You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5806)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (842)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (589)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Raczynski Edward 3Document1 pageRaczynski Edward 3Роджер МэннерсNo ratings yet

- A - PAUL KRUGMAN - Wonking Out Going Beyond The Inflation HeadlinesDocument5 pagesA - PAUL KRUGMAN - Wonking Out Going Beyond The Inflation HeadlinesРоджер МэннерсNo ratings yet

- Ernest Mandel Some Comments On H. Ticktin's Towards A Political Economy of The USSRDocument5 pagesErnest Mandel Some Comments On H. Ticktin's Towards A Political Economy of The USSRРоджер МэннерсNo ratings yet

- Connectionist Approaches in Economics and Management SciencesDocument269 pagesConnectionist Approaches in Economics and Management SciencesРоджер МэннерсNo ratings yet

- The Structure and Use of The Long-Term Econometric Model W8-D of The Polish EconomyDocument26 pagesThe Structure and Use of The Long-Term Econometric Model W8-D of The Polish EconomyРоджер МэннерсNo ratings yet

- Coronavirus NSW Dossier Lays Out Case Against China Bat Virus ProgramDocument30 pagesCoronavirus NSW Dossier Lays Out Case Against China Bat Virus ProgramРоджер МэннерсNo ratings yet

- Summary of TotalsDocument2 pagesSummary of TotalsDom Minix del RosarioNo ratings yet

- ENT300 BUSINESS PLAN Latest - Doc (Ref)Document61 pagesENT300 BUSINESS PLAN Latest - Doc (Ref)Nor HakimNo ratings yet

- Excerpt of Introduction To Political Economy, Lecture Notes by Daron Acemoglu (PoliticalDocument34 pagesExcerpt of Introduction To Political Economy, Lecture Notes by Daron Acemoglu (PoliticalKaren PerezNo ratings yet

- Product Manual For Plugs and Socket-Outlets For Household and Similar Purposes of Rated Voltage Up To and Including 250 V and Rated Current Up To and Including 16 A According ToDocument13 pagesProduct Manual For Plugs and Socket-Outlets For Household and Similar Purposes of Rated Voltage Up To and Including 250 V and Rated Current Up To and Including 16 A According Toakki3007No ratings yet

- BWN TicketDocument3 pagesBWN TicketSOUMMYA KARMAKARNo ratings yet

- Oleh:: Jutawan Dua LogamDocument42 pagesOleh:: Jutawan Dua LogamMustaffa Bin HashimNo ratings yet

- Sectoral and Regional Analysis of The Ethiopian Investment ScenarioDocument69 pagesSectoral and Regional Analysis of The Ethiopian Investment Scenariokassahun meseleNo ratings yet

- Tutorial 5 - Contract Terms and The Law of Agency (Student)Document4 pagesTutorial 5 - Contract Terms and The Law of Agency (Student)DibyeshNo ratings yet

- Matl Control ProcedureDocument3 pagesMatl Control Procedureimran_amamiNo ratings yet

- Bernard Hodgson (Auth.), Professor Bernard Hodgson (Eds.) - The Invisible Hand and The Common Good - (2004)Document465 pagesBernard Hodgson (Auth.), Professor Bernard Hodgson (Eds.) - The Invisible Hand and The Common Good - (2004)Erickson SantosNo ratings yet

- TallyDocument1 pageTallyIsha PatelNo ratings yet

- Nmat Quantitative Simulations (Mock 2) Section 1. Fundamental OperationsDocument2 pagesNmat Quantitative Simulations (Mock 2) Section 1. Fundamental OperationsRACKELLE ANDREA SERRANONo ratings yet

- Rolando Pacana vs. Atty. Maricel Pascual-Lopez-Case DigestDocument2 pagesRolando Pacana vs. Atty. Maricel Pascual-Lopez-Case Digestrejine mondragonNo ratings yet

- Estimation and Hypothesis Testing: Two Populations: Prem Mann, Introductory Statistics, 7/EDocument75 pagesEstimation and Hypothesis Testing: Two Populations: Prem Mann, Introductory Statistics, 7/ETanvir AhmedNo ratings yet

- Snap Door Lock: TechnopolymerDocument2 pagesSnap Door Lock: TechnopolymerAleksandar PetrusevskiNo ratings yet

- Acct Statement - XX6782 - 23012024Document5 pagesAcct Statement - XX6782 - 23012024Thejesh tejuNo ratings yet

- Catalog Disco D P HardwareDocument10 pagesCatalog Disco D P HardwareBillNo ratings yet

- ABS Ranking Journals 2018 PDFDocument38 pagesABS Ranking Journals 2018 PDFRig VedNo ratings yet

- NR - EE Chapter IDocument15 pagesNR - EE Chapter IGetachew GurmuNo ratings yet

- Production PLANNINGDocument16 pagesProduction PLANNINGFauzi RahmanNo ratings yet

- Quality Control Management AssignmentDocument8 pagesQuality Control Management AssignmentKimmy LyonsNo ratings yet

- Bargarh Handloom and Agro Producer CompanyDocument2 pagesBargarh Handloom and Agro Producer CompanyOrmas OdishaNo ratings yet

- Theory of Supply 1Document16 pagesTheory of Supply 1Chirag JunejaNo ratings yet

- CrawfordQC 1 21 2020Document90 pagesCrawfordQC 1 21 2020dchester smithNo ratings yet

- IE8693 - Production Planning and Control (Ripped From Amazon Kindle Ebooks by Sai Seena)Document342 pagesIE8693 - Production Planning and Control (Ripped From Amazon Kindle Ebooks by Sai Seena)hemnath kamachiNo ratings yet

- Complainant Vs Vs Respondent: Third DivisionDocument3 pagesComplainant Vs Vs Respondent: Third DivisionTrudgeOnNo ratings yet

- MC311 - Size LDocument30 pagesMC311 - Size LuyenmoclenNo ratings yet

- Agribisnis Lorjuk (Solen Grensalis) Dalam Analisis Targeting Dan Positioning Di Kabupaten PamekasanDocument12 pagesAgribisnis Lorjuk (Solen Grensalis) Dalam Analisis Targeting Dan Positioning Di Kabupaten PamekasanZaki AbdilahNo ratings yet

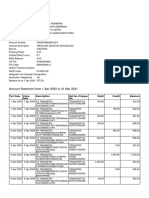

- Account Statement From 1 Apr 2020 To 31 Mar 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument14 pagesAccount Statement From 1 Apr 2020 To 31 Mar 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceHyper GamingNo ratings yet

- M 1 CPRDocument6 pagesM 1 CPRpg797391No ratings yet