You might also like

- Chapter 4 Solutions Horngren Cost AccountingDocument50 pagesChapter 4 Solutions Horngren Cost AccountingAnik Kumar MallickNo ratings yet

- AME - 2022 - Tutorial 4 - SolutionsDocument24 pagesAME - 2022 - Tutorial 4 - SolutionsjjpasemperNo ratings yet

- Cma Adnan Rashid Complete NotesDocument541 pagesCma Adnan Rashid Complete NotesHAREEM25% (4)

- Test ScenarioDocument12 pagesTest Scenariofarahcheha50% (2)

- Exercises Chapter 3Document13 pagesExercises Chapter 3mohsen bukNo ratings yet

- Accounting For Manufacturing OverheadDocument9 pagesAccounting For Manufacturing OverheadKenzel lawasNo ratings yet

- Chapter 04 ThompsonDocument27 pagesChapter 04 ThompsonCynthia Penoliar33% (3)

- Project Report On Accounting SystemDocument76 pagesProject Report On Accounting SystemSujeet KumarNo ratings yet

- Akuntansi Biaya UtsDocument2 pagesAkuntansi Biaya Utsfatkhatul khasanahNo ratings yet

- Job CostingDocument24 pagesJob CostingElaine YapNo ratings yet

- Cost Accounting Job Costing Chapter 4 Charles T Horngrens 13thDocument10 pagesCost Accounting Job Costing Chapter 4 Charles T Horngrens 13thHaris FayyazNo ratings yet

- No. 4-31,4-32,4-33 Page 143-144Document12 pagesNo. 4-31,4-32,4-33 Page 143-144Nemalai VitalNo ratings yet

- Tutorial + Homework Job Costing CADocument2 pagesTutorial + Homework Job Costing CAmiranti dNo ratings yet

- Asistensi + Homework Job Costing PDFDocument2 pagesAsistensi + Homework Job Costing PDFYogie YaditraNo ratings yet

- Faithjames Servano - SA No. 4 - Chapter 3 Job Order CostingDocument1 pageFaithjames Servano - SA No. 4 - Chapter 3 Job Order CostingFaith James ServanoNo ratings yet

- AFAR - 11.1-Cost Accounting (Job Order and Process Costing)Document3 pagesAFAR - 11.1-Cost Accounting (Job Order and Process Costing)Daniela AubreyNo ratings yet

- Costing 2 Material - 014417Document40 pagesCosting 2 Material - 014417sirjamtech36No ratings yet

- No. 4-20-21 Page 138-139Document6 pagesNo. 4-20-21 Page 138-139Nemalai VitalNo ratings yet

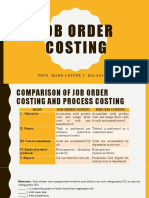

- Job Order Costing: Prof. Mark Lester T. Balasa, CpaDocument24 pagesJob Order Costing: Prof. Mark Lester T. Balasa, CpaNah HamzaNo ratings yet

- Acct602 Managerial AccountingDocument8 pagesAcct602 Managerial AccountingHaroon KhurshidNo ratings yet

- Exercises Lesson 3Document2 pagesExercises Lesson 3Nino LANo ratings yet

- HW 6 KeyDocument5 pagesHW 6 KeyRosinda ArendainNo ratings yet

- 4-18 Page 125 Laguna Mission Actual Costs Model ModelDocument9 pages4-18 Page 125 Laguna Mission Actual Costs Model ModelMisty Dawn BancroftNo ratings yet

- ACCT 213 ExerciseDocument5 pagesACCT 213 ExerciseMr MDRKHMNo ratings yet

- Chap 4 Job CostingDocument9 pagesChap 4 Job CostingWadiah AkbarNo ratings yet

- Exercises Job Costing Normal Costing - March 29 2023Document2 pagesExercises Job Costing Normal Costing - March 29 2023alica.durcekovaNo ratings yet

- ACCT3203 Contemporary Managerial Accounting: Lecture Illustration Examples With SolutionsDocument11 pagesACCT3203 Contemporary Managerial Accounting: Lecture Illustration Examples With SolutionsJingwen YangNo ratings yet

- Assignment Day 2Document5 pagesAssignment Day 2Indahna SulfaNo ratings yet

- Activity Based Costing ER - NewDocument14 pagesActivity Based Costing ER - NewFadillah LubisNo ratings yet

- Questions Part2 Srikant and Datar TextbookDocument5 pagesQuestions Part2 Srikant and Datar TextbookUmar SyakirinNo ratings yet

- Chapter 4 Suggested HomeworkDocument22 pagesChapter 4 Suggested HomeworkNguyễn Hoàng MyNo ratings yet

- Product CostingDocument16 pagesProduct CostingAyush100% (1)

- Exercises (8.1) : 180 Part OneDocument7 pagesExercises (8.1) : 180 Part OneZakaria HasaneenNo ratings yet

- Chapter 2 HomeworkDocument2 pagesChapter 2 HomeworkAliya KainazarovaNo ratings yet

- PBEIIDocument6 pagesPBEIIDirajen PMNo ratings yet

- AB CA 20-1 Kuis - 4 PDFDocument1 pageAB CA 20-1 Kuis - 4 PDFYogie YaditraNo ratings yet

- BBA211 Vol8 JobCostingDocument10 pagesBBA211 Vol8 JobCostingAnisha SarahNo ratings yet

- Cost Accounting 15th Edition Horngren Solutions Manual 1Document36 pagesCost Accounting 15th Edition Horngren Solutions Manual 1maryreynoldsxdbtqcfaje100% (24)

- Acc123 Reviewer With AnswerDocument11 pagesAcc123 Reviewer With AnswerLianaNo ratings yet

- 21S 2083 Quiz 1 CDocument5 pages21S 2083 Quiz 1 CAkshit GoyalNo ratings yet

- Chapter 4 Part II ContinueDocument5 pagesChapter 4 Part II ContinueYAHIA ADELNo ratings yet

- CH 3Document19 pagesCH 3hey100% (1)

- BA 115 Module 2A Problem SetsDocument15 pagesBA 115 Module 2A Problem SetsPaul Rainer De VillaNo ratings yet

- Strategic Cost Accounting: MBA-First YearDocument99 pagesStrategic Cost Accounting: MBA-First YearNada YoussefNo ratings yet

- JOB ORDER COSTING-Production LossesDocument7 pagesJOB ORDER COSTING-Production LossesJude TadiosNo ratings yet

- Module 9 10 ACCTG 31 1Document11 pagesModule 9 10 ACCTG 31 1GESPEJO, JC SHEEN O.No ratings yet

- Process Costing - CompleeteDocument42 pagesProcess Costing - CompleeteKarimatun NisaNo ratings yet

- 05 Handout 1Document6 pages05 Handout 1Reanne Mae BilogNo ratings yet

- Midterm - Quiz - AEC6Document4 pagesMidterm - Quiz - AEC6aprilNo ratings yet

- Chapter 3 Job Order CostingDocument31 pagesChapter 3 Job Order CostingzamanNo ratings yet

- Sample Midterm PDFDocument9 pagesSample Midterm PDFErrell D. GomezNo ratings yet

- Lecture-8.1 Job Order Costing (Theory)Document7 pagesLecture-8.1 Job Order Costing (Theory)Nazmul-Hassan SumonNo ratings yet

- Management Information - ND2020 - Suggested - AnswersDocument4 pagesManagement Information - ND2020 - Suggested - Answerskawsar alamNo ratings yet

- CAC C5M1 Accounting For Factory OverheadDocument6 pagesCAC C5M1 Accounting For Factory OverheadKyla Mae AllamNo ratings yet

- Acc123 ReviewerDocument6 pagesAcc123 ReviewerYuki GraceNo ratings yet

- Tutorial Topic 6 Week 10 PDFDocument5 pagesTutorial Topic 6 Week 10 PDFAnonymous KovGERSNo ratings yet

- Production Departments Direct Labor Rate Manufacturing Overhead Application RatesDocument10 pagesProduction Departments Direct Labor Rate Manufacturing Overhead Application RatesSano ManjiroNo ratings yet

- Cost12ism 04Document42 pagesCost12ism 04d.pagkatoytoyNo ratings yet

- Skema PSPM 15-16 Aa025Document5 pagesSkema PSPM 15-16 Aa025Dehey KNo ratings yet

- Efficiency of Investment in a Socialist EconomyFrom EverandEfficiency of Investment in a Socialist EconomyMieczyslaw RakowskiNo ratings yet

- This Study Resource Was: Chapter 2-Professional Practice of Accountancy: An OverviewDocument5 pagesThis Study Resource Was: Chapter 2-Professional Practice of Accountancy: An OverviewNhel AlvaroNo ratings yet

- Ce Laws, Contracts and SpecificationsDocument20 pagesCe Laws, Contracts and SpecificationsMIKE ARTHUR DAVIDNo ratings yet

- Bobcat Compact Excavator E16 Operation Maintenance Manual 6989423Document14 pagesBobcat Compact Excavator E16 Operation Maintenance Manual 6989423andrewshelton250683psa100% (71)

- Motivating PeopleDocument4 pagesMotivating Peoplesweetgirl11No ratings yet

- Planning, Your, Development,, Guide, For, IndividualsDocument8 pagesPlanning, Your, Development,, Guide, For, IndividualscrdiNo ratings yet

- Diversification Strategy: Diversification in The Context of Growth StrategiesDocument7 pagesDiversification Strategy: Diversification in The Context of Growth StrategiesZainab ChitalwalaNo ratings yet

- Moa ImmersionDocument7 pagesMoa ImmersionJeriel Gener ApurilloNo ratings yet

- 100 Marks ProjectDocument89 pages100 Marks ProjectVijay Rane100% (1)

- Perdev 10Document22 pagesPerdev 10Rodalyn Dela Cruz NavarroNo ratings yet

- TAS 200 Insurance Dec 2016Document10 pagesTAS 200 Insurance Dec 2016tanziam66No ratings yet

- Structure of Banking in IndiaDocument22 pagesStructure of Banking in IndiaTushar Kumar 1140No ratings yet

- Silo - Tips A Level Business Paper 3 Specimen Assessment Material Mark SchemeDocument22 pagesSilo - Tips A Level Business Paper 3 Specimen Assessment Material Mark SchemeJohnny PlaysNo ratings yet

- 4 - Flows in The Supply Chain Term IVDocument27 pages4 - Flows in The Supply Chain Term IVBashishth GuptaNo ratings yet

- Specimen Signature Form: InstructionsDocument1 pageSpecimen Signature Form: InstructionsPatOcampoNo ratings yet

- Monmouth Student Template UpdatedDocument14 pagesMonmouth Student Template Updatedhao pengNo ratings yet

- NikeDocument3 pagesNikeArpita SahuNo ratings yet

- Kevin Cullen Resume 2015Document3 pagesKevin Cullen Resume 2015Kevin CullenNo ratings yet

- Relationship Management/Business Development ProfessionalDocument3 pagesRelationship Management/Business Development ProfessionalAhamed IbrahimNo ratings yet

- HPB Trafigura PRDocument2 pagesHPB Trafigura PRahmadhatakeNo ratings yet

- Introduction To Information SystemDocument43 pagesIntroduction To Information SystemMaruf AhmedNo ratings yet

- The Purchase Cube: A Three-Dimensional Typology of Purchase Behaviors (Baumgartner 2010)Document3 pagesThe Purchase Cube: A Three-Dimensional Typology of Purchase Behaviors (Baumgartner 2010)Vishnu ShankerNo ratings yet

- Employee Satisfaction of Hotel Industry - A Case Study of The GranDocument53 pagesEmployee Satisfaction of Hotel Industry - A Case Study of The GranParth PatelNo ratings yet

- Introduction To Business Law: Lecture 6: The Law Relating To Sale of Movable Goods - DefinitionsDocument9 pagesIntroduction To Business Law: Lecture 6: The Law Relating To Sale of Movable Goods - DefinitionsPrithibi IshrakNo ratings yet

- BDCC 03 00032 v2 PDFDocument30 pagesBDCC 03 00032 v2 PDFChintuNo ratings yet

- Epressing Resul So That, Such ThatDocument2 pagesEpressing Resul So That, Such Thatسدن آرماNo ratings yet

- EkspendityurprasesDocument3 pagesEkspendityurprasesKyree VladeNo ratings yet

- Sap SoxDocument3 pagesSap SoxSreedhar.DNo ratings yet

- Critical Study of White Collar CrimeDocument6 pagesCritical Study of White Collar CrimepawanNo ratings yet