You might also like

- Port Finance: Interest Rate Market On SolanaDocument11 pagesPort Finance: Interest Rate Market On SolanaMI POCOPHONENo ratings yet

- Anchor: Gold Standard For Passive Income On The Blockchain: Nicholas Platias, Eui Joon Lee, Marco Di Maggio June 2020Document11 pagesAnchor: Gold Standard For Passive Income On The Blockchain: Nicholas Platias, Eui Joon Lee, Marco Di Maggio June 2020giakhanh3989No ratings yet

- L2P Finance Whitepaper0.2Document8 pagesL2P Finance Whitepaper0.2briton336No ratings yet

- Litepaper Bonded Sep 29Document13 pagesLitepaper Bonded Sep 29Optimuz OptimuzNo ratings yet

- Halodao Litepaper Building A Global Stablecoin MarketDocument20 pagesHalodao Litepaper Building A Global Stablecoin MarketTimchosen UzuaNo ratings yet

- Iq Yellow PaperDocument15 pagesIq Yellow PaperAtreyu GreenNo ratings yet

- Interest Rate Swaps (Final)Document35 pagesInterest Rate Swaps (Final)Harish SharmaNo ratings yet

- Attacking The DeFi Ecosystem With Flash Loans For Fun and ProfitDocument29 pagesAttacking The DeFi Ecosystem With Flash Loans For Fun and ProfitPatricio Ibarra GuzmánNo ratings yet

- Aave Protocolo Libro BlancoDocument25 pagesAave Protocolo Libro BlancoJ Peña RuedaNo ratings yet

- We L Nance White PaperDocument9 pagesWe L Nance White PaperSaiyavong MITTHASONENo ratings yet

- OpenZeppelin AaveV3Document18 pagesOpenZeppelin AaveV3vijobo9104No ratings yet

- Libor Forward RatesDocument17 pagesLibor Forward RatesKofikoduahNo ratings yet

- 19 - 1st January 2009 (010109)Document8 pages19 - 1st January 2009 (010109)Chaanakya_cuimNo ratings yet

- Defi Flash LoanDocument25 pagesDefi Flash LoanKarim OubelkacemNo ratings yet

- Gitman - PPT - ch06 Bond ValuationDocument56 pagesGitman - PPT - ch06 Bond ValuationFerry GumilarNo ratings yet

- Cash Money Markets: Minimum Correct Answers For This Module: 6/12Document15 pagesCash Money Markets: Minimum Correct Answers For This Module: 6/12Jovan SsenkandwaNo ratings yet

- Financial Risk Management: A Simple IntroductionFrom EverandFinancial Risk Management: A Simple IntroductionRating: 4.5 out of 5 stars4.5/5 (7)

- Financial Engineering-1 2Document17 pagesFinancial Engineering-1 2Jay KapadiaNo ratings yet

- Re: Blackrock Comments On Proposed Margin Requirements For Uncleared SwapsDocument5 pagesRe: Blackrock Comments On Proposed Margin Requirements For Uncleared SwapsMarketsWikiNo ratings yet

- R45 Derivative Markets and InstrumentsDocument24 pagesR45 Derivative Markets and InstrumentsSumair ChughtaiNo ratings yet

- Providence College School of Business: FIN 417 Fixed Income Securities Fall 2021 Instructor: Matthew CallahanDocument51 pagesProvidence College School of Business: FIN 417 Fixed Income Securities Fall 2021 Instructor: Matthew CallahanAlexander MaffeoNo ratings yet

- Libor Market Model Specification and CalibrationDocument29 pagesLibor Market Model Specification and CalibrationGeorge LiuNo ratings yet

- Whitepaper v1.0Document22 pagesWhitepaper v1.0psastrowardoyoNo ratings yet

- 46Document35 pages46Abhishek GuptaNo ratings yet

- Nu Nu: Jordan Lee September 23, 2014Document15 pagesNu Nu: Jordan Lee September 23, 2014PenNo ratings yet

- AFM 2: Interest Rate Swaps: S Krishnamoorthy:, Cell:9821461488Document24 pagesAFM 2: Interest Rate Swaps: S Krishnamoorthy:, Cell:9821461488Johar MenezesNo ratings yet

- Bond Calculation FormulaDocument37 pagesBond Calculation FormulaPriya KansalNo ratings yet

- QTNHTM - Chapter 3 - Tools For Managing and Hedging Against RiskDocument93 pagesQTNHTM - Chapter 3 - Tools For Managing and Hedging Against RiskVui VũNo ratings yet

- Perspectives in Modelling of PricingDocument52 pagesPerspectives in Modelling of Pricingnil_parkarNo ratings yet

- WhitepaperDocument13 pagesWhitepaperAbhiraj dNo ratings yet

- Chapter-6 Gitman FinanceDocument46 pagesChapter-6 Gitman FinanceShoyeb ImteazNo ratings yet

- Chap 5 Money Bond MarketsDocument37 pagesChap 5 Money Bond MarketsGayatheri PerumalNo ratings yet

- The Yield Protocol: On-Chain Lending With Interest Rate DiscoveryDocument15 pagesThe Yield Protocol: On-Chain Lending With Interest Rate DiscoveryxanderNo ratings yet

- Bill Akron Case Scenario: Exhibit 1 Select Spot and Forward RatesDocument5 pagesBill Akron Case Scenario: Exhibit 1 Select Spot and Forward RatesNGOC NHINo ratings yet

- Two Type of Margins Have Been SpecifiedDocument8 pagesTwo Type of Margins Have Been SpecifiedPraveen KumarNo ratings yet

- International Financial Management PgapteDocument30 pagesInternational Financial Management Pgapterameshmba100% (1)

- Safemoon: A Deflationary Reflection Token With Automated Liquidity AcquisitionDocument3 pagesSafemoon: A Deflationary Reflection Token With Automated Liquidity AcquisitionCamerinside charlyNo ratings yet

- Libor Transition Guide Key Risks and Mit-1Document12 pagesLibor Transition Guide Key Risks and Mit-1KarimFathNo ratings yet

- SwapsDocument44 pagesSwapsAditya Paul SharmaNo ratings yet

- Derivatives - Futures and ForwardsDocument56 pagesDerivatives - Futures and ForwardsSriram VasudevanNo ratings yet

- Swaps Caps BloombergnematnejadDocument10 pagesSwaps Caps BloombergnematnejadZhu YanNo ratings yet

- Defi Lending ProtocolsDocument6 pagesDefi Lending ProtocolsAthanasios TsagkadourasNo ratings yet

- Understanding Asset Swapped Convertible Option Transactions MSDWDocument24 pagesUnderstanding Asset Swapped Convertible Option Transactions MSDWhchan280% (5)

- Module 7 - Bond ValuationDocument37 pagesModule 7 - Bond ValuationMethlyNo ratings yet

- Alpha Lending WhitepaperDocument36 pagesAlpha Lending WhitepaperOlagbemide Kehinde SundayNo ratings yet

- Chapter 5 Securities Operations and Risk ManagementDocument27 pagesChapter 5 Securities Operations and Risk ManagementMRIDUL GOELNo ratings yet

- Investment of BanksDocument2 pagesInvestment of BanksIpsita GuhaNo ratings yet

- Debt Valuation and InterestDocument103 pagesDebt Valuation and InterestTaqiya NadiyaNo ratings yet

- TWAP Oracle Attacks - Easier Done Than SaidDocument8 pagesTWAP Oracle Attacks - Easier Done Than SaidANDREW KIMANINo ratings yet

- FIN 308-Chapter 6-With NotesDocument56 pagesFIN 308-Chapter 6-With NotesrNo ratings yet

- This Section Reviews The Following Asset Liability ManagementDocument8 pagesThis Section Reviews The Following Asset Liability ManagementHAN SUKARMANNo ratings yet

- R52 Fixed Income Markets Issuance Trading and FundingDocument43 pagesR52 Fixed Income Markets Issuance Trading and FundingDiegoNo ratings yet

- CFA® Level II - Derivatives: Forward Markets and ContractsDocument30 pagesCFA® Level II - Derivatives: Forward Markets and ContractsSyedMaazNo ratings yet

- Mat-K 3.2 Lecture Notes: Mathematical Modeling and Optimization With Applications in FinanceDocument40 pagesMat-K 3.2 Lecture Notes: Mathematical Modeling and Optimization With Applications in Financepawan_gurubhaiNo ratings yet

- Demystifying RippleWorks' xCurrent: An XRP Technical Guide: Unpacking the Properties That Enable Seamless Global Transactions: Bridging Borders: XRP's Vision for Faster, Efficient Worldwide Transactions, #3From EverandDemystifying RippleWorks' xCurrent: An XRP Technical Guide: Unpacking the Properties That Enable Seamless Global Transactions: Bridging Borders: XRP's Vision for Faster, Efficient Worldwide Transactions, #3No ratings yet

- Komal Traesury AssignmentDocument11 pagesKomal Traesury AssignmentmanaskaushikNo ratings yet

- Int. Rate Derivatives & It's Application in IndiaDocument52 pagesInt. Rate Derivatives & It's Application in IndiaSachin GadhaveNo ratings yet

- T3TSL - Syndicated Loans - R14Document283 pagesT3TSL - Syndicated Loans - R14tayutaNo ratings yet

- R48 Derivative Markets and InstrumentsDocument179 pagesR48 Derivative Markets and InstrumentsAaliyan Bandealy100% (1)

- Lecture 9 TVM (Practical Applications)Document22 pagesLecture 9 TVM (Practical Applications)Devyansh GuptaNo ratings yet

- Dharani ProjectDocument76 pagesDharani ProjectSUMIT THAKURNo ratings yet

- Fee DetailsDocument8 pagesFee DetailsArchana BakshNo ratings yet

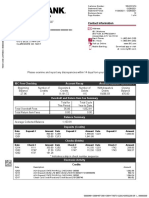

- Bank Account Statement: Mr. John Doe 2 Post Alley, Seattle, WA 98101Document3 pagesBank Account Statement: Mr. John Doe 2 Post Alley, Seattle, WA 98101leeo100% (1)

- Barclays DUS Primer 3-9-2011Document11 pagesBarclays DUS Primer 3-9-2011pratikmhatre123No ratings yet

- Problems To Be Solved in ClassDocument4 pagesProblems To Be Solved in ClassAlp SanNo ratings yet

- A. ConsumableDocument1 pageA. ConsumableKAYE JAVELLANANo ratings yet

- Engineering Economy: Annuity (Continued)Document3 pagesEngineering Economy: Annuity (Continued)Sean Matthew L. OcampoNo ratings yet

- Coldwell Banker Home Buyer's GuidebookDocument25 pagesColdwell Banker Home Buyer's GuidebookLani Rosales100% (2)

- Journal EntriesDocument2 pagesJournal EntriesAmaryNo ratings yet

- G2ADocument12 pagesG2ASivaa RockNo ratings yet

- Tutorial Solution Chap 5Document4 pagesTutorial Solution Chap 5Nurul AriffahNo ratings yet

- Banking Regulation Act-1949 RBI Act-1934 Negotiable Instrument Act-1881Document7 pagesBanking Regulation Act-1949 RBI Act-1934 Negotiable Instrument Act-1881Ashraf AliNo ratings yet

- ThirdPartyRetrieveDocument - Asp 3Document4 pagesThirdPartyRetrieveDocument - Asp 3Elizabeth HilsonNo ratings yet

- Chapter 25: Step by Step Murabaha Financing: Bank ClientDocument3 pagesChapter 25: Step by Step Murabaha Financing: Bank ClientAlton JurahNo ratings yet

- Bonnie Lundbohm - 2025Document5 pagesBonnie Lundbohm - 2025Peter MariluchNo ratings yet

- Yuvaraja'S College Mysore (Autonomous) : Bill ID / Reference Number Student Name Register Number DateDocument2 pagesYuvaraja'S College Mysore (Autonomous) : Bill ID / Reference Number Student Name Register Number DateBADGER I AVINo ratings yet

- Money and Inflation Questions PDFDocument62 pagesMoney and Inflation Questions PDFHabyarimana ProjecteNo ratings yet

- CBP Circular No. 905Document6 pagesCBP Circular No. 905Daniel Danjur Daguman86% (7)

- The Financial Crisis and Policy John H. CochraneDocument6 pagesThe Financial Crisis and Policy John H. Cochraneapi-26186913No ratings yet

- Difference On Bba and MMDocument1 pageDifference On Bba and MMJelena CientaNo ratings yet

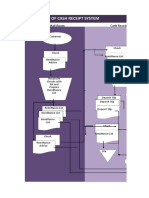

- Flowchart of Cash Receipt System: Mail Room Cash ReceiptsDocument17 pagesFlowchart of Cash Receipt System: Mail Room Cash ReceiptsStephanie Diane SabadoNo ratings yet

- Loan Functions of BanksDocument38 pagesLoan Functions of BanksEunice EsteraNo ratings yet

- Establish and Maintain A Cash Account SystemDocument23 pagesEstablish and Maintain A Cash Account Systemzemen tadesse67% (3)

- Dealing Room OperationDocument43 pagesDealing Room Operationkaashifhassan100% (2)

- TeplateDocument8 pagesTeplatejigyasha oarmarNo ratings yet

- EXIM INDIA BlockchainDocument18 pagesEXIM INDIA BlockchainKrish GopalakrishnanNo ratings yet

- ExhibithDocument21 pagesExhibithlarry-612445No ratings yet

- Top 60 Bank Interview QuestionsDocument12 pagesTop 60 Bank Interview QuestionsRamojeevaNo ratings yet

- Full Name of The BankDocument7 pagesFull Name of The BankRitchyrd CasemNo ratings yet