You might also like

- Applied Corporate Finance. What is a Company worth?From EverandApplied Corporate Finance. What is a Company worth?Rating: 3 out of 5 stars3/5 (2)

- Dividend Growth Investing: A Step-by-Step Guide to Building a Dividend Portfolio for Early RetirementFrom EverandDividend Growth Investing: A Step-by-Step Guide to Building a Dividend Portfolio for Early RetirementNo ratings yet

- 003 Equity-Method-2Document2 pages003 Equity-Method-2caparvez25No ratings yet

- Financial Statement Analysis - Concept Questions and Solutions - Chapter 2Document20 pagesFinancial Statement Analysis - Concept Questions and Solutions - Chapter 2stefy934100% (2)

- Chapter 12 Assigned Question SOLUTIONSDocument61 pagesChapter 12 Assigned Question SOLUTIONSDang ThanhNo ratings yet

- Demas Taufik - Task 13Document8 pagesDemas Taufik - Task 13DemastaufiqNo ratings yet

- Full Download Advanced Accounting 12th Edition Beams Solutions ManualDocument36 pagesFull Download Advanced Accounting 12th Edition Beams Solutions Manualrojeroissy2232s100% (39)

- Dwnload Full Advanced Accounting 12th Edition Beams Solutions Manual PDFDocument13 pagesDwnload Full Advanced Accounting 12th Edition Beams Solutions Manual PDFunrudesquirtjghzl100% (11)

- Investment in AssociateDocument33 pagesInvestment in AssociateKimivy BusaNo ratings yet

- T1 FIN MA2 Capital Budgeting DecisionsDocument120 pagesT1 FIN MA2 Capital Budgeting DecisionsMangoStarr Aibelle VegasNo ratings yet

- Dwnload Full Advanced Accounting 11th Edition Beams Solutions Manual PDFDocument35 pagesDwnload Full Advanced Accounting 11th Edition Beams Solutions Manual PDFwilliambrowntdoypjmnrc100% (14)

- Full Download Advanced Accounting 11th Edition Beams Solutions ManualDocument35 pagesFull Download Advanced Accounting 11th Edition Beams Solutions Manualrojeroissy2232s100% (19)

- Chapter 5 Investments in Equity SecuritiesDocument13 pagesChapter 5 Investments in Equity SecuritiesKrissa Mae Longos100% (2)

- Chapter 17 and 18 - Investment in Associates What Is An Associate? Accounting Procedures of Investment in AssociateDocument2 pagesChapter 17 and 18 - Investment in Associates What Is An Associate? Accounting Procedures of Investment in AssociateRanee DeeNo ratings yet

- Microsoft Word - FAR01 - Accounting For Equity InvestmentsDocument4 pagesMicrosoft Word - FAR01 - Accounting For Equity InvestmentsDisguised owlNo ratings yet

- Investment in Associate 18Document3 pagesInvestment in Associate 18gab camonNo ratings yet

- Investment Holding CompanyDocument6 pagesInvestment Holding CompanyAnas AjwadNo ratings yet

- Unit 7 Investment Centres: ObjectivesDocument11 pagesUnit 7 Investment Centres: ObjectivesMeera SolankeNo ratings yet

- SBR Mock1 As - s20 j21Document14 pagesSBR Mock1 As - s20 j21percy mapetereNo ratings yet

- Solution Manual For Advanced Accounting 13Th Edition Beams Anthony Bettinghaus Smith 0134472144 9780134472140 Full Chapter PDFDocument30 pagesSolution Manual For Advanced Accounting 13Th Edition Beams Anthony Bettinghaus Smith 0134472144 9780134472140 Full Chapter PDFrose.carvin242100% (11)

- FSA Assignment III Group 4Document4 pagesFSA Assignment III Group 4Kristina Kitty100% (1)

- IntaccDocument19 pagesIntaccMelita CarriedoNo ratings yet

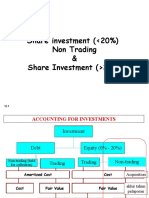

- 12.2 Share Investment Non Trading & Share Invesment Lebih 20%Document18 pages12.2 Share Investment Non Trading & Share Invesment Lebih 20%TIFFANNY SHELIANo ratings yet

- SBR - Mock A - AnswersDocument14 pagesSBR - Mock A - AnswersDylan MutambanengweNo ratings yet

- Chap 002Document121 pagesChap 002Selena SevvinNo ratings yet

- Fundamental Principles of Measuring ValueDocument17 pagesFundamental Principles of Measuring ValueHari RaoNo ratings yet

- Bab 2Document6 pagesBab 2Elsha Cahya Inggri MaharaniNo ratings yet

- Palmones Adrio B. Investment in Equity SecuritiesDocument18 pagesPalmones Adrio B. Investment in Equity SecuritiesAndrei GoNo ratings yet

- Chapter 3 - Consolidations - Subsequent To The Date of AcquisitionDocument79 pagesChapter 3 - Consolidations - Subsequent To The Date of AcquisitionBLe BerNo ratings yet

- Assessment-3b-2 (1) (AutoRecovered)Document6 pagesAssessment-3b-2 (1) (AutoRecovered)Trúc NguyễnNo ratings yet

- 2019 Quarter One Report: Presented by You ExecDocument21 pages2019 Quarter One Report: Presented by You ExecdayanaNo ratings yet

- BSA 3202 Topic 1 - Investment in AssociatesDocument15 pagesBSA 3202 Topic 1 - Investment in AssociatesFrancis Abuyuan100% (1)

- Reporting Intercorporate Investments and Consolidation of Wholly Owned Subsidiaries With No DifferentialDocument121 pagesReporting Intercorporate Investments and Consolidation of Wholly Owned Subsidiaries With No DifferentialZahra Zafirah AmaliaNo ratings yet

- CAPITAL STRUCTURE and COCDocument37 pagesCAPITAL STRUCTURE and COCRashen DilNo ratings yet

- Fundamental Principles of Measuring and Managing ValueDocument17 pagesFundamental Principles of Measuring and Managing ValueLuismy VacacelaNo ratings yet

- Advacc BookDocument4 pagesAdvacc Book20220633No ratings yet

- Ap FinalDocument16 pagesAp FinalAkshi BhagiaNo ratings yet

- Module 3 Divisible ProfitsDocument8 pagesModule 3 Divisible ProfitsVijay KumarNo ratings yet

- As at 29 February 2020: Invesco Enhanced Income LimitedDocument2 pagesAs at 29 February 2020: Invesco Enhanced Income LimitedRebeccaLangfordNo ratings yet

- FM in Construction 2Document23 pagesFM in Construction 2YosiNo ratings yet

- Managerial Accounting: Individual Report OnDocument13 pagesManagerial Accounting: Individual Report OnRishav KoiralaNo ratings yet

- Non-Discounting Criteria Discounting CriteriaDocument89 pagesNon-Discounting Criteria Discounting CriteriaAytenew AbebeNo ratings yet

- Accounting: Lecture 4.2 Associates & JVDocument14 pagesAccounting: Lecture 4.2 Associates & JVcynthiama7777No ratings yet

- As 23Document6 pagesAs 23abhishekkapse654No ratings yet

- Chap002 Consolidation of Wholly Owned Subsidiaries With No DifferentialDocument73 pagesChap002 Consolidation of Wholly Owned Subsidiaries With No DifferentialMd. Rejaul Ahsan ChowdhuryNo ratings yet

- Reporting Intercorporate Investments and Consolidation of Wholly Owned Subsidiaries With No DifferentialDocument96 pagesReporting Intercorporate Investments and Consolidation of Wholly Owned Subsidiaries With No DifferentialEl Phi RaNo ratings yet

- ADocument89 pagesAJohn Carlo O. BallaresNo ratings yet

- Return On Equity:: A Compelling Case For InvestorsDocument15 pagesReturn On Equity:: A Compelling Case For InvestorsPutri LucyanaNo ratings yet

- Paper - 8: Financial Management and Economics For Finance Part A: Financial Management Questions Ratio AnalysisDocument29 pagesPaper - 8: Financial Management and Economics For Finance Part A: Financial Management Questions Ratio AnalysisEFRETNo ratings yet

- S2 PPTDocument12 pagesS2 PPTPUSHKAL AGGARWALNo ratings yet

- Valuation Model StartupDocument2 pagesValuation Model StartupLi XianNo ratings yet

- Course Name Course Code Student Name Student ID DateDocument7 pagesCourse Name Course Code Student Name Student ID Datemona asgharNo ratings yet

- Chapter Four AdvDocument23 pagesChapter Four AdvMisganu AyanaNo ratings yet

- Full Download Advanced Accounting 13th Edition Beams Solutions ManualDocument36 pagesFull Download Advanced Accounting 13th Edition Beams Solutions Manualjacksongubmor100% (34)

- TAX 2202E TBS02 02.solutionDocument3 pagesTAX 2202E TBS02 02.solutionZhitong LuNo ratings yet

- Reporting Intercorporate Investments and Consolidation of Wholly Owned Subsidiaries With No DifferentialDocument96 pagesReporting Intercorporate Investments and Consolidation of Wholly Owned Subsidiaries With No DifferentialShinta PakpahanNo ratings yet

- Paper - 8: Financial Management and Economics For Finance Part A: Financial Management Questions Ratio AnalysisDocument29 pagesPaper - 8: Financial Management and Economics For Finance Part A: Financial Management Questions Ratio AnalysisBharat NotnaniNo ratings yet

- T7 - Long-Lived AssetsDocument42 pagesT7 - Long-Lived AssetsJhonatan Perez VillanuevaNo ratings yet

- CPU - Financial Acctg & Reporting II - CHAPTER 2Document25 pagesCPU - Financial Acctg & Reporting II - CHAPTER 2Princess Jonabelle BaylonNo ratings yet

- 5 FinDocument35 pages5 FinMansour HamjaNo ratings yet

- 002 Equity MethodDocument4 pages002 Equity Methodcaparvez25No ratings yet

- 002 Lease-Accouting-2Document2 pages002 Lease-Accouting-2caparvez25No ratings yet

- 008 EBIT-and-EBITDADocument7 pages008 EBIT-and-EBITDAcaparvez25No ratings yet

- 014 HW-3-begDocument6 pages014 HW-3-begcaparvez25No ratings yet

- 013 Double-Entry-AccoutningDocument11 pages013 Double-Entry-Accoutningcaparvez25No ratings yet

- 002 CashDocument4 pages002 Cashcaparvez25No ratings yet

- General Mathematics11 - q2 - Clas1 - Simple-and-Compound-Interest - v3Document19 pagesGeneral Mathematics11 - q2 - Clas1 - Simple-and-Compound-Interest - v3Kim Yessamin MadarcosNo ratings yet

- Account SummaryDocument1 pageAccount Summaryvanita kunnoNo ratings yet

- 1 - Acc 311 Exam II Spring 2015Document9 pages1 - Acc 311 Exam II Spring 2015MUHAMMAD AZAMNo ratings yet

- Dashboard Pinnacle CPA Review Study Guide (Sir Brad's Version)Document43 pagesDashboard Pinnacle CPA Review Study Guide (Sir Brad's Version)Mica TolentinoNo ratings yet

- Sandhiya Project FinalDocument59 pagesSandhiya Project Finalss1364310No ratings yet

- Reporter No. 4 - Pdic LawDocument47 pagesReporter No. 4 - Pdic LawJi YuNo ratings yet

- Bus Math11 Slo QTR2-WK 1 - 2Document5 pagesBus Math11 Slo QTR2-WK 1 - 2Alma Dimaranan-Acuña100% (1)

- Wealth Creation: Back Cover Front Cover Gate Fold FrontDocument128 pagesWealth Creation: Back Cover Front Cover Gate Fold Frontvijay sharmaNo ratings yet

- Test CasesDocument10 pagesTest Casespuneet mishraNo ratings yet

- Emerging Areas For Articleship ExperienceDocument17 pagesEmerging Areas For Articleship ExperienceAmit JainNo ratings yet

- LVL - Subsidiary Sales & Purchases 2020Document34 pagesLVL - Subsidiary Sales & Purchases 2020rheamaenarciso613No ratings yet

- IT Certificate 2020-21 BajajDocument1 pageIT Certificate 2020-21 BajajPushpendra SinghNo ratings yet

- AccountingDocument50 pagesAccountingAshyanna UletNo ratings yet

- Financial Analytics - Unit - 5 Portfolio Analytics - 2022Document50 pagesFinancial Analytics - Unit - 5 Portfolio Analytics - 2022Nila TamilselvanNo ratings yet

- Internship AbrshDocument23 pagesInternship AbrshAbrsh AbNo ratings yet

- Ch-4 Ratios TheoryDocument3 pagesCh-4 Ratios TheoryShubham PhophaliaNo ratings yet

- NIYODocument11 pagesNIYOMohamed Aftab GNo ratings yet

- Debt To Total Asset RatioDocument13 pagesDebt To Total Asset RatioMjNo ratings yet

- 905 XXXXXXXXX 20267Document2 pages905 XXXXXXXXX 20267snbnbbNo ratings yet

- Online Banking Services of India: 2/16/2022 Devanshi ParmarDocument96 pagesOnline Banking Services of India: 2/16/2022 Devanshi ParmarFLEX FFNo ratings yet

- Cashflow StatementDocument16 pagesCashflow StatementJames NdegwaNo ratings yet

- Write Your Answer For Part A HereDocument9 pagesWrite Your Answer For Part A HereMATHEW JACOBNo ratings yet

- 11MEMORANDUM OF AGREEMENT FOR MT103 (Repaired)Document21 pages11MEMORANDUM OF AGREEMENT FOR MT103 (Repaired)ᜆ᜔ᜀᜄ᜔ᜀ ᜉ᜔ᜀᜄ᜔ᜉ᜔ᜀᜎ᜔ᜀᜌ᜔ᜀNo ratings yet

- Capital Markets Institutions, Instruments, and Risk Management Fifth EditionDocument20 pagesCapital Markets Institutions, Instruments, and Risk Management Fifth EditionFrancis0% (2)

- Accounting IAS Model Answers Series 3 2013Document8 pagesAccounting IAS Model Answers Series 3 2013Aung Zaw HtweNo ratings yet

- Int. Acc 1 Chap 2Document7 pagesInt. Acc 1 Chap 2Nicole Anne Santiago SibuloNo ratings yet

- Portfolio PerformanceDocument30 pagesPortfolio PerformanceSiddhant AggarwalNo ratings yet

- Quiz EiDocument3 pagesQuiz EiJOY LYN REFUGIONo ratings yet

- Accounting TermsDocument5 pagesAccounting TermsShanti GunaNo ratings yet

- Study Material CH.-2 Goodwil ValuationDocument9 pagesStudy Material CH.-2 Goodwil Valuationvsy9926No ratings yet