You might also like

- US Internal Revenue Service: I1099ac 06Document4 pagesUS Internal Revenue Service: I1099ac 06IRSNo ratings yet

- 0 - 1098 Mortgage Interest 2022 - 01122023 - 162111Document1 page0 - 1098 Mortgage Interest 2022 - 01122023 - 162111Osvaldo CalderonUACJNo ratings yet

- Rental Property Worksheet TemplateDocument3 pagesRental Property Worksheet TemplateBella Melendres100% (1)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- How The American Dream Has Changed Over TimeDocument3 pagesHow The American Dream Has Changed Over TimeKellie ClarkNo ratings yet

- Rental Properties 2021: Guide For Rental Property OwnersDocument52 pagesRental Properties 2021: Guide For Rental Property Ownersuly01 cubillaNo ratings yet

- Tenant L AgreementDocument14 pagesTenant L AgreementSrikar ChinmayaNo ratings yet

- Property Rental PDFDocument25 pagesProperty Rental PDFlewisweiss363No ratings yet

- HMRC - Trust and UK Estate PropertyDocument8 pagesHMRC - Trust and UK Estate PropertyRay Walsh100% (1)

- 07 Income From Property (50 59)Document11 pages07 Income From Property (50 59)jafferyasim100% (2)

- Business Analysis of NestleDocument39 pagesBusiness Analysis of NestleFaiZan Mahmood100% (2)

- 17 CIR v. Tours SpecialistsDocument3 pages17 CIR v. Tours SpecialistsChedeng KumaNo ratings yet

- P158-PR-RFQ-ITB-001-02 Clarification 2 - PLNDocument2 pagesP158-PR-RFQ-ITB-001-02 Clarification 2 - PLNhasan shahriarNo ratings yet

- Gartner IT Key Metrics Data: 2011 Summary ReportDocument12 pagesGartner IT Key Metrics Data: 2011 Summary ReportVincent BoixNo ratings yet

- Report On Summer Training (July 2019) : Organization: Irrigation Department, Guwahati West Division, UlubariDocument22 pagesReport On Summer Training (July 2019) : Organization: Irrigation Department, Guwahati West Division, UlubariKunal Das75% (4)

- Exclusive Right To Market Property AgreementDocument5 pagesExclusive Right To Market Property Agreementkat perezNo ratings yet

- Tratamentul Total Al CanceruluiDocument71 pagesTratamentul Total Al CanceruluiAntal98% (98)

- US Internal Revenue Service: I1040se - 2001Document6 pagesUS Internal Revenue Service: I1040se - 2001IRSNo ratings yet

- US Internal Revenue Service: I1040se - 1997Document5 pagesUS Internal Revenue Service: I1040se - 1997IRSNo ratings yet

- Short-Term Rentals 2021Document2 pagesShort-Term Rentals 2021Finn KevinNo ratings yet

- US Internal Revenue Service: I1040sd - 1999Document7 pagesUS Internal Revenue Service: I1040sd - 1999IRSNo ratings yet

- US Internal Revenue Service: I1040sd - 2002Document9 pagesUS Internal Revenue Service: I1040sd - 2002IRSNo ratings yet

- US Internal Revenue Service: I8582cr - 1997Document13 pagesUS Internal Revenue Service: I8582cr - 1997IRSNo ratings yet

- IRD Rental Properties Ir264Document41 pagesIRD Rental Properties Ir264Roger DaltryNo ratings yet

- US Internal Revenue Service: I1040se - 2002Document6 pagesUS Internal Revenue Service: I1040se - 2002IRSNo ratings yet

- House PropertyDocument22 pagesHouse PropertyAmrit TejaniNo ratings yet

- US Internal Revenue Service: I1099ac - 2001Document4 pagesUS Internal Revenue Service: I1099ac - 2001IRSNo ratings yet

- US Internal Revenue Service: I8582cr - 1998Document13 pagesUS Internal Revenue Service: I8582cr - 1998IRSNo ratings yet

- EA EA2 SU3 OutlineDocument9 pagesEA EA2 SU3 OutlineAdil AliNo ratings yet

- Fundamentals of Taxation 2015 8Th Edition Cruz Test Bank Full Chapter PDFDocument66 pagesFundamentals of Taxation 2015 8Th Edition Cruz Test Bank Full Chapter PDFmarushiapatrina100% (9)

- US Internal Revenue Service: I1040sc - 2003Document9 pagesUS Internal Revenue Service: I1040sc - 2003IRSNo ratings yet

- SA105 Notes 2023Document12 pagesSA105 Notes 2023ellylid73No ratings yet

- Guide On Business Use of Home DeductionDocument2 pagesGuide On Business Use of Home DeductionHitaishi PrakashNo ratings yet

- US Internal Revenue Service: I1040sfDocument7 pagesUS Internal Revenue Service: I1040sfIRSNo ratings yet

- 37 Income From House PropertyDocument7 pages37 Income From House Propertytejasgjain100% (1)

- House Property Nikita1Document19 pagesHouse Property Nikita1Amrit Tejani100% (1)

- SA105 English Notes-2021Document12 pagesSA105 English Notes-2021Dominic NooneyNo ratings yet

- US Internal Revenue Service: I1040sc - 2000Document8 pagesUS Internal Revenue Service: I1040sc - 2000IRSNo ratings yet

- Taxation of Income From House Property: 8 November 2011Document17 pagesTaxation of Income From House Property: 8 November 2011Ravinder GoelNo ratings yet

- US Internal Revenue Service: I1040sf - 2001Document6 pagesUS Internal Revenue Service: I1040sf - 2001IRSNo ratings yet

- IRS Form 5405Document2 pagesIRS Form 5405maxcpa100% (1)

- Right To Acquire RTA1 Form 2022Document7 pagesRight To Acquire RTA1 Form 2022Hajar NachitNo ratings yet

- US Internal Revenue Service: I1099sDocument4 pagesUS Internal Revenue Service: I1099sIRSNo ratings yet

- US Internal Revenue Service: I1040sd - 2000Document8 pagesUS Internal Revenue Service: I1040sd - 2000IRSNo ratings yet

- GST/HST New Housing Rebate Application For Houses Purchased From A BuilderDocument4 pagesGST/HST New Housing Rebate Application For Houses Purchased From A BuilderEffel PradoNo ratings yet

- US Internal Revenue Service: I1040se - 2004Document6 pagesUS Internal Revenue Service: I1040se - 2004IRSNo ratings yet

- Hubert Tagoe w9Document1 pageHubert Tagoe w9Hubert TagoeNo ratings yet

- US Internal Revenue Service: I1040sf - 2003Document6 pagesUS Internal Revenue Service: I1040sf - 2003IRSNo ratings yet

- Fundamentals of Taxation 2015 8Th Edition Cruz Solutions Manual Full Chapter PDFDocument48 pagesFundamentals of Taxation 2015 8Th Edition Cruz Solutions Manual Full Chapter PDFmarushiapatrina100% (8)

- Sa105 NotesDocument14 pagesSa105 Notesmarijana_jovanovikNo ratings yet

- Residential Tenancy Agreement (Standard Form of Lease)Document13 pagesResidential Tenancy Agreement (Standard Form of Lease)khodadadpNo ratings yet

- Fundamentals of Taxation 2014 7th Edition Cruz Test BankDocument58 pagesFundamentals of Taxation 2014 7th Edition Cruz Test Bankmohurrum.ginkgo.iabwuz100% (27)

- US Internal Revenue Service: I1065bsk - 2001Document10 pagesUS Internal Revenue Service: I1065bsk - 2001IRSNo ratings yet

- US Internal Revenue Service: I8582cr - 1995Document14 pagesUS Internal Revenue Service: I8582cr - 1995IRSNo ratings yet

- US Internal Revenue Service: I8582cr - 1993Document14 pagesUS Internal Revenue Service: I8582cr - 1993IRSNo ratings yet

- Property Rental Toolkit: 2019-20 Self Assessment Tax Returns Published April 2020Document28 pagesProperty Rental Toolkit: 2019-20 Self Assessment Tax Returns Published April 2020jonofsNo ratings yet

- Instructions For Form 4562: Depreciation and Amortization (Including Information On Listed Property)Document12 pagesInstructions For Form 4562: Depreciation and Amortization (Including Information On Listed Property)IRSNo ratings yet

- US Internal Revenue Service: I1040se - 2006Document7 pagesUS Internal Revenue Service: I1040se - 2006IRSNo ratings yet

- Ir 264Document44 pagesIr 264Anonymous jbvNLNANLINo ratings yet

- US Internal Revenue Service: I1040sc - 2005Document10 pagesUS Internal Revenue Service: I1040sc - 2005IRSNo ratings yet

- US Internal Revenue Service: F2106ez - 1996Document2 pagesUS Internal Revenue Service: F2106ez - 1996IRSNo ratings yet

- Shareholder's Instructions For Schedule K-1 (Form 1120S) : Pager/SgmlDocument8 pagesShareholder's Instructions For Schedule K-1 (Form 1120S) : Pager/SgmlIRSNo ratings yet

- Tax HandoutDocument6 pagesTax Handoutshekharsuhani5No ratings yet

- Greenburgh Complex LeaseDocument27 pagesGreenburgh Complex LeaseNewsdayNo ratings yet

- 2 - Income From PropertyDocument5 pages2 - Income From PropertyALI HUSSAINNo ratings yet

- US Internal Revenue Service: F1041es - 2005Document5 pagesUS Internal Revenue Service: F1041es - 2005IRSNo ratings yet

- Text Solutions - CH8Document16 pagesText Solutions - CH8Josef Galileo SibalaNo ratings yet

- 2008 Credit Card Bulk Provider RequirementsDocument112 pages2008 Credit Card Bulk Provider RequirementsIRSNo ratings yet

- US Internal Revenue Service: 2290rulesty2007v4 0Document6 pagesUS Internal Revenue Service: 2290rulesty2007v4 0IRSNo ratings yet

- 2008 Objectives Report To Congress v2Document153 pages2008 Objectives Report To Congress v2IRSNo ratings yet

- 2008 Data DictionaryDocument260 pages2008 Data DictionaryIRSNo ratings yet

- Cma Intermediate Youtube Faculties LinksDocument6 pagesCma Intermediate Youtube Faculties LinksPAVITHRA MURUGANNo ratings yet

- 147 Dodd Hall: Jagnew@geog - Ucla.eduDocument3 pages147 Dodd Hall: Jagnew@geog - Ucla.edulantea1No ratings yet

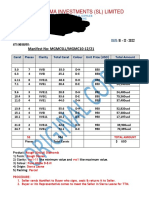

- Bryanston Inve Vijay Karpe 22090934Document2 pagesBryanston Inve Vijay Karpe 22090934Karan RathodNo ratings yet

- Congress Policy Brief - CoCoLevyFundsDocument10 pagesCongress Policy Brief - CoCoLevyFundsKat DinglasanNo ratings yet

- Banco Central de Chile - Indicadores Diarios - Euro (Pesos Por Euro) - Año 2017Document9 pagesBanco Central de Chile - Indicadores Diarios - Euro (Pesos Por Euro) - Año 2017Lorena MutizábalNo ratings yet

- Managerial Remuneration Checklist FinalDocument4 pagesManagerial Remuneration Checklist FinaldhuvadpratikNo ratings yet

- Pending Home SalesDocument2 pagesPending Home SalesAmber TaufenNo ratings yet

- ACSI Travel Report 2018-2019: American Customer Satisfaction IndexDocument14 pagesACSI Travel Report 2018-2019: American Customer Satisfaction IndexJeet SinghNo ratings yet

- 6 Ch14 - Central BanksDocument63 pages6 Ch14 - Central BanksNgọc Ngô Thị MinhNo ratings yet

- Chapter 1 Microeconomics For Managers Winter 2013Document34 pagesChapter 1 Microeconomics For Managers Winter 2013Jessica Danforth GalvezNo ratings yet

- Inventory ProblemsDocument2 pagesInventory ProblemsKhaja MohiddinNo ratings yet

- 320 - 33 - Powerpoint-Slides - Chapter-10-Monopolistic-Competition-Oligopoly (Autosaved)Document37 pages320 - 33 - Powerpoint-Slides - Chapter-10-Monopolistic-Competition-Oligopoly (Autosaved)Ayush KumarNo ratings yet

- ODMP Inception Report Volume 1 (Of 2)Document134 pagesODMP Inception Report Volume 1 (Of 2)Ase JohannessenNo ratings yet

- Cera Sanitaryware Limited: Annual Report 2007-08Document40 pagesCera Sanitaryware Limited: Annual Report 2007-08Rakhi183No ratings yet

- Manifest 232Document2 pagesManifest 232Elev8ted MindNo ratings yet

- Ca De-4Document4 pagesCa De-4Kevin Marcos FelicianoNo ratings yet

- Assignment On BelgiumDocument21 pagesAssignment On Belgiumgalib gosnoforNo ratings yet

- An Analytical Study On Impact of Credit Rating Agencies in India 'S DevelopmentDocument14 pagesAn Analytical Study On Impact of Credit Rating Agencies in India 'S DevelopmentRamneet kaur (Rizzy)No ratings yet

- Dos With Assumption of MortgageDocument3 pagesDos With Assumption of MortgagejosefNo ratings yet

- Farewell Address WorksheetDocument3 pagesFarewell Address Worksheetapi-261464658No ratings yet

- NTSE MAT Solved Sample Paper 1 PDFDocument17 pagesNTSE MAT Solved Sample Paper 1 PDFAlmelu AvinashNo ratings yet

- Cabinet Members 2020Document2 pagesCabinet Members 2020AMNo ratings yet

- An Investigation Into The Determinants of Cost Efficiency in The Zambian Banking SectorDocument45 pagesAn Investigation Into The Determinants of Cost Efficiency in The Zambian Banking SectorKemi OlojedeNo ratings yet

- Eco - II AssignmentDocument10 pagesEco - II AssignmentPrerna JhaNo ratings yet