You might also like

- Name: Shahihul Islam NPM: 22001082171 Class: A1Document2 pagesName: Shahihul Islam NPM: 22001082171 Class: A1shahihul IslamNo ratings yet

- Tutorial + Homework Job Costing CADocument2 pagesTutorial + Homework Job Costing CAmiranti dNo ratings yet

- Asistensi + Homework Job Costing PDFDocument2 pagesAsistensi + Homework Job Costing PDFYogie YaditraNo ratings yet

- Faithjames Servano - SA No. 4 - Chapter 3 Job Order CostingDocument1 pageFaithjames Servano - SA No. 4 - Chapter 3 Job Order CostingFaith James ServanoNo ratings yet

- Assignment Day 2Document5 pagesAssignment Day 2Indahna SulfaNo ratings yet

- Exercises Job Costing Normal Costing - March 29 2023Document2 pagesExercises Job Costing Normal Costing - March 29 2023alica.durcekovaNo ratings yet

- Job CostingDocument24 pagesJob CostingElaine YapNo ratings yet

- 137a-1 Exam#1 RDocument2 pages137a-1 Exam#1 RWallace YeungNo ratings yet

- Chapter 4 Part II ContinueDocument5 pagesChapter 4 Part II ContinueYAHIA ADELNo ratings yet

- Process Costing - CompleeteDocument42 pagesProcess Costing - CompleeteKarimatun NisaNo ratings yet

- Questions Part2 Srikant and Datar TextbookDocument5 pagesQuestions Part2 Srikant and Datar TextbookUmar SyakirinNo ratings yet

- Exercises (8.1) : 180 Part OneDocument7 pagesExercises (8.1) : 180 Part OneZakaria HasaneenNo ratings yet

- Chapter 4 Suggested HomeworkDocument22 pagesChapter 4 Suggested HomeworkNguyễn Hoàng MyNo ratings yet

- 05 Handout 1Document6 pages05 Handout 1Reanne Mae BilogNo ratings yet

- ACCT 213 ExerciseDocument5 pagesACCT 213 ExerciseMr MDRKHMNo ratings yet

- 3 Process and Job Order Costing System 2019Document8 pages3 Process and Job Order Costing System 2019Abdallah SadikiNo ratings yet

- Job Order Costing Seatwork 3Document2 pagesJob Order Costing Seatwork 3Charie VelasquezNo ratings yet

- Absorption Costing QuestionsDocument10 pagesAbsorption Costing QuestionsJean LeongNo ratings yet

- Solution:: Step: 1 of 7: Job Costing, Accounting For Manufacturing Overhead, Budgeted Rates. The PisanoDocument5 pagesSolution:: Step: 1 of 7: Job Costing, Accounting For Manufacturing Overhead, Budgeted Rates. The PisanoHerry SugiantoNo ratings yet

- BBA211 Vol8 JobCostingDocument10 pagesBBA211 Vol8 JobCostingAnisha SarahNo ratings yet

- AFAR - 11.1-Cost Accounting (Job Order and Process Costing)Document3 pagesAFAR - 11.1-Cost Accounting (Job Order and Process Costing)Daniela AubreyNo ratings yet

- Cost Accounting Job Costing Chapter 4 Charles T Horngrens 13thDocument10 pagesCost Accounting Job Costing Chapter 4 Charles T Horngrens 13thHaris FayyazNo ratings yet

- Module 9 10 ACCTG 31 1Document11 pagesModule 9 10 ACCTG 31 1GESPEJO, JC SHEEN O.No ratings yet

- Costing 2 Material - 014417Document40 pagesCosting 2 Material - 014417sirjamtech36No ratings yet

- JOB Order CostingDocument4 pagesJOB Order CostingWag NasabiNo ratings yet

- Chapter 10 Answer PDFDocument13 pagesChapter 10 Answer PDFshaneNo ratings yet

- Exercises Lesson 3Document2 pagesExercises Lesson 3Nino LANo ratings yet

- AB CA 20-1 Kuis - 4 PDFDocument1 pageAB CA 20-1 Kuis - 4 PDFYogie YaditraNo ratings yet

- AME - 2022 - Tutorial 4 - SolutionsDocument24 pagesAME - 2022 - Tutorial 4 - SolutionsjjpasemperNo ratings yet

- ACCT3203 Contemporary Managerial Accounting: Lecture Illustration Examples With SolutionsDocument11 pagesACCT3203 Contemporary Managerial Accounting: Lecture Illustration Examples With SolutionsJingwen YangNo ratings yet

- Class Case 3 - Star Engineering CompanyDocument3 pagesClass Case 3 - Star Engineering Company9ry5gsghybNo ratings yet

- Product CostingDocument16 pagesProduct CostingAyush100% (1)

- Chap 4 Job CostingDocument9 pagesChap 4 Job CostingWadiah AkbarNo ratings yet

- Cma Adnan Rashid Complete NotesDocument541 pagesCma Adnan Rashid Complete NotesHAREEM25% (4)

- Accounting For Manufacturing OverheadDocument9 pagesAccounting For Manufacturing OverheadKenzel lawasNo ratings yet

- Job Order CostingDocument51 pagesJob Order CostingKenneth TallmanNo ratings yet

- No. 4-20-21 Page 138-139Document6 pagesNo. 4-20-21 Page 138-139Nemalai VitalNo ratings yet

- Chapter 3 Exercises - ABC SystemDocument2 pagesChapter 3 Exercises - ABC SystemMandy KhouryNo ratings yet

- No. 4-31,4-32,4-33 Page 143-144Document12 pagesNo. 4-31,4-32,4-33 Page 143-144Nemalai VitalNo ratings yet

- 5Document46 pages5Navindra JaggernauthNo ratings yet

- Quiz1 AllDocument8 pagesQuiz1 AllanxiaaNo ratings yet

- 4-18 Page 125 Laguna Mission Actual Costs Model ModelDocument9 pages4-18 Page 125 Laguna Mission Actual Costs Model ModelMisty Dawn BancroftNo ratings yet

- Chapter 2 HomeworkDocument2 pagesChapter 2 HomeworkAliya KainazarovaNo ratings yet

- Tutorial Topic 3 Overhead CostingDocument5 pagesTutorial Topic 3 Overhead CostingPuneetNo ratings yet

- Jetter Engine Corporation Casting Department Cost of Production Report For February Materials Labor Started in Process This Period Quantity ScheduleDocument9 pagesJetter Engine Corporation Casting Department Cost of Production Report For February Materials Labor Started in Process This Period Quantity SchedulePricilla PutriNo ratings yet

- Tutorial 5Document7 pagesTutorial 5YANG YUN RUINo ratings yet

- Costaccounting IIDocument255 pagesCostaccounting IIAbith MathewNo ratings yet

- Assignment Cover Sheet: Northrise UniversityDocument6 pagesAssignment Cover Sheet: Northrise UniversitySapcon ThePhoenixNo ratings yet

- CAC C5M1 Accounting For Factory OverheadDocument6 pagesCAC C5M1 Accounting For Factory OverheadKyla Mae AllamNo ratings yet

- 6 - Accounting For Factory OverheadDocument10 pages6 - Accounting For Factory OverheadChris Aruh BorsalinaNo ratings yet

- Ma As2Document6 pagesMa As2Omar AbidNo ratings yet

- Midterm - Quiz - AEC6Document4 pagesMidterm - Quiz - AEC6aprilNo ratings yet

- FA2 - ExcelDocument1 pageFA2 - ExcelGretchen MontoyaNo ratings yet

- Skema PSPM 16-17 Aa025Document4 pagesSkema PSPM 16-17 Aa025Dehey KNo ratings yet

- Lecture-7 Overhead (Part 5) PDFDocument10 pagesLecture-7 Overhead (Part 5) PDFNazmul-Hassan Sumon100% (5)

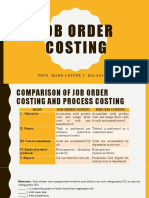

- Job Order Costing: Prof. Mark Lester T. Balasa, CpaDocument24 pagesJob Order Costing: Prof. Mark Lester T. Balasa, CpaNah HamzaNo ratings yet

- Production Departments Direct Labor Rate Manufacturing Overhead Application RatesDocument10 pagesProduction Departments Direct Labor Rate Manufacturing Overhead Application RatesSano ManjiroNo ratings yet

- IPO - Market Update - Apr'2024Document96 pagesIPO - Market Update - Apr'2024Samim Al RashidNo ratings yet

- Macroeconomics: Ninth Canadian EditionDocument44 pagesMacroeconomics: Ninth Canadian EditionUzma KhanNo ratings yet

- A Marxist Analysis of The Characters of Shrek 2Document9 pagesA Marxist Analysis of The Characters of Shrek 2Zeynep Didem KöseNo ratings yet

- Account StatementDocument12 pagesAccount StatementSaurav RaiNo ratings yet

- Daily Report (Hidar 23 2016)Document4 pagesDaily Report (Hidar 23 2016)girmay.filmon5No ratings yet

- SA2 G8 Sample Paper MathDocument5 pagesSA2 G8 Sample Paper MathXkasper GamingNo ratings yet

- Consulting Math Drills - Chart Questions v5Document50 pagesConsulting Math Drills - Chart Questions v5FTU Ngo Thi Van Anh100% (2)

- Break Even MathDocument2 pagesBreak Even MathMuhammad Akmal HossainNo ratings yet

- 54e1 60e1 Railway Turnouts Techspec WebDocument36 pages54e1 60e1 Railway Turnouts Techspec WebShah SudAaisNo ratings yet

- C4 Nitro Scalping Part 1Document98 pagesC4 Nitro Scalping Part 1aaaaNo ratings yet

- VJT Engineering Solutions PVT LTD: Proforma InvoiceDocument2 pagesVJT Engineering Solutions PVT LTD: Proforma InvoiceGanga DharNo ratings yet

- Rectification of ErrorsDocument22 pagesRectification of ErrorsMonica Marimuthu100% (1)

- Assume The Same Information For The Pacific Boat Company As in Problem 10Document2 pagesAssume The Same Information For The Pacific Boat Company As in Problem 10Elliot RichardNo ratings yet

- Capsim Tips and TricksDocument4 pagesCapsim Tips and TricksAlyNo ratings yet

- BillDocument1 pageBillSunil KumarNo ratings yet

- 3 Activity Cost BehaviourDocument49 pages3 Activity Cost BehaviourTheresia RumsowekNo ratings yet

- "Mero Share" Application Form: Æd) /F) Z) O/æ SF) ) JF LNGSF) Nflu LGJ) BG KMF/FDDocument2 pages"Mero Share" Application Form: Æd) /F) Z) O/æ SF) ) JF LNGSF) Nflu LGJ) BG KMF/FDANKITNo ratings yet

- LLP SolutionDocument22 pagesLLP SolutionOm JogiNo ratings yet

- Assignment 3 - AccountingDocument5 pagesAssignment 3 - AccountingGulzar JamalNo ratings yet

- Steel MidtermDocument3 pagesSteel MidtermDave JarangueNo ratings yet

- FB Part Bill-7 of Protik Fine Ceramics Factory BuildingDocument7 pagesFB Part Bill-7 of Protik Fine Ceramics Factory BuildingShafiul AlamNo ratings yet

- Second Term Activity 1Document4 pagesSecond Term Activity 1shuntrixieNo ratings yet

- MV CFA Institute Investment FoundationsDocument5 pagesMV CFA Institute Investment FoundationsDavid D'souzaNo ratings yet

- IPWEA Asset - Management - Plan - 2014Document284 pagesIPWEA Asset - Management - Plan - 2014KhairahMukhlisahHertantoNo ratings yet

- Economic Analysis and The Psychology of Utility - Aplications To Compensation PolicyDocument7 pagesEconomic Analysis and The Psychology of Utility - Aplications To Compensation PolicyCamiloPiñerosTorresNo ratings yet

- ECO111 - Test 01 - Individual Assignment 01Document2 pagesECO111 - Test 01 - Individual Assignment 01Hoang Phi Khanh QP2664No ratings yet

- GP English 2015 PDFDocument436 pagesGP English 2015 PDFwolfwbearwNo ratings yet

- Session 3Document12 pagesSession 3Julie ArnaudNo ratings yet

- Some People Believe That The Rapid Increase in Population These Days Is Unsustainable and Will Eventually Lead To A Global CrisisDocument4 pagesSome People Believe That The Rapid Increase in Population These Days Is Unsustainable and Will Eventually Lead To A Global CrisisAmir Raza FscNo ratings yet

- F5 Variances TestDocument5 pagesF5 Variances Testv0524 vNo ratings yet