You might also like

- Grading System (Refer To Course Plan) Forms of Business Sole ProprietorshipDocument24 pagesGrading System (Refer To Course Plan) Forms of Business Sole ProprietorshipDANIELLE TORRANCE ESPIRITUNo ratings yet

- Far0 MidtermDocument12 pagesFar0 MidtermSophia LampaNo ratings yet

- A Brief Introduction To Accounting: Submitted BY Aditya KapoorDocument18 pagesA Brief Introduction To Accounting: Submitted BY Aditya KapoorLLYOD FRANCIS LAYLAYNo ratings yet

- Fundamentals in Accounting - Chapter - 1-2Document18 pagesFundamentals in Accounting - Chapter - 1-2bonao.maryangelieNo ratings yet

- CHAPTER 1 (Lecture Notes)Document20 pagesCHAPTER 1 (Lecture Notes)Nor Farhanah NanaNo ratings yet

- ACCA102 - Midterm Reviewer Part 1Document1 pageACCA102 - Midterm Reviewer Part 1Fuhoe NekoNo ratings yet

- Reviewer Chapter 1 - Book 1 - Comprehensive ExamDocument5 pagesReviewer Chapter 1 - Book 1 - Comprehensive ExamKrizel Dixie ParraNo ratings yet

- Notes 1: "Accounting Is The Language of Business."Document4 pagesNotes 1: "Accounting Is The Language of Business."Krissha GalonNo ratings yet

- Fabm12 1ST QTRDocument4 pagesFabm12 1ST QTRAraNo ratings yet

- 5 Short Term FinancingDocument27 pages5 Short Term FinancingJNo ratings yet

- Financial AccountingDocument17 pagesFinancial AccountingAnusha EnigallaNo ratings yet

- Accounting Essentials Chapter 1 SynthesisDocument3 pagesAccounting Essentials Chapter 1 SynthesisdaraNo ratings yet

- Basic Accounting Concepts and PrinciplesDocument16 pagesBasic Accounting Concepts and PrinciplesRenmar CruzNo ratings yet

- Slide of Session 1-2Document32 pagesSlide of Session 1-2tranhlthNo ratings yet

- Corporatesecretarialservices PDFDocument8 pagesCorporatesecretarialservices PDFViswanathan RajagopalanNo ratings yet

- 1st Periodical Exam in Fundamentals of Accountancy and Business Management 1 ReviewerDocument9 pages1st Periodical Exam in Fundamentals of Accountancy and Business Management 1 ReviewerJaderick BalboaNo ratings yet

- Introduction To AccountingDocument17 pagesIntroduction To AccountingSiddeq HalimNo ratings yet

- Mariz Delos Santos - Fincon - 31-BFM-01Document7 pagesMariz Delos Santos - Fincon - 31-BFM-01Tine Delos SantosNo ratings yet

- Mariz Delos Santos - Fincon - 31-BFM-01Document7 pagesMariz Delos Santos - Fincon - 31-BFM-01Tine Delos SantosNo ratings yet

- ACC106 Chapter 1Document20 pagesACC106 Chapter 1ErynNo ratings yet

- FAR101-31 - Corporation Formation P1Document14 pagesFAR101-31 - Corporation Formation P1jacelespinosa64No ratings yet

- AIS Chapter 5 Access and ControlDocument5 pagesAIS Chapter 5 Access and ControltesfayeNo ratings yet

- ACC117 - Chapter 1 - Introduction To AccountingDocument28 pagesACC117 - Chapter 1 - Introduction To AccountingFlix HusniNo ratings yet

- Financial Accounting For Managers: Shailesh PeriwalDocument7 pagesFinancial Accounting For Managers: Shailesh PeriwalNatasha DassNo ratings yet

- Solutions Manual: Introduction To AccountingDocument5 pagesSolutions Manual: Introduction To AccountingAlison JcNo ratings yet

- The Accounting Environment and Accounting FrameworkDocument2 pagesThe Accounting Environment and Accounting FrameworkLing lingNo ratings yet

- Chapter 2Document50 pagesChapter 2mokeNo ratings yet

- 11 12 PDFDocument2 pages11 12 PDFDANIELLE TORRANCE ESPIRITUNo ratings yet

- Accountig 101Document6 pagesAccountig 101GBierneza, Angel Babes P.No ratings yet

- Financial AccountingDocument11 pagesFinancial Accountingkaiaav.i09No ratings yet

- Cost Accounting (Chapter 1-3)Document5 pagesCost Accounting (Chapter 1-3)eunice0% (1)

- Sec Quarter Entrep ReviewerDocument14 pagesSec Quarter Entrep ReviewerSherie Hazzell BasaNo ratings yet

- Financial Management AnalysisDocument11 pagesFinancial Management AnalysisKansha GuptaNo ratings yet

- Financial Accounting and Reporting - FundamentalsDocument8 pagesFinancial Accounting and Reporting - FundamentalsChristine DulutanNo ratings yet

- REVIEWERDocument12 pagesREVIEWEREva Mae LabardaNo ratings yet

- Financial Statements Meaning and CharacteristicsDocument64 pagesFinancial Statements Meaning and CharacteristicsAbhishek Sinha100% (1)

- General Purpose FS Special Purpose FSDocument3 pagesGeneral Purpose FS Special Purpose FSKylie CortezNo ratings yet

- 2021 06 24 Conflict Resolution For FPO ManagementDocument16 pages2021 06 24 Conflict Resolution For FPO ManagementSOURAV ANANDNo ratings yet

- ACC111Document5 pagesACC111Trisha SacmanNo ratings yet

- Chapter 15 MADocument6 pagesChapter 15 MApaulaNo ratings yet

- MODULE 1 NotesDocument3 pagesMODULE 1 NotesJoshua AlvarezNo ratings yet

- MBA 2021 - Pre-LOB - Sessions 1 and 2Document42 pagesMBA 2021 - Pre-LOB - Sessions 1 and 2martinNo ratings yet

- ACC117 - Chapter 1 - Introduction To Accounting PDFDocument25 pagesACC117 - Chapter 1 - Introduction To Accounting PDFirfan ShahrilNo ratings yet

- Financial Decision Making Tools: Financial Statements: Presented By: Dr. Anthony Ly B. Dagang Anthony - Dagang@lccdo - Edu.phDocument31 pagesFinancial Decision Making Tools: Financial Statements: Presented By: Dr. Anthony Ly B. Dagang Anthony - Dagang@lccdo - Edu.phmila dacarNo ratings yet

- Framework Theory - StudentDocument27 pagesFramework Theory - StudentKrushna MateNo ratings yet

- AABE IPSAS Adoption Road Map Presentation To Charities by Dawit MDocument66 pagesAABE IPSAS Adoption Road Map Presentation To Charities by Dawit MGere Tassew100% (1)

- Chap 1 Intro of BookkeepDocument14 pagesChap 1 Intro of BookkeepTan Shu YuinNo ratings yet

- Introduction To Financial AccountingDocument64 pagesIntroduction To Financial AccountingAnonymous HumanNo ratings yet

- Resume of Hasin SadmanDocument3 pagesResume of Hasin Sadmancitfhatil2017No ratings yet

- PAINEL 1 - Transfer Pricing & IntangiblesDocument20 pagesPAINEL 1 - Transfer Pricing & Intangiblesedson souzaNo ratings yet

- Week 1 - Introduction To AccountingDocument34 pagesWeek 1 - Introduction To AccountingAidon StanleyNo ratings yet

- Week 1 - Introduction To AccountingDocument34 pagesWeek 1 - Introduction To AccountingAidon StanleyNo ratings yet

- Finalized Mod 1&2 ReviewerDocument4 pagesFinalized Mod 1&2 ReviewerJoshua AlvarezNo ratings yet

- ATSA Certification Accounting Fact Sheet NQ4Document3 pagesATSA Certification Accounting Fact Sheet NQ4DENISE COLENo ratings yet

- CS Executive Corporate and Management AccountingDocument17 pagesCS Executive Corporate and Management AccountingSuraj Srivatsav.SNo ratings yet

- Screenshot 2022-09-28 at 1.19.27 AMDocument19 pagesScreenshot 2022-09-28 at 1.19.27 AMLabhya GuptaNo ratings yet

- Basic Accounting PrinciplesDocument11 pagesBasic Accounting Principlesjackielyn garletNo ratings yet

- Accounting ReviewerDocument25 pagesAccounting ReviewerPrincess Marie JuanNo ratings yet

- Projman (Ca51029)Document17 pagesProjman (Ca51029)DANIELLE TORRANCE ESPIRITUNo ratings yet

- Pre-Numbered Documents, Special Journals, Subsidiary LedgersDocument2 pagesPre-Numbered Documents, Special Journals, Subsidiary LedgersDANIELLE TORRANCE ESPIRITUNo ratings yet

- 11 12 PDFDocument2 pages11 12 PDFDANIELLE TORRANCE ESPIRITUNo ratings yet

- 1 2 PDFDocument2 pages1 2 PDFDANIELLE TORRANCE ESPIRITUNo ratings yet

- AIS Reviewer 5Document2 pagesAIS Reviewer 5DANIELLE TORRANCE ESPIRITUNo ratings yet

- Read-Ph 1st Term NotesDocument3 pagesRead-Ph 1st Term NotesDANIELLE TORRANCE ESPIRITUNo ratings yet

- Man-Sci 1st Term NotesDocument11 pagesMan-Sci 1st Term NotesDANIELLE TORRANCE ESPIRITUNo ratings yet

- Und - Self 1st Term NotesDocument46 pagesUnd - Self 1st Term NotesDANIELLE TORRANCE ESPIRITUNo ratings yet

- Path-Fit 1ST Term NotesDocument2 pagesPath-Fit 1ST Term NotesDANIELLE TORRANCE ESPIRITUNo ratings yet

- Ele Imhpssdp 1ST Term NotesDocument7 pagesEle Imhpssdp 1ST Term NotesDANIELLE TORRANCE ESPIRITUNo ratings yet

- Readings in Philippine History o o oDocument3 pagesReadings in Philippine History o o oDANIELLE TORRANCE ESPIRITUNo ratings yet

- Freshmen Orientation PPT AY21 22 For Distribution To StudentsDocument78 pagesFreshmen Orientation PPT AY21 22 For Distribution To StudentsDANIELLE TORRANCE ESPIRITUNo ratings yet

- Man-Econ 1ST Term NotesDocument4 pagesMan-Econ 1ST Term NotesDANIELLE TORRANCE ESPIRITUNo ratings yet

- Africa Fintech Rising SummitDocument15 pagesAfrica Fintech Rising Summitace187No ratings yet

- Module 1, Assessment 1Document31 pagesModule 1, Assessment 1praveena100% (2)

- Resume of KarencoslinDocument3 pagesResume of Karencoslinapi-24131152No ratings yet

- Account Transactions: Winnie VillanuevaDocument14 pagesAccount Transactions: Winnie VillanuevaPaula Bautista100% (7)

- Retail Banking SystemsDocument4 pagesRetail Banking Systemssheik abdullahNo ratings yet

- Opinio New CommissionDocument3 pagesOpinio New CommissionAbhishek GuptaNo ratings yet

- ICICI BANK - Rural Finance Provided by ICICI BankDocument41 pagesICICI BANK - Rural Finance Provided by ICICI BankChaturvedi DivyanshuNo ratings yet

- Department of Labor: 96 19484Document5 pagesDepartment of Labor: 96 19484USA_DepartmentOfLaborNo ratings yet

- AmsaiDocument1 pageAmsaiDidi MiiraNo ratings yet

- Comparative Analysis of Retail Loan Provided by Axis Bank & Other BanksDocument59 pagesComparative Analysis of Retail Loan Provided by Axis Bank & Other Banksvivekgaurthestud93% (14)

- Comprehensive Problem-Analysis of TransactionDocument43 pagesComprehensive Problem-Analysis of TransactionJoanna DandasanNo ratings yet

- 24.06.2019 - 45TGZPXA GEDA ProformaDocument2 pages24.06.2019 - 45TGZPXA GEDA ProformaSisay TakeleNo ratings yet

- Company Paystub Salary Slip Template Free Word FormatDocument1 pageCompany Paystub Salary Slip Template Free Word FormatdilipomiNo ratings yet

- Beginning InventoryDocument10 pagesBeginning InventoryMegersa DinsaNo ratings yet

- Karakteristik Uang Elektronik Dalam Sistem PembayaranDocument33 pagesKarakteristik Uang Elektronik Dalam Sistem PembayaranDicky KurniawanNo ratings yet

- For InterviewsDocument68 pagesFor InterviewsAlfonso Joel GonzalesNo ratings yet

- Lesson 2 Quiz MaterialDocument4 pagesLesson 2 Quiz Materiallinkin soyNo ratings yet

- Program For FinTECH Summit 2021 1639535495Document4 pagesProgram For FinTECH Summit 2021 1639535495ArisNo ratings yet

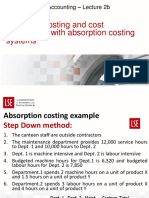

- Job-Order Costing and Cost Assignment With Absorption Costing SystemsDocument50 pagesJob-Order Costing and Cost Assignment With Absorption Costing SystemsAnh Quan NguyenNo ratings yet

- FAR 1 - Midterm - Practice Questions 3Document2 pagesFAR 1 - Midterm - Practice Questions 3Yanela YishaNo ratings yet

- Iop HDFC LTDDocument72 pagesIop HDFC LTDSimreen HuddaNo ratings yet

- A - Updated Price List & Payment BW Food Court 10012020Document8 pagesA - Updated Price List & Payment BW Food Court 10012020sishir mandalNo ratings yet

- M/s Rishabh Creations Sikka Knitting FabDocument1 pageM/s Rishabh Creations Sikka Knitting FabVarun AgarwalNo ratings yet

- Test Bank Financial Markets and Institutions 6th Edition Saunders PDFDocument58 pagesTest Bank Financial Markets and Institutions 6th Edition Saunders PDFRa'fat Jallad100% (1)

- Investment Analysis and Portfolio Management: Frank K. Reilly & Keith C. BrownDocument65 pagesInvestment Analysis and Portfolio Management: Frank K. Reilly & Keith C. BrownWhy you want to knowNo ratings yet

- Financial & Managerial Accounting Mbas: Oanhnguyenth231Document64 pagesFinancial & Managerial Accounting Mbas: Oanhnguyenth231Hồng LongNo ratings yet

- Abm-12 Midterm ExamDocument4 pagesAbm-12 Midterm ExamMich Valencia100% (2)

- Forex Operations: Prof S P GargDocument25 pagesForex Operations: Prof S P GargProf S P Garg100% (2)

- The Indian CRM MarketDocument6 pagesThe Indian CRM MarketChethan KumarNo ratings yet

- Layers Egg Production Business Plan FinancialsDocument11 pagesLayers Egg Production Business Plan FinancialsTinashe RunganoNo ratings yet

- Getting to Yes: How to Negotiate Agreement Without Giving InFrom EverandGetting to Yes: How to Negotiate Agreement Without Giving InRating: 4 out of 5 stars4/5 (652)

- The ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!From EverandThe ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!Rating: 4.5 out of 5 stars4.5/5 (14)

- I Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)From EverandI Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)Rating: 4.5 out of 5 stars4.5/5 (14)

- A Beginners Guide to QuickBooks Online 2023: A Step-by-Step Guide and Quick Reference for Small Business Owners, Churches, & Nonprofits to Track their Finances and Master QuickBooks OnlineFrom EverandA Beginners Guide to QuickBooks Online 2023: A Step-by-Step Guide and Quick Reference for Small Business Owners, Churches, & Nonprofits to Track their Finances and Master QuickBooks OnlineNo ratings yet

- The Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindFrom EverandThe Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindRating: 5 out of 5 stars5/5 (231)

- The Accounting Game: Learn the Basics of Financial Accounting - As Easy as Running a Lemonade Stand (Basics for Entrepreneurs and Small Business Owners)From EverandThe Accounting Game: Learn the Basics of Financial Accounting - As Easy as Running a Lemonade Stand (Basics for Entrepreneurs and Small Business Owners)Rating: 4 out of 5 stars4/5 (33)

- Purchasing, Inventory, and Cash Disbursements: Common Frauds and Internal ControlsFrom EverandPurchasing, Inventory, and Cash Disbursements: Common Frauds and Internal ControlsRating: 5 out of 5 stars5/5 (1)

- The E-Myth Chief Financial Officer: Why Most Small Businesses Run Out of Money and What to Do About ItFrom EverandThe E-Myth Chief Financial Officer: Why Most Small Businesses Run Out of Money and What to Do About ItRating: 4.5 out of 5 stars4.5/5 (14)

- Your Amazing Itty Bitty(R) Personal Bookkeeping BookFrom EverandYour Amazing Itty Bitty(R) Personal Bookkeeping BookNo ratings yet

- How to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)From EverandHow to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)Rating: 4.5 out of 5 stars4.5/5 (5)

- Accounting 101: From Calculating Revenues and Profits to Determining Assets and Liabilities, an Essential Guide to Accounting BasicsFrom EverandAccounting 101: From Calculating Revenues and Profits to Determining Assets and Liabilities, an Essential Guide to Accounting BasicsRating: 4 out of 5 stars4/5 (7)

- How to Measure Anything: Finding the Value of "Intangibles" in BusinessFrom EverandHow to Measure Anything: Finding the Value of "Intangibles" in BusinessRating: 4.5 out of 5 stars4.5/5 (28)

- Accounting For Small Businesses QuickStart Guide: Understanding Accounting For Your Sole Proprietorship, Startup, & LLCFrom EverandAccounting For Small Businesses QuickStart Guide: Understanding Accounting For Your Sole Proprietorship, Startup, & LLCRating: 5 out of 5 stars5/5 (1)

- Tax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesFrom EverandTax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesNo ratings yet

- Overcoming Underearning(TM): A Simple Guide to a Richer LifeFrom EverandOvercoming Underearning(TM): A Simple Guide to a Richer LifeRating: 4 out of 5 stars4/5 (21)

- Financial Accounting For Dummies: 2nd EditionFrom EverandFinancial Accounting For Dummies: 2nd EditionRating: 5 out of 5 stars5/5 (10)

- Ratio Analysis Fundamentals: How 17 Financial Ratios Can Allow You to Analyse Any Business on the PlanetFrom EverandRatio Analysis Fundamentals: How 17 Financial Ratios Can Allow You to Analyse Any Business on the PlanetRating: 4.5 out of 5 stars4.5/5 (14)

- Start, Study and Pass The CPA Exam FAST - Proven 8 Step CPA Exam Study PlaybookFrom EverandStart, Study and Pass The CPA Exam FAST - Proven 8 Step CPA Exam Study PlaybookRating: 5 out of 5 stars5/5 (4)

- Warren Buffett and the Interpretation of Financial Statements: The Search for the Company with a Durable Competitive AdvantageFrom EverandWarren Buffett and the Interpretation of Financial Statements: The Search for the Company with a Durable Competitive AdvantageRating: 4.5 out of 5 stars4.5/5 (109)

- The Credit Formula: The Guide To Building and Rebuilding Lendable CreditFrom EverandThe Credit Formula: The Guide To Building and Rebuilding Lendable CreditRating: 5 out of 5 stars5/5 (1)

- Finance Basics (HBR 20-Minute Manager Series)From EverandFinance Basics (HBR 20-Minute Manager Series)Rating: 4.5 out of 5 stars4.5/5 (32)

- Accounting Principles: Learn The Simple and Effective Methods of Basic Accounting And Bookkeeping Using This comprehensive Guide for Beginners(quick-books,made simple,easy,managerial,finance)From EverandAccounting Principles: Learn The Simple and Effective Methods of Basic Accounting And Bookkeeping Using This comprehensive Guide for Beginners(quick-books,made simple,easy,managerial,finance)Rating: 4.5 out of 5 stars4.5/5 (5)