You might also like

- FSDocument44 pagesFSMaria Beatriz Aban Munda100% (2)

- Chart of Accounts Assets Liabilities Owner'S Equity Income ExpensesDocument2 pagesChart of Accounts Assets Liabilities Owner'S Equity Income ExpensesErika Bucao100% (1)

- Financial Accounting Ii Sample QuizDocument2 pagesFinancial Accounting Ii Sample QuizThea FloresNo ratings yet

- Financial Accounting and ReportingDocument1 pageFinancial Accounting and ReportingPaula BautistaNo ratings yet

- Problem 3 ACCA101Document3 pagesProblem 3 ACCA101Nicole FidelsonNo ratings yet

- Worksheet AssignmentDocument2 pagesWorksheet AssignmentLyca MaeNo ratings yet

- Adjusting Entries FarDocument2 pagesAdjusting Entries FarKylha BalmoriNo ratings yet

- ACC 1 Quiz No. 14 Answer KeyDocument9 pagesACC 1 Quiz No. 14 Answer Keynicole bancoroNo ratings yet

- Short Case ActivitiesDocument2 pagesShort Case ActivitiesRaff LesiaaNo ratings yet

- Answer 1Document7 pagesAnswer 1Mylene HeragaNo ratings yet

- Journalizing Merchandising TransactionsDocument3 pagesJournalizing Merchandising TransactionsMarian Augelio PolancoNo ratings yet

- Trial Balance - Daria TolentinoDocument1 pageTrial Balance - Daria TolentinoShaira Nicole VasquezNo ratings yet

- Balance Sheet Bella EnterprisesDocument2 pagesBalance Sheet Bella EnterprisesmarivicNo ratings yet

- Business TransactionsDocument6 pagesBusiness TransactionsMarlyn Joy Yacon100% (1)

- General Ledger - Adrianne, Mendoza-BSBA-1 BLK BDocument6 pagesGeneral Ledger - Adrianne, Mendoza-BSBA-1 BLK BJaks ExplorerNo ratings yet

- Fabm 1 Reviewer Q1Document8 pagesFabm 1 Reviewer Q1raydel dimaanoNo ratings yet

- Assets Equity LiabilitiesDocument2 pagesAssets Equity LiabilitiesMathew VisarraNo ratings yet

- LedgerDocument3 pagesLedgerAnonnNo ratings yet

- Accounting 1Document16 pagesAccounting 1Rommel Angelo AgacitaNo ratings yet

- Recording Transactions in A Financial Transaction WorksheetDocument1 pageRecording Transactions in A Financial Transaction WorksheetSHENo ratings yet

- Learning Task 2 Financial Statements of Rosalina Besario SurveyorsDocument6 pagesLearning Task 2 Financial Statements of Rosalina Besario SurveyorsNeil Matundan100% (1)

- Sample ProblemDocument6 pagesSample ProblemKen Ashley100% (1)

- General Journal, GeveraDocument2 pagesGeneral Journal, GeveraFeiya LiuNo ratings yet

- Assignment Adjusting EntriesDocument2 pagesAssignment Adjusting EntriesKim Patrick VictoriaNo ratings yet

- Holy Cross of Davao College: Other Campuses: Camudmud (IGACOS), Bajada (SOS Drive)Document3 pagesHoly Cross of Davao College: Other Campuses: Camudmud (IGACOS), Bajada (SOS Drive)Haries Vi Traboc Micolob100% (1)

- Worksheet and Financial Statement 4Document21 pagesWorksheet and Financial Statement 4Bhebz Erin MaeNo ratings yet

- Chapter 6 Win Ballada 2019Document7 pagesChapter 6 Win Ballada 2019Rea Mariz JordanNo ratings yet

- Adjusting Entries ExampleDocument5 pagesAdjusting Entries ExampleSiak Ni LynnLadyNo ratings yet

- Fabm 1 ExamDocument2 pagesFabm 1 ExamJasfer Niño100% (1)

- FABM Assignment WS FS P C TB 1Document34 pagesFABM Assignment WS FS P C TB 1memae0044No ratings yet

- Comprehensive Illustrative ProblemDocument2 pagesComprehensive Illustrative ProblemLyssa Marie Avenido GuelosNo ratings yet

- Financial Transaction WorksheetDocument6 pagesFinancial Transaction WorksheetAnya DaniellaNo ratings yet

- Financial WorksheetDocument6 pagesFinancial WorksheetCelyn DeañoNo ratings yet

- MerchandisingDocument11 pagesMerchandisingAIRA NHAIRE MECATE100% (1)

- John Bala Maps Worksheet December 31, 2015 Account Title Unadjusted Trial Balance Adjustments Debit Credit Debit CreditDocument3 pagesJohn Bala Maps Worksheet December 31, 2015 Account Title Unadjusted Trial Balance Adjustments Debit Credit Debit CreditJessie ForpublicuseNo ratings yet

- Quiz SolutionDocument3 pagesQuiz SolutionKim Patrick VictoriaNo ratings yet

- Laurente Cleaning Services LedgerDocument3 pagesLaurente Cleaning Services LedgerAriel Palay100% (1)

- Basic Accounting ModelDocument3 pagesBasic Accounting Modeldlinds2X1No ratings yet

- Managerial Economics ReviewerDocument26 pagesManagerial Economics ReviewerAlyssa Faith NiangarNo ratings yet

- Accounting For Sole Proprietorship Problem3-6Document3 pagesAccounting For Sole Proprietorship Problem3-6Rocel Domingo100% (1)

- Total: Nancy Mulles Data Encoders May 15 2018Document6 pagesTotal: Nancy Mulles Data Encoders May 15 2018Tashnim AreejNo ratings yet

- Group 6Document6 pagesGroup 6Love KarenNo ratings yet

- General Journal: Date Account Titles and Explanation Ref Debit CreditDocument17 pagesGeneral Journal: Date Account Titles and Explanation Ref Debit CreditPrecious NosaNo ratings yet

- CO VallejoDocument9 pagesCO VallejoTeyangNo ratings yet

- Resuento - Ulob ActivitiesDocument16 pagesResuento - Ulob Activitiesemem resuentoNo ratings yet

- Bank RecolonizationDocument1 pageBank Recolonizationasma100% (1)

- Special JournalDocument7 pagesSpecial JournalJohn Christopher Sta AnaNo ratings yet

- Accbp100 2nd Exam Part 1Document2 pagesAccbp100 2nd Exam Part 1emem resuento100% (1)

- BuenaventuraBSA1B Problems1 4 Pages 410 413Document37 pagesBuenaventuraBSA1B Problems1 4 Pages 410 413AnonnNo ratings yet

- Chapter 9 Accounting Cycle of A Service BusinessDocument59 pagesChapter 9 Accounting Cycle of A Service BusinessArlyn Ragudos BSA1No ratings yet

- Chapter 1 & 2Document13 pagesChapter 1 & 2Ali100% (1)

- Adjusting EntriesDocument2 pagesAdjusting Entriesitsayuhthing100% (1)

- Practice Problem 11.0: Name Date Course/Year ScoreDocument5 pagesPractice Problem 11.0: Name Date Course/Year ScoreCatherine GonzalesNo ratings yet

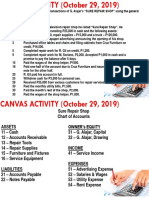

- Canvas Activity - Journalizing - Oct - 29 PDFDocument2 pagesCanvas Activity - Journalizing - Oct - 29 PDFJian Francisco100% (2)

- C3 - Problem 11 - Journalizing TransactionsDocument2 pagesC3 - Problem 11 - Journalizing TransactionsLorence John ImperialNo ratings yet

- Account Titles and Its ElementsDocument3 pagesAccount Titles and Its ElementsJeb PampliegaNo ratings yet

- Comprehensive Problem - MerchandisingDocument12 pagesComprehensive Problem - MerchandisingLaura OliviaNo ratings yet

- Tesorero, Princess Kelly V, HRM 1-4 Baen m9Document6 pagesTesorero, Princess Kelly V, HRM 1-4 Baen m9Kelly TesoreroNo ratings yet

- ACCTG CYCLE Comprehensive ProblmDocument12 pagesACCTG CYCLE Comprehensive ProblmMaria Nicole OasinNo ratings yet

- FAA - Unit 1 - 2021Document11 pagesFAA - Unit 1 - 2021Pranjal ChopraNo ratings yet

- CA-Ipcc Old Course: Advanced AccountingDocument125 pagesCA-Ipcc Old Course: Advanced AccountingAruna Rajappa100% (1)

- Advanced Financial Accounting and Reporting: ConceptualDocument6 pagesAdvanced Financial Accounting and Reporting: ConceptualYeji BabeNo ratings yet

- 704Document3 pages704Bhoomi GhariwalaNo ratings yet

- Lesson 9 - JOURNALIZING EXTERNAL TRANSACTIONSDocument6 pagesLesson 9 - JOURNALIZING EXTERNAL TRANSACTIONSMayeng MonayNo ratings yet

- IntAcc 3 Non-Financial LiabilitiesDocument10 pagesIntAcc 3 Non-Financial LiabilitiesKim EllaNo ratings yet

- Financial Modelling CIA 2Document45 pagesFinancial Modelling CIA 2Saloni Jain 1820343No ratings yet

- Data Dukung NS Dan Catatan Atas Laporan KeuanganDocument57 pagesData Dukung NS Dan Catatan Atas Laporan KeuanganHafizd Az ZeinNo ratings yet

- Paper 1: Principles and Practice of AccountingDocument2 pagesPaper 1: Principles and Practice of AccountingrajNo ratings yet

- Tax 101 PDFDocument11 pagesTax 101 PDFEmerson Peralta0% (2)

- Midterm Exam (Regulatory Framework and Legal Issues in Business Law) 2021 - Prof. Gerald SuarezDocument4 pagesMidterm Exam (Regulatory Framework and Legal Issues in Business Law) 2021 - Prof. Gerald SuarezAlexandrea Bella Guillermo67% (3)

- Petition For Settlement of EstateDocument4 pagesPetition For Settlement of EstateSTEPHEN NIKOLAI CRISANGNo ratings yet

- Retire Young Retire RichDocument14 pagesRetire Young Retire RichMeraiya NayanNo ratings yet

- Almario, Khristin Allison Asynch Atp Week 3Document4 pagesAlmario, Khristin Allison Asynch Atp Week 3Khristin AllisonNo ratings yet

- Unit-4 Study MaterialDocument19 pagesUnit-4 Study MaterialSETHUMADHAVAN BNo ratings yet

- Project Report On TATA MOTORS 1Document31 pagesProject Report On TATA MOTORS 1Manoj gajavelliNo ratings yet

- Department of Accountancy: Holy Angel University Intermediate Accounting 1Document9 pagesDepartment of Accountancy: Holy Angel University Intermediate Accounting 1Shania LiwanagNo ratings yet

- Revaluation AccountDocument23 pagesRevaluation Accountsneha sasidharanNo ratings yet

- Comprehension Questions Act 1Document2 pagesComprehension Questions Act 1sama0% (1)

- 2018 SAJC H2 Prelim P1 + SolutionDocument20 pages2018 SAJC H2 Prelim P1 + Solutiontoh tim lamNo ratings yet

- Student Account Charges Explained: BeginDocument6 pagesStudent Account Charges Explained: BeginBobNo ratings yet

- Loan Document 155465Document11 pagesLoan Document 155465Omkar DesaiNo ratings yet

- Partners Current Account 1Document6 pagesPartners Current Account 1Blo MahnNo ratings yet

- Education Loan of Sbi BankDocument52 pagesEducation Loan of Sbi BankRahul SanasNo ratings yet

- Law On Partnership NOTESDocument14 pagesLaw On Partnership NOTESRence MarcoNo ratings yet

- 04-46 Angel Jose Warehousing v. Chelda EnterprisesDocument4 pages04-46 Angel Jose Warehousing v. Chelda EnterprisesGene Charles MagistradoNo ratings yet

- Module 4 - Credit InvestigationDocument37 pagesModule 4 - Credit InvestigationAllan Cris RicafortNo ratings yet

- Ratio Analysis AssignmentDocument39 pagesRatio Analysis AssignmentBarzala CarcarNo ratings yet

- MAF253 SS Common Test May 2022Document7 pagesMAF253 SS Common Test May 2022Nurfatihah JohariNo ratings yet

- Standard, The Conceptual Framework Overrides That StandardDocument6 pagesStandard, The Conceptual Framework Overrides That StandardwivadaNo ratings yet