You might also like

- Chapter 3Document20 pagesChapter 3Nareen RajNo ratings yet

- Professional Accounting PackageDocument72 pagesProfessional Accounting PackageAnmol poudelNo ratings yet

- What Is Accounting???Document15 pagesWhat Is Accounting???Modassar NazarNo ratings yet

- Topic 5 Acc2013Document60 pagesTopic 5 Acc2013yellowcat91No ratings yet

- Topic 3 Recording of Data - Double Entry SystemDocument57 pagesTopic 3 Recording of Data - Double Entry SystemJonisNo ratings yet

- (L) Chapter 7 Trade ReceivablesDocument8 pages(L) Chapter 7 Trade ReceivablesCHZE CHZI CHUAHNo ratings yet

- Chapter 02Document14 pagesChapter 02SHANTANU KHARENo ratings yet

- Session 2 Revenue Recognition AR InventoryDocument41 pagesSession 2 Revenue Recognition AR InventoryNANo ratings yet

- L03 App of Double Entry Principles (P1)Document8 pagesL03 App of Double Entry Principles (P1)calebNo ratings yet

- Accounting For Receivables: Learning ObjectivesDocument68 pagesAccounting For Receivables: Learning ObjectivesDeeb. DeebNo ratings yet

- Effects and Equation-Individual AssignmentDocument8 pagesEffects and Equation-Individual AssignmentAbduzzahir Bin Mohd SaidNo ratings yet

- Accounting For Receivables: Learning ObjectivesDocument66 pagesAccounting For Receivables: Learning ObjectivesSamar BarakehNo ratings yet

- Fa 2 B 10-15Document114 pagesFa 2 B 10-15Muhammad Moaz ZahidNo ratings yet

- Acc106 Chapter Four Textbook Questions Nur Hazani 2020818012Document7 pagesAcc106 Chapter Four Textbook Questions Nur Hazani 2020818012nur hazaniNo ratings yet

- Topic 1.1.1 Additional NotesDocument6 pagesTopic 1.1.1 Additional NotesMei Yi YeoNo ratings yet

- Poa T - 1Document3 pagesPoa T - 1SHEVENA A/P VIJIANNo ratings yet

- Golden Rules of AccountingDocument5 pagesGolden Rules of AccountingVinay ChintamaneniNo ratings yet

- Debit and Credit Rules of AccountingDocument6 pagesDebit and Credit Rules of AccountingsbcluincNo ratings yet

- Basic of Accounts Tally Is A Package: AccountingDocument9 pagesBasic of Accounts Tally Is A Package: AccountingArista TechnologiesNo ratings yet

- Acc102 W1Document47 pagesAcc102 W1Moheb RefaatNo ratings yet

- Double Entry System 2: DR CRDocument22 pagesDouble Entry System 2: DR CRews8iy7jNo ratings yet

- Chap 3 Accounting Classification & Equation (Basic+Expended) - ClassDocument37 pagesChap 3 Accounting Classification & Equation (Basic+Expended) - Classnabkill100% (1)

- Double Entry, General Ledger, Trial BalanceDocument27 pagesDouble Entry, General Ledger, Trial BalancePraween BimsaraNo ratings yet

- Solution Chapter 3Document3 pagesSolution Chapter 3arha_86867820No ratings yet

- Management Accounting 2Document10 pagesManagement Accounting 2Aditya KulkarniNo ratings yet

- CH 09Document27 pagesCH 09Imtiaz PiasNo ratings yet

- 5 - ConceptsDocument10 pages5 - ConceptsAsma GaniNo ratings yet

- 3 Accounting MechanicsDocument50 pages3 Accounting MechanicsVasu Narang100% (1)

- In-Class Exercise Chapter 5Document6 pagesIn-Class Exercise Chapter 5Thomas TermoteNo ratings yet

- CHAP 7 - LECTURER'S NOTES (1) (AutoRecovered)Document11 pagesCHAP 7 - LECTURER'S NOTES (1) (AutoRecovered)ManzMalayaNo ratings yet

- ExcerptDocument10 pagesExcerptyomvzNo ratings yet

- Topic 2-The Double Entry SystemDocument37 pagesTopic 2-The Double Entry Systemirdina amalinNo ratings yet

- Chapter 7 ReceivablesDocument58 pagesChapter 7 ReceivablesMuhammad AmirulNo ratings yet

- Chapter 7 ReceivablesDocument87 pagesChapter 7 ReceivablesLEE WEI LONGNo ratings yet

- RulesDocument10 pagesRuleskainat zahid100% (1)

- Chapter 2Document37 pagesChapter 2Thùy Vân NguyễnNo ratings yet

- Finance Test 2022Document4 pagesFinance Test 2022matheneyah03No ratings yet

- Accounting Group Work 2.Document4 pagesAccounting Group Work 2.Glaze MorazNo ratings yet

- Basic Documentation and Books of Account: Topic 3Document32 pagesBasic Documentation and Books of Account: Topic 3vickramravi16No ratings yet

- CH 09Document69 pagesCH 09Jubaida Naznin Chowdhury JefrinNo ratings yet

- Ledgers and Double-Entry Accounting System: Woods, Chapter 11 Thomas, Chapter 3 & 4Document39 pagesLedgers and Double-Entry Accounting System: Woods, Chapter 11 Thomas, Chapter 3 & 4LAI WEI,No ratings yet

- Ffa W12343Document22 pagesFfa W12343DaddyNo ratings yet

- Lecture Slides - Chapter 9 & 10Document103 pagesLecture Slides - Chapter 9 & 10Phan Đỗ QuỳnhNo ratings yet

- AccountsDocument4 pagesAccountsPranshu BansalNo ratings yet

- Ledger Accounts and Double Entry Course NotesDocument7 pagesLedger Accounts and Double Entry Course Notesshakhawat_cNo ratings yet

- Tally NotesDocument32 pagesTally NotesenuNo ratings yet

- Chapter 4 Acctg For ReceivableDocument27 pagesChapter 4 Acctg For Receivablesyadyna safiaNo ratings yet

- Financial Accounting and AnalysisDocument9 pagesFinancial Accounting and AnalysisYT MotivationNo ratings yet

- Accounting For Managerial Decision MakingDocument31 pagesAccounting For Managerial Decision MakingAshutosh SinghNo ratings yet

- Acc117-Chapter 4-1Document25 pagesAcc117-Chapter 4-1Fadilah JefriNo ratings yet

- Special Lecture 1 Accounting For A Merchandising & Manufacturing Business Learning ObjectivesDocument9 pagesSpecial Lecture 1 Accounting For A Merchandising & Manufacturing Business Learning ObjectivesJenelee Angela MagnoNo ratings yet

- Accounting For Receivables: Learning ObjectivesDocument63 pagesAccounting For Receivables: Learning ObjectivesBayaderNo ratings yet

- 06b Introduction To Financial Accounting and Financial Statements LectureDocument44 pages06b Introduction To Financial Accounting and Financial Statements LectureJoseph IbrahimNo ratings yet

- Principle of Double Entry & Trial Balance: Prepared By: Nurul Hassanah HamzahDocument35 pagesPrinciple of Double Entry & Trial Balance: Prepared By: Nurul Hassanah HamzahNur Amira NadiaNo ratings yet

- Chapter 2Document20 pagesChapter 2chanreaksmeytepNo ratings yet

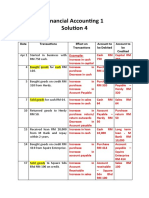

- Financial Accounting 1 - Solution 4Document3 pagesFinancial Accounting 1 - Solution 4mardhiahNo ratings yet

- Double Entry and TB (Part 1)Document9 pagesDouble Entry and TB (Part 1)Aymen Asad KhanNo ratings yet

- Bookkeeping Mock Questions2022 - GG1712Document10 pagesBookkeeping Mock Questions2022 - GG1712Karan KhannaNo ratings yet

- Journal, Ledger, TB & Final AccountsDocument11 pagesJournal, Ledger, TB & Final AccountsSanjay Dutta100% (1)

- Quantitative Methods Quiz 1Document9 pagesQuantitative Methods Quiz 1Hareen JuniorNo ratings yet

- Organizational Behavior (Final Exam Answer)Document1 pageOrganizational Behavior (Final Exam Answer)Hareen JuniorNo ratings yet

- Event ExecutionDocument1 pageEvent ExecutionHareen JuniorNo ratings yet

- Mathematical Methods For Business, Economics & FinanceDocument67 pagesMathematical Methods For Business, Economics & FinanceHareen JuniorNo ratings yet

- Written Test 20%Document12 pagesWritten Test 20%Hareen JuniorNo ratings yet

- Dealing Employees' Emotions and Influence BehaviourDocument3 pagesDealing Employees' Emotions and Influence BehaviourHareen JuniorNo ratings yet

- IB - Mediviron Clininc Pakistan UpdatedDocument14 pagesIB - Mediviron Clininc Pakistan UpdatedHareen JuniorNo ratings yet

- Group Assignment Question 4 - Hui YiDocument2 pagesGroup Assignment Question 4 - Hui YiHareen JuniorNo ratings yet

- BAAB1014 Accounting - (Group 1 Assignment)Document10 pagesBAAB1014 Accounting - (Group 1 Assignment)Hareen Junior100% (1)

- ECONOMICS (International Trade)Document2 pagesECONOMICS (International Trade)Hareen JuniorNo ratings yet

- Chapter 8 InventoriesDocument3 pagesChapter 8 InventoriesHareen JuniorNo ratings yet

- Bafb1023 (Output & Cost)Document2 pagesBafb1023 (Output & Cost)Hareen JuniorNo ratings yet

- Revision Question BAAB1014 May 23-1Document6 pagesRevision Question BAAB1014 May 23-1Hareen JuniorNo ratings yet

- Evaluation and JustificationDocument1 pageEvaluation and JustificationHareen JuniorNo ratings yet

- Revision Set 1Document4 pagesRevision Set 1Hareen JuniorNo ratings yet

- RelationshipCloze W11Document1 pageRelationshipCloze W11Hareen JuniorNo ratings yet

- Business REVISION SET 2 MCQDocument5 pagesBusiness REVISION SET 2 MCQHareen JuniorNo ratings yet

- Fallacies ExerciseDocument2 pagesFallacies ExerciseHareen JuniorNo ratings yet

- November TimetableDocument1 pageNovember TimetableHareen JuniorNo ratings yet

- CAUSE AND EFFECT ESSAY (Sleep Deprivation)Document2 pagesCAUSE AND EFFECT ESSAY (Sleep Deprivation)Hareen JuniorNo ratings yet

- Foundation in Law/Business Assignment Cover SheetDocument18 pagesFoundation in Law/Business Assignment Cover SheetHareen JuniorNo ratings yet

- ImmigrationDocument14 pagesImmigrationHareen JuniorNo ratings yet

- To Inform The Public On Why Malaysia Lives On Low Base Wages. What Are The Provided?Document5 pagesTo Inform The Public On Why Malaysia Lives On Low Base Wages. What Are The Provided?Hareen JuniorNo ratings yet

- Shadow of King SolomonDocument6 pagesShadow of King SolomonHareen JuniorNo ratings yet

- Chapter Review QuestionsDocument7 pagesChapter Review QuestionsHareen JuniorNo ratings yet

- Hartalega Holdings BerhadDocument23 pagesHartalega Holdings BerhadHareen JuniorNo ratings yet

- Script-Study SkillsDocument3 pagesScript-Study SkillsHareen JuniorNo ratings yet

- FIB Sep 2020 Sector and GroupingDocument5 pagesFIB Sep 2020 Sector and GroupingHareen JuniorNo ratings yet

- Communication Skills (Minimum Wages in Malaysia)Document8 pagesCommunication Skills (Minimum Wages in Malaysia)Hareen JuniorNo ratings yet

- Intellectual PropertyDocument6 pagesIntellectual PropertyFe EsperanzaNo ratings yet

- Astm A391-A391m-07Document3 pagesAstm A391-A391m-07NadhiraNo ratings yet

- Ringkasan KesDocument2 pagesRingkasan Kesaz_zafirahNo ratings yet

- Proposed Guidelines For Academic Regalia RentalsDocument2 pagesProposed Guidelines For Academic Regalia Rentalsigp norsuNo ratings yet

- Jurisdiction of Philippine CourtsDocument6 pagesJurisdiction of Philippine CourtsTiny WOnderNo ratings yet

- Emergency Binder ChecklistDocument2 pagesEmergency Binder ChecklistAgustin Peralta100% (1)

- Article On Hindu Undivided Family PDFDocument14 pagesArticle On Hindu Undivided Family PDFprashantkhatanaNo ratings yet

- Liberalism and The American Natural Law TraditionDocument73 pagesLiberalism and The American Natural Law TraditionPiguet Jean-GabrielNo ratings yet

- Historical Development of Land Disputes and Their Implications On Social Cohesion in Nakuru County, KenyaDocument11 pagesHistorical Development of Land Disputes and Their Implications On Social Cohesion in Nakuru County, KenyaInternational Journal of Innovative Science and Research TechnologyNo ratings yet

- Quality Control Review Guide For Single Audits - Final (Dec 2016)Document27 pagesQuality Control Review Guide For Single Audits - Final (Dec 2016)HBL AFGHANISTANNo ratings yet

- Declaration Form: District Police Station Mouza With J. L. No. Khatian No. Plot No. Total Area Area OwnedDocument1 pageDeclaration Form: District Police Station Mouza With J. L. No. Khatian No. Plot No. Total Area Area Ownedalok dasNo ratings yet

- 229-79577 - EN - 10204 - Type - 3 - 2 - Certification - Services.2 Inspection Certification PDFDocument2 pages229-79577 - EN - 10204 - Type - 3 - 2 - Certification - Services.2 Inspection Certification PDFBranza TelemeaNo ratings yet

- Office Functions - SDO - OSDS - v2 PDFDocument6 pagesOffice Functions - SDO - OSDS - v2 PDFtiny aNo ratings yet

- Legmed A (For PDF Reading)Document324 pagesLegmed A (For PDF Reading)Sofia BrondialNo ratings yet

- Bayan v. Zamora, G.R. No. 138570, October 10, 2000Document4 pagesBayan v. Zamora, G.R. No. 138570, October 10, 2000Rea AbonNo ratings yet

- 1 What Is TortDocument8 pages1 What Is TortDonasco Casinoo ChrisNo ratings yet

- AllBeats 133Document101 pagesAllBeats 133Ragnarr FergusonNo ratings yet

- Duterte Approves Mandatory ROTC Senior HighDocument1 pageDuterte Approves Mandatory ROTC Senior HighSteeeeeeeephNo ratings yet

- Ughurs in ChinaDocument8 pagesUghurs in ChinaLeland MurtiffNo ratings yet

- MTD 24A46E729 Chipper-Shredder Owner's ManualDocument20 pagesMTD 24A46E729 Chipper-Shredder Owner's ManualcpprioliNo ratings yet

- America The Story of Us Episode 3 Westward WorksheetDocument1 pageAmerica The Story of Us Episode 3 Westward WorksheetHugh Fox III100% (1)

- Dangerous Drugs Act 1952 (Revised 1980) - Act 234Document80 pagesDangerous Drugs Act 1952 (Revised 1980) - Act 234peterparker100% (2)

- BK 291Document108 pagesBK 291Santi Jonas LopezNo ratings yet

- THE FEAST OF TABERNACLES - Lighthouse Library International PDFDocument16 pagesTHE FEAST OF TABERNACLES - Lighthouse Library International PDFEnrique RamosNo ratings yet

- Freest Patricks Day Literacy and Math Prin TablesDocument14 pagesFreest Patricks Day Literacy and Math Prin Tablesبوابة اقرأNo ratings yet

- Social Situation in The French SuburbsDocument13 pagesSocial Situation in The French Suburbsazaleea_roseNo ratings yet

- Subhash Chandra Bose The Untold StoryDocument9 pagesSubhash Chandra Bose The Untold StoryMrudula BandreNo ratings yet

- Continuing Professional DevelopmentDocument20 pagesContinuing Professional DevelopmentLorenz Ardiente100% (1)

- Tinkle Digest MalaVikaDocument17 pagesTinkle Digest MalaVikaHarika Bandaru0% (1)

- ASME B31.8 - 2003 (A)Document192 pagesASME B31.8 - 2003 (A)luigiNo ratings yet