You might also like

- Projected Financial Statements To Be Submitted To The Bank For Loan ProposalDocument46 pagesProjected Financial Statements To Be Submitted To The Bank For Loan ProposalAMIT K SINGH83% (12)

- F3 Study NotesDocument251 pagesF3 Study NotesHamza AliNo ratings yet

- SF RS (I) 1-28: Accounting For Investment in Associated Comp AniesDocument25 pagesSF RS (I) 1-28: Accounting For Investment in Associated Comp AniesRilo WiloNo ratings yet

- Flow Chart-1Document1 pageFlow Chart-1Pankaj MahajanNo ratings yet

- Flow Chart (L-2)Document1 pageFlow Chart (L-2)JazaNo ratings yet

- Private EquityDocument9 pagesPrivate Equitysv798dctq9No ratings yet

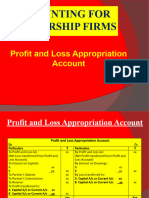

- Partnership Firms Part 2 Appropriation of ProfitDocument14 pagesPartnership Firms Part 2 Appropriation of ProfitDeepti BistNo ratings yet

- Activity 1Document5 pagesActivity 1Karylle ComiaNo ratings yet

- As 23Document6 pagesAs 23abhishekkapse654No ratings yet

- Change in Profit-Sharing RatioDocument3 pagesChange in Profit-Sharing RatioPainNo ratings yet

- TTS - LBO PrimerDocument5 pagesTTS - LBO PrimerKrystleNo ratings yet

- Investments in Associates and Investments in Jointly Controlled EntitiesDocument47 pagesInvestments in Associates and Investments in Jointly Controlled EntitiesPhilip Dan Jayson LarozaNo ratings yet

- Retirement or Death of Partner NewDocument5 pagesRetirement or Death of Partner NewAnkit Roy100% (1)

- Partnership Firms - Part5 Guarantee and Past AdjustmentDocument15 pagesPartnership Firms - Part5 Guarantee and Past AdjustmentDeepti BistNo ratings yet

- Business & Financial RiskDocument26 pagesBusiness & Financial RiskPrabhuvardhan ReddyNo ratings yet

- Mod 5 Dividend Decisions Handout SNDocument7 pagesMod 5 Dividend Decisions Handout SNAkhilNo ratings yet

- InsuranceDocument15 pagesInsurancekananguptaNo ratings yet

- 002 Equity MethodDocument4 pages002 Equity Methodcaparvez25No ratings yet

- Accounting For Equity InvestmentsDocument13 pagesAccounting For Equity InvestmentsMUHAMMAD SAJJADNo ratings yet

- Fundamentals PDFDocument103 pagesFundamentals PDFDhairya JainNo ratings yet

- Investments-In-Associate by Justine Louie SantiagoDocument30 pagesInvestments-In-Associate by Justine Louie SantiagoMark Gelo WinchesterNo ratings yet

- Part1 Topic 4 Reconstitution of PartnershipDocument21 pagesPart1 Topic 4 Reconstitution of PartnershipShivani ChoudhariNo ratings yet

- Capital Structure and Firm ValueDocument31 pagesCapital Structure and Firm Valuearunima1486No ratings yet

- Dividend DecisionDocument13 pagesDividend DecisionFALAK OBERAINo ratings yet

- Module 4Document5 pagesModule 4imsana minatozakiNo ratings yet

- Mod 1 FullDocument42 pagesMod 1 FullZAIL JEFF ALDEA DALENo ratings yet

- 12 AccountancyDocument4 pages12 AccountancyAbhishek DhillonNo ratings yet

- Dayag Notes Partnership FormationDocument3 pagesDayag Notes Partnership FormationGirl Lang AkoNo ratings yet

- Chapter 17Document36 pagesChapter 17metarereNo ratings yet

- Accounting For Business CombinationsDocument13 pagesAccounting For Business CombinationsLu CasNo ratings yet

- Ad Acc As QusDocument196 pagesAd Acc As QusRadhika GargNo ratings yet

- Ias 28 Investment in AssociateDocument2 pagesIas 28 Investment in AssociateMireya YueNo ratings yet

- Preparation of Separate Financial StatementsDocument29 pagesPreparation of Separate Financial StatementschingNo ratings yet

- Capital Structure and Firm ValueDocument18 pagesCapital Structure and Firm ValuechandanNo ratings yet

- Changes in A PartnershipDocument18 pagesChanges in A PartnershipHadi HarizNo ratings yet

- ACC2001 Lecture 10 Interco TransactionsDocument42 pagesACC2001 Lecture 10 Interco Transactionsmichael krueseiNo ratings yet

- Dividend Policy: Saurty Shekyn Das (1310709) BSC (Hons) Finance (Minor: Law) Dfa2002Y (3) Corporate Finance 20 April 2015Document9 pagesDividend Policy: Saurty Shekyn Das (1310709) BSC (Hons) Finance (Minor: Law) Dfa2002Y (3) Corporate Finance 20 April 2015Anonymous H2L7lwBs3No ratings yet

- Pas 28 Investments in Associates and Joint VenturesDocument2 pagesPas 28 Investments in Associates and Joint VenturesR.A.No ratings yet

- SS&C GlobeOp - FA ModuleDocument34 pagesSS&C GlobeOp - FA ModuleAnil Dube100% (1)

- 74697bos60485 Inter p1 cp5 U3Document35 pages74697bos60485 Inter p1 cp5 U3aryanharsh2004No ratings yet

- M&A GlossaryDocument12 pagesM&A GlossaryKhouseyn IslamovNo ratings yet

- Lecture 7 Company AccountingDocument25 pagesLecture 7 Company AccountingSalah MobarakNo ratings yet

- Capital StructuresDocument44 pagesCapital StructuresAnupam JenaNo ratings yet

- PARTNERSHIPDocument8 pagesPARTNERSHIPShayne BenaweNo ratings yet

- Are Depreciation and Amortization Included in Gross Profit - InvestopediaDocument5 pagesAre Depreciation and Amortization Included in Gross Profit - InvestopediaBob KaneNo ratings yet

- Accounting For PartnershipDocument15 pagesAccounting For Partnershipnagesh dashNo ratings yet

- Entrepreneurial Finance Leach & Melicher: Venture Capital Valuation MethodsDocument29 pagesEntrepreneurial Finance Leach & Melicher: Venture Capital Valuation MethodsIT manNo ratings yet

- Solvency Valuation RatiosDocument13 pagesSolvency Valuation RatiosAnushka JindalNo ratings yet

- Jeesoo Kim - AGS Presentation 2022 (V3)Document18 pagesJeesoo Kim - AGS Presentation 2022 (V3)Jeesoo KimNo ratings yet

- 2020 BP Cost of Capital EVADocument17 pages2020 BP Cost of Capital EVAPhuc NguyenNo ratings yet

- Advacc BookDocument4 pagesAdvacc Book20220633No ratings yet

- Partnership FormationDocument16 pagesPartnership FormationKian BarredoNo ratings yet

- Total Return Total Return: 2/3 BHK Homes Cradled by Trees, in Bangalore 2/3 BHK Homes Cradled by Trees, in BangaloreDocument12 pagesTotal Return Total Return: 2/3 BHK Homes Cradled by Trees, in Bangalore 2/3 BHK Homes Cradled by Trees, in Bangalorenetra14520No ratings yet

- Audit of Investment-LectureDocument15 pagesAudit of Investment-LecturemoNo ratings yet

- Key-Terms and Chapter Summary-8-1Document2 pagesKey-Terms and Chapter Summary-8-1Jeetalal GadaNo ratings yet

- Partnership CharacteristicsDocument22 pagesPartnership Characteristicslou-924No ratings yet

- Cost of Capital PDFDocument37 pagesCost of Capital PDFBala RanganathNo ratings yet

- Cheat Sheet FADM PDFDocument2 pagesCheat Sheet FADM PDFmohitks01_89No ratings yet

- Accounting For PartnetshipDocument36 pagesAccounting For PartnetshipKelvin mwaiNo ratings yet

- Audio Chapter 12 - Companies PART CDocument13 pagesAudio Chapter 12 - Companies PART CprunellaNo ratings yet

- Chapter 11 Pricing Strategies For Firms With Market PowerDocument14 pagesChapter 11 Pricing Strategies For Firms With Market Powerdimitri fox100% (1)

- MTP - Intermediate - Syllabus 2016 - Dec2019 - Set1: Paper 5-Financial AccountingDocument7 pagesMTP - Intermediate - Syllabus 2016 - Dec2019 - Set1: Paper 5-Financial AccountingvijaykumartaxNo ratings yet

- Gr9EMST2L2 SlidesDocument16 pagesGr9EMST2L2 SlidesadoliveiraNo ratings yet

- Instant Download Ebook PDF Eu Employment Law Oxford European Union Law Library 4th Edition PDF ScribdDocument41 pagesInstant Download Ebook PDF Eu Employment Law Oxford European Union Law Library 4th Edition PDF Scribdchester.whelan11198% (47)

- LC Issuance Request LetterDocument4 pagesLC Issuance Request LetterAakay EnterprisesNo ratings yet

- Mad About Sports PVT LTD: Venkateswarlu GurramDocument1 pageMad About Sports PVT LTD: Venkateswarlu GurramGv IareNo ratings yet

- ACCTG 102 (Cash and Cash Equivalent)Document4 pagesACCTG 102 (Cash and Cash Equivalent)Yoonah KimNo ratings yet

- Configuration For Procurement - SAP GSTDocument36 pagesConfiguration For Procurement - SAP GSTRANJAN GHOSHNo ratings yet

- 2024 CDS ExaminationDocument1 page2024 CDS Examination007potterharryNo ratings yet

- COMM204 (Little's Law and Its Application)Document18 pagesCOMM204 (Little's Law and Its Application)Sahil ParekhNo ratings yet

- Substantive Test of LiabilitiesDocument60 pagesSubstantive Test of Liabilitiesjulia4razoNo ratings yet

- Program Development ProcessDocument37 pagesProgram Development ProcessLeah NarneNo ratings yet

- Operating Segment StudentsDocument4 pagesOperating Segment StudentsAG VenturesNo ratings yet

- Annex C - Barangay Inventory and Turnover Form No. 2 Final Inventory and Turnover of BPFRDs and Money AccountabilitiesDocument2 pagesAnnex C - Barangay Inventory and Turnover Form No. 2 Final Inventory and Turnover of BPFRDs and Money AccountabilitiesNico & Hope So100% (4)

- APPLIED ECONOMICS Quater 3 Module 4 EditedDocument14 pagesAPPLIED ECONOMICS Quater 3 Module 4 EditedSharmaine TapalesNo ratings yet

- Ind Nifty EnergyDocument2 pagesInd Nifty EnergyPrabhakar DalviNo ratings yet

- Indonesia Aviation Decarbonization Roundtable - FinalDocument33 pagesIndonesia Aviation Decarbonization Roundtable - FinalEvans Azka FNo ratings yet

- Model Question (Complimentary Course-1) Co 1131: Managerial EconomicsDocument2 pagesModel Question (Complimentary Course-1) Co 1131: Managerial EconomicsJaseel MuhammadNo ratings yet

- QP BST 1Document8 pagesQP BST 1qwertyNo ratings yet

- TBChap 012Document237 pagesTBChap 012omar altamimiNo ratings yet

- InvoiceDocument8 pagesInvoiceAlex StratNo ratings yet

- CE On Income TaxDocument4 pagesCE On Income TaxalyssaNo ratings yet

- Ucpb BranchesDocument4 pagesUcpb BranchesWinter SNo ratings yet

- Working Capital ManagementDocument7 pagesWorking Capital ManagementIsmail MarzukiNo ratings yet

- 4offer MJ 04.03 .21Document3 pages4offer MJ 04.03 .21SANDESH GHANDATNo ratings yet

- Integrating Multi-Functional Shared Services: Better Together!Document8 pagesIntegrating Multi-Functional Shared Services: Better Together!Vikram BiswasNo ratings yet

- Business Econ - 3Document13 pagesBusiness Econ - 3Tharindu DhananjayaNo ratings yet

- Dr. Yogesh Gurjar King of HeartsDocument6 pagesDr. Yogesh Gurjar King of HeartsbhaveshreddygunNo ratings yet