

- Mobilcut 102 Hoja TecnicaDocument2 pagesMobilcut 102 Hoja TecnicaCAGERIGONo ratings yet

- Lab 1Document8 pagesLab 1Нурболат ТаласбайNo ratings yet

- Basic Details: Government Eprocurement SystemDocument4 pagesBasic Details: Government Eprocurement SystemNhai VijayawadaNo ratings yet

- UntitledDocument6 pagesUntitledCoky IrcanNo ratings yet

- 13 - Conclusion and SuggestionsDocument4 pages13 - Conclusion and SuggestionsjothiNo ratings yet